- Home

- »

- Clothing, Footwear & Accessories

- »

-

Musical Instrument Market Size & Share Report, 2026-2033GVR Report cover

![Musical Instrument Market (2026 - 2033)Report]()

Musical Instrument Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Stringed, Percussion, Wind, Keyboard), By Distribution Channel (Online, Offline), By Region (North America, Europe, APAC, Central & South America, MEA), And Segment Forecasts

Market Size, 2025

$17.5BMarket Estimate, 2026

$18.8BMarket Forecast, 2033

$31.4BCAGR, 2026–2033

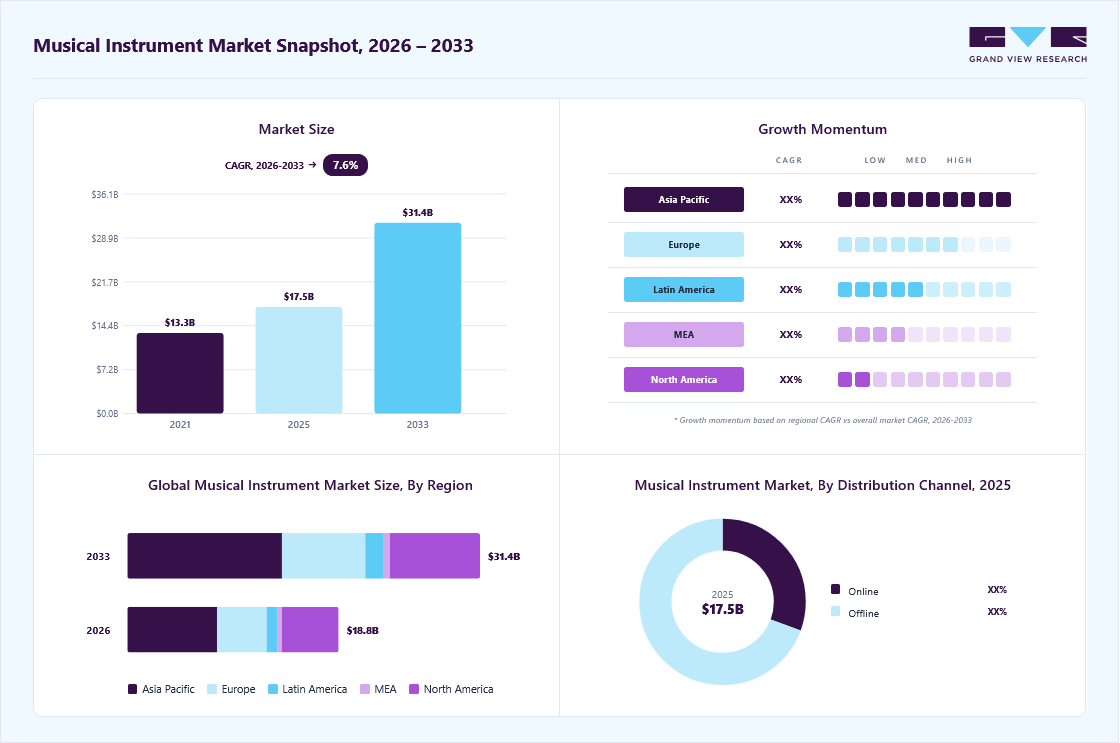

7.6%Musical Instrument Market Summary

The global musical instrument market size was valued at USD 17.5 billion in 2025 and is projected to grow from USD 18.8 billion in 2026 to USD 31.4 billion by 2033, at a CAGR of 7.6% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 42.2% in 2025. The global market is increasingly shaped by demand for structured skill development, creative expression, and long-term engagement, rather than casual or novelty-driven use.

Key Market Trends & Insights

- By type: Stringed instruments segment held the largest market share of 64.9% in 2025.

