- Home

- »

- Electronic Devices

- »

-

Laptop Market Size, Share And Growth Report, 2026-2033GVR Report cover

![Laptop Market (2026 - 2033)Report]()

Laptop Market (2026 - 2033)

Size, Share, & Trends Analysis Report By Type (Traditional Laptop, 2-in-1 Laptop), By Screen Size (Upto 10.9", 13" To 14.9", 15.0" To 16.9"), By Price, By End Use (Personal, Business, Gaming), By Region, and Segment Forecasts

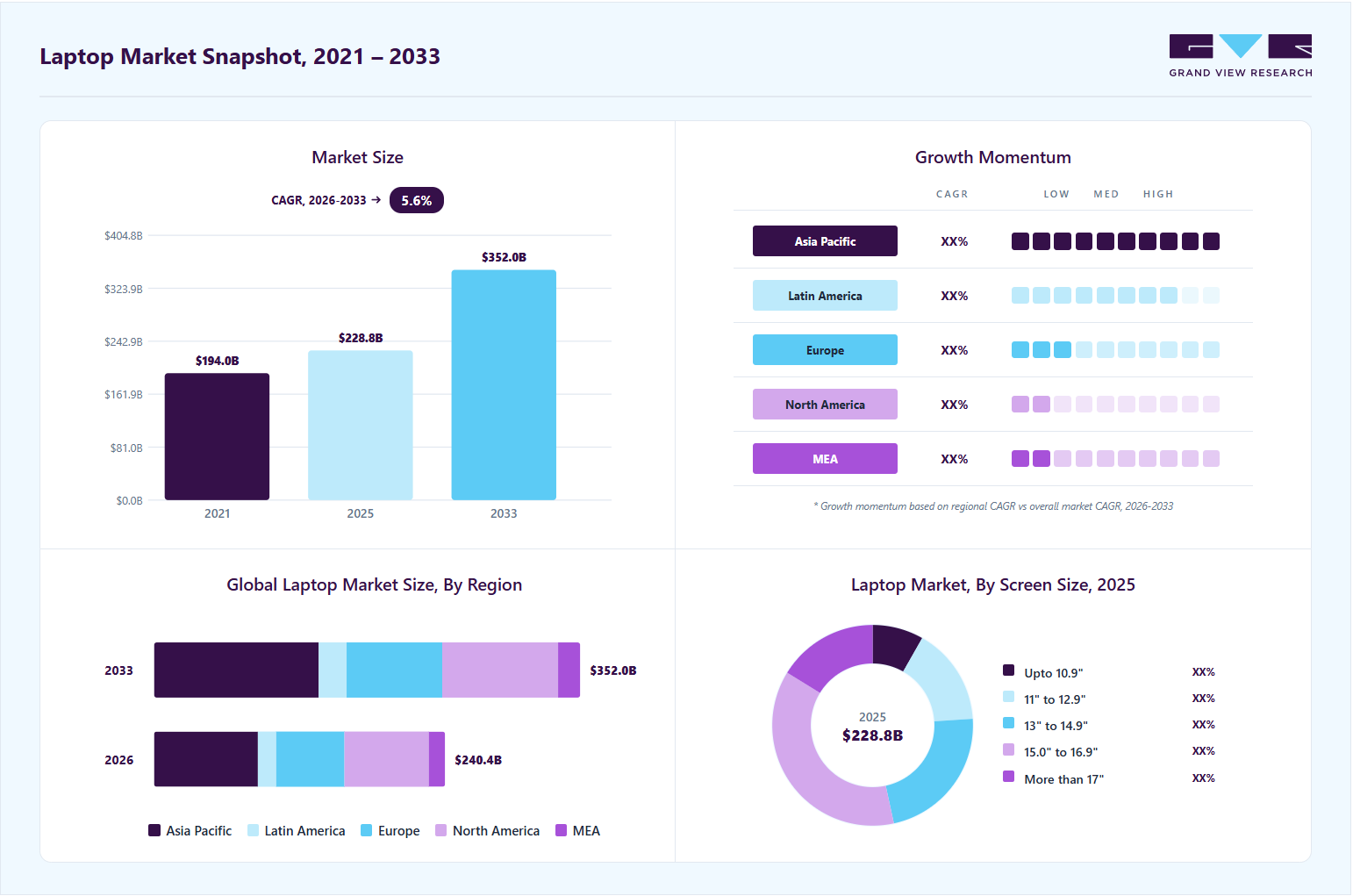

Market Size, 2025

$228.8BMarket Estimate, 2026

$240.4BMarket Forecast, 2033

$352.0BCAGR, 2026–2033

5.6%Laptop Market Summary

The global laptop market size was valued at USD 228.8 billion in 2025 and is projected to grow from USD 240.4 billion in 2026 to USD 352.0 billion by 2033, at a CAGR of 5.6% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 35.2% in 2025. The market is continuously expanding owing to rising disposable incomes, expanding internet connectivity, and consumers' growing inclination toward advanced laptops for their system performance and design.

Key Market Trends & Insights

- By type: Traditional laptop segment held the largest market share of 76.3% in 2025.

- By screen size: 15.0" to 16.9" segment held the largest market share in 2025.

- By price: USD 1501 to USD 2000 segment held the largest market share of 34.4% in 2025.

- By end use: Business segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (35.2% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 228.8 Billion

- Estimated market size in 2026: USD 240.4 Billion

- Projected market size by 2033: USD 352.0 Billion

- CAGR (2026-2033): 5.6%

Improvements in the price-to-performance ratio and longer hardware lifespans are contributing to the growing adoption of laptops among consumers, particularly in developing countries such as India and Brazil. As laptops become more affordable while delivering stronger performance capabilities, consumer demand continues to increase across both personal and professional applications. In addition, the market is experiencing strong sales volumes due to rising demand for gaming laptops, high-speed graphics cards, and ultra-thin laptop designs that offer enhanced portability and performance. According to a 2025 study by the International Telecommunication Union, 74% of the global population uses the internet. The expanding internet user base has become a major driver of growth in the laptop industry, as increased digital connectivity worldwide drives demand for computing devices. This trend is also positively influencing related sectors, including