- Home

- »

- Healthcare IT

- »

-

Laboratory Informatics Market Size Report, 2026-2033GVR Report cover

![Laboratory Informatics Market (2026 - 2033)Report]()

Laboratory Informatics Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (LIMS, ELN, SDMS, LES, EDC & CDMS, CDS, ECM), By Delivery Mode (Web-based, On-Premise, Cloud Based), By Component, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$4.1BMarket Estimate, 2026

$4.3BMarket Forecast, 2033

$5.9BCAGR, 2026–2033

4.9%Laboratory Informatics Market Summary

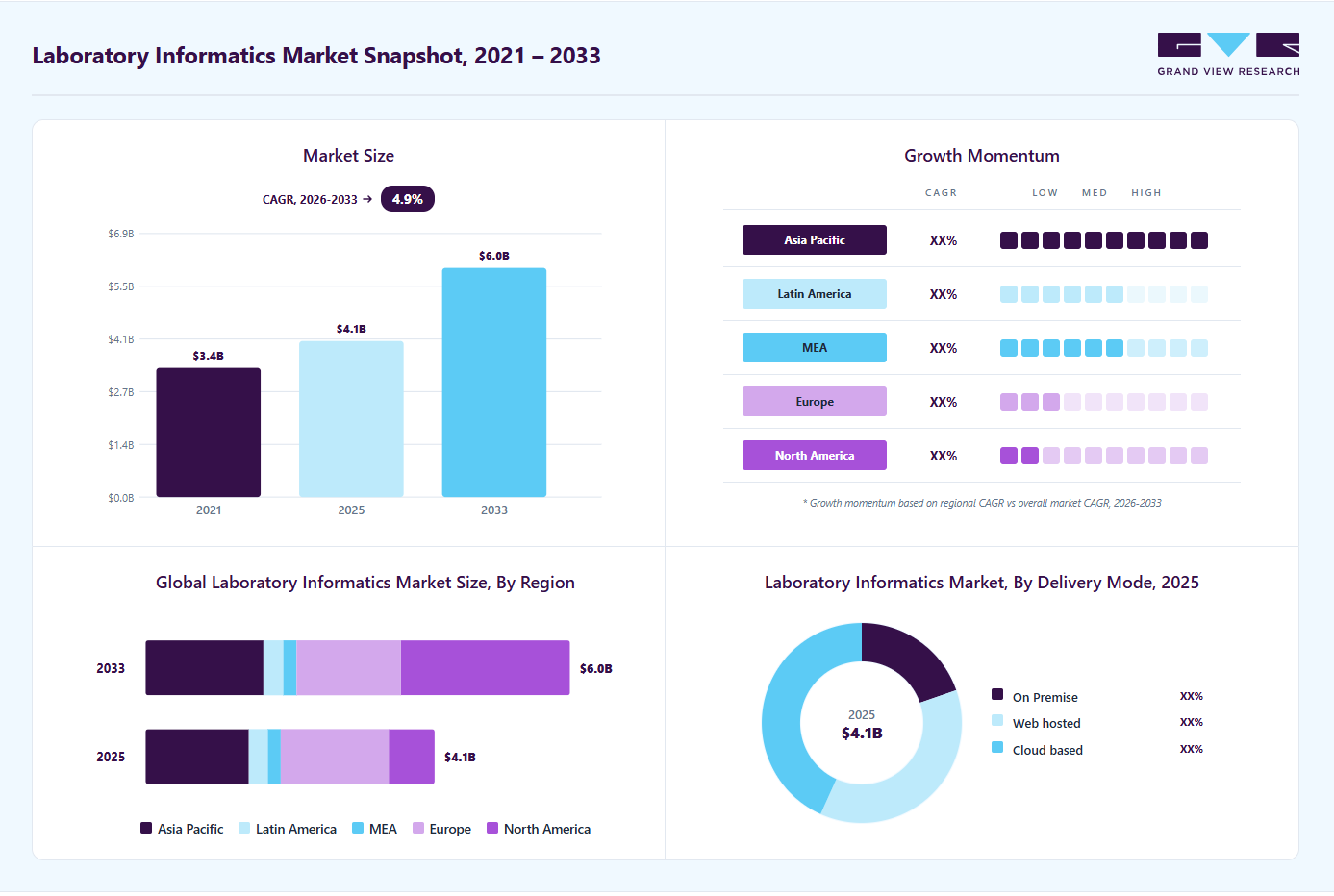

The global laboratory informatics market size was valued at USD 4.1 billion in 2025 and is expected to grow from USD 4.3 billion in 2026 to USD 5.9 billion by 2033, at a CAGR of 4.9% from 2026 to 2033. North America held the largest revenue share of 42.7% of the global market in 2025. Rising demand for laboratory automation is driving adoption, fueled by advancements in molecular genomics, genetic testing, and personalized medicine.

Key Market Trends & Insights

- By product: Laboratory information management systems (LIMS) segment held the largest market share of 51.2% in 2025.

- By component: Services segment held the largest market share of 58.5% in 2025.

- By delivery mode: Web-based segment held the largest market share of 43.3% in 2025.

- By end use: life sciences segment held the largest revenue share of 28.9% in 2025

Regional Highlights

- Largest regional market: North America (42.7% market share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 4.1 Billion

- Estimated market size in 2026: USD 4.3 Billion

- Projected market size by 2033: USD 5.9 Billion

- CAGR (2026-2033): 4.9%

The shift toward cancer genomics and increased patient engagement further accelerates this trend. Moreover, research labs are increasingly adopting cloud, mobile, and voice technologies, boosting demand for lab informatics solutions. The adoption of laboratory informatics solutions is increasingly expanding across healthcare, pharmaceuticals, biotechnology, and contract research organizations, driven by the need for enhanced efficiency, error reduction, and data management. Laboratory information systems are increasingly used in biobanks, academic research institutes, and CROs due to their advantages, including process optimization, regulatory compliance, intellectual property protection, reduced throughput time, and paperless data management.

")

Moreover, the rise of advanced technologies such as artificial intelligence and robotics for process automation in healthcare has made laboratory operations more reproducible and efficient, allowing faster experiment setup, execution, and analysis. High-throughput systems enable rapid evaluation of experimental results, boosting overall laboratory productivity. In addition, advancements in laboratory equipment are accelerating the transition from manual data evaluation to automated methods, improving accuracy and speed. For instance, in January 2026, SandboxAQ launches OpenFold3, an open-source AI model for pharma R&D. It enables rapid, structure-free binding affinity prediction, addressing early-stage drug discovery bottlenecks.

