- Home

- »

- Water & Sludge Treatment

- »

-

Membrane Filtration Market Size , Share Report, 2026 - 2033GVR Report cover

![Membrane Filtration Market Size, Share & Trends Report]()

Membrane Filtration Market (2026 - 2033) Size, Share & Trends Analysis Report By Membrane Material (Ceramic, Polymeric), By Module Design (Spiral Wound, Tubular Systems, Plate & Frame, Hollow Fiber), By Technology (Reverse Osmosis, Ultrafiltration, Microfiltration, Nanofiltration), By Application, By Region, And Segment Forecasts

Market Size, 2025

$19.4BMarket Estimate, 2026

$20.7BMarket Forecast, 2033

$35.0BCAGR, 2026–2033

7.8%Membrane Filtration Market Summary

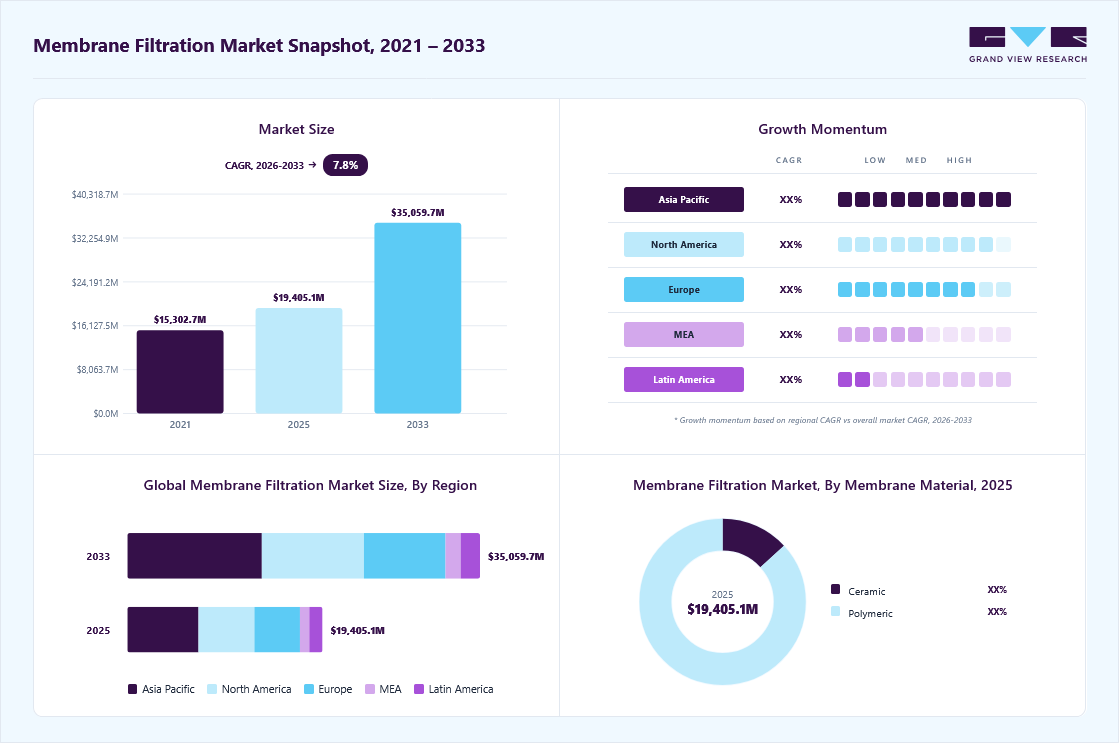

The global membrane filtration market size was valued at USD 19.4 billion in 2025 and is projected to grow from USD 20.7 billion in 2026 to USD 35.0 billion by 2033, at a CAGR of 7.8% from 2026 to 2033. The market in asia pacific dominated with a revenue share of 36.5% in 2025. Rapid urbanization, population growth, and industrialization are creating pressure on existing water resources, prompting adoption of efficient filtration technologies.

Key Market Trends & Insights

- By membrane material: Polymeric segment dominated the market with a revenue share of 86.8 % in 2025.

- By module design: Spiral wound segment accounted for a revenue share of 45.8% in 2025.

- By application: Water & wastewater segment accounted for a revenue share of 41.7% in 2025.