the gaming laptop industry, laptop accessories market, and laptop battery market, creating broader growth opportunities across the laptop ecosystem.Several companies are focusing on developing affordable laptops to address consumer demand in countries with lower purchasing power, which is expected to attract a broader customer base and support growth in the laptop industry, including the expansion of the B2B laptop PC market. Affordable pricing strategies, combined with improving device capabilities, are helping manufacturers increase market penetration across emerging economies and price-sensitive consumer segments. For instance, in March 2026, Apple introduced the MacBook Neo, a budget-focused laptop aimed at the affordable laptop segment. The device offers Apple silicon performance, a Liquid Retina display, and all-day battery life, with a starting price of USD 599. The launch aims to make premium laptop experiences more accessible by delivering strong performance and modern design at a lower price point. This development is expected to intensify competition in the affordable laptop segment, encouraging manufacturers to improve product features while maintaining competitive pricing. It may also accelerate the transition toward premium capabilities within lower-priced categories, further strengthening innovation across the laptop industry as a whole.

")

In addition, digital transformation is creating a significant impact on the global education sector, changing traditional learning and training methods. Digital classrooms continue to gain wider acceptance as educational institutions increasingly adopt technology-driven learning environments. Concepts such as Bring Your Own Device (BYOD), Artificial Intelligence (AI), and personalized learning approaches are reshaping teaching, learning, and assessment processes. These advancements are creating more immersive and interactive educational experiences while expanding students’ access to visual and technology-enabled learning tools.

Overall, the global laptop industry is expected to witness steady growth, supported by increasing internet penetration, accelerating digital transformation, and rising demand for both high-performance and affordable laptops. Expanding adoption across education, gaming, enterprise, and personal use segments is further strengthening market development, while continued growth in the gaming laptop industry, laptop accessories market, laptop battery market, and B2B laptop PC market is creating broader opportunities across the laptop ecosystem.