- By distribution channel: Offline channel segment held the largest market share of 69.5% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (42.2% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 17.5 Billion

- Estimated market size in 2026: USD 18.8 Billion

- Projected market size by 2033: USD 31.4 Billion

- CAGR (2026-2033): 7.6%

Consumers across age groups are investing in instruments as tools for learning, performance, and emotional well-being, supported by growing participation in formal music education, private tutoring, and self-guided practice. Entry-level instruments, practice-oriented models, and culturally significant instruments continue to see sustained demand as music is positioned as a lifelong skill rather than a short-term hobby.Purchasing behavior in the musical instrument industry is strongly influenced by learning outcomes, progression potential, and instructional support. Parents and adult learners favor instruments that can accommodate different proficiency levels and offer clear pathways for improvement, whether through graded learning systems, teacher-led instruction, or digital lesson integration. This trend benefits both modern instruments with app-based guidance and traditional categories such as the Mridangam market, where demand is closely tied to classical music training, certification programs, and performance-based learning structures.

")

Technology and content ecosystems are also reshaping the market by enhancing accessibility and engagement. Online tutorials, virtual classes, performance-sharing platforms, and influencer-led instruction are playing a critical role in instrument discovery and skill acquisition. At the same time, consumers place increasing emphasis on build quality, tonal consistency, durability, and cultural authenticity, particularly for acoustic and traditional instruments. As a result, manufacturers are balancing innovation with craftsmanship, ensuring that both digital-enabled instruments and heritage categories like mridangam remain relevant in a market driven by learning depth, emotional connection, and sustained musical practice. For instance, in September 2025, Yamaha announced a major refresh of its SILENT Cello lineup with the launch of the SVC300 Series, the first full redesign in nearly 20 years. The new models use Yamaha’s SRT Powered System to deliver a more realistic acoustic cello sound while retaining the benefits of quiet practice and flexible performance. Designed for advanced and professional players, the series focuses on improved tonal depth, natural response, and modern playability in noise-sensitive settings.

Manufacturers and distribution channels play a central role in shaping the structure and accessibility of the musical instrument industry, with clear differentiation between global brands, regional specialists, and traditional instrument makers. Large manufacturers focus on scale, product standardization, and global reach, supplying instruments through authorized dealers, music specialty stores, and institutional channels such as schools and academies. At the same time, artisan-led producers and heritage instrument makers, particularly in segments such as the mridangam market, operate through localized workshops, teacher networks, and cultural institutions where craftsmanship, tonal quality, and authenticity are critical purchase criteria. On the distribution side, physical music stores remain essential for instrument trials, tuning support, and expert guidance, while online channels and direct-to-consumer platforms are expanding reach by offering detailed product information, instructional content, and access to a wider range of price points.

Consumer Insights

Consumer behavior in the market reflects a clear shift toward purpose-driven ownership, where instruments are purchased with defined learning, performance, or cultural objectives rather than casual experimentation. Buyers increasingly enter the category through formal pathways such as music schools, private tutors, certification programs, religious or cultural institutions, and online learning platforms, making instructional compatibility and progression capability central to purchase decisions. First-time buyers prioritize ease of learning and tuning stability, while repeat and upgrade buyers focus on tonal accuracy, craftsmanship, and long-term playability.

Consumers rely heavily on teacher recommendations, performance demonstrations, peer comparisons, and recorded sound samples before committing to purchase, particularly for mid- to high-value instruments. Physical trial remains important for acoustic instruments, but digital discovery has become influential through tutorial videos, performance recordings, and side-by-side comparisons that highlight sound quality and build standards. Instruments perceived as disposable, difficult to maintain, or lacking a clear skill-development path tend to see lower repeat adoption.

Spending patterns indicate a willingness to invest when instruments are positioned as durable learning assets rather than short-term purchases. Entry-level demand is strong, but consumers show higher lifetime value when instruments support skill progression, resale potential, and reparability. In traditional segments, including classical and regional instruments, buyers place added importance on authenticity, material sourcing, and alignment with established pedagogy.

Type Insights

Based on type, stringed instruments market led the market with the largest revenue share of 64.9% in 2025. Instruments such as guitars, violins, and basses continue to be widely adopted due to their adaptability across multiple genres and skill levels, making them suitable for beginners as well as advanced players. Stringed instruments offer strong expressive range and immediate tonal feedback, which supports sustained practice and creative experimentation over time. Their prominence is further reinforced by extensive availability of learning resources, including formal instruction, digital tutorials, and hybrid learning platforms that enable self-paced skill development.