Furthermore, laboratories are increasingly seeking to adopt advanced technology infrastructure to support new initiatives, remove inefficiencies, and improve their service offerings. Among products, LIMS has the highest growth potential and ability to capture the market followed by Electronic Lab Notebooks (ELN) and Enterprise Content Management (ECM). Other products have comparatively low growth potential and the ability to gain market share. The high growth potential and market-capturing ability of LIMS can be attributed to the growth of value-based healthcare and increase in demand for new interoperability & information sharing/reporting requirements.

Case Study

Problem Statement: The Garvan Institute of Medical Research, a leading Australian medical research organization, faced challenges in managing the vast amounts of data generated by its genomics research. To address this, the institute implemented a comprehensive laboratory informatics solution from Autoscribe Informatics.

-

Garvan's researchers were generating massive volumes of genomic data that needed to be efficiently stored, organized, and accessed.

-

The institute's previous systems were unable to keep up with the growing data demands, leading to inefficiencies and delays in research.

-

Garvan needed a flexible, scalable informatics platform that could integrate with its existing laboratory workflows and instrumentation.

Solution: Garvan deployed Autoscribe's Matrix Gemini LIMS to centralize its data management and streamline research operations. The LIMS provided the institute with the following capabilities:

-

Automated sample tracking and management

-

Seamless integration with lab instruments and equipment

-

Customizable workflows to support Garvan's unique research processes

-

Robust data storage and retrieval to facilitate collaboration & analysis

Outcomes

-

The implementation of the Matrix Gemini LIMS has enabled Garvan to:

-

Improve the efficiency and productivity of its genomics research

-

Enhance data integrity and traceability through automated sample management

-

Facilitate collaboration among researchers by providing centralized access to data

-

Achieve greater visibility and control over its laboratory operation

Analyst Insights

The case study of the Garvan Institute of Medical Research in Australia illustrates the transformative impact that laboratory informatics can have on academic research organizations. By implementing a comprehensive LIMS solution, the institute was able to streamline its genomics research, enhance data integrity, and facilitate collaboration among its researchers. The growing demand from such organizations is contributing to market growth.