Market Dynamics

Drivers - AI-Driven Processor Innovation and Rising Demand for High-Performance Computing in Laptops

The laptop industry is being strongly driven by rapid advancements in artificial intelligence (AI), increasing demand for high-performance computing, and the shift toward hybrid work. Consumers and enterprises are now prioritizing laptops that offer faster processing, better energy efficiency, and built-in AI capabilities to support tasks such as automation, content creation, real-time analytics, and enhanced security. In addition, growing adoption of cloud-based applications and AI-enabled software is pushing manufacturers to integrate more powerful CPUs and NPUs (neural processing units), making laptops more intelligent and efficient than traditional devices.

For instance, in January 2026, AMD introduced Ryzen AI 400 and PRO 400 processors for laptops, enhancing AI-powered Copilot+ PCs with up to 60 NPU TOPS. It also launched Ryzen AI Max+ for premium notebooks, improved gaming CPUs, and ROCm 7.2 software, expanding AI performance across consumer, enterprise, and gaming laptop markets. This development highlights how leading semiconductor companies are accelerating AI integration in laptops to meet evolving user demands. Overall, continuous innovation in AI-enabled processors and performance-focused computing is expected to remain a key driver of growth and transformation in the global laptop industry.

The laptop industry is experiencing a slowdown in upgrade cycles due to performance saturation, particularly with the rise of AI-enabled PCs. Modern laptops now feature powerful CPUs, GPUs, and integrated NPUs that deliver strong performance for professional workloads. As a result, the difference in user experience between new and older devices has become less noticeable for many users. This has reduced the urgency for frequent upgrades among individual users and enterprises. In addition, software optimization enables older devices to remain functional for longer.

This factor has led both consumers and enterprises to extend the life of their existing laptops instead of upgrading frequently. In mature markets, where current devices already support hybrid work, productivity tools, and basic AI features, the urgency to replace hardware has reduced significantly. Organizations are also focusing on cost control and delaying non-essential IT investments. Consumers, on the other hand, are prioritizing price and utility over premium upgrades. Overall, this trend is restraining new laptop demand and slowing market growth.

Market Concentration & Characteristics

The global laptop industry is moderately fragmented, while many smaller regional players continue to compete across price-sensitive and niche segments. The market is experiencing steady but relatively low growth, as it is already a mature hardware category with high penetration in developed regions. However, the pace of growth is gradually accelerating, driven by rising demand for AI-enabled laptops, hybrid work models, gaming upgrades, and refresh cycles in enterprise and education segments. This combination of maturity and innovation-led demand is shaping a stable yet evolving competitive environment.

From a structural perspective, the market shows very high innovation intensity, as vendors continuously invest in AI processors, better graphics performance, lightweight designs, and improved battery efficiency. The level of mergers and acquisitions is moderate, focused mainly on strengthening component ecosystems and expanding technological capabilities rather than on large-scale consolidation. Regulatory impact remains moderate, driven by sustainability requirements, energy efficiency norms, and trade policies. At the same time, substitute markets are relatively strong, with tablets, smartphones, and cloud-based computing solutions competing for entry-level and casual users. Finally, end user concentration is moderate, as demand is spread across enterprise, education, government, and consumer segments, with institutional buyers holding meaningful influence in bulk procurement decisions.

Type Insights

The traditional laptop segment accounted for the largest market share of 76.3% in 2025. Segment growth is driven by steady demand from the commercial segment, especially the gaming industry. The traditional laptop segment includes personal-use laptops/notebooks, mobile workstations, and gaming laptops. Traditional laptops are still preferred owing to more powerful components compared to their counterparts (hybrid or 2-in-1 laptops). In conclusion, the traditional laptop segment continues to dominate the market due to its strong performance capabilities, reliability, and suitability for both professional and gaming applications.