- By technology: Reverse osmosis segment accounted for a revenue share of 36.3% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (36.5% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 19.4 billion

- Estimated market size in 2026: USD 20.7 billion

- Projected market size by 2033: USD 35.0 billion

- CAGR (2026-2033): 7.8%

Membrane filtration offers high separation efficiency, low energy consumption, and scalability, making it suitable for municipal, industrial, and healthcare applications. Additionally, stringent regulations on water quality, environmental protection, and effluent discharge are compelling industries and municipalities to invest in advanced filtration systems.")

Technological advancements such as ultrafiltration, nanofiltration, and reverse osmosis membranes, along with growing awareness of water sustainability, are further accelerating market expansion globally across regions like North America, Europe, and Asia-Pacific.

Market Dynamics

The growing global demand for clean water and efficient wastewater treatment solutions is one of the major factors driving the membrane filtration market. Rapid urbanization, industrial expansion, and rising population levels are significantly increasing pressure on existing water resources, creating strong demand for advanced filtration technologies capable of removing contaminants, microorganisms, suspended solids, and dissolved impurities from water and industrial fluids. Industries such as food & beverage, pharmaceuticals, chemicals, dairy processing, biotechnology, and municipal water treatment are increasingly adopting membrane filtration systems to improve product quality, ensure regulatory compliance, and support water reuse initiatives.

One of the major challenges affecting the membrane filtration market is membrane fouling, which can significantly reduce system efficiency and increase maintenance requirements over time. During filtration processes, contaminants such as suspended particles, biological matter, oils, salts, and chemical deposits can accumulate on the membrane surface, restricting flow rates and affecting filtration performance. Frequent cleaning, membrane replacement, and system downtime associated with fouling can increase operational complexity and overall maintenance expenses for end users.

Industry Concentration & Characteristics

The membrane filtration market is moderately fragmented, with a mix of global manufacturers and numerous regional players competing for market share. Large companies focus on technological innovation, high-performance membranes, and comprehensive service offerings, while smaller regional firms provide cost-effective, niche, or specialized solutions. This structure maintains competition without complete consolidation, as customers choose between established brands for reliability and smaller providers for customized or localized solutions. Moderate fragmentation also encourages continuous product development and market diversification.

The membrane filtration market shows high degree of innovation, driven by the development of high-performance membranes such as ultrafiltration, nanofiltration, and reverse osmosis. Innovations focus on improving filtration efficiency, energy consumption, fouling resistance, and lifespan. Companies are also integrating smart monitoring systems and modular designs to optimize operations. Continuous research and adoption of advanced materials support diverse applications in water treatment, food & beverage, pharmaceuticals, and industrial processes.

Merger and acquisition activity in the market is significant and largely strategic. Large players often acquire regional or specialized membrane manufacturers to gain market share, enhance R&D, and integrate complementary solutions. These strategic activities allow firms to offer comprehensive filtration systems, improve competitiveness, and respond to growing global demand efficiently.

Regulations significantly influence the membrane filtration market, particularly in water quality, wastewater treatment, and industrial effluent management. Governments worldwide impose strict standards for potable water, environmental protection, and industrial discharges. Compliance with these regulations drives adoption of advanced filtration technologies. Regulatory pressure encourages innovation, investment in high-efficiency membranes, and the expansion of monitoring and maintenance services to ensure safe, clean, and sustainable water management practices globally.

Membrane Material Insights

“The ceramic segment is expected to grow at a considerable CAGR of 9.2% from 2026 to 2033 in terms of revenue”

The polymeric segment dominated the market with a revenue share of 86.8 % in 2025 due to its cost-effectiveness, flexibility, and ease of fabrication. Polymeric membranes, such as polyethersulfone (PES), polyvinylidene fluoride (PVDF), and polypropylene, are widely used in water treatment, wastewater recycling, and industrial processes. Their high permeability, chemical resistance, and adaptability to ultrafiltration and microfiltration applications drive adoption across municipal and industrial sectors, particularly in emerging economies with growing demand for affordable and scalable filtration solutions.

The ceramic membrane segment is expected to expand due to its durability, high thermal stability, and resistance to harsh chemical and abrasive conditions. Ceramic membranes are increasingly used in industries such as food and beverage, pharmaceuticals, and wastewater treatment, where long-term performance and low maintenance are critical. Despite higher costs, their longevity, fouling resistance, and ability to handle extreme conditions make them attractive for high-value industrial applications, supporting steady market growth globally.

