- Home

- »

- Next Generation Technologies

- »

-

Open Banking Market Size & Share, Industry Report, 2033GVR Report cover

![Open Banking Market Size, Share & Trends Report]()

Open Banking Market (2026 - 2033) Size, Share & Trends Analysis Report By Services (Banking & Capital Markets, Payments), By Deployment (Cloud, On-premise), By Distribution Channel (Back Channels, App Markets), By Region, And Segment Forecasts

Market Size, 2025

$39.8BMarket Estimate, 2026

$50.5BMarket Forecast, 2033

$287.3BCAGR, 2026–2033

28.2%Open Banking Market Summary

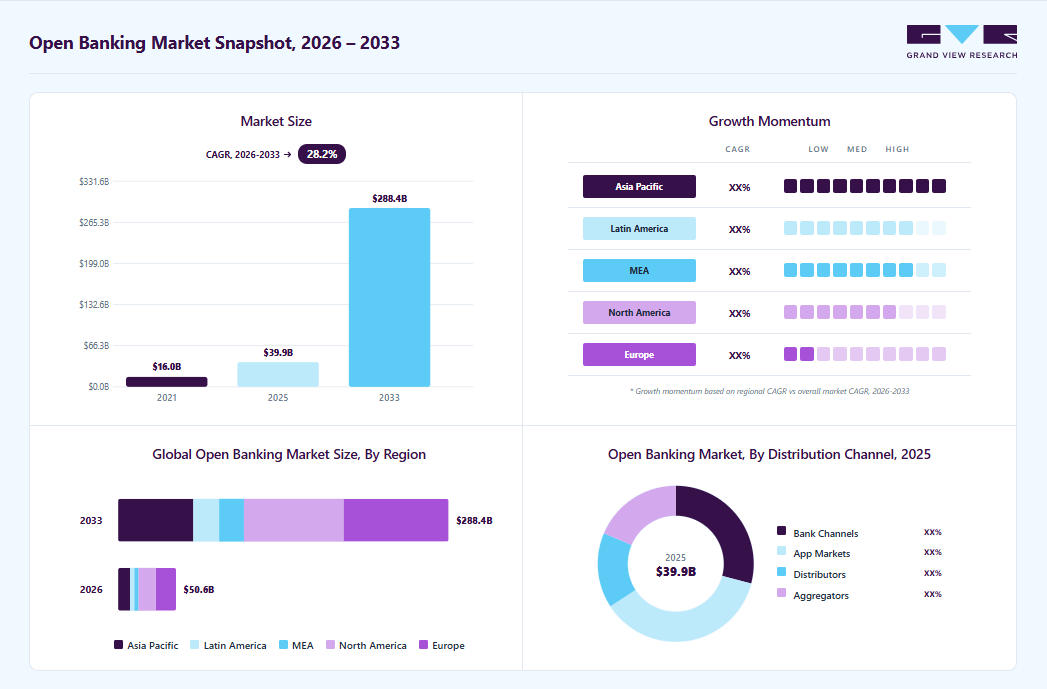

The global open banking market size was valued at USD 39.8 billion in 2025 and is projected to grow from USD 50.5 billion in 2026 to USD 288.3 billion by 2033, growing at a CAGR of 28.2% from 2026 to 2033. The North America market held the largest share of 35.8% of the global market in 2025. Open banking allows third-party financial service providers open access to transactions and other financial data from bank and non-bank financial institutions using APIs.

Key Market Trends & Insights

- By service: Banking & capital markets segment dominated the market in 2025 and accounted for the largest share of 45.9%.

- By deployment: On-premise segment accounted for the largest market share in 2025.

- By distribution channel: App markets segment dominated the market in 2025.

Regional Highlights

- Largest regional market: Europe (35.8% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- The open banking industry in the Germany held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 39.8 Billion

- Estimated market size in 2026: USD 50.5 Billion

- Projected market size by 2033: USD 288.3 Billion

- CAGR (2026-2033): 28.2%

Open banking is gaining momentum globally, supported by multiple growth drivers. Consumers are increasingly seeking automated and digital ways to transfer money, manage their finances, access and analyze their financial data, and gain greater transparency and control over their information. Use cases continue to expand, including funding investment accounts, topping up digital wallets, and applying for mortgages. At the same time, supportive regulatory frameworks, continuous innovation by open banking providers, and growing demand for seamless and enhanced financial experiences are further accelerating adoption worldwide.

")

The rapid digitization and rising adoption of technologies, including artificial intelligence, machine learning, and big data analytics in the industry worldwide, are anticipated to drive the growth of the open banking industry. Big data analytics is used in the industry to tailor the services and boost the user experience, which is anticipated to attract more customers. Furthermore, the improved security of APIs is another major factor fueling the market's growth. In addition, the growing e-commerce and online shopping trends worldwide bode well for the growth of the industry.