The percussion instrument segment is anticipated to grow at the fastest CAGR of 7.6% from 2026 to 2033, supported by their expanding role in live performance, studio recording, and contemporary music production. Instruments such as acoustic drum kits, hand percussion, electronic drums, and hybrid percussion systems are witnessing higher adoption across genres including rock, pop, jazz, fusion, worship music, and electronic music. Demand is being reinforced by the growth of live events, independent music creation, and content-driven performance formats, where rhythm-centric instruments form the backbone of ensemble sound.

Distribution Channel Insights

Sale of musical instrument through offline channels led the market with the largest revenue share of 69.5% in 2025. Consumers continue to prefer physical stores because instruments require hands-on evaluation of sound quality, build finish, weight balance, and playability, factors that are difficult to assess through online listings alone. Offline music stores and specialty retailers support this preference through live demonstrations, sound trials, instrument tuning assistance, and expert guidance from trained staff. The ability to compare multiple brands, models, and price tiers in real time, along with immediate product availability and after-sales services such as maintenance and repairs, continues to reinforce offline channels as the dominant sales route in the global market.

The online sales of musical instrument are projected to grow at the substantial CAGR of 8.9% from 2026 to 2033, reflecting changing purchase behavior and greater comfort with digital evaluation of higher-value instruments. Consumers increasingly use online channels to assess detailed specifications such as sound profiles, electronic features, connectivity options, and compatibility with recording or practice software, supported by demo videos, professional reviews, and verified user feedback. Online platforms also enable quicker access to newly launched electronic instruments, digital keyboards, electronic drum kits, and hybrid models that may have limited physical retail presence.

Regional Insights

North America Musical Instrument Market Trends

North America musical instrument industry accounted for a revenue share of 27.1% in 2025. The U.S. and Canada host a dense ecosystem of live venues, recording studios, churches, schools, and independent artists, which sustains consistent demand for guitars, keyboards, percussion, and electronic instruments. North America also leads in home-studio adoption, with musicians investing in instruments that integrate easily with recording software, audio interfaces, and streaming platforms. In addition, the region shows high uptake of premium and mid-range instruments, supported by a mature retail landscape of specialty music stores, brand flagships, and omnichannel distributors.

U.S. Musical Instrument Market Trends

The musical instrument industry in the U.S. is expected to grow at a CAGR of 6.9% from 2026 to 2033. Demand in the U.S. is increasingly shaped by musicians seeking instruments that integrate seamlessly with recording software, streaming platforms, and live performance setups, particularly across guitars, keyboards, electronic drums, and hybrid instruments. Manufacturers are focusing on improved sound modeling, connectivity with digital audio workstations, and modular hardware designs that support customization and long-term use. In addition, U.S. consumers place high value on build quality, reliability, and upgrade potential, encouraging brands to invest in durable materials, efficient electronics, and firmware-based feature updates.

The musical instrument industry in Canada is expected to grow at a CAGR of 7.1% from 2026 to 2033. Canadian musicians increasingly favor instruments that offer compatibility with digital audio workstations, home-studio setups, and live performance systems, particularly across guitars, keyboards, electronic drums, and hybrid instruments. Demand is reinforced by the country’s strong culture of local gigs, community performances, and small-scale studio production, which encourages investment in versatile and reliable instruments. Manufacturers serving the Canadian market are emphasizing sound accuracy, cold-climate durability, modular components, and long product lifecycles, aligning with consumer expectations for performance consistency and value retention.

Europe Musical Instrument Market Trends

Europe musical instrument industry accounted for a revenue share of 23.6% in 2025. Europe benefits from a well-established retail and distribution ecosystem comprising specialty music stores, independent instrument dealers, conservatories, and brand-authorized outlets, ensuring broad accessibility across both Western and Central European countries. Consumer demand is shaped by high standards for craftsmanship, tonal quality, and material authenticity, particularly for stringed, keyboard, and acoustic instruments. In addition, Europe shows strong adoption of instruments aligned with ensemble performance, orchestral participation, and live events, while growing interest in home studios and recording-compatible instruments is supporting demand for electronic and hybrid formats.

