- Home

- »

- Plastics, Polymers & Resins

- »

-

Microplastics Market Size, Growth Report, 2026-2033GVR Report cover

![Microplastics Market (2026 - 2033)Report]()

Microplastics Market (2026 - 2033)

Size, Share & Trends Analysis Report By Source (Primary Microplastics, Secondary Microplastics), By Polymer Type (PE, PP, PS, PET), By End-use (Consumer Goods, Building & Construction, Automotive, Packaging, Textile), By Region, And Segment Forecasts

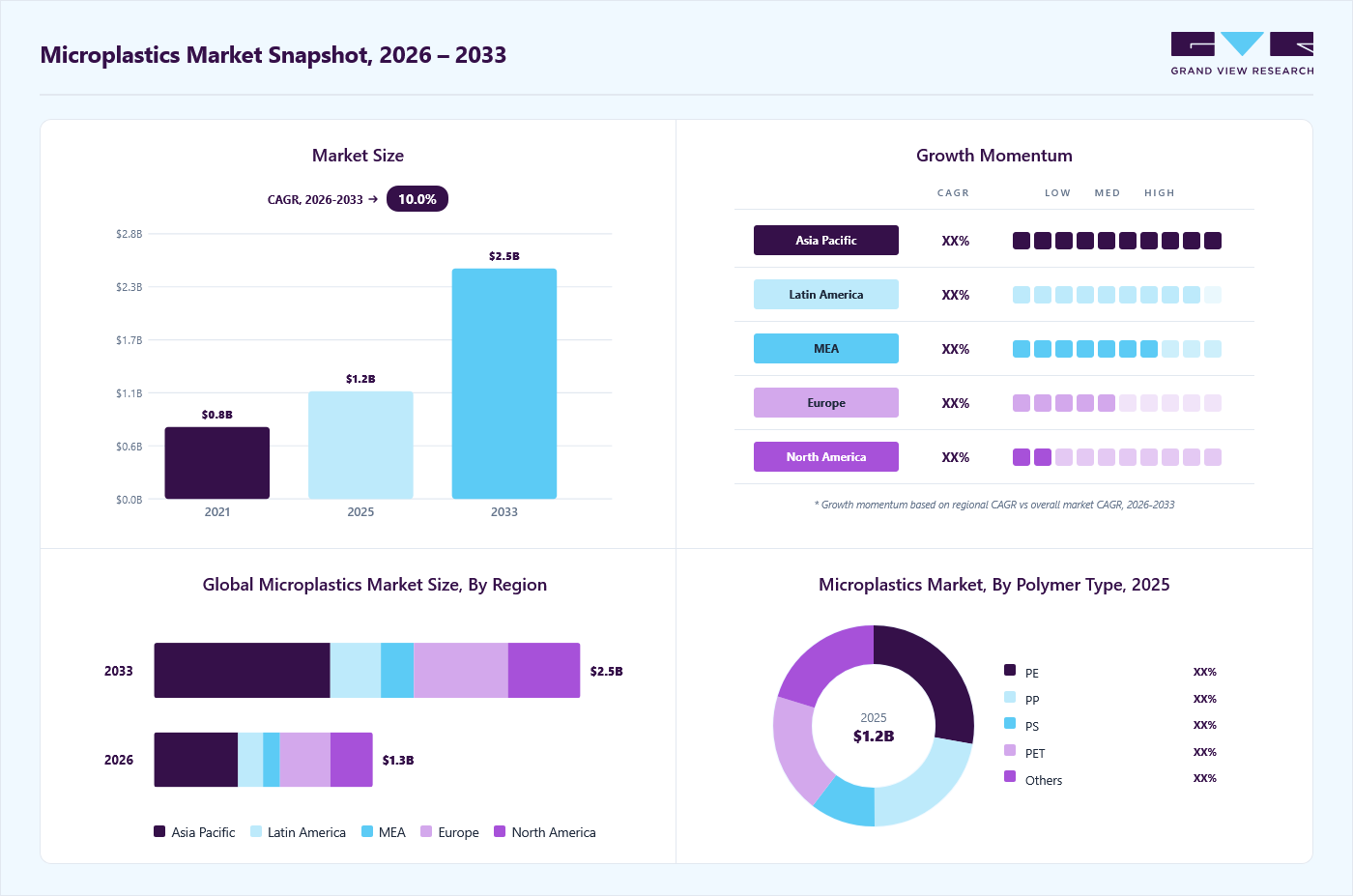

Market Size, 2025

$1.2BMarket Estimate, 2026

$1.3BMarket Forecast, 2033

$2.5BCAGR, 2026–2033

10.0%Microplastics Market Summary

The global microplastics market size was valued at USD 1.2 billion in 2025 and is projected to grow from USD 1.3 billion in 2026 to USD 2.5 billion by 2033, at a CAGR of 10.0% from 2026 to 2033. Asia Pacific dominated the global market, accounting for the largest revenue share of 38.0% in 2025.. Growing industrial use of plastic materials across packaging, textiles, automotive, and consumer goods is increasing the generation of secondary microplastics during product life cycles and disposal, driving the market growth.

