- Home

- »

- Medical Devices

- »

-

Neurodiagnostics Market Size & Share Report, 2026-2033GVR Report cover

![Neurodiagnostics Market (2026 - 2033)Report]()

Neurodiagnostics Market (2026 - 2033)

Size, Share & Trends Analysis Report By Technology (Neuroimaging Technologies (Computed Tomography, Magnetic Resonance Imaging)), By End Use, By Region, And Segment Forecasts

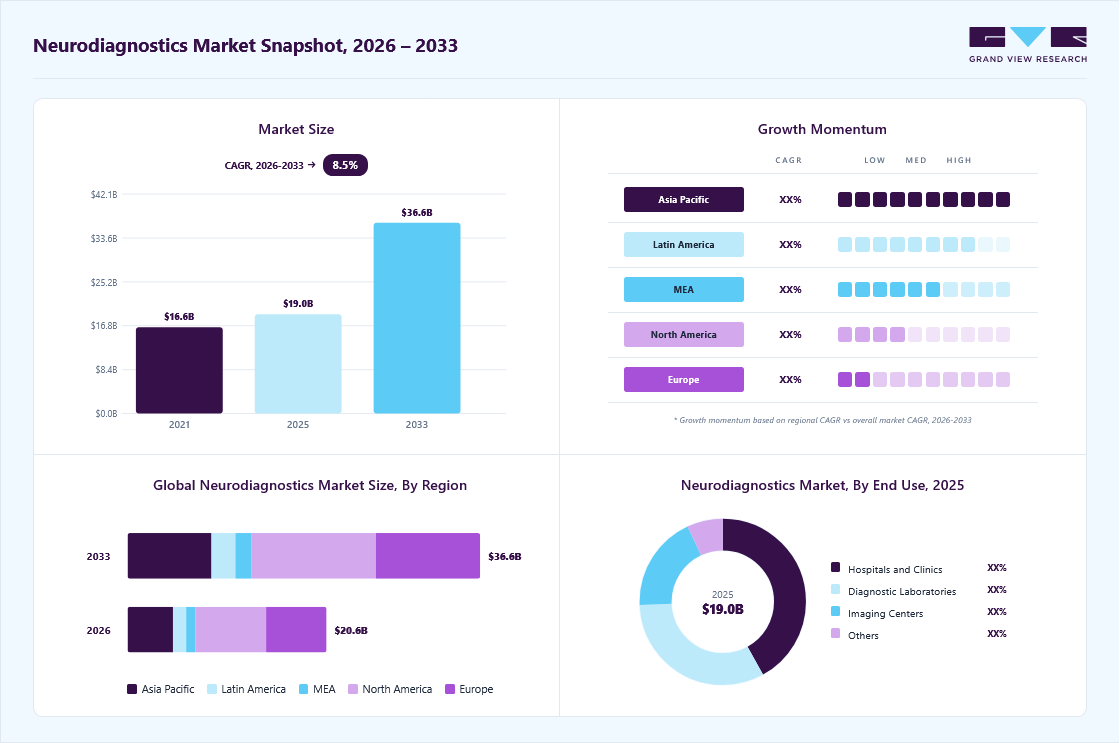

Market Size, 2025

$19.0BMarket Estimate, 2026

$20.6BMarket Forecast, 2033

$36.6BCAGR, 2026–2033

8.5%Neurodiagnostics Market Summary

The global neurodiagnostics market size was valued at USD 19.0 billion in 2025 and is projected to grow from USD 20.6 billion in 2026 to USD 36.6 billion by 2033, at a CAGR of 8.5% from 2026 to 2033. The market in North America dominated with a revenue share of 35.6% in 2025. This growth is primarily driven by the increasing prevalence of neurological disorders such as epilepsy, Alzheimer’s disease, Parkinson’s disease, stroke, and depression, which are creating sustained demand for accurate and early diagnostic solutions.

Key Market Trends & Insights

- By end use: Hospitals and clinics segment held the largest market share of 41.9% in 2025.

