- Home

- »

- Next Generation Technologies

- »

-

Managed Print Services Market Size, Industry Report, 2033GVR Report cover

![Managed Print Services Market (2026 - 2033)Report]()

Managed Print Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Deployment (On-Premise, Cloud), By Enterprise Size (Large Enterprises, SMEs), By Channel, By End-use (BFSI, Education, Government, Healthcare), By Region, and Segment Forecasts

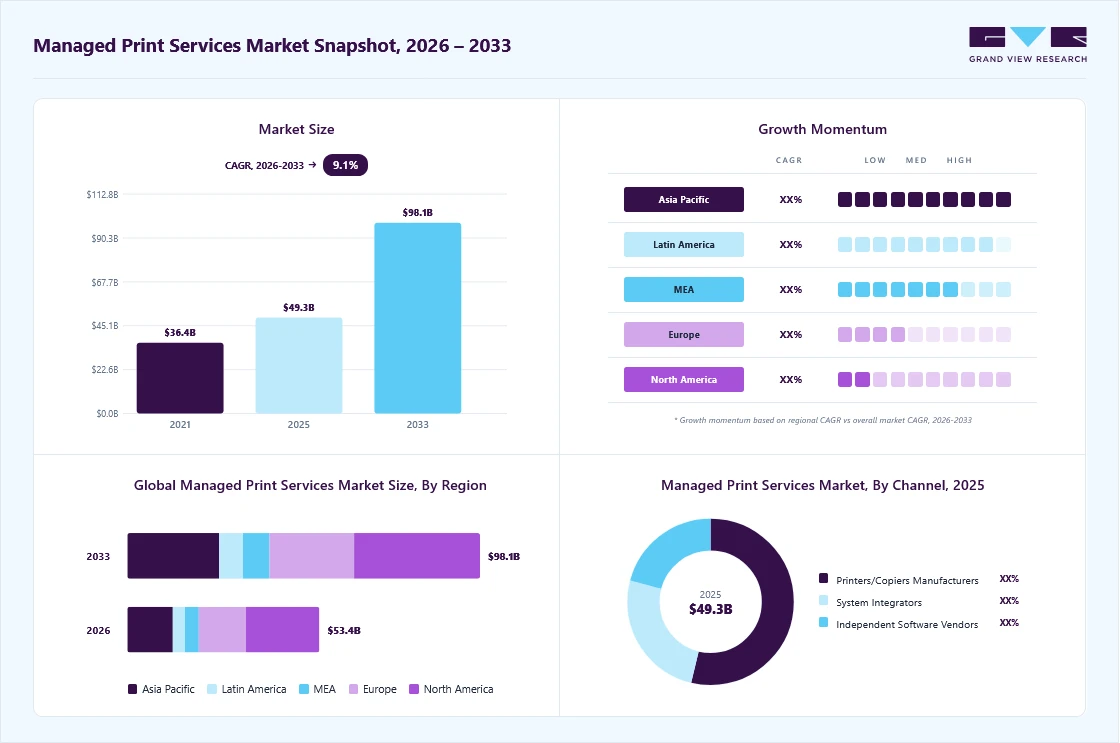

Market Size, 2025

$49.3BMarket Estimate, 2026

$53.4BMarket Forecast, 2033

$98.1BCAGR, 2026–2033

9.1%Managed Print Services Market Summary

The global managed print services market size was valued at USD 49.3 billion in 2025 and is projected to grow from USD 53.4 billion in 2026 to USD 98.1 billion by 2033, at a CAGR of 9.1% from 2026 to 2033. The market in North America dominated with a revenue share of 38.6% in 2025. Organizations across industries such as BFSI, healthcare, retail, manufacturing, education, and government are adopting advanced MPS solutions over traditional, device-centric print management approaches to improve cost efficiency, security, and operational visibility in a complex, distributed work environment.

Key Market Trends & Insights

- By channel: Printers/copiers manufacturers segment held the largest market share of 52.7% in 2025.

- By deployment: On-premises segment held the largest market share in 2025.

- By enterprise size: Large enterprises segment held the largest market share in 2025.