The 2-in-1 laptop segment is expected to grow at the fastest CAGR during the forecast period. The growing preference for mobility (carrying capability) and greater computing power are among the major factors driving demand for 2-in-1 laptops worldwide. In addition to superior multitasking, ports and docking, flexibility, and processing speed, over the last few years, 2-in-1 laptops have been witnessing increased demand amongst working professionals, who are increasingly replacing their full-keyboard laptops with 2-in-1 models ideal for touchscreen data entry, presentations, and note-taking. Overall, the 2-in-1 laptop segment is expected to gain strong momentum as demand for flexible, portable computing solutions rises. This trend reflects a broader shift toward hybrid work environments and the use of multifunctional devices across professional and personal applications.

Screen Size Insights

The 15.0” to 16.9” segment accounted for the largest market share in 2025. The segment growth is attributed to the benefits offered by 15-inch or larger laptops, including suitability for multitasking, a slim, sleek design, high storage capacity, and suitability for gaming and business use, among others. All these attributes of 15-inch display laptops, along with the increased availability of laptops in this display size, are expected to drive segment growth over the forecast period. Overall, the 15.0” to 16.9” display segment continues to dominate the laptop industry due to its balanced combination of performance, portability, and usability. This size range is expected to maintain strong demand as it effectively meets the needs of both professional and gaming users.

The 11" to 12.9" segment is expected to grow at a significant CAGR over the forecast period, driven by rising demand for compact, lightweight computing devices. This growth is supported by rising adoption among travelers and professionals who prioritize portability without compromising essential computing capabilities. In addition, manufacturers are continually enhancing the performance and features of small-form-factor laptops, making them better suited for everyday productivity tasks. The growing availability of slim and efficient models is further strengthening consumer preference for this segment.

Price Insights

The USD 1501 to USD 2000 segment held a dominant share of the market in 2025, driven by strong demand for high-performance computing devices that balance premium features with relatively accessible pricing. Laptops in this range typically offer advanced specifications, including powerful processors, dedicated graphics cards, high RAM capacity, and enhanced display technologies, making them highly suitable for gaming, content creation, and professional workloads. This segment is also widely preferred by enterprise users and power users who require reliable performance for data-intensive applications without moving into ultra-premium price categories. As a result, the combination of performance efficiency, durability, and value for money has positioned this segment as a key revenue contributor in the global laptop industry.

The USD 1001 to USD 1500 segment is expected to witness the fastest CAGR over the forecast period, driven by increasing demand for mid-premium laptops that offer a strong balance between performance and affordability. This segment is gaining traction among professionals, students, and creative users who require higher computing power for multitasking, content creation, and business applications without investing in ultra-premium devices. Continuous improvements in processors, graphics capabilities, and battery efficiency are further enhancing the value proposition of laptops in this price range. Overall, the rising preference for high-performance yet cost-effective devices is expected to boost demand in this segment significantly. Growing adoption across both enterprise and consumer segments is likely to make it a key growth driver in the global laptop industry.

End Use Insights

The business segment accounted for the largest market share in the market in 2025. where enterprises and professional users drive consistent demand for reliable, secure, and high-performance devices. Businesses seek laptops equipped with advanced features, such as AI-powered processors, robust security tools, long battery life, and seamless connectivity, to support hybrid and remote work models. This demand is primarily driven by digital transformation initiatives, the need for enhanced productivity in flexible work environments, and the ongoing replacement of aging fleets with modern AI-ready machines. Moreover, growth in the laptop ecosystem is also creating opportunities in adjacent categories such as the laptop carry case market, laptop table market, and laptop battery market, as enterprises increasingly invest in accessories and supporting infrastructure to improve mobility and device usability. Overall, the business segment is expected to continue its steady growth, as companies invest in robust laptops to boost employee efficiency, ensure data security, and stay competitive in a fast-evolving workplace.