The musical instrument industry in the UK accounted for a revenue share of 18.9% of the Europe revenue in 2025. The UK benefits from a dense network of specialty music retailers, independent instrument dealers, conservatoires, and brand-authorized stores, which ensures wide availability of instruments across major cities and regional hubs. Consumer demand is strongly influenced by expectations around craftsmanship, tonal clarity, and material quality, particularly for guitars, keyboards, pianos, and acoustic instruments.

The musical instrument industry in Germany is expected to grow at a CAGR of 7.3% from 2026 to 2033. Germany benefits from a well-established network of specialty music retailers, independent instrument makers, conservatories, and brand-authorized dealers that ensure broad access to musical instrument across major cities and regional centers. Consumer purchasing decisions are heavily influenced by expectations around craftsmanship, tonal accuracy, durability, and material authenticity, particularly for pianos, keyboards, stringed instruments, and high-quality acoustic products.

Asia Pacific Musical Instrument Market Trends

Asia Pacific musical instrument market dominated with revenue share 42.2% in 2025 and is expected to grow at the fastest CAGR of 8.1% from 2026 to 2033. Consumers are increasingly investing in instruments such as guitars, keyboards, electronic drums, and hybrid instruments that support recording, live performance, and digital integration. Rising smartphone penetration and widespread access to online platforms are accelerating discovery of instruments through tutorials, performance videos, and musician-led social media content, particularly among younger users in China, India, Southeast Asia, and other high-growth markets. In addition, rapid expansion of e-commerce, improving retail infrastructure, and growing exposure to global music trends are strengthening adoption across both entry-level and mid-range instruments, positioning Asia Pacific as one of the most dynamic regions in the global musical instrument industry.

The musical instrument industry in China accounted for a revenue share of 43.1% of the Asia Pacific revenue in 2025. Consumers actively purchasing guitars, keyboards, electronic drums, and hybrid instruments that can be used for live performances, studio recording, and digital music production. Instrument discovery and purchase decisions are heavily influenced by short-video platforms, livestream demonstrations, and musician-led social commerce, which play a central role in shaping trends among younger urban consumers.

The musical instrument industry in India is expected to grow at the fastest CAGR of 9.2% from 2026 to 2033. Rising participation in live gigs, studio sessions, temple and event performances, and social-media-led music creation is encouraging purchases of instruments that support recording, amplification, and portability. Growth is further supported by widespread smartphone usage and strong reliance on YouTube, Instagram, and short-video platforms for learning songs, discovering instruments, and following local musicians.

Central And South America Musical Instrument Market Trends

Central and South America musical instrument industry is expected to grow at the fastest CAGR of 7.3% from 2026 to 2033, supported by strong regional engagement with live music, performance-led genres, and community-based music culture. Consumers across the region are increasingly investing in guitars, keyboards, percussion, and electronic or hybrid instruments that are suitable for live performances, rehearsals, and informal recording environments. High participation in genres such as Latin pop, regional folk, gospel, and contemporary fusion continues to sustain demand for rhythm- and melody-focused instruments.

Middle East And Africa Musical Instrument Market Trends

Middle East and Africa musical instrument industry is expected to grow at the fastest CAGR of 7.1% from 2026 to 2033, supported by rising demand linked to live performance, cultural expression, and expanding entertainment activity across the region. Consumer spending is increasingly directed toward instruments such as guitars, keyboards, percussion, and amplified instruments that are suited for stage performance, worship settings, community events, and contemporary music formats. Growing exposure to global music trends through digital platforms and social media is influencing purchasing behavior, particularly among younger urban consumers who engage in live performances, informal recording, and content creation.

Key Musical Instrument Company Insights

The global musical instrument industry is characterized by the presence of well-established instrument manufacturers alongside a growing number of technology-driven and digitally native brands, all competing to address evolving consumer expectations around learning depth, sound quality, and engagement. Companies are increasingly developing smart and hybrid instruments that combine traditional craftsmanship with digital capabilities such as app-based learning, real-time feedback, connectivity, and adaptive practice modes. These innovations are designed to enhance skill acquisition, sustain long-term engagement, and support self-guided as well as instructor-led learning. At the same time, manufacturers continue to focus on improving build quality, tonal consistency, durability, and ergonomic design, positioning musical instrument as long-term skill-development tools and creative assets rather than short-term recreational products.