- By end-use: BFSI segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (38.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 49.3 Billion

- Estimated market size in 2026: USD 53.4 Billion

- Projected market size by 2033: USD 98.1 Billion

- CAGR (2026-2033): 9.1%

This shift is driven by rising document management costs, growing cybersecurity risks, and the need to support hybrid and remote work models, prompting enterprises to deploy integrated MPS platforms that combine fleet optimization, consumables management, security controls, analytics, and workflow automation. Cloud-based and SaaS-enabled MPS solutions are gaining strong traction, enabling centralized monitoring, predictive maintenance, and seamless integration with enterprise IT systems while supporting scalable deployments across multi-location and global operations.The market is witnessing accelerated adoption of AI- and ML-driven analytics, predictive device monitoring, automated supply replenishment, and intelligent document workflows, as organizations seek to move beyond reactive print management toward proactive, data-driven optimization. Vendors are increasingly differentiating through capabilities such as real-time fleet analytics, print usage behavior analysis, secure pull printing, zero-trust security frameworks, and advanced reporting dashboards that help enterprises quantify cost savings, reduce downtime, and improve sustainability outcomes. At the same time, rising regulatory scrutiny around data protection and compliance is driving demand for MPS solutions with robust encryption, user authentication, audit trails, and compliance-ready document handling.

")

In addition, rising digitalization, increased document volumes in regulated industries, and sustainability initiatives are further reshaping enterprise print strategies, with organizations leveraging MPS to reduce paper waste, energy consumption, and carbon footprint. Many enterprises are integrating MPS with digital document management, content services platforms, and business process automation tools to streamline workflows such as invoicing, onboarding, claims processing, and records management. For instance, enterprises are increasingly adopting print policies, usage analytics, and rules-based automation through MPS platforms to minimize unnecessary printing and optimize device utilization across departments.

Consequently, the market is evolving from a tactical, cost-containment solution into a strategic IT and operations enabler that supports security, sustainability, digital transformation, and measurable business performance. As organizations prioritize operational resilience, data security, and efficiency in a hybrid workplace environment, MPS is increasingly viewed as a long-term value-creation platform rather than a standalone print outsourcing service, underpinning sustained cost savings, productivity improvements, and competitive advantage in a digitally evolving enterprise landscape.

Channel Insights

The printers/copiers manufacturers segment accounted for the largest revenue share of 52.7% in 2025, driven by enterprises’ preference for OEM-led, end-to-end print management solutions that combine hardware, consumables, software, and services under unified contracts. Growth in this channel is further supported by OEMs’ transition toward software-defined and AI-enabled print platforms, integrating cloud connectivity, remote monitoring, and workflow automation to support hybrid work environments and distributed enterprise operations. For instance, in October 2025, Xerox introduced two new digital presses as part of its expanding production ecosystem, reinforcing its strategy to integrate advanced hardware with automation, analytics, and workflow solutions, highlighting the broader shift among manufacturers toward recurring, services-led revenue models. Consequently, printer and copier manufacturers dominate the MPS market as enterprises increasingly favor tightly integrated, scalable, and globally supported print management solutions aligned with digital transformation and operational efficiency objectives.

The independent software vendors segment is expected to register the fastest CAGR in the market during the forecast period, driven by growing enterprise demand for software-centric print management solutions that can operate across heterogeneous device environments. ISVs are gaining traction by offering advanced capabilities such as cloud-native print management, AI-driven analytics, predictive maintenance insights, security overlays, and seamless integration with enterprise IT, document management, and workflow automation platforms. As organizations adopt hybrid work models and multi-vendor print fleets, ISV solutions are favored for their flexibility, rapid deployment, and ability to enhance existing MPS engagements without requiring hardware replacement. Moreover, the rising shift toward SaaS delivery models, subscription-based pricing, and data-driven optimization is enabling ISVs to scale quickly across regions and customer segments, positioning this channel as the fastest-growing segment within the evolving MPS ecosystem.