The gaming segment is anticipated to register the fastest growth over the forecast period, fueled by both hardcore gamers and a rising base of casual and content-creating users who demand high-performance machines. Gaming laptops are preferred for their powerful processors, dedicated GPUs, high-refresh-rate displays, advanced cooling systems, and immersive audio experiences that deliver smooth gameplay and superior visuals. This growth is mainly driven by the booming esports industry, rising popularity of PC gaming, demand for portable high-performance devices, and the expanding overlap between gaming and content creation. Rising gaming laptop adoption is also driving demand across supporting product categories, including the laptop carry case market, laptop table market, and laptop battery market, as users increasingly seek portability, convenience, and extended device performance. Overall, the gaming laptop segment is expected to maintain strong momentum, as continuous technological advancements and growing consumer interest in immersive entertainment continue to drive upgrades and new purchases.

Regional Insights

The North America laptop industry is expected to experience significant growth during the forecast period and is characterized by high consumer spending power, strong enterprise demand, and rapid adoption of premium and innovative devices. This market is primarily driven by the surge in AI-powered laptops, ongoing business fleet refreshes due to the end of Windows 10 support, growing demand for high-performance gaming machines, and the continued need for reliable devices supporting hybrid work, remote learning, and content creation. The expansion of the United States market remains a major contributor to regional growth, supported by strong technology adoption and increasing investments in advanced computing infrastructure. Overall, the North America market is expected to maintain steady and healthy growth, supported by technological innovation, early adoption of new features, and consistent replacement demand from both businesses and consumers.

U.S. Laptop Market Trends

The U.S. laptop industry continues to show steady expansion, marked by high consumer spending, strong enterprise adoption, and rapid uptake of premium and innovative devices across consumer, business, and gaming segments. This market is primarily driven by the strong demand for AI-powered laptops, rising popularity of high-performance gaming laptops, ongoing business fleet upgrades, and the continued need for reliable, high-productivity devices to support hybrid work, remote learning, and content creation. Overall, the United States market is expected to deliver steady, resilient growth, driven by technological advancements, early adoption of new features, and consistent replacement demand from both businesses and individual consumers.

Europe Laptop Market Trends

The laptop industry in Europe is anticipated to register significant growth from 2026 to 2033, driven by increasing digitalization across industries, rising adoption of remote and hybrid work models, and strong demand from the education sector. The growing preference for high-performance, lightweight laptops is further driving market expansion across both consumer and enterprise segments. In addition, ongoing digital transformation initiatives and expanding cloud-based services are encouraging organizations to upgrade their IT infrastructure, boosting laptop adoption. The increasing focus on sustainability and demand for eco-friendly devices are also influencing product innovation in the region. Overall, strong technological adoption and evolving workplace and learning environments are expected to support the continued growth of the Europe market.

The UK laptop industry is experiencing steady growth, supported by strong digital adoption across workplaces, education institutions, and households. A key driving factor specific to the country is the widespread adoption of hybrid working models across the corporate sector, where organizations continue to provide or support laptop use for flexible work arrangements. In addition, government-led digital learning initiatives in schools and increasing reliance on cloud-based business operations are further strengthening demand for modern, portable computing devices. Rising consumer demand for high-performance laptops suitable for both professional and personal use is also driving market expansion. Overall, continued digital transformation across key sectors and a sustained hybrid work culture are expected to support the stable growth of the UK market.

The Germany laptop industry continues to hold a strong position in Europe. A key country-specific driver is the rapid implementation of Industry 4.0 initiatives, where German manufacturing and engineering companies are increasingly deploying advanced laptops to support automation, data analytics, and connected production systems. In addition, the education sector is also contributing to growth through increased adoption of digital learning tools and government-led digital classroom programs. Furthermore, strict data protection requirements under GDPR are encouraging organizations to invest in secure, high-performance devices for business use. Overall, continued industrial digitization, strong enterprise demand, and growing digital infrastructure are expected to support stable growth in the German market.

Asia Pacific Laptop Market Trends

Asia Pacific laptop industry accounted for the largest share in the global market in 2025, driven by rapid digitalization, expanding internet penetration, and increasing adoption of laptops across education, business, and personal use. A key regional driver is the large-scale expansion of the education technology ecosystem in countries such as India and China, where government-led digital learning initiatives and affordable device programs are significantly increasing laptop adoption among students. In addition, the rapid growth of IT services, outsourcing industries, and start-up ecosystems across India, Southeast Asia, and Australia is boosting demand for high-performance business laptops. Overall, strong economic development, digital transformation initiatives, and expanding end user applications are expected to drive sustained growth of the Asia Pacific market.

