- Home

- »

- Advanced Interior Materials

- »

-

Non-lethal Weapons Market Size & Share Report, 2026-2033GVR Report cover

![Non-lethal Weapons Market (2026 - 2033)Report]()

Non-lethal Weapons Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product(Conducted Energy Devices, Directed Energy Systems), By End Use (Civil & Defense, Defense), By Region(North America, Europe, Asia Pacific, Central & South America, Middle East & Africa), And Segment Forecasts

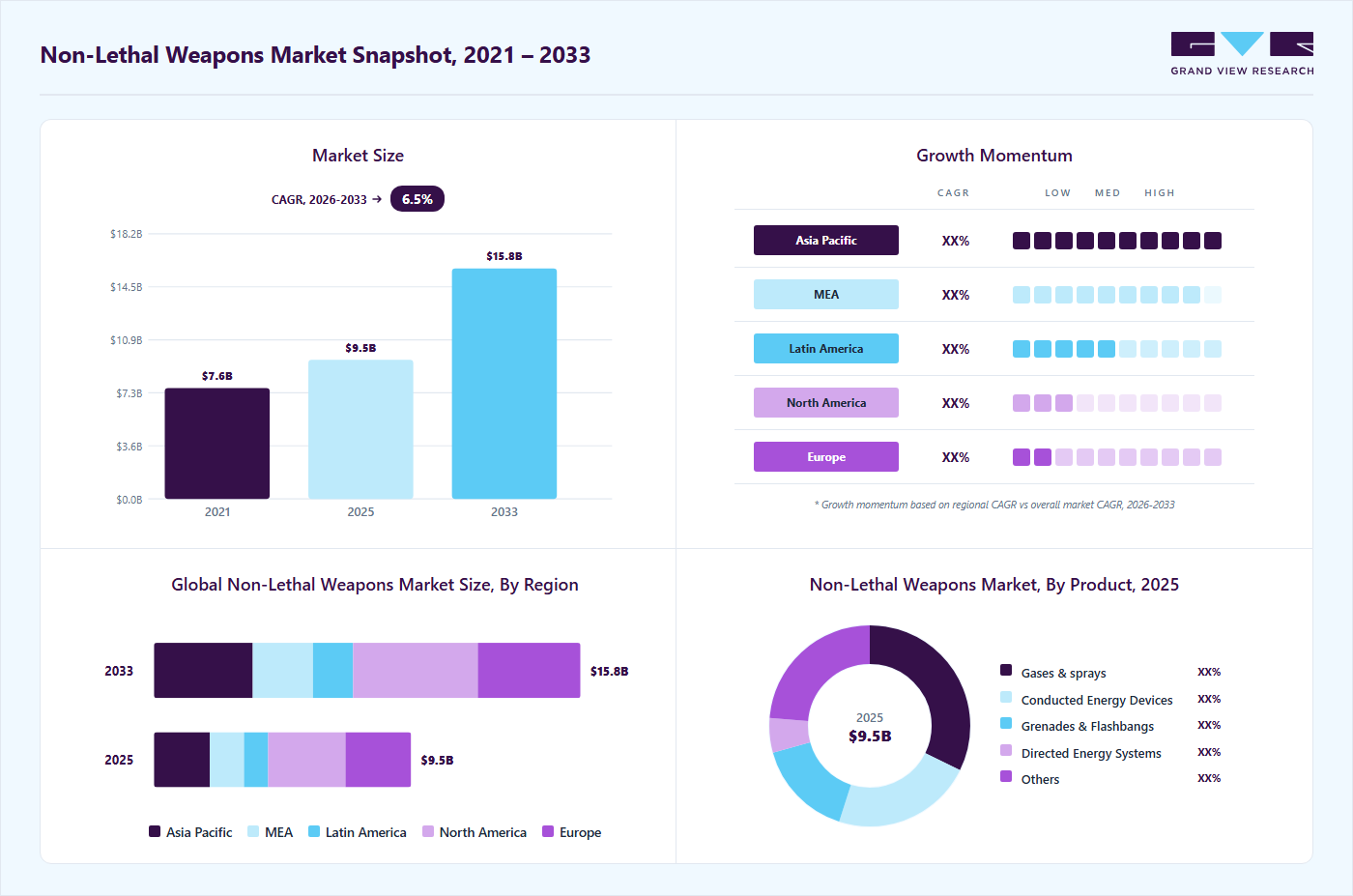

Market Size, 2025

$9.5BMarket Estimate, 2026

$10.2BMarket Forecast, 2033

$15.8BCAGR, 2026–2033

6.5%Non-lethal Weapons Market Summary

The global non-lethal weapons market size was valued at USD 9.5 billion in 2025 and is projected to grow from USD 10.2 billion in 2026 to USD 15.8 billion by 2033, growing at a CAGR of 6.5% from 2026 to 2033. North America dominated the market with the largest revenue share of 31.0% in the global market in 2025. The demand for non-lethal weapons is increasing due to rising instances of civil unrest, protests, and demonstrations globally.

Key Market Trends & Insights

- By product: Gases & sprays segment held the largest market share of 32.2% in 2025.

- By end use: Defense segment held the largest market share of 74.4% in 2025.

Regional Highlights

- Largest regional market: North America (31.0% revenue share, 2025).

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 9.5 Billion

- Estimated market size in 2026: USD 10.2 Billion

- Projected market size by 2033: USD 15.8 Billion

- CAGR (2026-2033): 6.5%

Law enforcement agencies are under growing pressure to use alternatives to lethal force in order to minimize casualties and ensure public safety. Military operations in peacekeeping missions also rely on these weapons to control hostile crowds without escalating conflicts. Increasing urbanization has led to denser populations, necessitating safer crowd-control measures. Public scrutiny on police brutality and accountability is compelling governments to adopt less-lethal solutions. Security at large gatherings such as sporting events, political rallies, and concerts further drives adoption.Key demand drivers include modernization initiatives in law enforcement