Module Design Insights

“The hollow fiber segment is expected to grow at a considerable CAGR of 7.7% from 2026 to 2033 in terms of revenue”

The spiral wound segment accounted for a revenue share of 45.8% in 2025 due to its compact design, high surface area, and efficiency in water and wastewater treatment applications. Widely used in reverse osmosis, nanofiltration, and ultrafiltration systems, spiral wound membranes offer cost-effective performance and easy scalability. Industries and municipalities prefer them for desalination, industrial process water, and purification systems, driving adoption globally, particularly in regions with increasing water scarcity and regulatory pressure for clean water.

The hollow fiber segment is anticipated to expand due to its high packing density, self-supporting structure, and superior filtration efficiency. Hollow fiber membranes are suitable for ultrafiltration and microfiltration applications, including municipal water treatment, wastewater recycling, and industrial processes. Their ability to handle high volumes, ease of backwashing, and modular scalability make them attractive for both small and large-scale systems, supporting growth in regions emphasizing sustainable water management and advanced purification solutions.

Technology Insights

“The nanofiltration segment is expected to grow at a considerable CAGR of 8.4% from 2026 to 2033 in terms of revenue”

The reverse osmosis segment accounted for a revenue share of 36.3% in 2025. Market demand continues rising for high‑purity water in desalination, municipal, and industrial water treatment. Its ability to remove nearly all salts and contaminants makes it indispensable for potable and process water, driving adoption especially in water‑scarce regions and large infrastructure projects. Technological advances and efficiency improvements further support RO’s expansion.

Nanofiltration (NF) is projected to grow rapidly as industries adopt it for selective removal of organic compounds and divalent ions with lower energy needs than RO. NF’s efficiency in water softening, wastewater reuse, and compliance with tightening discharge standards boosts its appeal. Growth is amplified by expanding applications in food & beverage, pharmaceuticals, and industrial water treatment, along with increasing investments in advanced membrane technologies.

Application Insights

“The pharmaceutical segment is expected to grow at a considerable CAGR of 9.0% from 2026 to 2033 in terms of revenue”

The water & wastewater segment accounted for a revenue share of 41.7% in 2025. Rising global water scarcity, stringent environmental regulations on discharge quality, and the need for efficient wastewater recycling are driving increased adoption of membrane systems by municipal and industrial sectors. Advanced filtration offers scalable, chemical‑free treatment that removes contaminants effectively, supporting sustainable water reuse and infrastructure expansion worldwide.

Pharmaceutical segment is expected to grow significantly during the forecast period due to growing demand for high‑purity filtration in drug manufacturing, biologics production, and sterile processing. Membrane technology ensures removal of microbes, proteins, and particulates to meet strict regulatory and quality standards. Expansion of biopharmaceuticals, vaccines, and advanced therapeutics fuels investments in membrane systems for sterile filtration, purification, and process efficiency.

Regional Insights

Asia Pacific Membrane Filtration Market Trends

Asia Pacific region dominated the market and accounted for 36.5% of the global market share in 2025 driven by population expansion, urbanization, and increasing water scarcity. Countries invest heavily in water and wastewater treatment infrastructure to meet rising demand and regulatory requirements. Industrialization in sectors such as textiles, chemicals, and food processing fuels the need for efficient filtration and reuse solutions. Government incentives and public–private partnerships accelerate project deployment. Technological advancements and lower costs make membrane systems more attractive. Regional focus on sustainable water management supports long‑term market expansion.

China’s membrane filtration market is growing rapidly as environmental protection and water resource management become national priorities. The government enforces stringent water quality standards and invests in large‑scale water and wastewater treatment infrastructure. Rapid industrial growth in manufacturing, chemicals, and electronics drives demand for high‑efficiency membrane systems. Urbanization increases municipal water treatment projects and reuse initiatives. Domestic innovation in membrane materials and technology reduces costs and enhances performance. China’s focus on sustainable development and pollution control further accelerates adoption across sectors.

India’s membrane filtration market is expanding due to rising demand for potable water, wastewater treatment, and industrial use. Water scarcity, urbanization, and pollution challenges prompt government and private investment in advanced membrane technologies. Municipal programs focus on wastewater reuse and improving access to clean water. Industries such as pharmaceuticals, food processing, and textiles increasingly adopt membrane systems for efficient separation. Cost‑effective and energy‑efficient solutions attract widespread use.

