- Home

- »

- Advanced Interior Materials

- »

-

Iron Casting Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Iron Casting Market (2026 - 2033)Report]()

Iron Casting Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Gray, Ductile, Malleable), By Application (Automotive, Machinery & Tools, Railways), By Region (North America, Europe, APAC, Central & South America, Middle East & Africa), And Segment Forecasts

Market Size, 2025

$124.2BMarket Estimate, 2026

$131.9BMarket Forecast, 2033

$216.8BCAGR, 2026–2033

7.4%Iron Casting Market Summary

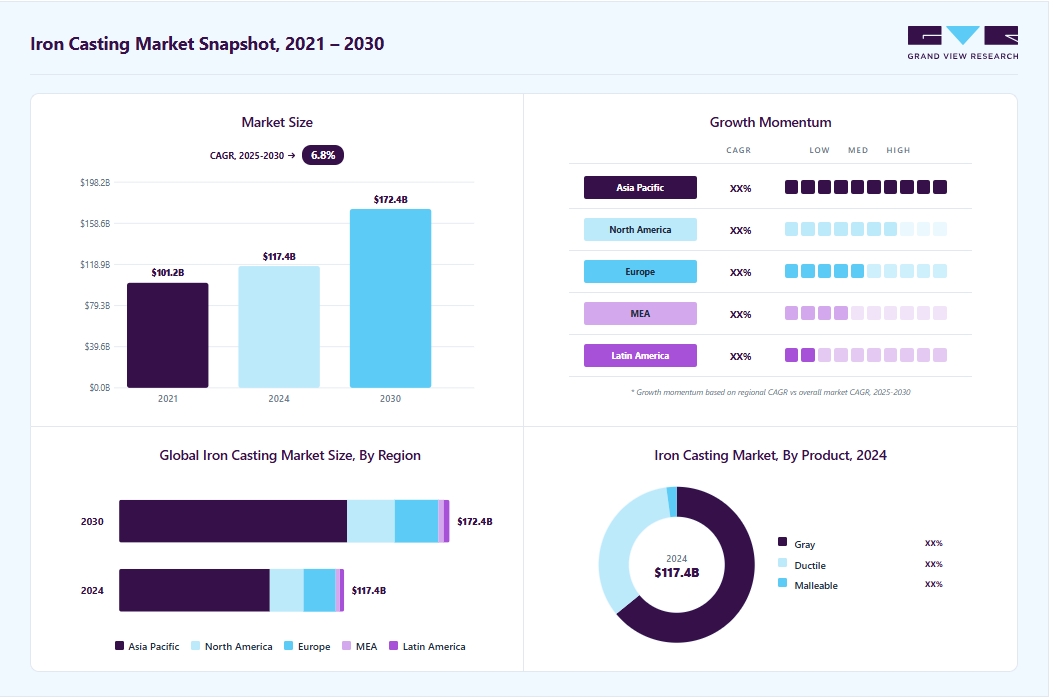

The iron casting market size was estimated at USD 124.2 billion in 2025 and is projected to grow from USD 131.9 billion in 2026 to USD 216.8 billion by 2033, growing at a CAGR of 7.4% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 67.3% in 2025. The market growth is anticipated to be driven by the rising investments in the railway industry worldwide and the demand for iron cast pipes from water-related infrastructure projects and oil & gas.

Key Market Trends & Insights

- By product: Gray iron casting segment led the market with the largest revenue share of 64.1% in 2025.

- By application: Automotive segment led the market with the largest revenue share of 29.4% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (67.3% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 124.2 Billion

- Estimated market size in 2026: USD 131.9 Billion

- Projected market size by 2033: USD 216.8 Billion

- CAGR (2026-2033): 7.4%

In terms of application, the railway is anticipated to register a CAGR of 8.1% in terms of revenue during the forecast period. Rising investments in railway infrastructure are anticipated to positively impact the iron casting market growth over the forecast period. For instance, in April 2025, the 135-year-old rail bridge over the Mithi River in Bandra, Mumbai, one of the last remaining cast-iron screw-pile bridges on Indian Railways, began to be dismantled and replaced, marking the end of the cast-iron era in Indian railway infrastructure. Built in 1888, the bridge featured eight massive cast iron pillars weighing 8-10 tons and extending 15-20 meters deep into the riverbed to anchor the structure. This transition is significant in the context of iron casting, as the bridge’s original screw-pile design exemplified the 19th-century engineering marvels made possible by cast iron technology.")

