- Home

- »

- Electronic Devices

- »

-

Smartphone Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Smartphone Market (2026 - 2033)Report]()

Smartphone Market (2026 - 2033)

Size, Share & Trends Analysis Report By Operating System (Android, iOS), By Distribution Channel (Online, Offline), By Price Range (Entry Level, Mid-Range, Premium), By Region, And Segment Forecasts

Market Size, 2025

$537.6BMarket Estimate, 2026

$556.4BMarket Forecast, 2033

$749.1BCAGR, 2026–2033

4.3%Smartphone Market Summary

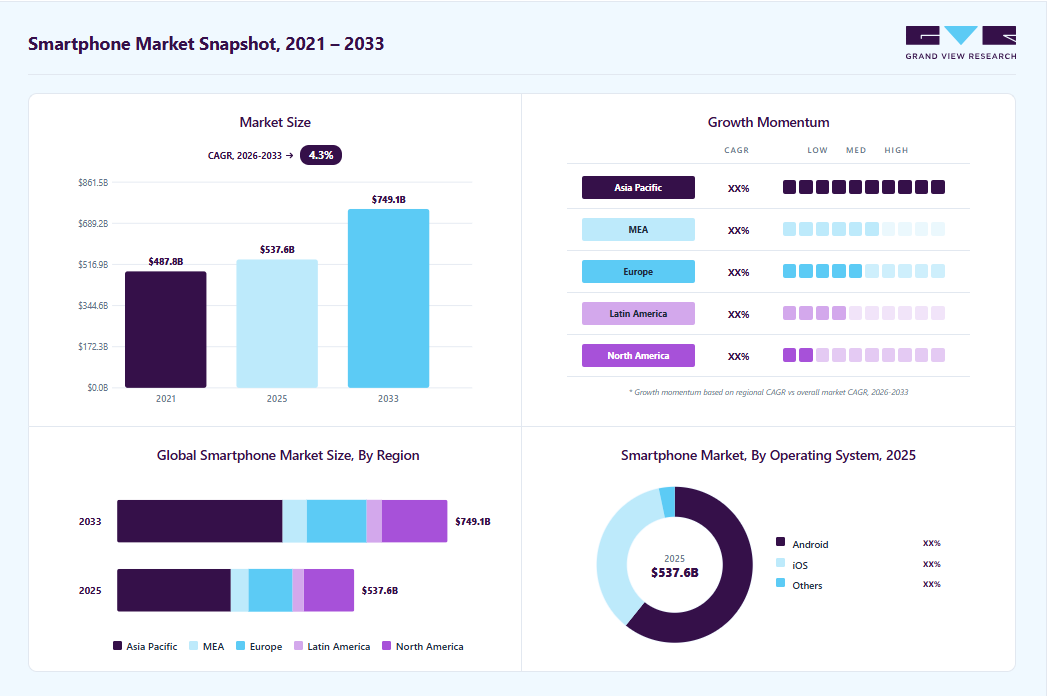

The global smartphone market size was valued at USD 537.6 billion in 2025 and is projected to grow from USD 556.4 billion in 2026 to USD 749.1 billion by 2033, at a CAGR of 4.3% from 2026 to 2033, due to rising consumer demand for feature-rich yet affordable devices, rapid advancements in 5G connectivity, and increasing digital dependency across emerging and developed economies. The market in Asia Pacific dominated with a revenue share of 47.9% in 2025. Key drivers include the proliferation of AI-powered functionalities such as on-device generative AI, enhanced mobile photography, and real-time language translation, as well as growing integration with IoT ecosystems.

Key Market Trends & Insights

- By operating system: Android segment held the largest market share of 60.8% in 2025.

- By distribution channel: Offline segment held the largest market share in 2025.

- By price range: Mid-range segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (47.9% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 537.6 Billion

- Estimated market size in 2026: USD 556.4 Billion

- Projected market size by 2033: USD 749.1 Billion

- CAGR (2026-2033): 4.3%

Smartphone adoption is further supported by expanding e-commerce penetration, competitive pricing strategies, and shorter replacement cycles driven by faster technological obsolescence. Moreover, sustainability initiatives such as modular repairability, use of recycled materials, and energy-efficient chipsets are becoming central to brand differentiation, while demand from sectors like gaming, fintech, and enterprise mobility continues to reshape device capabilities and performance expectations.")