- By technology: Neuroimaging technologies segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (35.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 19.0 Billion

- Estimated market size in 2026: USD 20.6 Billion

- Projected market size by 2033: USD 36.6 Billion

- CAGR (2026-2033): 8.5%

In addition, the rising geriatric population is significantly contributing to market expansion, as elderly individuals are more susceptible to neurodegenerative and cerebrovascular diseases. Technological advancements such as AI-integrated imaging, portable EEG devices, and high-resolution MRI and CT systems are improving diagnostic accuracy and workflow efficiency, further accelerating adoption across hospitals and diagnostic centers.")

The advancements in neuroimaging technologies and the launch of new and innovative technologies by the key players in the market are further anticipated to drive market growth. For instance, in January 2025, Siemens Healthineers unveiled its latest diagnostic imaging innovations at the Asian Oceanian Congress of Radiology (AOCR) 2025 held in Chennai, strengthening its commitment to transforming healthcare through safe, accessible, flexible, and sustainable technologies that support improved patient care.

The showcase featured the Dry Cool technology-enabled, virtually helium-free 1.5T MAGNETOM Flow MRI, the Dual Source CT scanner SOMATOM Pro. Pulse, the locally manufactured Digital X-ray system MULTIX Impact E, and AI-powered ultrasound systems ACUSON Maple and ACUSON Sequoia. These solutions are designed to enhance diagnostic accuracy, improve workflow efficiency, and expand access to high-quality imaging, particularly across diverse healthcare settings.

Depression drives growth in the neurodiagnostic industry. The rising global burden of depressive disorders is increasing demand for objective brain-based evaluation tools such as MRI, PET, and EEG to better understand disease mechanisms, support research, and guide treatment selection. Depression is a significant mental health disorder worldwide and a leading cause of disability, creating sustained clinical and research demand for advanced neurological assessment technologies. Neuroimaging and neurophysiological techniques are used to study brain circuit changes, identify biomarkers, and support the development of personalized therapies, which directly expands the use of neurodiagnostic equipment and services.

Parkinson’s disease and Alzheimer’s disease significantly drive the neurodiagnostics industry, due to their rising global prevalence, progressive neurological damage, and strong need for early and accurate diagnosis. Parkinson’s disease prevalence varies globally but continues to increase, with studies showing rates ranging widely across regions and rising incidence particularly in aging populations, which increases demand for neuroimaging, electrophysiology tests, and biomarker-based diagnostics to support early detection and disease monitoring.

According to the Alzheimer’s Association (2025)

-

An estimated 7.2 million Americans aged 65 and older will be living with Alzheimer’s dementia by 2025.

-

74% of those affected will be aged 75 or older.

-

Approximately 1 in 9 people (11%) aged 65 and older in the U.S. have Alzheimer’s dementia.

-

The prevalence increases with age, affecting 33.4% of people aged 85 and older.

According to the Parkinson’s Foundation

-

An estimated 1.1 million people in the U.S. are currently living with Parkinson’s disease.

-

This number is projected to increase to 1.2 million by 2030.

Market Concentration & Characteristics

The neurodiagnostic industry is in a significant growth stage, driven by the rising prevalence of neurological disorders, technological advancements, and increasing healthcare investments.

The degree of innovation in the neurodiagnostics industry is high and continues to accelerate, driven by rapid advancements in artificial intelligence, neuroimaging technologies, biomarker discovery, and digital health integration. AI-enabled analysis of MRI, PET, and EEG data is improving early detection and diagnostic accuracy for neurological disorders such as Alzheimer’s disease, Parkinson’s disease, epilepsy, and depression. In June 2025, Hyperfine announced the FDA clearance of its next-generation Swoop System, powered by Optive AI software, marking a transformative advancement in portable MRI technology. The upgraded system delivers a significant leap in image quality, enhancing diagnostic accuracy and accessibility in point-of-care neuroimaging.