and military organizations aimed at adopting less harmful defense mechanisms. Technological advancements such as directed energy weapons, acoustic devices, and improved chemical irritants enhance operational efficiency. Rising threats of terrorism, border conflicts, and insurgencies also accelerate the procurement of non-lethal systems. Growth in private security and protection of critical infrastructure supports steady adoption. Pressure from international human rights organizations prompts governments to adopt non-lethal crowd management solutions.

")

Governments worldwide are actively promoting the adoption of non-lethal weapons through defense modernization programs and law enforcement upgrades. Initiatives such as funding for riot control, border security, and peacekeeping have included provisions for these systems. International cooperation programs often supply less-lethal technologies to developing nations as part of security assistance. Export regulations on lethal-force equipment have further driven the adoption of alternatives. Countries such as the U.S., UK, India, and China have integrated non-lethal systems into standard policing kits.

Drivers, Opportunities & Restraints

The market is being propelled by a heightened emphasis on reducing casualties in military and law enforcement activities, a surge in civil disturbances, and the need for crowd management, as well as increasing regulatory oversight on the application of force. Authorities are investing in less-lethal options to reconcile public safety with respect for human rights. Furthermore, the upgrading of law enforcement tools and the growth of homeland security funding are contributing to ongoing demand.

The market faces challenges stemming from strict regulatory guidelines that govern procurement, use standards, and export restrictions. Financial constraints in developing countries limit extensive modernization efforts, while concerns about misuse, unintended deaths, and potential human rights violations can provoke public opposition and litigation risks. Furthermore, differences in performance across operational settings and the need for specialized training may hinder adoption among certain law enforcement agencies.