Deployment Insights

The on-premises segment accounted for the largest share in the global market in 2025, driven by enterprises’ preference for direct control over their print infrastructure, security, and compliance, particularly in highly regulated industries such as BFSI, healthcare, and government. On-premises MPS solutions enable organizations to manage large, distributed fleets of printers and multifunction devices while maintaining data residency, enforcing strict access controls, and optimizing operational efficiency through centralized monitoring and analytics. Despite the growing adoption of cloud-based MPS, on-premises deployments continue to dominate due to their reliability, integration with legacy IT systems, and ability to support mission-critical workflows that demand high levels of security and performance.

The cloud segment is expected to grow at a significant CAGR during the forecast period, due to increasing hybrid work models and the need for centralized, remote print management. Enterprises are also leveraging cloud MPS for cost optimization, enhanced security, and seamless integration with digital workflows. In addition, growing demand for scalable, serverless, and multi-brand cloud print solutions is fueling significant growth in the cloud deployment segment. For instance, in July 2025, Ricoh launched CloudStream, a secure, serverless cloud printing platform that enables enterprises to manage multi-brand print environments remotely, with enhanced workflow automation, security, and sustainability features. These developments highlight the accelerating shift toward cloud-native MPS solutions, positioning this segment as a key segment in the global market.

Enterprise Size Insights

The large enterprises segment accounted for the largest market share in 2025, driven by the need to optimize costs, enhance security, and manage complex, distributed print environments across multiple locations. In addition, large organizations are adopting advanced analytics, automated workflows, and secure print management to improve operational efficiency and compliance, while supporting hybrid work models. Moreover, growing demand for high-value, scalable, and secure print solutions is reinforcing the dominance of this segment. For instance, in January 2026, Fiery introduced the XF 9 print management platform, unlocking new capabilities for large-format and enterprise print environments with enhanced automation, high-value output, and seamless integration into enterprise workflows. These developments highlight that large enterprises continue to lead MPS adoption, leveraging advanced technologies to achieve greater control, efficiency, and measurable value from their print services.

The SMEs segment is projected to register the fastest CAGR over the forecast period, driven by growing adoption of cost-effective and cloud-enabled print management solutions among small and medium-sized businesses. SMEs are increasingly leveraging subscription-based and SaaS-oriented MPS platforms to reduce upfront infrastructure costs, simplify fleet management, and gain real-time visibility into print usage and expenses. The segment’s growth is further fueled by demand for scalable solutions that support hybrid work environments, enhance security, and integrate seamlessly with existing IT systems without the need for extensive on-premises infrastructure. Consequently, as organizations continue to prioritize operational efficiency and digital transformation, SMEs are emerging as the fastest-growing adopters of MPS solutions globally.

End-use Insights

The BFSI segment accounted for the largest market share in 2025, as organizations require secure and compliant print environments to manage high volumes of sensitive documents such as loan forms, KYC records, compliance reports, and customer communications, driving significant investment in MPS solutions that optimize costs and enhance operational control. In addition, document security, regulatory compliance, and analytics-driven print governance are key drivers for continued MPS adoption in the BFSI sector, while hybrid and cloud-integrated print services are increasingly supporting digital transformation initiatives across financial institutions. The BFSI industry’s stringent data security needs and high print volumes are accelerating the deployment of advanced MPS offerings that deliver secure print release, user authentication, encryption, and automated fleet monitoring. Consequently, these developments highlight that the BFSI segment remains the dominant end-use vertical in the global MPS market, reflecting its critical need for secure, efficient, and compliant print management solutions.

Retail & consumer goods is expected to register the fastest growth during the forecast period in the global market. Companies in this space often face high-volume printing demands due to seasonal promotions and inventory management, where MPS helps reduce downtime through proactive maintenance and automated supply replenishment. This approach not only boosts efficiency but also supports sustainability goals by minimizing waste and energy use in printing processes. For consumer goods firms, MPS enables better customization of product labels and marketing materials, adapting quickly to market changes while maintaining compliance with regulatory standards.

Regional Insights

North America accounted for the largest market share of 38.6% in 2025 in the global market. MPS providers in this region leverage advanced printing solutions and cloud computing to offer more efficient, secure, and scalable print management solutions. Integrating IoT-enabled printers with real-time monitoring and proactive maintenance reduces downtime and enhances operational efficiency. In addition, adopting cloud-based MPS solutions facilitates remote management and improves accessibility, making it easier for organizations to manage their print environments across multiple locations.