North America Membrane Filtration Market Trends

North America’s membrane filtration market is growing rapidly due to strict water quality regulations, expanding municipal treatment infrastructure, and rising industrial demand. The region emphasizes advanced water and wastewater treatment solutions to address aging systems, water scarcity, and environmental compliance. Growing industries including food & beverage, chemicals, and power are adopting membrane technologies for efficient separation and reuse. Investment in research, government incentives, and technological innovation in membranes further drive market expansion, with both public and private sectors prioritizing sustainable water management.

U.S. is expected to experience strong growth in the membrane filtration market as federal and state regulations demand higher water quality and wastewater reuse. Aging water infrastructure requires modernization with efficient membrane systems, increasing public and private investment. Strong industrial growth in pharmaceuticals, food processing, and electronics fuels demand for high‑precision filtration. Innovation in membrane materials and energy‑efficient systems enhances adoption. Funding programs and sustainability goals encourage implementation of advanced technologies. Overall focus on water security and environmental protection supports steady market growth.

Mexico’s membrane filtration market is growing as the country addresses water scarcity and contamination challenges. Municipalities and industries are increasingly adopting membrane systems for potable water production and wastewater treatment. Regulatory pressure to improve water quality and reduce pollution promotes investment in advanced filtration technologies. Growth in manufacturing, food processing, and pharmaceuticals stimulates demand for reliable separation solutions.

Europe Membrane Filtration Market Trends

The Europe membrane filtration market is expected to grow at 7.7% CAGR during forecast period and is expanding due to stringent environmental standards, water reuse targets, and industrial demand. European Union directives on wastewater discharge and reuse are pushing municipalities to adopt advanced membrane systems. Industries including chemicals, food & beverage, and pharmaceuticals require high‑purity water for processes, increasing filtration demand. Investment in innovation and sustainability initiatives supports cutting‑edge membrane technologies. Aging infrastructure upgrades and climate resilience efforts further drive growth.

Germany's membrane filtration market is one of the most advanced in Europe, emphasizes high environmental standards and efficient water management. German industries such as automotive, chemicals, and pharmaceuticals require advanced filtration for process water and wastewater treatment. Municipal efforts to modernize aging infrastructure boost demand for membrane solutions. Strict regulations on effluent quality and resource reuse drive technology adoption. German research institutions and companies lead in membrane innovation, improving energy efficiency and performance.

UK membrane filtration market is expanding due to regulatory pressure to improve water quality and increase wastewater recycling. Utility companies are investing in advanced treatment technologies to address aging infrastructure and environmental targets. Industrial sectors including food & beverage, pharmaceuticals, and energy require high‑precision filtration for process water and effluent management. Demand for energy‑efficient, high‑performance membranes grows with focus on sustainability, circular water use, and resilience to climate‑related water challenges.

Middle East & Africa Membrane Filtration Market Trends

Middle East & Africa membrane filtration market is growing as water scarcity and desert climates drive demand for reliable water treatment solutions. Many countries invest in desalination, brackish water treatment, and wastewater reuse to support population and industrial needs. Government programs emphasize infrastructure development and sustainable water management. Industries such as oil & gas, chemicals, and food processing adopt membrane technologies for efficient separation and reuse.

Saudi Arabia’s membrane filtration market is expanding due to acute water scarcity and heavy reliance on desalination and reuse. The government invests significantly in large‑scale water treatment and wastewater recycling projects to support population growth and economic development. Industries including petrochemicals, energy, and manufacturing adopt membrane technologies for efficient separation and process water reuse.

Latin America Membrane Filtration Market Trends

Latin America’s membrane filtration market is growing as countries seek to improve water quality, address scarcity, and modernize treatment infrastructure. Municipalities invest in advanced filtration for potable water and wastewater reuse, driven by regulatory improvements and environmental concerns. Industrial sectors like mining, food & beverage, and chemicals adopt membrane systems for efficient separation and compliance.

Brazil’s membrane filtration market is expanding as water challenges and regulatory demands increase demand for advanced treatment solutions. Municipal initiatives prioritize drinking water quality and wastewater reuse, especially in urban areas facing scarcity. Industrial growth in agriculture, food processing, and chemicals fuels adoption of membrane technologies. Government programs and investment in infrastructure upgrades support deployment.

Key Companies & Market Share Insights

Some of the key players operating in the market include Alfa Laval, GEA Group and 3Mamong others.