Growth opportunities are fueled by a rising demand for advanced, technology-driven, less-lethal solutions that improve accuracy and minimize unintended harm. Increased investments in homeland security, the growing use by private security firms, and purchasing programs in developing nations offer significant untapped potential. Ongoing research and development aimed at enhancing ergonomics, extending range capabilities, and integrating smart monitoring systems is anticipated to create new revenue opportunities and bolster global market presence.

Market Concentration & Characteristics

The non-lethal weapons industry is moderately consolidated, with major defense contractors holding significant shares alongside smaller specialized vendors. Leading players leverage strong procurement ties with governments and large agencies. Smaller firms focus on niche innovations such as acoustic or entangling devices. Mergers and acquisitions are common, as established players acquire startups to diversify portfolios. Market entry barriers are high due to regulatory approvals, rigorous testing, and credibility requirements. Procurement remains concentrated among government and defense organizations, resulting in relatively high end-user concentration.

Substitute threats in this market come primarily from non-hardware alternatives such as de-escalation training, predictive policing, and the use of barriers for crowd control. Surveillance and intelligence-based preventive approaches can reduce reliance on physical deterrents. However, substitutes cannot fully replicate the operational impact of non-lethal weapons in real-time confrontations. Highly regulated chemical irritants also act as limited substitutes but face ethical concerns. Personal protective equipment for law enforcement offers some protection, but does not eliminate the need for deterrents. Overall, substitution threats are moderate, as situational requirements still necessitate physical non-lethal tools.

Product Insights

The gases & sprays segment held the highest revenue share of 32.23% in 2025, driven by its cost-effectiveness, ease of deployment, and wide acceptance among law enforcement and civilian users. Their portability and ability to quickly disperse crowds or neutralize individuals without causing permanent harm make them the first line of choice in riot control and self-defense. Growing sales of civilian defense sprays in retail channels further strengthen their share, while bulk procurement by police and military agencies ensures steady institutional demand.

The directed energy systems segment is expected to grow at the fastest CAGR of 6.7% over the forecast period, as governments and security forces adopt advanced technologies for crowd control and area denial. These systems offer precision, scalability, and reduced risk of collateral damage compared to traditional kinetic options. Defense contractors and specialized firms are increasing R&D investments, and several countries are piloting directed-energy deployments in border security and maritime operations, pushing this segment toward faster adoption in the next decade.

End Use Insights

The defense segment held the highest revenue market share of 74.42% in 2025, driven by large-scale adoption by military and paramilitary organizations. Governments worldwide are procuring riot-control agents, flashbangs, acoustic hailing devices, and less-lethal munitions to enhance their non-lethal capabilities in peacekeeping and counter-insurgency operations. Defense dominance is further supported by substantial budgets, international security missions, and the need for compliance with humanitarian laws that emphasize minimizing fatalities while maintaining effective operational control.

The civil & commercial segment is expected to grow at the fastest CAGR of 6.8% over the forecast period, driven by rising concerns over personal safety, workplace security, and retail crime, which are driving demand for consumer-friendly self-defense solutions. Companies like Byrna, SABRE, and Mace are tapping into a growing customer base that seeks alternatives to firearms, offering launchers, sprays, and smart self-defense devices. Increasing e-commerce availability, marketing campaigns focused on personal safety, and heightened urban crime awareness are key drivers of this segment's fast-paced growth.

Regional Insights

North America dominated the global non-lethal weapons market, accounting for the largest revenue share of 31.0% in 2025, driven by robust defense and law enforcement budgets. The U.S. leads procurement, supported by modernization initiatives in policing and homeland security. Strong presence of major defense contractors accelerates innovation in directed energy and acoustic systems. Municipalities and federal agencies increasingly seek accountability-focused integrated solutions. Public scrutiny of lethal force practices strengthens reliance on non-lethal options. Canada also shows growing adoption in law enforcement, particularly for crowd management. The region remains a hub for innovation, procurement, and regulatory influence in the sector.