Key Market Trends & Insights

- By source: Primary microplastics segment is anticipated to grow at a CAGR of 10.8% from 2026 to 2033.

- By polymer type: PE segment is expected to grow at a CAGR from 10.9% from 2026 to 2033 in terms of revenue.

- By end use: Textile segment is expected to grow at a CAGR of 10.0% from 2026 to 2033 in terms of revenue.

Regional Highlights

- Largest regional market: Asia Pacific (38.0% revenue share, 2025)

- By country: The India microplastics industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 1.2 Billion

- Estimated market size in 2026: USD 1.3 Billion

- Projected market size by 2033: USD 2.5 Billion

- CAGR (2026-2033): 10.0%

The microplastics industry is undergoing a structural transition from conventional synthetic microparticles toward biodegradable and bio-based substitutes. Regulatory bans on intentionally added microplastics in cosmetics, detergents, and coatings are accelerating substitution across end-use industries. Simultaneously, demand for advanced detection and removal technologies is rising, particularly in water treatment and industrial effluents. Innovation is concentrated in membrane filtration, enzymatic degradation, and bio-based materials, indicating a shift from volume-driven consumption to technology-led mitigation and replacement solutions.

")

Drivers, Opportunities & Restraints

The primary growth driver for the microplastics market is the convergence of regulatory enforcement and rising environmental and health concerns. Governments are introducing strict policies targeting microplastic emissions, while public awareness of contamination in water, food, and human systems is intensifying. According to OECD, up to 3 million tons of microplastics enter the environment annually, reinforcing the urgency for mitigation solutions. This has increased investments in wastewater treatment upgrades, filtration systems, and monitoring technologies, creating sustained demand across municipal and industrial applications.

A significant opportunity lies in the commercialization of microplastic removal and alternative material technologies. Advanced filtration systems are being integrated into municipal infrastructure, while biological degradation methods are emerging as high-growth segments. In parallel, the transition toward biodegradable polymers and natural substitutes in personal care and agriculture is creating new revenue pools. Early-stage innovation, combined with regulatory support, is enabling new entrants and specialized solution providers to scale in niche yet high-value segments.

High capital intensity and technological limitations remain key constraints. Microplastic detection, separation, and recycling processes require advanced infrastructure and are often energy-intensive, limiting large-scale deployment. Many solutions remain at pilot or early commercialization stages, creating scalability challenges. High investment requirements and operational complexity restrict adoption among smaller municipalities and industries. Additionally, the heterogeneous nature and small size of microplastics complicate efficient collection and processing, delaying cost optimization and widespread implementation.

Market Concentration & Characteristics

The market growth stage is high, and the pace of growth is accelerating. The market exhibits consolidation, with key players dominating the industry landscape. Major companies such as Lamberti S.p.A., Cospheric LLC, Applied Microspheres GmbH, EPRUI Biotech Co., Ltd., Nanjing Chemical Material Corp., Bangs Laboratories, Inc., Polysciences, Inc., and others play a significant role in shaping the market dynamics. These leading players often drive innovation in the market by introducing new products, technologies, and materials to meet the industry's evolving demands.

The microplastics market demonstrates moderate to high innovation intensity, primarily concentrated in detection, filtration, and material substitution technologies. Advanced filtration systems, including membrane-based and multi-stage separation technologies, are being refined for higher efficiency and scalability, although standardization gaps persist. According to OECD, filtration solutions are commercially available but lack uniform performance benchmarks, limiting large-scale adoption. At the same time, innovation is expanding into biodegradable polymers and enzymatic degradation methods, indicating a gradual shift from mitigation-focused solutions toward preventive material redesign across industrial value chains.

Regulatory frameworks are exerting a strong structural impact on the microplastics industry by reshaping product design, manufacturing practices, and supply chain compliance. The introduction of restrictions on intentionally added microplastics under REACH, and the 2025 regulation on plastic pellet loss prevention are driving mandatory risk management and reporting across industries. These policies are accelerating the phase-out of conventional microplastics in consumer applications while stimulating investments in alternatives and containment technologies, thereby directly influencing market demand patterns and innovation priorities.