U.S. Managed Print Services Market Trends

The managed print services market in the U.S. is experiencing strong growth. MPS providers in the U.S. bring extensive knowledge and experience in managing complex print environments, offering businesses expert guidance and support. These providers offer various services, including print fleet management, document management, workflow optimization, and security solutions. The availability of dedicated support services minimizes downtime and maintains business continuity. In line with this trend, U.S.-based MPS providers are strengthening long-term partnerships with major organizations to expand service reach and ensure operational reliability. For instance, in June 2025, DOCUmation has extended its multi-year partnership with the San Antonio Spurs, continuing to deliver Managed Print Services and onsite print management at the Frost Bank Center, supporting operational efficiency while strengthening its presence in the U.S. market. This partnership reinforces the role of long-term MPS contracts in driving steady demand and brand visibility across the market.

Europe Managed Print Services Market Trends

The managed print services (MPS) market in Europe is anticipated to register significant growth from 2026 to 2033. MPS providers offer solutions that optimize printing environments, consolidate devices, and automate workflows, leading to significant cost savings and enhanced productivity. In addition, there is a growing emphasis on digital transformation, with European companies integrating MPS to streamline document management, enhance security, and support flexible work arrangements. In response to these trends, major market players are expanding their managed print portfolios with subscription-based and cloud-driven offerings. For instance, in March 2024, HP Development Company, L.P. launched a Managed Print Services Subscription in Europe, offering flexible annual plans, cloud-based printing, automatic supply replenishment, device monitoring, next-business-day repairs, and fleet analytics, supporting distributed workplaces and remote employees across key European countries. This launch is expected to accelerate the adoption of subscription-based managed print services in Europe by simplifying fleet management and reducing costs for hybrid and distributed organizations.

The UK managed print services market is experiencing strong growth, driven by businesses seeking to cut operational costs, enhance document security, and support hybrid working environments amid ongoing digital transformation efforts. Providers focus on cloud-integrated solutions, proactive device monitoring, and automated consumables management to minimize downtime and improve workflow efficiency across sectors such as finance, public services, and professional firms. Sustainability remains a priority, with emphasis on reducing paper usage and energy consumption through smarter print policies and eco-friendly hardware options.

The managed print services market in Germany is witnessing robust growth, driven by strict regulatory demands such as GDPR for data security and strong emphasis on environmental sustainability through initiatives such as the EU Green Deal. Businesses across manufacturing, public sector, and professional services rely on MPS to manage complex multi-site printer fleets, achieve cost efficiencies, and integrate secure, cloud-hybrid solutions that support digital workflows.

France managed print services market is growing significantly at a CAGR from 2026 to 2033. Businesses increasingly turn to MPS to cut operational costs, consolidate device fleets, and shift toward hybrid or cloud-based models that support remote work while meeting environmental standards through reduced paper use and energy-efficient devices. Market key players such as Canon, HP, Ricoh, and Kyocera dominate, offering tailored solutions that integrate analytics and proactive maintenance to minimize downtime. Sustainability remains a priority, with many contracts now including carbon tracking features aligned with EU green initiatives.

Asia Pacific Managed Print Services Market Trends

The managed print services (MPS) market in the Asia Pacific is expected to register the fastest CAGR from 2026 to 2033. The Asia Pacific region is experiencing rapid economic growth and industrialization, driving the demand for the MPS market. As businesses expand and industrial activities increase, there is a higher demand for efficient and cost-effective printing solutions. MPS allows companies to streamline their print operations, reduce costs, and improve productivity, which is essential in fast-growing economies where businesses pursue maintaining a competitive edge. The increasing number of small and medium-sized enterprises (SMEs) in the region also contributes to the demand for MPS.

India managed print services market is poised for robust growth from 2026 to 2033. MPS providers offer solutions enabling secure and efficient printing from remote locations, ensuring employees have access to print services regardless of location. Features such as cloud printing, mobile printing, and secure print release facilitate seamless printing for remote and hybrid workforces. By adapting to these new work models, MPS solutions aid Indian businesses in maintaining productivity and flexibility in a changing work environment.