The laptop industry in Japan is poised for robust growth from 2026 to 2033. A key driver is Japan’s ongoing workforce digital transformation and aging population, which is accelerating the adoption of laptops for remote work, telemedicine, and digital services to improve productivity and accessibility. In addition, strong demand from the corporate sector for lightweight, high-performance, and secure laptops is supporting market growth, especially in industries such as finance, manufacturing, and IT services.

The laptop industry in China is projected to expand significantly from 2026 to 2033, driven by the government’s strong focus on digital education modernization and smart campus development, which is significantly increasing laptop usage among students across urban and rural regions. In addition, China’s dominance in global electronics manufacturing is enabling faster availability of advanced and cost-competitive laptops, further supporting domestic adoption. Strong demand from the corporate sector, especially in IT services, e-commerce, and manufacturing automation, is also driving laptop penetration for business operations and remote connectivity.

Key Laptop Company Insights

Key players operating in the laptop industry are Acer Inc., Apple Inc., ASUSTeK Computer Inc., HP Development Company, L.P. and others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In March 2026, Lenovo launched new AI-powered laptops, tablets, and gaming devices at MWC 2026, targeting creators, gamers, and productivity users. The lineup includes Yoga, IdeaPad, and Legion devices with advanced performance, AI features, and foldable concepts. These innovations highlight the growing demand for premium, flexible, and intelligent laptops worldwide.

-

In January 2026, Acer introduced new Windows 11 Copilot+ PCs, including the Swift 16 AI and Predator Helios Neo 16S AI laptops. Powered by Intel Core Ultra Series 3 processors and NVIDIA RTX 5070 GPUs, these devices offer advanced performance, a thin design, and AI features, reflecting the growing demand for high-performance and premium laptops.

-

In January 2025, ASUS launched its 2026 Copilot+ AI laptop lineup at CES, featuring ProArt, Zenbook, and Vivobook series powered by Intel, AMD, and Qualcomm processors. The devices offer advanced AI capabilities, OLED displays, and lightweight designs for creators and everyday users. This reflects rising demand for AI-enabled and premium laptops globally.

Key Laptop Companies:

The following key companies have been profiled for this study on the laptop market.

-

Acer Inc.

-

Apple Inc.

-

ASUSTeK Computer Inc.

-

HP Development Company, L.P.

-

Huawei Technologies Co., Ltd.

-

LG

-

Dell

-

Lenovo

-

Micro-Star International Co., Ltd. (MSI)

-

Microsoft Corporation

-

Panasonic Corporation

-

Razer Inc.

-

Samsung Electronics Co., Ltd.

-

Sony Corporation

-

TOSHIBA CORPORATION

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Lenovo; HP Development Company, L.P.; Dell; Apple Inc.; ASUSTeK Computer Inc.; Acer Inc.

- Focus on large-scale global production, cost optimization, and diversified product portfolios across consumer, business, and gaming segments

- Strong emphasis on enterprise contracts, long-term institutional partnerships, and ecosystem integration

- High brand trust and global market penetration across developed and emerging markets

- Strong R&D capabilities enabling frequent product refresh cycles, AI integration, and premium device innovation

- Slower adaptability in highly disruptive or low-cost segments due to large organizational structure

- Heavy dependence on mature markets, leading to slower incremental growth rates compared to emerging challengers

Emerging Players: Huawei Technologies Co., Ltd.; Microsoft Corporation; Razer Inc.; LG; Panasonic Corporation; Sony Corporation

- Focus on premium, innovation-led, or ecosystem-integrated laptops

- Target niche segments such as gaming, ultra-premium ultrabooks, or regional markets instead of full global mass penetration

- Strong technological ecosystems (Microsoft Windows integration, Huawei AI capabilities, Sony premium design expertise)