Market Concentration & Characteristics

The chart below illustrates the relationship between market concentration, industry characteristics, and industry participants. The x-axis represents the level of industry concentration, ranging from low to high. The y-axis represents various industry characteristics, including industry competition, impact of regulations, level of partnerships & collaborations activities, degree of innovation, and regional expansion. For instance, the laboratory informatics market is fragmented, with many service providers entering the market. The degree of innovation is high, and the level of mergers & acquisitions activities is moderate. The impact of regulations on the industry is high, and the regional expansion of the industry is moderate.

The degree of innovation in the industry is high. The market is experiencing significant innovation as numerous providers introduce new products to meet demand for scientific data integration solutions in various industries. For instance, in May 2024, Thermo Fisher Scientific Inc. launched Applied Biosystems Axiom BloodGenomiX Array and Software. This innovative solution is designed for precise blood genotyping in clinical studies.

The level of merger & acquisition in the industry is moderate due to a rise in acquisition of emerging players by major players to increase their capabilities, expand product portfolios, and improve competencies. For instance, in July 2025, Clinisys acquired Orchard Software from Francisco Partners. This acquisition is likely to deliver comprehensive, scalable cloud-based informatics for healthcare, life sciences, public health, physician offices, reference labs, and veterinary clinics.

"We are excited to welcome Orchard to the Clinisys family... expanding with Orchard’s proven solution in the physician office, reference, and veterinary laboratory space was a clear decision for us. Together, we can better serve the entire spectrum of lab and diagnostic customers by enabling healthier and safer communities worldwide."

- Michael Simpson, Clinisys's CEO,

The impact of regulations on the market is high. The primary objective of a laboratory is to ensure the generation of high-quality and reliable experimental data that complies with the industry's regulatory guidelines. The combination of technological advancements, stringent regulatory needs, and increasing commercial pressures has resulted in the rapid generation of vast amounts of data from various aspects, including research and development, quality assurance, and manufacturing. This is creating significant challenges for data management processes and conventional documentation requirements, particularly in regulated environments such as the life sciences sector.

The level of regional expansion in industry is moderate due to increasing demand for laboratory informatics solutions in developing countries. For instance, in February 2024, LabWare opened a new office located in central Seoul, Korea. This expansion represents a significant step forward in its global mission to deliver world-leading laboratory informatics solutions to customers worldwide.

Product Insights

Based on product, the laboratory information management systems (LIMS) segment dominated the market with revenue share of 51.22% in 2025. In addition, this segment is anticipated to grow at the fastest CAGR during the forecast period. This is attributed to increasing demand for efficient data management and automation in laboratories across various industries, such as healthcare, life sciences, food, beverage and agriculture industries, environmental testing, etc. LIMS solutions offer comprehensive functionalities, including sample tracking, data analysis, compliance with regulatory standards, and integration with laboratory instruments, which enhances productivity, accuracy, & data integrity.

The Enterprise Content Management (ECM) segment is anticipated to grow significantly over the forecast year. The adoption of ECM is increasing over time as it offers integrated and comprehensive solutions to meet the growing challenges in the healthcare industry. ECM offers a centralized approach to capture, create, organize, access, and analyze an organization’s entire ecosystem of media, knowledge assets, and electronic documents. The services offered by companies for ECM are consultation, design, implementation, and maintenance of these software solutions.

Delivery Mode Insights

Based on delivery mode, the cloud-based segment dominated the market with the largest revenue share of 43.25% in 2025. The cloud-based segment is anticipated to grow at the fastest growth rate over the forecast year. This is due to its affordability, scalability, dependability, and sophisticated capabilities that meet the expanding storage and computational demands in healthcare. The rise of cloud laboratories offers a chance to leverage AI and machine learning to refine experimental methods and improve data accuracy with algorithms. For instance, in October 2023, Sapio Sciences introduced Sapio Jarvis, the first scientific data cloud specifically designed for scientists. Sapio Jarvis consolidates various lab data and integrates it with scientific context to speed up drug development processes by utilizing advanced analytics & artificial intelligence.