The level of M&A (mergers and acquisitions) activity in the neurodiagnostics industry is moderate to high, driven by the need to expand technology, diversify portfolios, and enter high-growth neurological segments. Large medical device and diagnostics companies are actively acquiring smaller firms specializing in AI-based brain imaging analysis, neuro-monitoring technologies, and digital neurology platforms to strengthen their innovation pipelines. In addition, strategic partnerships and acquisitions help companies expand geographic presence, accelerate regulatory approvals, and gain access to proprietary biomarker and software capabilities. In January 2024, Oragenics announced the acquisition of Neurology assets from Odyssey Health. The assets obtained, which include the primary concussion asset, ONP-002, and a unique nasal delivery device, are expected to significantly broaden Oragenics' market potential. The company views these assets as a strategic fit, and its proficiency in intranasal drug delivery addresses a growing healthcare issue.

Regulations have a high impact on the neurodiagnostics industry, as neurological diagnostic devices must meet strict safety, accuracy, and clinical validation requirements before approval. Regulatory bodies such as the FDA (U.S.), EMA (Europe), and other national authorities require extensive clinical evidence, quality system compliance, and post-market surveillance, which can increase development timelines and costs. However, clear regulatory pathways and fast-track approvals for breakthrough or AI-based diagnostic tools are helping accelerate innovation and market entry. In addition, regulations related to data privacy, especially for AI-driven neurodiagnostic software and cloud-based platforms, are shaping product design and commercialization strategies.

Technology Insights & Trends

The neuroimaging technologies segment accounted for the largest market revenue share in 2025. The advancements in neuroimaging technologies and the launch of new and innovative technologies by the key players in the market are further anticipated to drive market growth. For instance, in February 2024, Philips collaborated with Synthetic MR to introduce quantitative brain imaging in MR based on artificial intelligence. The Smart Quant Neuro 3D technology helps in the auto-measurement of different cells in the brain, facilitates decision support for brain diseases, and monitors the effect of therapy. The technology is expected to help in the advancement of neurology care for patients.

The in vitro diagnostics segment is expected to grow at the fastest CAGR over the forecast period. The IVD examinations offer significant insights into disease diagnosis, patient health monitoring, and treatment guidance. The advancement in technology, particularly in terms of portability, accuracy, and cost-effectiveness, is further expected to drive segmental growth. For instance, in March 2024, Beckman Coulter and Fujirebio announced the expansion of their partnership agreement to facilitate the development of patient-friendly and blood-based neurodegenerative disease diagnostics. Such partnerships are likely to lead to the advancement of in vitro diagnostics in neurology and foster growth in the market.

End Use Insights

The hospitals and clinics segment led the market with the largest revenue share of 41.92% in 2025. This s attributed to the preferred choice for many patients, positioning these facilities as the primary destination for such services. Furthermore, patients with neurological disorders often require continuous monitoring and follow-up appointments, leading to an increased demand for neurodiagnostic devices in these settings. The advancement of hospital services to improve diagnostics and care is expected to further drive market growth. For instance, in April 2023, Phoenix Children’s Hospital unveiled its expanded neurodiagnostic laboratory to enhance comfort and care for children undergoing electroencephalogram (EEG), electromyography (EMG), sleep studies, and nerve conduction studies.

The imaging centers segment is expected to witness at the fastest CAGR during the forecast period. This growth can be attributed to technological advancements, the growing prevalence of neurological disorders, and investments in and the launch of neurodiagnostic centers. Integrating AI algorithms into neuroimaging analysis has revolutionized the interpretation of scans, enabling faster, more precise results. This advancement empowers clinicians to make well-informed decisions, ultimately enhancing diagnostic accuracy. For instance, in September 2022, Qure.ai, a health tech firm, partnered with University Medical Center Rotterdam and Erasmus MC to introduce an AI Innovation Lab for Medical Imaging. The innovation center is expected to explore the role of AI in detecting abnormalities for chest, neuro, and musculoskeletal conditions. The development of such innovation centers is expected to enhance the technologies at imaging centers further and drive market growth.

Regional Insights & Trends

North America dominated the global neurodiagnostics market with the largest revenue share of 35.64% in 2025. The region's dominance can be attributed to factors such as a well-developed healthcare infrastructure, extensive research and development, and substantial healthcare spending. In addition, the region has a high prevalence of neurological conditions, underscoring the need for neurodiagnostic procedures. The existence of robust healthcare systems, effective reimbursement frameworks, and proficient healthcare professionals also plays a pivotal role in solidifying North America's position as a leader in the neurodiagnostics industry.