- High innovation focus enabling differentiation through design, software integration, and advanced features

- Limited global market share and weaker distribution networks compared to mature OEMs

- Higher pricing and narrower product portfolios restrict mass-market scalability

Laptop Market Report Scope

Report Attribute

Details

Market size in 2025

USD 228.8 billion

Estimated market size in 2026

USD 240.4 billion

Projected market size by 2033

USD 352.0 billion

Growth rate

CAGR of 5.6% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report Coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Type, screen size, price, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Acer Inc.; Apple Inc.; ASUSTeK Computer Inc.; HP Development Company, L.P.; Huawei Technologies Co., Ltd.; LG; Dell; Lenovo; Micro-Star International Co., Ltd. (MSI); Microsoft Corporation; Panasonic Corporation; Razer Inc.; Samsung Electronics Co., Ltd.; Sony Corporation; TOSHIBA CORPORATION

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Laptop Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global laptop market report based on type, screen size, price, end use, and region.

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Traditional Laptop

-

2-in-1 Laptop

-

-

Screen Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Upto 10.9”

-

11” to 12.9”

-

13" to 14.9"

-

15.0" to 16.9"

-

More than 17"

-

-

Price Outlook (Revenue, USD Billion, 2021 - 2033)

-

Upto 500

-

USD 501 to USD 1000

-

USD 1001 to USD 1500

-

USD 1501 to USD 2000

-

Above USD 2001

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Personal

-

Business

-

Gaming

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Region-specific analysis for the Southeast Asia laptop market

Provided Southeast Asia laptop market covering country-wise demand trends.

Added value chain analysis highlighting China-based manufacturing influence on regional availability

Helped the client identify high-growth sub-markets within Southeast Asia Improved accuracy of regional forecasting and investment prioritization

Inclusion of additional key global players in the laptop market report

Expanded competitive landscape to include emerging and niche players such as Framework, LG Electronics, Samsung, Dynabook, and Xiaomi alongside major OEMs

Provided data on players by premium, gaming, business, and budget laptop categories

Enabled a more complete competitive benchmarking across both established and emerging brands Improved strategic decision-making for partnerships and competitive positioning

Country-specific laptop market analysis

Built country-level breakdown for India, including demand drivers such as education digitization, government initiatives, and enterprise adoption

Supported localization strategy for market entry and expansion in India Helped identify pricing-sensitive segments and high-volume demand channels

Frequently Asked Questions About This Report

Asia Pacific dominated with a 35.2% revenue share in 2025.

Some key players operating in the laptop market include Acer Inc.; Apple Inc.; ASUSTeK Computer Inc.; Dell; HP Development Company, L.P.; Huawei Technologies Co., Ltd.; LG; Lenovo; Micro-Star International Co., Ltd. (MSI); Microsoft Corporation; Panasonic Corporation; Razer Inc.; Samsung Electronics Co., Ltd.; Sony Corporation; TOSHIBA CORPORATION among others.

The traditional laptop segment led with a 76.3% revenue share in 2025, while 2-in-1 laptop is the fastest-growing segment.

The 15.0” to 16.9” segment held the highest market share in 2025. while 11" to 12.9" is growing significantly.

The USD 1501 to USD 2000 segment held the highest market share in 2025, while USD 1001 to USD 1500 is the fastest-growing segment.

The business segment accounted for the largest share in 2025, while gaming is the fastest-growing segment.

Key factors include rising disposable incomes, growing internet connectivity, and the increasing inclination of consumers toward advanced laptops with respect to system performance and design.

The global laptop market size was estimated at USD 228.8 billion in 2025 and is expected to reach USD 240.4 billion in 2026.

The global laptop market is expected to grow at a compound annual growth rate of 5.6% from 2023 to 2030 to reach USD 352.0 billion by 2033.

About the Author(s)

Electronic Devices Research Team

Semiconductors & Electronics · Electronic DevicesThis report was authored by the electronic devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the electronic devices segment of the semiconductors & electronics industry. All findings are based on proprietary semiconductors & electronics databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.