-

3M is a diversified global technology company known for its innovative membrane filtration solutions used across water treatment, healthcare, and industrial sectors. Their membranes focus on improving water purity, filtration efficiency, and contaminant removal, supporting applications from potable water to wastewater treatment. Leveraging advanced materials and proprietary technology, 3M develops durable, high-performance membranes that address evolving regulatory standards and sustainability goals. Strong R&D capabilities and global presence enable 3M to meet diverse market needs with reliable, scalable filtration products.

-

Alfa Laval specializes in advanced membrane filtration technologies, serving industries like food & beverage, pharmaceuticals, and water treatment. Renowned for energy-efficient and sustainable separation solutions, Alfa Laval offers ultrafiltration, microfiltration, and reverse osmosis systems tailored for process optimization and environmental compliance. Their innovations enhance water reuse, reduce operational costs, and improve product quality. With decades of expertise, Alfa Laval combines engineering excellence and global service networks to deliver reliable, high-quality membrane filtration solutions supporting circular economy initiatives.

Key Membrane Filtration Companies:

The following are the leading companies in the membrane filtration market. These companies collectively hold the largest Market share and dictate industry trends.

- Alfa Laval

- GEA Group

- DuPont

- Pall Corporation

- Veolia

- 3M

- Pentair

- Porvair Filtration Group

- Donaldson Company, Inc.

- MMS Membrane Systems

- Koch Separation Solutions

- ProMinent

- SPX Flow

- TORAY INDUSTRIES, INC.

- MANN+HUMMEL

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature players: DuPont; Veolia; Pall Corporation

- These companies continuously strengthen their market leadership through membrane innovation, automation upgrades, digital monitoring solutions, and expansion of after-sales service capabilities across applications.

- They focus on strategic acquisitions, technology partnerships, and global manufacturing optimization to maintain strong positions across reverse osmosis, ultrafiltration, nanofiltration, and wastewater reuse systems.

- These players maintain a strong global market presence supported by established manufacturing facilities, direct subsidiaries, and extensive dealer and service networks across major water treatment regions.

- Their advantage lies in advanced membrane engineering, strong process integration capabilities, and the ability to offer complete treatment solutions.

- High capital expenditure requirements for research, automation, sustainability compliance, and advanced membrane manufacturing increase operating costs and result in premium system pricing.

- Their global operations create greater exposure to raw material cost fluctuations, regulatory changes, project delays, and strict environmental compliance requirements across multiple regions

Emerging players: Koch Separation Solutions; MMS Membrane Systems

- These companies focus on strengthening their position through specialized membrane expertise, selective automation upgrades, and expansion across high-growth applications.

- They emphasize strategic regional expansion, technology partnerships, and flexible customization to serve both large industrial clients and mid-sized manufacturers with application-specific filtration requirements

- Strong technical specialization in niche filtration areas such as industrial separation, biotechnology applications, and advanced wastewater reuse enables them to maintain strong customer loyalty and application-specific leadership.

- Greater operational flexibility, faster project execution, and localized technical support improve responsiveness while offering competitively priced solutions across regional and export markets

- Compared to mature leaders, some players have relatively narrower end-to-end treatment integration capabilities, particularly in fully turnkey global-scale municipal and industrial projects.

- These companies face considerable competition from larger multinational players with stronger installed bases, broader service networks, and stronger long-term customer relationships.

Recent Developments

-

In September 2025, Pall Corporation launched Membralox GP-IC, a ceramic membrane system with graduated permeability along the filter length. This innovative design boosts processing efficiency reduces capital and operating costs, and can recover up to 95% of value-added products. It significantly enhances filtration performance, supporting more sustainable and cost-effective food production processes.

-

In January 2025, Toray developed a high-efficiency membrane that doubles filtration performance, enhancing pharmaceutical manufacturing productivity and product quality. This innovation enables faster, more reliable filtration processes, supporting stricter quality standards and increased output in pharma production.