Cast iron, known for its compressive strength and moldability, was widely used in bridge construction during the industrial era. However, the material’s brittleness and susceptibility to corrosion over time have led to structural vulnerabilities, especially in critical infrastructure like railways. The replacement of the Mithi River Bridge with RCC reflects the broader shift in civil engineering from cast iron toward more durable and resilient materials, ensuring greater safety and longevity for modern rail networks.

Growing concerns among individuals about the potential health risks from non-stick cookware and increasing global demand for toxin-free kitchen cookware have led cast iron cookware manufacturers to increase their production capacity. This is expected to positively influence the growth of the gray cast iron segment of the market over the forecast period. For instance, in September 2024, Caraway announced the launch of its new Enameled Cast Iron Cookware Collection, marking a significant expansion of its non-toxic, design-driven kitchenware offerings. This collection combines traditional cast iron durability and heat retention with a unique three-layer enamel coating that eliminates seasoning and ensures easy cleaning.

Market Dynamics

The iron casting market is primarily driven by strong demand from the automotive, construction, infrastructure, and industrial machinery sectors. Iron castings remain essential for manufacturing engine blocks, brake components, pipes, fittings, pumps, compressors, and heavy equipment due to their high strength, durability, wear resistance, and cost-effectiveness. Rapid urbanization and increasing investments in transportation networks, water distribution systems, railways, and energy infrastructure are further boosting the consumption of iron cast components across both developed and emerging economies.

The growth of the global automotive industry remains one of the most significant drivers for the iron casting market. Iron castings are widely used in the manufacture of engine blocks, cylinder heads, brake drums, flywheels, transmission housings, differential cases, and suspension components due to their strength, durability, wear resistance, and cost-effectiveness. Despite the increasing adoption of lightweight materials in certain vehicle applications, iron continues to play a critical role in heavy-duty vehicles, commercial trucks, off-highway equipment, and performance-oriented automotive components where high mechanical strength and thermal stability are required. As vehicle production expands across developing economies and replacement demand remains strong in mature markets, the consumption of iron cast components continues to increase.

The transition toward advanced mobility solutions is also creating new opportunities for iron casting manufacturers. Growing production of hybrid vehicles, commercial electric vehicles, and heavy transport fleets requires robust cast components for drivetrain systems, motor housings, braking assemblies, and chassis applications. In addition, rising investments in automotive manufacturing facilities across Asia Pacific, North America, and Europe are strengthening demand for high-quality cast iron products. Continuous improvements in casting technologies, including automated molding and precision casting processes, are enabling manufacturers to produce lighter, more complex, and dimensionally accurate components, further supporting the adoption of iron castings across the automotive sector.

Volatility in raw material prices remains a key challenge for the iron casting market, as manufacturers rely heavily on inputs such as pig iron, steel scrap, ferroalloys, coke, and foundry sand. Prices of these materials are influenced by fluctuations in mining output, global trade policies, supply chain disruptions, transportation costs, and changes in industrial demand. Sudden increases in raw material costs can significantly raise production expenses and compress profit margins, particularly for small and medium sized foundries that have limited pricing power. In addition, frequent price fluctuations make long term procurement planning and contract negotiations more difficult, creating uncertainty across the supply chain and potentially affecting investment decisions and production schedules within the iron casting industry.