U.S. Non-lethal Weapons Market Trends

The non-lethal weapons market in the U.S. is expected to grow at a CAGR of 5.9% from 2026 to 2033. The non-lethal weapons market in the U.S. is characterized by high demand from federal, state, and local law enforcement. Homeland security initiatives and riot control requirements sustain steady procurement. Vendors often collaborate with training institutes to bundle hardware with operational guidelines. Federal grants support municipal and state-level purchases. Civil rights movements and lawsuits have increased the emphasis on safe and accountable deployment. Military applications in peacekeeping missions also contribute to adoption. The U.S. sets technical and regulatory benchmarks that significantly influence global market dynamics.

Asia Pacific Non-lethal Weapons Market Trends

The non-lethal weapons market in the Asia Pacific is driven by rapid urbanization, rising defense budgets, and rising public unrest. Countries like India, China, South Korea, and Japan are actively investing in advanced crowd-control solutions. Border disputes and anti-terrorism operations further strengthen regional demand. Local manufacturing capabilities, coupled with international supplier collaborations, aid market growth. Government-led police modernization programs often include non-lethal solutions. Growing participation in UN peacekeeping missions also boosts adoption. Asia Pacific remains one of the fastest-growing and strategically significant regions in this market.

China non-lethal weapons market is investing heavily in non-lethal systems to manage large urban populations and ensure domestic stability. The People’s Armed Police and law enforcement bodies deploy non-lethal options during crowd management and protests. Local manufacturers are rapidly expanding production capacities to cater to both domestic and export demand. Integration of these systems with China’s smart city surveillance platforms enhances situational awareness. Strict government oversight ensures compliance with national security objectives. Export restrictions from Western countries drive China to develop indigenous alternatives.

Europe Non-lethal Weapons Market Trends

The non-lethal weapons market in Europe emphasizes compliance with strict human rights norms and safety standards. EU-funded programs often focus on standardized, ethically acceptable, non-lethal technologies. Law enforcement modernization in countries such as France, the UK, and Italy drives procurement. Border security requirements also contribute to demand, especially in Southern Europe. Vendors face rigorous testing and certification processes to enter the market. The growing focus on accountability is driving integration with surveillance and transparency tools. Europe remains a regulation-driven but stable market with emphasis on low-collateral solutions.

Germany non-lethal weapons market is shaped by its strict regulatory frameworks and high-quality standards. Federal and state police agencies prioritize validated non-lethal solutions backed by rigorous trials. German firms are known for specialized innovations in mechanical effectors and entanglement systems. Export regulations often limit cross-border trade, influencing domestic vendor strategies. Public scrutiny of law enforcement further emphasizes the need for safe, low-injury options. Collaborations with research institutes support ongoing innovation and certification. Germany remains a highly quality-conscious and compliance-oriented segment within Europe.

Central & South America Non-lethal Weapons Market Trends

The non-lethal weapons market in CSA is witnessing rising adoption of non-lethal weapons due to urban violence, protests, and crime control needs. Countries like Brazil, Mexico, and Argentina are key markets, though budget constraints remain a challenge. International aid and donor programs occasionally finance procurement in smaller economies. Law enforcement agencies prefer rugged and cost-effective systems suitable for large crowds. Human rights concerns influence deployment strategies, particularly in politically unstable nations. Local partnerships and training packages are crucial for vendor penetration. The region shows steady but uneven growth, depending on political and economic stability.

Middle East & Africa Non-lethal Weapons Market Trends

The non-lethal weapons market in the MEA is driven by requirements for border protection, riot control, and protection of critical infrastructure. Large events such as pilgrimages, political gatherings, and sporting activities require advanced crowd management solutions. Defense modernization programs in Gulf nations increasingly include non-lethal portfolios. Regional unrest and insurgency threats further support adoption. Vendors often provide turnkey contracts including training, logistics, and sustainment. Varying regulatory standards across nations create both challenges and opportunities. Overall, MEA is an emerging but strategically important growth.