The managed print services market in China is witnessing rapid growth. Major providers such as HP, Canon, Ricoh, and local players focus on high-volume environments in manufacturing, e-commerce, and government sectors, where proactive monitoring and automated consumables delivery minimize disruptions. The market benefits from growing emphasis on sustainability, reducing paper usage amid stricter environmental regulations, while supporting hybrid work models with secure remote printing capabilities. Adoption remains robust due to cost pressures and the need for efficient compliance in regulated industries.

Key Managed Print Services Company Insights

Key players operating in the MPS industry are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals.

Key Managed Print Services Companies:

The following key companies have been profiled for this study on the managed print services market.

- ARC Document Solutions, LLC

- Canon Inc.

- HP Development Company, L.P.

- Konica Minolta, Inc.

- Lexmark International, Inc.

- Ricoh

- SAMSUNG ELECTRONICS CO., LTD.

- SHARP CORPORATION

- TOSHIBA CORPORATION

- Xerox Corporation

Recent Developments

-

In January 2026, Konica Minolta Business Solutions (UK) Ltd partnered with Viking Office Systems to expand access to advanced print and document management solutions across the Isle of Man, supporting regulated financial services customers and strengthening service quality amid ongoing changes in the market. This partnership is expected to improve service stability and drive demand for secure, high-performance managed print solutions in regulated and offshore financial markets.

-

In April 2025, Flotek Group launched a dedicated Managed Print Services division to meet growing demand for secure and efficient print and document management. Supported by its OES acquisition, the division will serve professional sectors and is led by industry expert Andrew Peto. This development strengthens competition in the market by expanding secure, sector-focused solutions and driving greater adoption of integrated print management services.

Managed Print Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 49.3 billion

Estimated Market size in 2026

USD 53.4 billion

Projected Markket size by 2033

USD 98.1 billion

Growth rate

CAGR of 9.1% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report Coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Channel, deployment, enterprise size, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

ARC Document Solutions, LLC; Canon Inc.; HP Development Company, L.P.; Konica Minolta, Inc.; Lexmark International, Inc.; Ricoh; SAMSUNG ELECTRONICS CO., LTD.; SHARP CORPORATION; TOSHIBA CORPORATION; Xerox Corporation

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Managed Print Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global managed print services market report based on channel, deployment, organization size, end-use, and region:

-

Channel Outlook (Revenue, USD Billion, 2021 - 2033)

-

Printers/Copiers Manufacturers

-

System Integrators

-

Independent Software Vendors

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-Premise

-

Cloud

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

SMEs

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Education

-

Government

-

Healthcare

-

Industrial Manufacturing

-

Retail & Consumer Goods

-

Telecom & IT

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global managed print services market size was estimated at USD 49.3 billion in 2025 and is expected to reach USD 53.4 billion in 2026.

The global managed print services market is expected to grow at a CAGR of 9.1% from 2026 to 2033 to reach USD 98.1 billion by 2033.

North America region dominated the MPS market with a share of 38.6% in 2025. This is attributable to the presence of printer/copier manufacturers, favorable government regulations and a rising number of startups in the region.

Some key players operating in the managed print services market include ARC Document Solutions, LLC, Canon Inc., HP Development Company, L.P., Konica Minolta, Inc., Lexmark International, Inc., Ricoh, SAMSUNG ELECTRONICS CO., LTD., SHARP CORPORATION, TOSHIBA CORPORATION, Xerox Corporation.

Key factors that are driving the market growth include reduce printing costs, optimize print workflows, and consolidate print fleets, shift to digital workflows and Heightened concerns around data security, document confidentiality, and regulatory compliance.

The printers/copiers manufacturers segment led with a 52.7% revenue share in 2025, while the independent software vendors segment is the fastest-growing.

The on-premises segment held the largest revenue share in 2025, while the cloud segment is expected to grow at a significant CAGR.

The large enterprises segment held the largest revenue share in 2025, while the SMEs segment is the fastest-growing.

BFSI segment held the largest share in 2025, while the retail & consumer goods segment is the fastest-growing.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.