Component Insights

Based on component, the services segment accounted for the largest revenue share of 58.50% in 2025. In addition, this segment is expected to grow at the fastest CAGR during the forecast period. This growth is attributed to the need for a flexible, expandable, and easy-to-use service-oriented LIMS for efficient data and process management. Large pharma and research labs outsource advanced analytics due to internal skill and resource shortages. The lab informatics market provides services such as compliance, social analytics, manufacturing analytics, predictive and preventive maintenance, and benchmarking.

The software segment is anticipated to grow at the fastest growth rate over the forecast year due to the availability of technologically advanced software, such as SaaS, which offers effective information management solutions for laboratories. The software offered for laboratory informatics can perform critical functions such as data capture, storage, interpretation, and analysis. Periodic upgradation of this software is necessary to coordinate with the latest analytics methods.

End Use Insights

Based on end use, the life sciences segment dominated the market with revenue share of 28.93% in 2025. The demand for laboratory informatics is increasing in the life sciences industry to develop innovative products, improve product quality, and operational efficiency. Laboratory informatics systems allow effective management of large amount of data and break down research & discovery silos. Increasing technological advances in healthcare owing to rising R&D in the field of medicine is anticipated to fuel the demand for LIMS. Increasing adoption of LIMS in hospital and research labs due to its growing application scope for patient engagement, workflow management, billing, patient health information tracking and quality assurance is expected to augment the growth.

The CROs segment is anticipated to grow at the fastest growth rate over the forecast year. The demand for efficient data management and regulatory compliance drives CROs to adopt advanced laboratory informatics solutions, such as ELN, LIMS, and SDMS. These technologies enable CROs to streamline workflows, ensure data integrity, enhance collaboration, and expedite the drug development process. With growth in the life sciences sector, the reliance on CROs for high-quality, cost-effective research solutions is also increasing.

Regional Insights

North America Laboratory Informatics Market Trends

North America region held the largest share of 42.68% in 2025. Rapid technological advancements, including measurement, digital, communication, and transportation technologies, have significantly impacted how clinical laboratories are organized, staffed, and equipped. Moreover, the increasing prevalence of point-of-care and critical care testing has necessitated real-time data availability and seamless information management to support clinical decision-making. Such factors are expected to propel market growth further.

U.S. laboratory informatics market held the largest share in 2025 due to technology advancement, regulatory demands, and complex operations. Innovations such as cloud computing, AI, and ML are revolutionizing data analysis and efficiency, essential for sectors from healthcare to environmental testing for enhanced decision-making and faster drug development. Moreover, regulatory and reimbursement dynamics in the U.S. strongly influence adoption. Compliance with CLIA, HIPAA, and FDA requirements requires robust informatics systems that ensure data security, validation, and accurate reporting.

Europe Laboratory Informatics Market Trends

Europe laboratory informatics market is anticipated to grow significantly due to the increasing automation and digitalization of laboratory data, substantial R&D activities, the requirement for efficient and scalable management across various industries, and technological advancements. For instance, in August 2025, ABN AMRO partnered with Infosys to develop a GenAI-powered, cloud-native solution for enterprise content management. Using Azure RAG, it automates complex document classification/extraction from billions of files, cutting processing time/costs, boosting compliance, and enhancing employee experience without manual downloads.

The laboratory informatics market in the UK is driven by healthcare digital transformation initiatives, rising diagnostic demand, and the modernization of laboratory services within the National Health Service (NHS). In addition, increasing adoption of genomic medicine, digitization of pathology, and the expansion of centralized laboratory networks are driving demand for integrated LIS and LIMS platforms.

Germany laboratory informatics market held the largest share in 2025, owing to the increasing laboratory automation, digitalization of laboratory data, and stringent regulations across industries. Moreover, the growing mergers, acquisitions, partnerships, and collaborations among key players to expand capabilities and market reach.