U.S. Neurodiagnostics Market Trends

The neurodiagnostics market in the U.S. accounted for the largest market share in North America in 2025, due to the increasing prevalence of mental, neurological, and neurodevelopmental disorders in the country. The country has a large patient pool suffering from neurology disorders, including Alzheimer’s disease, Parkinson’s disease, and epilepsy, which drives the demand for innovative diagnostic and therapeutic devices. The presence of leading medical device companies and extensive research activities further boosted the market. In addition, government initiatives and funding for neurology research and the development of new treatment modalities are significant growth drivers. For instance, in FY 2024, the total funding allocation for the BRAIN (Brain Research through Advancing Innovative Neurotechnology) Initiative amounted to USD 402 million, a 40% decrease from the FY 2023 budget.

The figure below shows that the highest number of cases by state is in California, with 17,363 cases and a rate of 37.5%, followed by Texas, with 10,427 cases and a rate of 38.8%. Georgia and Washington reported 4,219 and 3,695 cases, respectively, with rates exceeding 39%. Tennessee and Alabama also had significant numbers of cases, highlighting the prevalence of the condition in the southeastern U.S.

Note: The Number of Deaths Per 100,000 Total Population.

Europe Neurodiagnostics Market Trends

The neurodiagnostics market in Europe is growing. The increasing occurrence of neurological disorders and the heightened attention on timely identification and management are fueling market growth. According to the information published by the European Commission, around 165 million Europeans have a brain disorder, and around one in three people is expected to suffer from a neurological or mental disorder in their lives. The rising number of neurological disorders is also driving the development and launch of new, innovative brain-imaging products, which is expected to further drive market growth. According to the European Brain Council, as of 2025, an estimated 7 million people in Europe live with Alzheimer's disease, which is the most common form of dementia, highlighting the significant number of dementia cases across the continent. With a rapidly aging population, this number is projected to rise to 14 million by 2030.

The UK neurodiagnostics market is expected to grow at a significant CAGR over the forecast period, driven by the increasing number of elderly individuals and the rising incidence of neurological disorders in the country, which has led to a surge in demand for improved diagnostic tools and techniques. According to the Epilepsy Factsheet 2024, there are over 600,000 people with epilepsy in the UK. However, according to NHS England, as of June 30, 2024, 487,432 patients had a recorded diagnosis of dementia, an increase of 3,155 patients from May 31, 2024. The dementia diagnosis rate among individuals aged 65 and over reached 65.0% by June 30, 2024, up slightly from 64.8% on May 31, 2024. According to Parkinson's UK 2024, around 153,000 people in the UK are living with Parkinson's. By 2030, it is expected to increase by nearly 172,000.

The neurodiagnostics market in Germany is growing, primarily driven by the country’s aging population, rising burden of neurological disorders, strong healthcare infrastructure, and high adoption of advanced diagnostic technologies. Germany has one of the largest elderly populations in Europe, which increases the prevalence of neurodegenerative diseases such as Alzheimer’s and Parkinson’s, key conditions that require continuous neurological monitoring and diagnostic imaging. In addition, Germany’s well-established hospital and imaging center network supports strong utilization of MRI, EEG, and other neurodiagnostic tools. High healthcare spending, strong reimbursement systems, and early adoption of advanced medical technologies further support diagnostic testing volumes. Moreover, strict but innovation-focused EU and German medical device regulations ensure high-quality devices while encouraging technological advancement.

As per data published by The Robert Koch Institute, 2025

-

In 2022, the prevalence of dementia in Germany was 2.8 % of the population aged 40 and over. In women, the prevalence was 3.3%; in men, 2.4%. The prevalence of dementia rises sharply with age. For example, the prevalence among people aged 65 and over was 6.9 %.

-

In 2022, the prevalence of Parkinson's disease in Germany was 0.35 % of the population. This represents approximately 295,000 people. The prevalence is 0.34% in women and 0.36% in men. The prevalence of Parkinson's disease increases with age. It is 0.61% at age 40 and 1.42% at age 65.