Infrastructure development across emerging economies presents a significant growth opportunity for the iron casting market. Governments in countries across Asia Pacific, Latin America, the Middle East, and Africa are increasing investments in transportation networks, urban housing, water supply systems, wastewater treatment facilities, industrial parks, and energy infrastructure to support economic growth and urbanization. Iron castings are widely used in applications such as pipes, valves, fittings, manhole covers, drainage systems, railway components, and construction machinery due to their durability, strength, and cost effectiveness. As large scale infrastructure projects continue to expand and industrialization accelerates in developing regions, demand for iron casting products is expected to rise steadily, creating new opportunities for foundries and casting manufacturers worldwide.

Analyst Perspective

The iron casting market continues to benefit from strong demand across automotive, railways, machinery, power generation, and water infrastructure sectors. Growth is increasingly supported by investments in railway modernization, renewable energy projects, and industrial manufacturing expansion, particularly in Asia Pacific. Ductile iron castings are gaining traction due to their superior strength and durability, while gray iron remains the dominant product category because of its cost effectiveness and broad application base. Although lightweight materials such as aluminum are creating competitive pressure in automotive applications, iron castings remain essential for heavy duty and high performance components.

Product Insights & Trends

Based on product, gray iron casting segment led the market with the largest revenue share of 64.1% in 2025. Its growing applications in various industries, including railways, pipes & fittings, propel the segment growth in the iron casting industry. It has graphite particles that precipitate in a spherical form, resulting in high strength and toughness of ductile iron. Ductile cast iron is anticipated to register a CAGR of 7.0% in terms of revenue across the forecast period, ranging from 2025 to 2030.

Ductile cast iron is widely used for manufacturing tractors and implement parts, crankshafts, cylinder heads, switch boxes, electrical fittings, motor frames, flywheels, drive pulleys, work rolls, and circuit breakers. Its microstructure results in more ductile cast iron than gray or white cast iron, making it suitable for producing water and sewage pipes.

Malleable cast iron is widely used in numerous industries, including agriculture, tools and equipment, automotive, and metal and mining. It manufactures electrical fittings and equipment, washers, brackets, hand tools, mining hardware, pipe fittings, farm equipment, bearing caps, steering gear housing, and machine parts.

Application Insights & Trends

Based on application, automotive segment led the market with the largest revenue share of 29.4% in 2025. Engine blocks are usually cast from aluminum alloy or cast iron. Although aluminum offers weight reduction, cast iron is preferred owing to factors such as durability, the ability to resist high internal pressure, more strength, more horsepower, and cost-efficiency. In 2024, the automotive industry held the revenue share of over 29% in 2024 in global iron casting market.

In January 2025, Tata Motors is set to launch Avinya as an all-electric luxury brand positioned above its existing Tata lineup and below Land Rover. The connection to iron casting lies in the manufacturing and structural requirements of premium electric vehicles like Avinya. While the EMA platform emphasizes lightweight materials and advanced battery integration, iron casting remains crucial for specific components that require high strength and durability, such as subframes, suspension mounts, and specific drivetrain elements.

Iron castings are widely used in machinery and tools owing to their good wear resistance, high strength, and good machinability. Although steel is an alternative to cast iron, ductile iron is preferred over steel for manufacturing machine tools as it has good vibration-damping capacity.

Regional Insights

The North America iron casting market is set to experience steady growth, driven by robust economic indicators and substantial investments in infrastructure. For instance, according to the International Monetary Fund (IMF), in 2023, the real GDP growth in North America was estimated at 2.3%, with a slight decline to 2.0% in 2024 and 2025. The U.S. economy is a key contributor to this growth, highlighting the region's commitment to enhancing its economic landscape through significant construction and infrastructure initiatives.

U.S. Iron Casting Market Trends

In the U.S., infrastructure revitalization projects-spurred by the Bipartisan Infrastructure Law-boosted the need for ductile and gray iron castings used in piping, bridges, and heavy machinery. U.S. dominated the North America iron casting market with revenue share of over 84% in 2024. U.S.-based foundries like Waupaca Foundry and Neenah Enterprises ramped production capacity to meet increased domestic demand and reduce dependency on imported components. Simultaneously, the rise of electric vehicle (EV) manufacturing in Michigan and other automotive hubs led to increased investment in precision castings, particularly for lightweight and heat-resistant iron components.