Open banking adoption is further driven by growing demand from consumers, merchants, and billers, rising borrower interest in digital mortgage experiences, and increased usage of account-to-account (A2A) payments. The adoption of A2A and alternative payment methods is accelerating worldwide, supported by open banking’s ability to deliver seamless transaction experiences, particularly in areas such as bill payments, disbursements, and recurring transactions. In addition, enabled by open banking, A2A payments can be executed rapidly while providing enriched insights, including account ownership verification, balance validation, risk indicators, tokenization, and fraud detection signals. Across markets, open banking enhances the speed, efficiency, and convenience of A2A transactions, which in turn drives the growth of the market.

Regulatory developments are reshaping the open banking landscape, with key global markets progressing at varying stages of implementation. Europe and the UK were early adopters, introducing frameworks such as the Payment Services Directive (PSD2) and later the Payment Services Regulation (PSR). Across other regions, countries are actively developing their own regulatory structures. In Canada, the Department of Finance (DoF) and the Financial Consumer Agency of Canada (FCAC) are advancing initiatives to establish an open banking framework. Several African nations are also moving toward formal adoption, while countries such as Saudi Arabia and Bahrain are introducing innovative measures to pilot and scale open banking solutions.

Although the industry is anticipated to grow over the forecast period, it faces challenges such as concerns regarding growing cyberattacks and online fraud. Open banking encourages the sharing of critical customer information, which raises concerns over data security and privacy protection. However, various firms pursue different strategic initiatives to ensure that critical data is shared securely and consensually. Fintech firms also conform to regulations drafted by various governments worldwide to govern the terms under which consumers grant access to their data.

Service Insights

The banking & capital markets segment dominated the market in 2025 and accounted for the largest share of 45.9%. The growing demand for managing finances effectively among millennials is expected to drive the segment’s growth. Shifting focus from traditional investment methods to advanced investment solutions is expected to generate lucrative opportunities for the segment. The increasing adoption of advanced AI-enabled platforms that can suggest investment options as per customer needs through the integration of algorithms and analytics is expected to propel segment growth.

The payments segment is expected to grow at the fastest CAGR during the forecast period. The attributes of the growth are increased internet penetration across the world and a surge in the utilization of various platforms for online payments. Such developments occurred as an opportunity for banks to gain a competitive edge and strengthen their market position by collaborating or partnering with such platform providers. Furthermore, the rise in the launches of payment services by industry players also bodes well for the growth of the segment.

Deployment Insights

The on-premise segment accounted for the largest market share in 2025. It enables easy accessibility for customers, serving their needs better. The segment’s growth is also attributed to BFSI companies offering their APIs, which enable third parties and banks to offer cutting-edge services. In addition, a platform for open banking applications invites users to interact with their financial data in unconventional ways.

The cloud segment is expected to grow at the fastest CAGR during the forecast period. Cloud deployment service allows banks to collect, analyze, and provide customized services by leveraging an unprecedented amount of consumer data. In addition, cloud technology provides the highest standards of security. Moreover, the cloud enables scalability, flexibility, and real-time processing, which is expected to generate new opportunities for segment growth.

Distribution Channel Insights

The app markets segment dominated the market in 2025. The dominance can be attributed to the proliferation of smartphones globally. The growing adoption of mobile applications for buying and selling products and services is expected to drive the segment’s growth. Moreover, rising awareness regarding the utilization of bank-related services through mobile devices also bodes well for the segment’s growth.

The distributors segment is expected to grow at the fastest CAGR during the forecast period. The growth is ascribed to the fact that in a distributor model, banks function as service or product providers by processing what is eventually sold by a third-party provider. The customer interface is owned by a third-party provider, which is expected to offer unique opportunities for the segment’s growth. In addition, rising demand for embedded finance and digital financial services is further accelerating this segment, as distributors allow non-banking platforms to integrate financial capabilities efficiently.

Regional Insights

Europe open banking industry dominated the global market and accounted for a revenue share of 35.8% in 2025. Regional market growth can be ascribed to the increasing need to improve online payment security in the region. Government directives for banks to compel the opening of APIs are promoting market expansion in this region. The presence of numerous prominent companies in the region is further expected to fuel regional market growth.

Germany Open Banking Market Trends

The Germany open banking industry is expected to grow at a significant CAGR during the forecast period. The landscape of the German market is evolving with a focus on data security and privacy, driving the adoption of digital solutions and fostering collaboration between traditional banks and fintech startups.

The UK open banking industry held a substantial market share in 2025. The regional market is characterized by rapid innovation in fintech, supported by regulatory mandates such as PSD2, leading to increased competition and customer-centric financial services.