Membrane Filtration Market Report Scope

Report Attribute

Details

Market size in 2025

USD 19.4 billion

Estimated market size in 2026

USD 20.7 billion

Projected market size by 2033

USD 35.0 billion

Growth Rate

CAGR of 7.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market position analysis, competitive landscape, growth factors, and trends

Segments covered

Membrane material, module design, technology, application, and Region

Regional scope

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa

Country Scope

U.S., Canada, Mexico, Germany, France, UK, Italy, Spain, China, India, Japan, Australia, Brazil, Argentina, Saudi Arabia, South Africa, UAE

Key companies profiled

Alfa Laval, GEA Group, DuPont, Pall Corporation, Veolia, 3M, Pentair, Porvair Filtration Group, Donaldson Company, Inc., MMS Membrane Systems, Koch Separation Solutions, ProMinent, SPX Flow, TORAY INDUSTRIES, INC., MANN+HUMMEL.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Membrane Filtration Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels and provides an analysis on the industry trends in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the membrane filtration market on the basis of membrane material, module design, technology, application, and region:

-

Membrane Material Outlook (Revenue, USD Million; 2021 - 2033)

-

Ceramic

-

Polymeric

-

-

Module Design Outlook (Revenue, USD Million; 2021 - 2033)

-

Spiral Wound

-

Tubular Systems

-

Plate & Frame

-

Hollow Fiber

-

-

Technology Outlook (Revenue, USD Million; 2021 - 2033)

-

Reverse Osmosis

-

Ultrafiltration

-

Microfiltration

-

Nanofiltration

-

-

Application Outlook (Revenue, USD Million; 2021 - 2033)

-

Water & Wastewater

-

Food & Beverage

-

Pharmaceutical

-

Industrial Processing

-

Other

-

- Regional Outlook (Revenue, USD Million; 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

The regional segmentation customization maps the membrane filtration market by identifying country-level demand patterns across municipal water treatment, industrial process separation, pharmaceutical purification, and food & beverage filtration applications. It evaluates how factors such as freshwater scarcity, industrial concentration, desalination investments, and wastewater reuse mandates influence membrane adoption across each region.

This allows the client to identify not only where demand exists, but also why certain regions are becoming stronger procurement centers for membrane systems. It improves strategic planning for sales expansion, channel partnerships, and manufacturing allocation by linking regional demand directly to end-use industry growth and policy-driven infrastructure investments.

Competitive Benchmarking

The competitive benchmarking customization analyzes leading and emerging membrane filtration companies based on technology specialization, membrane lifespan performance, application focus, service capabilities, and penetration across sectors such as desalination, biopharmaceuticals, and industrial wastewater recovery.

This helps the client understand where competitors create real commercial advantage and where differentiation can be realistically built.

Opportunity Assessment

The opportunity assessment customization identifies future revenue pockets by evaluating fast-developing use cases such as zero liquid discharge systems, ultrapure water production, decentralized wastewater treatment, and membrane-based recovery systems for high-value industrial processes. It also assesses adoption potential in sectors with rising compliance pressure and water reuse targets.

This helps the client direct investments toward applications with stronger profitability and longer replacement cycles rather than only high-volume segments. It supports portfolio expansion and innovation planning by highlighting where membrane adoption is shifting from optional efficiency upgrades to critical operational requirements.

Frequently Asked Questions About This Report

The water & wastewater segment led with a 41.7% revenue share in 2025.

Spiral wound held the largest revenue share 45.8 % in 2025.

Polymeric held the largest share (over 86.8%) in 2025.

Asia Pacific dominated with a 36.5% revenue share in 2025.

The reverse osmosis segment dominated the market with a revenue share of 36.3 % in 2025.

The global membrane filtration market size was estimated at USD 19.4 billion in 2025 and is expected to reach USD 20.7 billion in 2026.

The membrane filtration market, in terms of revenue, is expected to grow at a compound annual growth rate of 7.8% from 2026 to 2033 and reach USD 35.0 billion by 2033.

Some of the key players operating in the membrane filtration market include Alfa Laval, GEA Group, DuPont, Pall Corporation, Veolia, 3M, Pentair, Porvair Filtration Group, Donaldson Company, Inc., MMS Membrane Systems, Koch Separation Solutions, ProMinent, SPX Flow, TORAY INDUSTRIES, INC.., MANN+HUMMEL.

Key factors driving the membrane filtration market include rising water scarcity, stringent environmental regulations, growing demand for clean and safe water, industrialization, and wastewater treatment needs. Technological advancements, energy-efficient membranes, and increasing applications in pharmaceuticals, food & beverage, and chemicals further accelerate market growth globally.

About the Author(s)

Water & Sludge Treatment Research Team

Bulk Chemicals · Water & Sludge TreatmentThis report was authored by the water & sludge treatment research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the water & sludge treatment segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.