Asia Pacific Laboratory Informatics Market Trends

Asia Pacific laboratory informatics market is expected to witness the fastest growth over the forecast period with the rising demand from pharmaceutical manufacturers seeking to improve efficiency and reduce costs. The presence of numerous CROs in developing countries such as India and China is expected to boost demand, complemented by the adoption of advanced technology-based laboratory information systems. Increased partnerships and collaborations among key regional players to drive market growth in the forecast period. For instance, in April 2024 , Autoscribe Informatics, Inc. announced the expansion of its customer network in Asia Pacific by opening an office in Australia. This move supported the company’s growing LIMS business and enabled it to better serve the region in digitalizing laboratory information

China laboratory informatics marketheld a significant market share in 2025, driven by the government's support for e-health services and national electronic health records. Technological advancements, such as AI, automation, and blockchain, are further enhancing lab informatics by improving predictive capabilities, data analytics, and patient outcomes.

India laboratory informatics marketis driven by the rising prevalence of chronic diseases, increasing healthcare digitization, and growing focus on regulatory compliance. Moreover, strong presence of pharmaceutical and biotechnology companies and increasing penetration of AI in healthcare and life science sector drives market growth.

Latin America Laboratory Informatics Market Trends

Latin America laboratory informatics market is anticipated to grow significantly due to a growing demand for advanced healthcare amid an aging population and rising chronic diseases. Government and private sector investments, along with technological advancements, are driving the market, with significant growth expected in LIMS and ELN systems as awareness of laboratory automation's importance increases.

Brazil laboratory informatics market is anticipated to grow significantly due to the rising per capita income, increasing government medical & healthcare spending, improving access to private healthcare facilities, and fast-growing healthcare R&D.

Middle East & Africa Laboratory Informatics Market Trends

Middle East & Africa laboratory informatics market is expected to grow significantly due to the government is implementing laboratory informatics systems to enhance patient care, with hospitals increasingly adopting these technologies. Market growth is driven by healthcare sector improvements, automation integration in labs, and increased public-private collaborations.

South Africa laboratory informatics marketis anticipated to grow significantly due to significant investments and government initiatives in modernizing laboratory operations aim to improve healthcare outcomes and data accuracy, addressing the rising burden of infectious and non-communicable diseases.

Key Laboratory Informatics Company Insights

Key players operating in the population health management market are undertaking various initiatives to strengthen their market presence and increase the reach of their products and services. Strategies such as new product launches and partnerships are playing a key role in propelling the market growth.

Key Laboratory Informatics Companies:

The following key companies have been profiled for this study on the laboratory informatics market.

- Abbott

- Agilent Technologies, Inc.

- IDBS

- LabLynx, Inc.

- LabVantage Solutions, Inc.

- LabWare

- McKesson Corporation

- PerkinElmer, Inc.

- Thermo Fisher Scientific, Inc.

- Waters

- Computing Solutions, Inc.

- CloudLIMS.com (LabSoft LIMS)

- Ovation

- LABTRACK

- AssayNet Inc.

Recent Developments

-

In January 2026, Sapio Sciences launched a partner ecosystem for ELaiN, its third-generation AI lab notebook (AILN). Integrations with third-party scientific apps enable seamless access to specialist tools like molecular docking, data analytics, and codon optimization within workflows. Natural language prompts drive AI coordination, ensuring compliance, security, and data governance in biopharma R&D.

-

In September 2025, LabWare released Clinical Health Solution 5.06 for clinical/public health labs. Key enhancements include out-of-box billing, result dashboards, send-out tracking, contact management, data dashboards, role definitions, search functions, and HL7 flexibility.

"Clinical Health 5.06 reflects our ongoing commitment to drive improved clinical laboratory operational efficiency with innovative LIMS capabilities. This version was released utilizing LabWare's comprehensive automated testing tool which allowed for a more rigorous and expanded validation testing footprint and will streamline testing for future versions."

- said Ed Krasovec, Director of Clinical Solutions at LabWare.

-

In February 2024, LabVantage Solutions, Inc., a provider of laboratory informatics solutions, now offers its advanced analytics, semantic search (AILANI), and purpose-built LIMS solutions within an integrated, digitally native ecosystem tailored to support R&D laboratory processes. This ecosystem enhances efficiency, productivity, decision-making, & collaboration and reduces operational costs.