Asia Pacific Neurodiagnostics Market Trends

The neurodiagnostics market in the Asia Pacific is projected to register at the fastest CAGR during the forecast period, driven by rapid healthcare infrastructure development, increasing healthcare expenditure, and rising patient awareness across emerging economies such as China, India, and Southeast Asian countries. The region is also benefiting from a large patient population, an expanding medical tourism industry, and strong government initiatives to improve access to advanced medical technologies. In addition, the growing presence of global and regional market players, along with increasing investments in healthcare modernization, is expected to accelerate market growth across Asia Pacific further.

The China neurodiagnostics market is growing due to the rising burden of neurological disorders, rapidly aging population, and increasing healthcare investment. China has a large and expanding elderly population, which is contributing to higher prevalence of stroke, Alzheimer’s disease, Parkinson’s disease, and other neurodegenerative conditions, thereby increasing demand for neurodiagnostic procedures such as MRI, CT, EEG, and neuro monitoring. According to a 2024 official report of the Chinese government, China has more than 16 million people who have dementia, including Alzheimer's disease, accounting for nearly 30% of the global total. In addition, government healthcare reforms, the expansion of hospital infrastructure, and improvements in access to advanced diagnostic technologies are supporting market expansion. The growing adoption of artificial intelligence in diagnostic imaging and increasing focus on early disease detection are further accelerating market growth. Moreover, rising healthcare awareness, urbanization, and improving insurance coverage are enabling more patients to undergo neurological diagnostic testing, supporting the overall development of the neurodiagnostics industry in China.

“Aiming to improve access to timely diagnosis, treatment, and support for people living with dementia, the Plan encourages all relevant stakeholders to collaborate with multidisciplinary and multi-level teams.”- Founding Member of Alzheimer's Disease China.

The neurodiagnostics market in India is growing due to the rising burden of neurological disorders, expanding healthcare infrastructure, and increasing adoption of advanced diagnostic technologies. The country is witnessing a surge in conditions such as stroke, epilepsy, Alzheimer’s disease, and Parkinson’s disease, driven by aging demographics, lifestyle risk factors, and higher survival rates from chronic diseases, which is increasing the need for early and accurate neurological diagnosis. National research estimates that roughly 8.8 million Indians aged 60 and above currently live with dementia. If prevalence remains unchanged, demographic ageing alone is expected to push that number to around 16.9 million by 2036, significantly increasing long-term demand for neurodiagnostic testing and monitoring.

Middle East Africa Neurodiagnostics Market Trends

The neurodiagnostics market in the Middle East & Africa is witnessing growth driven by the rising burden of neurological disorders, improved healthcare infrastructure, and the gradual adoption of advanced diagnostic technologies. Increasing cases of stroke, epilepsy, brain tumors, and neurodegenerative diseases are driving demand for EEG, MRI, CT, and other neurodiagnostic modalities across the region. In addition, governments in Gulf countries and parts of Africa are expanding hospital infrastructure and investing in digital health systems, which support diagnostic capacity and data-driven clinical decision-making.

Key Neurodiagnostics Company Insights

Some of the key companies in the neurodiagnostics industry include Canon Medical Systems Corporation; Siemens Healthineers AG; Koninklijke Philips N.V.; and Thermo Fisher Scientific, Inc.; Vendors in the market are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

Key Neurodiagnostics Companies:

The following key companies have been profiled for this study on the neurodiagnostics market.

- Canon Medical Systems Corporation

- Siemens Healthineers AG

- Koninklijke Philips N.V.

- Thermo Fisher Scientific, Inc.

- FUJIFILM Corporation

- Natus Medical Incorporated (Natus)

- Lifelines Neuro

- Advanced Brain Monitoring, Inc.

- NIHON KOHDEN CORPORATION.

- F. Hoffmann-La Roche Ltd

- GE HealthCare.

- Mitsar Co. LTD.

- Compumedics Limited

- Cadwell Industries

- Neurosoft

- Deymed Diagnostic

Recent Development

-

In January 2026, EBRAINS became an associate partner of the European Partnership for Brain Health (EP BrainHealth), contributing its expertise in digital research infrastructure. The ten-year, USD 589.74 million initiative unites over 55 institutions across 30+ countries to advance brain health research, promote collaboration, and translate findings into solutions for neurological and mental health conditions.