Key Musical Instrument Companies:

The following key companies have been profiled for this study on the musical instrument market.

- Casio Computer Co., Ltd.

- C.F. Martin & Co., Inc.

- D'addario & Company, Inc.

- Eastman Music Company

- Fender Musical Instrument Corporation

- Kawai Musical Instrument Mfg. Co., Ltd.

- Roland Corporation

- Steinway & Sons

- Yamaha Corporation

- Yanagisawa Wind Instruments Co., Ltd.

Recent Developments

-

In January 2026, Walmart expanded its online marketplace into premium musical instrument by launching a dedicated digital shop featuring established global brands. The new offering includes higher-quality guitars, drums, amplifiers, and accessories aimed at serious hobbyists and professional musicians, marking a move beyond entry-level music products. This expansion reflects Walmart Marketplace’s strategy to attract more specialized sellers and broaden its assortment into higher-value, passion-driven categories while leveraging its large online customer base.

-

In January 2026, Grammy-winning artist Molly Tuttle collaborated with C. F. Martin & Co. to introduce two signature acoustic guitars at the 2026 NAMM Show. The partnership resulted in one premium dreadnought model inspired by the sound and feel of her vintage instrument, alongside a more accessible version designed to reflect her preferred playability and comfort. Together, the launches aim to bring Tuttle’s musical style and tonal preferences to a broad range of players through distinct design details and performance-focused features.

Musical Instrument Market Report Scope

Report Attribute

Details

Market size in 2025

USD 17.5 billion

Estimated Market size in 2026

USD 18.8 billion

Projected Market size by 2033

USD 31.4 billion

Growth Rate

CAGR of 7.6% from 2026 to 2033

Actuals

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; Australia & New Zealand; South Korea; Brazil; South Africa

Key companies profiled

Casio Computer Co., Ltd.; C.F. Martin & Co., Inc.; D'addario & Company, Inc.; Eastman Music Company; Fender Musical Instrument Corporation; Kawai Musical Instrument Mfg. Co., Ltd.; Roland Corporation; Steinway & Sons; Yamaha Corporation; Yanagisawa Wind Instruments Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Musical Instrument Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global musical instrument market report based on type, distribution channel, and region.

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Stringed Instruments

-

Guitar

-

Violin

-

Cello

-

Others

-

-

Percussion Instruments

-

Drum Set

-

Tabla

-

Cajón

-

Others

-

-

Wind Instruments

-

Saxophone

-

Flute

-

Harmonica

-

Others

-

-

Keyboard Instruments

-

Piano

-

Accordion

-

Keyboard

-

Others

-

-

Others

-

-

Distribution Channel Outlook (Revenue, USD Million, 2021 - 2033)

-

Online

-

Offline

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia & New Zealand

-

South Korea

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa

-

South Africa

-

-

Frequently Asked Questions About This Report

Some key players operating in the musical instruments market include Casio Computer Co., Ltd., C.F. Martin & Co., Inc., D'addario & Company, Inc., Eastman Music Company, Fender Musical Instruments Corporation, Kawai Musical Instruments Mfg. Co., Ltd., and Roland Corporation.

Key factors that are driving the market growth include the rising number of music hobbyists worldwide and the increasing popularity of traditional folklore music in countries such as India and Indonesia.

The stringed instruments segment led with a 64.9% revenue share in 2025, while the percussion instrument segment is the fastest-growing.

The offline channels segment led with a 69.5% revenue share in 2025, while the online sales segment is projected to grow at the substantial CAGR of 8.9% from 2026 to 2033.

The global musical instrument market size was estimated at USD 17.5 billion in 2025 and is expected to reach USD 18.8 billion in 2026.

The global musical instrument market is expected to grow at a compound annual growth rate of 7.6% from 2026 to 2033 to reach USD 31.4 billion by 2033.

Asia Pacific dominated the musical instruments market with a share of 42.2% in 2025. This is attributable to the rising influence of western music in countries such as China, Japan, and India.

About the Author(s)

Clothing, Footwear & Accessories Research Team

Consumer Goods · Clothing, Footwear & AccessoriesThis report was authored by the clothing, footwear & accessories research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clothing, footwear & accessories segment of the consumer goods industry. All findings are based on proprietary consumer goods databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.