-

In November 2023, Thermo Fisher Scientific Inc. partnered with Flagship Pioneering, a bioplatform innovation firm. This strategic partnership aims to develop and expand multiproduct platforms quickly, create new platform companies focusing on innovative biotech tools & capabilities, and broaden their existing supply relationship across life science tools, diagnostics, & services.

-

In December 2023, PerkinElmer Inc. acquired Covaris, a company that develops solutions to drive life science innovations. This acquisition is intended to boost Covaris’ growth and expand PerkinElmer’s life sciences portfolio in the rapidly growing diagnostics market.

-

In September 2023, LabWare opened an office in Wageningen, The Netherlands. With this location, the company expanded its presence in six continents, with a network of over 40 offices.

-

In May 2023, FreeLIMS introduced an updated cloud-based LIMS with multiple modules and enhanced functionality to support automation, data management, and regulatory compliance, further driving adoption of laboratory informatics solutions in modern research environments.

Laboratory Informatics Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 4.1 billion

Estimated Market size in 2026

USD 4.3 billion

Projected Market size by 2033

USD 5.9 billion

Growth rate

CAGR of 4.9% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, delivery mode, component, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; China; Japan; India; South Korea; Australia; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait

Key companies profiled

Abbott; Agilent Technologies, Inc.; IDBS; LabLynx, Inc.; LabVantage Solutions, Inc.; LabWare; McKesson Corporation; PerkinElmer, Inc.; Thermo Fisher Scientific, Inc.; Waters; Computing Solutions, Inc.; CloudLIMS.com (LabSoft LIMS); Ovation; LABTRACK; AssayNet Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Laboratory Informatics Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global laboratory informatics market report based on product, delivery mode, component, and region.

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Laboratory Information Management Systems (LIMS)

-

Electronic Lab Notebooks (ELN)

-

Scientific Data Management Systems (SDMS)

-

Laboratory Execution Systems (LES)

-

Electronic Data Capture (EDC) & Clinical Data Management Systems (CDMS)

-

Chromatography Data Systems (CDS)

-

Enterprise Content Management (ECM)

-

-

Delivery Mode Outlook (Revenue, USD Million, 2021 - 2033)

-

Web-based

-

On-Premise

-

Cloud Based

-

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Software

-

Services

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Life Sciences

-

Pharmaceutical and Biotechnology Companies

-

Biobanks/Biorepositories

-

Contract Services Organizations

-

Molecular Diagnostics & Clinical Research Laboratories

-

Academic Research Institutes

-

-

CROs

-

Chemical Industry

-

Food & Beverage and Agriculture Industries

-

Environmental Testing Laboratories

-

Petrochemical Refineries and Oil & Gas Industry

-

Other Industries (Forensics and Metal & Mining Laboratories)

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

North America dominated with a 42.7% market share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The global laboratory informatics market size was estimated at USD 4.1 billion in 2025 and is expected to reach USD 4.3 billion in 2026.

The global laboratory informatics market is expected to grow at a compound annual growth rate of 4.9% from 2026 to 2033 to reach USD 5.9 billion by 2033.

The laboratory information management systems (LIMS) segment dominated the market with revenue share of 51.22% in 2025. This is attributed to increasing demand for efficient data management and automation in laboratories across various industries, such as healthcare, pharmaceuticals, biotechnology, and environmental testing.

The cloud-based segment dominated the market with revenue share of 43.25% in 2025. This is due to its affordability, scalability, dependability, and sophisticated capabilities that meet the expanding storage and computational demands in healthcare. The rise of cloud laboratories offers a chance to leverage AI and machine learning to refine experimental methods and improve data accuracy with algorithms.

Key players operating in the laboratory informatics market include Abbott; Agilent Technologies, Inc.; IDBS; LabLynx, Inc.; LabVantage Solutions, Inc.; LabWare; McKesson Corporation; PerkinElmer, Inc.; Thermo Fisher Scientific, Inc.; Waters; Computing Solutions, Inc.; CloudLIMS.com (LabSoft LIMS); Ovation; LABTRACK; AssayNet Inc.

The services segment held the largest revenue share of 58.50% in 2025, while the software segment is anticipated to grow at the fastest CAGR over the forecast period.

About the Author(s)

Healthcare IT Research Team

Healthcare · Healthcare ITThis report was authored by the healthcare it research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the healthcare it segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.