-

In December 2025, Cadwell and Medical Informatics Corp (MIC), the creators of the Sickbay Clinical Platform, announced a strategic partnership to establish a new standard for integrated data and monitoring in hospitals. Under this agreement, Cadwell Systems will become the first neurodiagnostic products integrated with Sickbay's enterprise-grade multimodal data architecture, enabling unified clinical intelligence beyond traditional device-centric systems.

-

In March 2024, Philips, in partnership with SyntheticMR, introduced an AI-based quantitative brain imaging system. The partnership is expected to help in the detection and analysis of several brain conditions, including multiple sclerosis, traumatic brain injuries, and dementia.

-

In March 2024, Neurophet introduced an AI-powered brain imaging analysis technology at AD/PD 2024. The technology is expected to help in the analysis of brain atrophy and white matter hyperintensities, which are found in the brain MRI of patients suffering from Alzheimer's disease.

-

In February 2024, Philips launched the Azurion neuro biplane system at #ECR2024. The system is expected to help speed up and improve minimally invasive diagnosis and treatment for neurovascular patients.

Neurodiagnostics Market Report Scope

Report Attribute

Details

Market size in 2025

USD 19.0 billion

Estimated market size in 2026

USD 20.6 billion

Projected market size by 2033

USD 36.6 billion

Growth rate

CAGR of 8.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Technology, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Canon Medical Systems Corporation; Siemens Healthineers AG; Koninklijke Philips N.V.; Thermo Fisher Scientific, Inc.; FUJIFILM Corporation; Natus Medical Incorporated (Natus); Lifelines Neuro; Advanced Brain Monitoring, Inc.; NIHON KOHDEN CORPORATION.; F. Hoffmann-La Roche Ltd; GE HealthCare.; Mitsar Co. LTD.; Compumedics Limited; Cadwell Industries; Neurosoft; Deymed Diagnostics

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Neurodiagnostics Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global neurodiagnostics market report based on technology, end use, and region:

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Neuroimaging Technologies

-

Computed Tomography (CT)

-

Magnetic Resonance Imaging (MRI)

-

Nuclear Medicine Imaging (PET, SPECT)

-

Near infrared spectroscopic imaging (NIRS)

-

Electro-encephalography (EEG)

-

Magneto-encephalography (MEG)

-

Voxel based morphometry (VBM)

-

-

In Vitro Diagnostics

-

Neuroinformatics

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals and Clinics

-

Diagnostic Laboratories

-

Imaging Centers

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

MEA

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global neurodiagnostics market size was valued at USD 19.0 billion in 2025 and is estimated at USD 20.6 billion for 2026.

The global neurodiagnostics market is expected to grow at a CAGR of 8.5% from 2026 to 2033, reaching USD 36.6 billion by 2033.

Key factors that are driving the market growth include increasing high demand for technologically advanced equipment for the early and precise diagnosis of various diseases and increasing prevalence and incidence of neurological diseases.

Asia Pacific is the fastest-growing region over the forecast period.

The hospitals and clinics segment led with a 41.9% revenue share in 2025, while imaging centers is the fastest-growing segment.

The neuroimaging technologies segment held the largest revenue share in 2025, while in vitro diagnostics is the fastest-growing technology.

Key players include Canon Medical Systems Corporation; Siemens Healthineers AG; Koninklijke Philips N.V.; Thermo Fisher Scientific, Inc.; FUJIFILM Corporation; Natus Medical Incorporated (Natus); Lifelines Neuro; Advanced Brain Monitoring, Inc.; NIHON KOHDEN CORPORATION.; F. Hoffmann-La Roche Ltd; GE HealthCare.; Mitsar Co. LTD.; Compumedics Limited; Cadwell Industries; Neurosoft; Deymed Diagnostics.

North America dominated with a 35.6% revenue share in 2025. This is attributable to the rising prevalence of neurological disorders, such as stroke, ischemic stroke, epilepsy, migraine, Parkinson’s disease across the US and Canada.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.