Key Non-lethal Weapons Company Insights

Leading companies are engaged in organic strategies like launching new products, upgrading technologies, innovating ammunition, and miniaturizing platforms, as well as inorganic approaches such as forming strategic partnerships, securing defense contracts, pursuing mergers and acquisitions, and establishing regional distribution alliances to enhance their product portfolios, increase their geographical reach, and secure long-term government procurement agreements.

Key Non-lethal Weapons Companies:

The following key companies have been profiled for this study on the non-lethal weapons market.

- NonLethal Technologies, Inc.

- Axon

- Combined Systems, Inc.

- Byrna

- CONDOR

- Zarc International Inc.

- SABRE

- TASER Self Defense

- Mace

- Armament Systems and Procedures

Recent Developments

-

In July 2025, Rheinmetall introduced the SSW40 (Squad Support Weapon 40) during live-fire demonstrations and industry showcases. The SSW40 is a magazine-fed 40 mm grenade launcher that fires both medium-velocity (MV) and low-velocity (LV) rounds, with ergonomic handling similar to that of an assault rifle. The live demonstrations highlighted its extended range of about 900 meters and its recoil-reduction technologies.

-

In June 2025, Armament Systems & Procedures (ASP) launched Defender LE, a new pepper spray product line targeted to law enforcement.

-

In March 2025, ASP, along with Byrna, SABRE, and TASER Self Defense, partnered with USCCA (U.S. Concealed Carry Association) to launch a course, “Non-Lethal Tools for Self-Defense”.

-

In February 2025, EDGE Group (UAE) entity CONDOR signed a contract with Brazil’s SENAPPEN to upgrade prison security in Brazil using non-lethal tech (NLT) and training.

Non-lethal Weapons Market Report Scope

Report Attribute

Details

Market size in 2025

USD 9.5 billion

Estimated Market size in 2026

USD 10.2 billion

Projected Market size by 2033

USD 15.8 billion

Growth rate

CAGR of 6.5% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, end use, region

Regional scope

North America; Asia Pacific; Europe; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Spain; China; Japan; India; South Korea; Saudi Arabia; UAE; Egypt; Kuwait; Qatar

Key companies profiled

NonLethal Technologies, Inc.; Axon; Combined Systems, Inc.; Byrna; CONDOR; Zarc International Inc.; SABRE; TASER Self Defense; Mace; Armament Systems and Procedures

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Non-lethal Weapons Market Report Segmentation

This report forecasts revenue growth at the regional & country levels and provides an analysis of industry trends in each subsegment from 2021 to 2033. For this study, Grand View Research has segmented the global non-lethal weapons market based on product, end use, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Gases & Sprays

-

Conducted Energy Devices

-

Grenades & Flashbangs

-

Directed Energy Systems

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Civil & Defense

-

Defense

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

-

Central & South America

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

Egypt

-

Qatar

-

Kuwait

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The gases & sprays segment held the market with the largest revenue share of 32.2% in 2025, while directed energy systems is the fastest-growing segment.

The defense segment held the market with the largest revenue share of 74.4% in 2025, while civil & commercial is the fastest-growing segment.

The global non-lethal weapons market size was valued at USD 9.5 billion in 2025 and is expected to reach USD 10.2 billion by 2026.

North America dominated the market with a revenue share of 31.0% in 2025.

Some key players in the non-lethal weapons market include NonLethal Technologies, Inc., Axon, Combined Systems, Inc., Byrna, CONDOR, Zarc International Inc., SABRE, TASER Self Defense, Mace, and Armament Systems and Procedures.

Key factors driving the non-lethal weapons market include rising civil unrest and protests, growing demand for crowd-control solutions, increased focus on minimizing fatalities in law enforcement, adoption of advanced technologies in directed energy and CEDs, and government investments in modernizing policing and defense capabilities.

The global non-lethal weapons market is expected to grow at a CAGR of 6.5% from 2026 to 2033, reaching USD 15.8 billion by 2033.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.