Asia Pacific Open Banking Market Trends

The Asia Pacific open banking industry is expected to grow at the fastest CAGR during the forecast period. The regional market growth can be attributed to the growing awareness of the benefits offered by open banking systems among countries such as China, India, and Japan. In addition, the rapid development of digital payment services in Asia Pacific countries is also expected to contribute significantly to the growth of the regional market.

India’s open banking industry is expected to grow at the fastest CAGR during the forecast period. Factors such as a unique combination of digital public infrastructure, regulatory innovation, and strong fintech adoption are expected to contribute to the growth of the market.

The China open banking industry held a significant market share in 2025. The Chinese market is propelled by tech giants offering comprehensive financial ecosystems, integrating banking services with e-commerce, payments, and wealth management, reshaping the financial landscape.

North America Open Banking Market Trends

North America open banking industry is expected to register a moderate CAGR from 2026 to 2033. The market is driven by consumer demand for seamless digital experiences, prompting banks to invest in APIs and collaborate with fintech firms to enhance innovation and competitiveness.

The U.S. open banking industry held a dominant position in the region in 2025. The market is marked by a surge in fintech adoption, driven by regulatory reforms and consumer demand for personalized financial services, fostering a dynamic ecosystem of banking innovation.

Key Open Banking Company Insights

Some of the key companies in the open banking industry include Banco Bilbao Vizcaya Argentaria, S.A., Crédit Agricole, Finastra, NCR Corporation, Jack Henry & Associates, Inc., and others. Organizations are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Banco Bilbao Vizcaya Argentaria, S.A. provides financial and commercial banking services. Solutions offered by the company include treasury management, regulatory APIs, and a digital ecosystem. The company offers its API and open banking solutions through its BBVA API Market.

-

Finastra is a financial software solution company offering a range of digital banking services, such as knowledge services, support services, client advisory services, managed services, and collaborative design engagement, implementation, and delivery. The company’s solutions for open banking include digital banking, U.S. digital & retail banking, and international digital & retail banking.

Key Open Banking Companies:

The following key companies have been profiled for this study on the open banking market.

- Banco Bilbao Vizcaya Argentaria, S.A.

- Crédit Agricole

- Worldline

- Qwist

- Finastra

- Capgemini

- Mambu

- Fiserv, Inc.

Recent Developments

-

In February 2026, Truist Financial Corporation launched its first open banking integration by partnering with Mastercard’s open finance technology. This API-driven platform enables Truist’s consumer and small business clients to securely access and manage their financial data in a centralized manner, enhancing transparency, personalization, and control across an expanding network of trusted fintech applications.

-

In November 2025, SBS, a global financial technology firm, introduced an upgraded version of its SBP Open Banking Platform, aimed at enabling banks to deliver next-generation digital payments and embedded finance solutions across Europe.

Open Banking Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 50.56 billion

Revenue forecast in 2033

USD 288.36 billion

Growth rate

CAGR of 28.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Service, deployment, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; Kingdom of Bahrain; South Africa

Key companies profiled

Banco Bilbao Vizcaya Argentaria, S.A.; Crédit Agricole; Worldline; Qwist; Finastra; Capgemini; Mambu; Fiserv, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Open Banking Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global open banking market report based on service, deployment, distribution channel, and region:

-

Service Outlook (Revenue, USD Million, 2021 - 2033)

-

Banking & Capital Markets

-

Payments

-

Digital Currencies

-

Value Added Services

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud

-

On-premise

-

-

Distribution Channel Outlook (Revenue, USD Million, 2021 - 2033)

-

Bank Channels

-

App Markets

-

Distributors

-

Aggregators

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

Kingdom of Bahrain

-

South Africa

-

-

Frequently Asked Questions About This Report

Key factors that are driving the open banking systems market growth include the integration of big data analytics and AI into banking systems and the adoption of digitalization.

The global open banking market size was estimated at USD 39.9 billion in 2025 and is expected to reach USD 50.6 billion in 2026.

Banking & capital held the largest revenue share in 2025, while payments segment is the fastest-growing market.

Europe dominated with a 35.8% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The global open banking market is expected to grow at a compound annual growth rate of 28.2% from 2026 to 2033 to reach USD 288.3 billion by 2033.

Europe dominated the open banking market with a share of 35.8% in 2025. The regional market growth can be ascribed to the increasing requirement for improving online payment security in the region.

Some key players operating in the open banking market include Banco Bilbao Vizcaya Argentaria, S.A., Crédit Agricole, Worldline, Qwist, Finastra, Capgemini, Mambu, and Fiserv, Inc.

The on-premise segment accounted for the largest market share in 2025, while cloud segment is the fastest-growing market.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.