Source Insights

The secondary microplastics segment dominated the market, accounting for a revenue share of 70.9% in 2025, and is forecast to grow at a 9.6% CAGR from 2026 to 2033. Secondary microplastics are being driven by the continued fragmentation of post-consumer plastic waste across marine, urban, and agricultural environments. Rising consumption of short-life plastic products in flexible packaging, synthetic textiles, and disposable goods is increasing long-term particle generation after disposal. Environmental monitoring programs are identifying higher concentrations of fragmented polyethylene and polypropylene particles in wastewater and soil streams, which is expanding demand for analytical testing and removal technologies. The segment is also gaining policy attention because secondary particles account for a large share of uncontrolled microplastic contamination across global ecosystems.

The primary microplastics segment is expected to grow at a 10.8% CAGR over the forecast period. The segment growth is supported by industrial demand for engineered microparticles that deliver controlled performance in specialized applications. These particles are still used in coatings, personal care formulations, abrasive media, and industrial additives, where particle-size consistency is critical. Although regulations are tightening in consumer applications, industrial users continue to require precision polymer beads for product stability and surface performance. Demand is shifting toward traceable, lower-impact formulations, driving growth in premium-grade materials that comply with evolving environmental standards without reducing formulation efficiency.

Polymer Type Insights

The PE segment dominated the microplastics market, accounting for a revenue share of 27.9% in 2025, and is forecast to grow at a 10.9% CAGR from 2026 to 2033. Polyethylene remains a major polymer segment because of its dominant use in films, containers, agricultural sheets, and consumer packaging. Its high production volume creates a large base for microplastic generation through weathering, abrasion, and waste leakage. Recent environmental sampling continues to show polyethylene among the most frequently detected polymers in surface water and sediment. This prevalence is increasing investment in polymer-specific detection methods and recovery systems. The segment is further supported by the need to monitor polyethylene particles, given their widespread presence in industrial and municipal waste streams.

The PP segment is expected to expand at a 10.5% CAGR over the forecast period. Polypropylene demand is driven by its growing use in automotive components, nonwoven fabrics, food containers, and household products. The polymer’s low density allows particles to remain suspended in water for longer periods, making it a priority in environmental monitoring programs. Research activity on polypropylene degradation has increased, as UV exposure and mechanical wear accelerate particle release from durable goods. This is creating demand for improved filtration systems and polymer identification tools, particularly in wastewater treatment and industrial discharge management applications.

End-use Insights

The consumer goods segment led the microplastics industry, accounting for a revenue share of 30.8% in 2025, and is projected to grow at a 10.9% CAGR from 2026 to 2033. In consumer goods, microplastics are used as functional microspheres and polymer particles to enhance product performance and aesthetics. Applications include personal care formulations in which microbeads act as exfoliants or texture modifiers, as well as in cosmetics for light diffusion and a smooth finish. They are also used in household products such as polishes and detergents for controlled abrasiveness. The need for consistent particle size, low cost, and formulation stability drives their use. Demand persists in non-restricted applications despite increasing regulatory scrutiny on rinse-off products.

The building & construction segment is expected to grow at the fastest CAGR of 10.5% over the forecast period. In the building and construction industry, microplastics are incorporated into coatings, paints, sealants, and insulation materials as polymer microspheres and fine particles. These particles improve properties such as crack resistance, thermal insulation, weight reduction, and surface finish. Expandable microspheres are widely used to reduce density in plasters and coatings while maintaining structural performance. The need for lightweight materials, energy-efficient construction, and durability enhancement drives the segment growth. Increasing infrastructure development and the adoption of advanced construction chemicals continue to support their application across residential and commercial projects.

Regional Insights

The Asia Pacific microplastics market held the largest revenue share of 38.0% in 2025. The region is expected to grow at a CAGR of 11.1% over the forecast period. Asia Pacific is experiencing strong growth, driven by large-scale manufacturing and cost-efficient polymer processing. Microplastics are widely used as raw materials for packaging films, textiles, and consumer goods due to their versatility and low processing costs. Rapid urbanization and the expansion of e-commerce are increasing the demand for flexible packaging, directly supporting microplastic consumption. The region’s dominance is supported by a large consumer base and the expansion of end-use industries such as packaging and textiles, which require a consistent supply of polymer microparticles for mass production.

The China microplastics market is expected to grow during the forecast period. China’s demand is anchored in its integrated plastics value chain and export-oriented manufacturing. Microplastics are widely used in synthetic textiles, coatings, and molded components due to their scalability and compatibility with high-throughput processing systems. Government-led industrial policies supporting advanced materials and recycling are improving the domestic availability of secondary microplastics. In addition, strong growth in the electronics, automotive, and packaging sectors continues to drive demand for polymer microparticles as cost-effective raw materials for lightweight, durable product manufacturing.