Asia Pacific Iron Casting Market Trends

Asia Pacific dominated the iron casting market with the largest revenue share of 67.3% in 2025. Asia Pacific is one of the world's largest consumers of iron castings. The increasing demand for iron castings in various industries, such as infrastructure and construction, automotive, renewables, machine tooling, and pipes, is anticipated to augment the demand over the forecast period. The countries in the region are investing in improving railway connectivity, which is anticipated to augment the demand for iron castings. For instance, in October 2021, the Vietnam government announced to invest USD 10.5 billion to build and upgrade rail infrastructure across the country by 2030.

China Iron Casting Market Trends

The iron casting market in the China held the largest share in the Asia Pacific region in 2025.

Europe Iron Casting Market Trends

The iron casting industry in Europe is characterized by a strong industrial base, advanced manufacturing technologies, and a significant presence in end user industries such as automotive, construction, and machinery. Countries like Germany, Italy, France, and the UK are leading contributors, with Germany holding a dominant position due to its well-established automotive and engineering sectors. European foundries benefit from stringent quality standards and environmental regulations that have led to the adoption of cleaner and more efficient casting techniques. The emphasis on lightweight and high-strength components, particularly in automotive and transportation, drives innovation in material formulations and process automation.

Key Iron Casting Company Insights

Some of the key players operating in the market include Proterial Ltd., LIAONING BORUI MACHINERY CO., LTD (DANDONG FOUNDRY), and Brakes India.

-

Proterial Ltd., originally founded as Tobata Foundry in 1910, has evolved into a global leader in high-performance materials manufacturing. The company has a rich history marked by key mergers and acquisitions, including collaborations with Hitachi Metals and other specialized firms.

-

Dandong Foundry has nearly 70 years of experience in producing grey iron and ductile iron castings. The company’s annual output reaches 8,000 tons, and 50% of its products are exported to markets such as the U.S., Germany, Australia, UK, Italy, and Japan, reflecting our strong global presence.

Key Iron Casting Companies

The following key companies have been profiled for this study on the iron casting market.

-

Proterial Ltd.

-

LIAONING BORUI MACHINERY CO., LTD (DANDONG FOUNDRY)

-

Brakes India

-

OSCO Industries Inc.

-

Chamberlin

-

Crescent Foundry

-

Georg Fischer Ltd

-

Grupo Industrial Saltillo (GIS)

-

Newby Holdings Limited

-

Castings P.L.C.

-

CALMET

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (e.g. Proterial Ltd., Brakes India, OSCO Industries Inc., Chamberlin)

- Mature participants in the iron casting market primarily focus on high volume production, process standardization, and long term supply relationships with automotive, industrial machinery, construction equipment, railway, and infrastructure sectors.

- These companies operate large foundries equipped with advanced molding, melting, machining, and finishing capabilities to produce a broad range of gray iron, ductile iron, and malleable iron castings.

- Established players possess strong competitive advantages through their extensive manufacturing infrastructure, technical expertise, and long standing relationships with major industrial customers.

- Their large production capacities enable them to achieve economies of scale, optimize raw material procurement, and maintain competitive pricing while delivering consistent product quality.

- Despite their strong market positions, mature players face challenges associated with high energy consumption, labor costs, and environmental compliance requirements.

- Iron casting operations require substantial investments in melting furnaces, emission control systems, and waste management infrastructure.

Emerging & Regional Players (e.g., LIAONING BORUI MACHINERY CO., LTD. (DANDONG FOUNDRY), Crescent Foundry, CALMET)

- Emerging participants in the iron casting market generally focus on specialized casting applications, regional customer bases, and flexible manufacturing capabilities.

- Rather than competing directly with established foundries on production volume, these companies often target niche opportunities involving customized castings, short production runs, and specialized industrial components.

- Emerging companies benefit from operational flexibility and the ability to quickly adapt to changing customer requirements.