The increasing penetration of smartphones and other smart devices across both developed and emerging economies also contributes to the growth of the market. Smartphones have become essential tools for communication, entertainment, and productivity, driving consistent demand. In addition, the rise of wearable technology, such as smartwatches and fitness trackers, has contributed to market expansion as awareness of health and fitness grows. The integration of these devices with other smart home products, such as voice assistants and security systems, has further boosted consumer interest and spending in this sector. For instance, in January 2025, Alarm.com, a U.S.-based technology company, launched its new AI Deterrence (AID) service, an advanced automated audio response system designed to strengthen property security. Leveraging artificial intelligence, the service issues personalized verbal warnings to potential intruders, adapting its messages based on visual cues such as clothing and environmental context.

Market Dynamics

The growing demand for mobile entertainment and gaming is driving the smartphone market, as consumers increasingly use smartphones as their primary source of digital entertainment. Video streaming, live content consumption, mobile esports, cloud gaming, short-form video platforms, and interactive social media applications have transformed smartphones from communication devices into entertainment hubs. Consumers spend a significant portion of their daily digital time watching content, playing games, participating in online communities, and engaging with immersive applications directly through their smartphones. This behavioral shift creates a strong connection between entertainment consumption and smartphone demand, as users seek devices that can deliver smoother graphics, faster processing, and uninterrupted connectivity. This directly contributes to smartphone market growth by increasing replacement cycles, boosting demand for feature-rich devices, and expanding the addressable consumer base across both premium and mid-range categories.

The rise of subscription-based entertainment ecosystems is also contributing significantly to the expansion of the smartphone market. Consumers increasingly access streaming platforms, music services, live sports broadcasts, digital cinema releases, and interactive content on mobile devices for convenience and portability. This creates a direct relationship between smartphone usage and digital entertainment consumption, as consumers expect uninterrupted access to content wherever they are. Smartphones with high-resolution displays, enhanced sound systems, larger battery capacities, and efficient connectivity features are becoming increasingly attractive in this environment. The demand for better multimedia experiences is driving users to shift from entry-level devices to smartphones with advanced content consumption capabilities. This supports market growth by increasing average selling prices, accelerating product upgrades, and creating opportunities for brands to differentiate through entertainment-focused features.

The volatility in semiconductor pricing and supply availability significantly constrains the smartphone market, as modern smartphones depend heavily on advanced chipsets for performance, connectivity, and power efficiency. Semiconductor components such as processors, GPUs, memory chips, and 5G modems are among the most expensive and critical parts of a smartphone. When semiconductor prices rise due to supply chain disruptions, geopolitical factors, or production bottlenecks, manufacturers face higher unit production costs. This directly influences smartphone pricing strategies, forcing companies to either increase retail prices or reduce features to maintain cost balance. Both outcomes negatively affect market demand, as higher prices reduce affordability and downgraded features reduce product attractiveness. The relationship between semiconductor cost fluctuations and smartphone innovation is also strong because budget constraints can delay product launches or limit technological upgrades.

The growth of foldable and innovative form-factor devices is emerging as a major opportunity for the smartphone market, as it expands the definition of what a smartphone can offer beyond traditional slab designs. Foldable devices offer larger-screen experiences in a portable format, combining smartphone mobility with tablet-like productivity. This creates a strong relationship between form-factor innovation and market expansion, as it attracts both premium consumers and productivity-focused users seeking enhanced multitasking capabilities. As consumers increasingly demand differentiated, futuristic devices, foldable smartphones offer a clear upgrade incentive over conventional models. This drives higher average selling prices and increases revenue potential for manufacturers, even if unit volumes remain relatively niche.

Market Concentration & Characteristics

The smartphone market is moderately to highly concentrated, with a few dominant global manufacturers such as Apple, Samsung Electronics, Xiaomi, OPPO, and vivo accounting for a significant share of global shipments and revenues. These companies maintain strong market positions through extensive product portfolios, global distribution networks, advanced R&D capabilities, and integrated hardware-software ecosystems. The market presents high entry barriers due to substantial capital requirements, complex semiconductor supply chains, intellectual property protections, brand loyalty, and large-scale manufacturing efficiencies. Additionally, strategic partnerships with telecom operators, online marketplaces, and component suppliers further strengthen the competitive positioning of leading players.