North America Microplastics Market Trends

Advanced manufacturing ecosystems and high-value applications drive demand for microplastics as functional raw materials. Strong consumption in packaging, automotive, and consumer goods sustains volume uptake, particularly for engineered polymer microparticles used in coatings, lightweight components, and performance additives. Regulatory pressure has shifted usage toward controlled industrial applications and recycled microplastics. Mature recycling infrastructure and sustainability mandates are accelerating integration of secondary microplastics into production cycles, supporting circular material flows and consistent feedstock availability.

U.S. Microplastics Market Trends

The U.S. microplastics industry is characterized by high innovation intensity and application-specific demand. Microplastics are increasingly utilized in specialty coatings, 3D printing powders, and advanced composites for the aerospace and automotive sectors. Regulatory actions, such as microbead bans, have redirected use away from personal care toward industrial and packaging applications. At the same time, investments in chemical recycling and polymer recovery technologies are improving the quality of microplastic feedstock, enabling its use as a substitute for virgin resins in high-performance applications.

Europe Microplastics Market Trends

Europe’s market is shaped by stringent environmental regulations and circular economy targets. While restrictions limit intentional use in certain applications, demand persists in industrial uses such as coatings, paints, and engineered plastics, where performance requirements are critical. Packaging, construction, and automotive sectors account for a major share of plastic consumption, indirectly sustaining demand for microplastic-based raw materials. Regulatory frameworks are simultaneously driving a transition toward recycled and bio-based microplastics, fostering innovation in sustainable material formulations.

Key Microplastics Company Insights

The microplastics industry is highly competitive, with several key players dominating the landscape. Major companies in the market include Lamberti S.p.A.; Cospheric LLC; Applied Microspheres GmbH; EPRUI Biotech Co., Ltd.; Nanjing Chemical Material Corp.; Bangs Laboratories, Inc.; and Polysciences, Inc. The market is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their products.

Key Microplastics Companies:

The following key companies have been profiled for this study on the microplastics market.

- Lamberti S.p.A.

- Cospheric LLC

- Applied Microspheres GmbH

- EPRUI Biotech Co., Ltd.

- Nanjing Chemical Material Corp.

- Bangs Laboratories, Inc.

- Polysciences, Inc.

Recent Developments

-

In June 2025, Eastman launched Esmeri CC1N10, a readily biodegradable cellulose ester micropowder for color cosmetics. The ingredient is designed to replace synthetic polymer microparticles in lipsticks, foundations, and pressed powders, delivering soft-focus effects, improved color payoff, and uniform coverage.

-

In March 2025, Daicel introduced BELLOCEA BS7, an eco-friendly cosmetic texture improver based on cellulose acetate spherical particles. The product is positioned as a substitute for microbeads in cosmetics and is aimed at applications such as foundations, where softness, surface smoothness, and biodegradability must be balanced.

Microplastics Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 1.3 billion

Revenue forecast in 2033

USD 2.5 billion

Growth rate

CAGR of 10.0% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue & volume forecast, competitive landscape, growth factors, and trends

Segments covered

Source, polymer type, end-use, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Europe; Germany; UK; France; Italy; Spain; China; India; Japan; South Korea; Australia; Brazil; Argentina; Saud Arabia; UAE; South Africa

Key companies profiled

Lamberti S.p.A.; Cospheric LLC; Applied Microspheres GmbH; EPRUI Biotech Co., Ltd.; Nanjing Chemical Material Corp.; Bangs Laboratories, Inc.; Polysciences, Inc.

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Microplastics Market Report Segmentation

This report forecasts volume & revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global microplastics market report based on source, polymer type, end-use, and region:

-

Source Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Primary Microplastics

-

Secondary Microplastics

-

-

Polymer Type Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

PE

-

PP

-

PS

-

PET

-

Others

-

-

End-use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Textile

-

Packaging

-

Consumer Goods

-

Building & Construction

-

Automotive

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global microplastics market size was valued at USD 1.2 billion in 2025 and is estimated at USD 1.3 billion for 2026.

The global microplastics market is expected to grow at a CAGR of 10.0% from 2026 to 2033, reaching USD 2.5 billion by 2033.

The secondary microplastics segment dominated the market across source segmentation in terms of revenue, accounting for 70.9% market share in 2025, and is forecast to grow at a 9.6% CAGR from 2026 to 2033.

Key players include Lamberti S.p.A.; Cospheric LLC; Applied Microspheres GmbH; EPRUI Biotech Co., Ltd.; Nanjing Chemical Material Corp.; Bangs Laboratories, Inc.; Polysciences, Inc.

Growing industrial use of plastic materials across packaging, textiles, automotive, and consumer goods is increasing the generation of secondary microplastics during product life cycles and disposal, driving the market.

Asia Pacific dominated with a 38.0% revenue share in 2025.

PE segment dominated the market and accounted for the largest revenue share of 27.9% in 2025.

Consumer goods segment held the largest share (over 30.0%) in 2025, while building & construction is the fastest-growing segment.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.