- Their smaller organizational structures allow faster decision making, shorter product development cycles, and greater responsiveness to custom casting specifications.

- Emerging participants face significant challenges related to limited production scale, lower financial resources, and reduced purchasing power for raw materials.

- Competing against large established foundries with integrated operations and extensive customer networks can be difficult, particularly in price sensitive market segments.

Recent Developments

-

In June 2022, Brakes India pioneered by collaborating with Volvo Group to produce 'green castings' for engine components. These castings are manufactured using 100% renewable energy and sustainable practices to reduce carbon emissions significantly. The initiative is expected to produce over 180,000 tons of iron castings annually, potentially reducing CO₂ emissions by 210 million tons across the industry if widely adopted. This collaboration underscores the growing emphasis on eco-friendly manufacturing processes in the automotive sector.

-

Crescent Foundry has emerged as a leading cast iron product manufacturer, emphasizing quality and technological advancement. With a production capacity of 2,500 tons per month, the company caters to over 50 countries, supplying products for various sectors, including agriculture, telecom, and infrastructure. Their commitment to innovation is evident in their use of advanced technologies and adherence to international standards, positioning them as a key player in the global market.

Iron Casting Market Report Scope

Report Attribute

Details

Market definition

The market size refers to the total consumption of iron cast components produced from molten iron and utilized across various end-use industries in a single year, including automotive, machinery, pipes and fittings, railways, power generation, and others.

Market size in 2025

USD 124.2 billion

Estimated market size in 2026

USD 131.9 billion

Projected market size by 2033

USD 216.8 billion

Growth rate

CAGR of 7.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, and region.

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S., Canada, Mexico, Germany, UK, France, Italy, Spain, India, China, Japan, South Korea, Brazil, Saudi Arabia, UAE

Key companies profiled

Proterial Ltd., LIAONING BORUI MACHINERY CO., LTD. (DANDONG FOUNDRY), Brakes India, OSCO Industries Inc., Chamberlin, Crescent Foundry, Georg Fischer Ltd., Grupo Industrial Saltillo (GIS), Newby Holdings Limited, Castings P.L.C., CALMET

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Iron Casting Market Report Segmentation

This report forecasts volume & revenue growth at the global, country, and regional levels and provides an analysis of the latest trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global iron casting market report based on product, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Gray Cast Iron

-

Ductile Cast Iron

-

Malleable Cast Iron

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Automotive

-

Machinery & tools

-

Pipes & fittings

-

Railways

-

Power generation

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

Italy

-

UK

-

Russia

-

Türkiye

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Indonesia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

-

Research Methodology

The iron casting market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each iron casting segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Product

Revenue Capture Definition

Gray

Gray iron casting refers to cast iron products manufactured with a graphite microstructure in the form of flakes, giving the fractured surface a gray appearance.

Ductile

Ductile iron casting, also known as nodular or spheroidal graphite iron casting, consists of cast iron in which graphite is present as spherical nodules rather than flakes.

Malleable

Malleable iron casting refers to cast iron products produced by heat treating white iron castings to transform brittle carbides into temper carbon nodules. This process enhances ductility, toughness, and shock resistance.

Application

Revenue Capture Definition

Automotive

This segment includes iron castings used in passenger vehicles, commercial vehicles, and off highway equipment.

Machinery & tools

Machinery and tools applications comprise iron castings used in industrial equipment, machine tools, pumps, compressors, agricultural machinery, and construction equipment.

Pipes & fittings

This segment covers iron castings utilized in water distribution systems, sewage networks, oil and gas pipelines, and industrial fluid handling systems.

Railways

Railway applications include iron castings used in locomotives, freight wagons, passenger coaches, braking systems, track components, and infrastructure equipment.

Power generation

This segment encompasses iron castings employed in thermal, hydroelectric, wind, and other power generation facilities.

Others

The others segment includes iron castings used across diverse industries such as marine, mining, construction, aerospace support equipment, consumer goods, and municipal infrastructure.

Estimation Model

Layer Name

Key Question

Description

Metal Component Demand Base Layer

What forms the demand base?

Identify global demand for cast metal components across major end use industries including automotive, construction, industrial machinery, agriculture, railways, mining, energy, and heavy equipment. Assess production volumes of equipment and machinery that utilize iron castings. This layer establishes the total addressable demand for iron casting products.

Iron Casting Application Penetration Layer

Where are iron castings utilized?

Estimate the penetration of iron castings across key applications such as engine blocks, brake components, pipes and fittings, pumps, valves, machine tools, transmission systems, construction equipment, and infrastructure products. Analyze adoption trends across developed and emerging manufacturing economies.

Casting Consumption Intensity Layer

How much iron casting is consumed?

Analyze average iron casting consumption across end use sectors based on production output, equipment size, component complexity, and replacement rates. Evaluate the utilization of gray iron, ductile iron, malleable iron, and other cast iron grades. Consumption intensity varies according to industrial activity, infrastructure investments, and engineering requirements.

Revenue Layer

How is market revenue generated?

Market revenue is quantified through the production and sale of iron castings supplied to automotive, industrial, construction, energy, and infrastructure sectors. Revenue is generated from the sale of finished cast components and customized casting solutions. Market value is influenced by casting volumes, raw material prices, manufacturing costs, product specifications, and demand from downstream industries.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Europe Iron Casting Market Assessment

A customized study focused specifically on the European gray and ductile iron casting market, covering country-level demand analysis, production trends, end-use industries, trade dynamics, and competitive landscape across major European economies.

Helped the North America-based client evaluate market opportunities within Europe, understand regional demand-supply dynamics, and support strategic expansion and sourcing decisions in the European iron casting industry.

Global Iron Casting Market Segmentation & End-Use Analysis

A market study covering industry value chain analysis, regulatory framework, market dynamics, and detailed product outlook for gray, ductile, and malleable cast iron. The study also included historical and forecast analysis across key application segments such as automotive, machinery & tools, pipes & fittings, railways, and power generation.

A market study covering industry value chain analysis, regulatory framework, market dynamics, and detailed product outlook for gray, ductile, and malleable cast iron. The study also included historical and forecast analysis across key application segments such as automotive, machinery & tools, pipes & fittings, railways, and power generation.

Opportunity Assessment

Identification of high growth opportunities across automotive production, industrial machinery expansion, railway modernization projects, water infrastructure development, renewable energy equipment manufacturing, and power generation investments.

Enabled prioritization of high return growth segments and emerging regional opportunities. Supported long term investment planning, foundry modernization initiatives, and strategic business development decisions aligned with evolving industrial requirements.

Frequently Asked Questions About This Report

The iron casting market is expected to grow at a compound annual growth rate of 7.4% from 2026 to 2033 to reach USD 216.8 billion by 2033.

North America is anticipated to register the fastest CAGR over the forecast period.

Based on product, gray iron cast accounted for the largest revenue share of 64.1% in 2025.

The key factor that is driving the growth of the global iron casting market is resurgent demand from end-use sectors such as machinery and tools, railway, and energy infrastructure. Also, growing investments in the railway industry worldwide, coupled with rising demand for iron cast pipes from water-related infrastructure projects and the oil and gas sector, are driving demand for cast iron.

Asia Pacific dominated the market with revenue share of 67.3% in 2025.

Based on application, automotive accounted for the largest revenue share of 29.4% in 2025.

Some of the key players operating in the iron casting market are Proterial Ltd., LIAONING BORUI MACHINERY CO., LTD. (DANDONG FOUNDRY), Brakes India, OSCO Industries Inc., Chamberlin, Crescent Foundry, Georg Fischer Ltd., Grupo Industrial Saltillo (GIS), Newby Holdings Limited, Castings P.L.C., CALMET.

The iron casting market size was valued at USD 124.2 billion in 2025 and is expected to reach USD 131.9 billion in 2026.

China dominated the Asia Pacific iron casting market with a revenue share of 57.3% in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.