In terms of market characteristics, the smartphone industry is highly innovation-driven and fast evolving, with strong emphasis on artificial intelligence (AI), 5G connectivity, foldable displays, mobile gaming, computational photography, and ecosystem integration. Demand is primarily driven by rising smartphone penetration, replacement cycles, digital content consumption, and increasing adoption of mobile-based financial and enterprise applications. The market is characterized by rapid product launch cycles, aggressive pricing competition, premiumization trends, and growing consumer preference for integrated digital ecosystems. Furthermore, customer retention is strongly influenced by operating systems, app ecosystems, cloud services, and device interoperability, resulting in moderate-to-high vendor lock-in, particularly within premium smartphone segments.

Operating System Insights

The Android segment dominated the market and accounted for the revenue share of 60.8% in 2025. The Android segment is gaining momentum globally due to its strong alignment with evolving consumer expectations around content creation, performance optimization, and software longevity. Manufacturers are increasingly integrating advanced artificial intelligence features at the system level, such as intelligent imaging, contextual search, and on-device productivity tools, to elevate the user experience in the mid-premium category.

The others segment is anticipated to grow at the highest CAGR during the forecast period. The others segment includes HarmonyOS. The adoption of HarmonyOS in the smartphone market is being strongly driven by the increasing demand for alternative mobile operating systems that can provide ecosystem diversity and reduce dependence on traditional platform dominance. As the smartphone market matures, both manufacturers and consumers are seeking differentiated software experiences that offer greater flexibility, ecosystem control, and localized innovation. This creates a direct relationship between operating system diversification and smartphone market growth, as software platforms often influence device purchase decisions as strongly as hardware specifications.

Distribution Channel Insights

The offline segment dominated the market and accounted for the largest revenue share in 2025. The offline segment continues to hold a dominant share of smartphone distribution, offering an immersive shopping experience that digital platforms cannot fully replicate. As premiumization accelerates, consumers increasingly seek in-store validation of product quality, camera performance, display standards, and building materials before committing to high-value purchases

The online segment is expected to grow at a significant CAGR during the forecast period. Online sales accounted for a significant share of the smartphone market due to their enhanced convenience, transparent pricing, and ease of product comparison. Consumers benefit from access to a broad range of models, exclusive limited-time promotions, and flexible payment and delivery options. Additionally, this sales channel demonstrates growth during high-demand periods such as festive seasons and end-of-quarter campaigns, where e-commerce platforms leverage their extensive reach and operational efficiency.

Price Range Insights

The mid-range segment dominated the market and accounted for the largest revenue share in 2025. This segment continues to witness robust traction as consumers across both developed and emerging markets seek smartphones that offer a balanced combination of performance, camera capabilities, design, and battery efficiency without entering flagship price brackets. The growth is largely fueled by buyers upgrading from entry-level devices and users seeking near-premium features such as AMOLED displays, fast charging, 5G connectivity, and multi-lens AI-powered cameras within accessible price bands.

The premium segment is expected to grow at a significant CAGR over the forecast period. This growth is attributed to the rising demand for devices that deliver high-performance computing, advanced AI integration, and sophisticated imaging capabilities. Consumers, especially in metropolitan and upper-tier cities, are increasingly adopting flagship models that double as productivity tools and lifestyle statements. These users prioritize ecosystem continuity, long-term software updates, and exclusive service access, such as cloud backups, premium support, and security features integrated with wearables and home devices.

Regional Insights

North America held a significant share in the global market in 2025. The North American smartphone market is driven by strong consumer preference for premium devices with advanced features such as AI-powered cameras, foldable screens, and 5G integration. A high replacement rate, driven by frequent upgrade programs offered by carriers and OEMs, sustains demand. Additionally, the rapid adoption of mobile payment systems, integration of smartphones into connected ecosystems like smart homes and vehicles, and the push for eco-friendly devices with longer lifecycles are fueling market expansion.

U.S. Smartphone Market Trends

The smartphone market in the U.S. is expected to grow significantly at a CAGR of 3.3% from 2026 to 2033. In the U.S., smartphone growth is supported by intense competition among carriers providing attractive financing and trade-in programs that lower the entry barrier for high-end devices. The proliferation of e-commerce platforms and direct-to-consumer sales models enhances accessibility.

Europe Smartphone Market Trends

The smartphone market in Europe is anticipated to register considerable growth from 2026 to 2033. The European smartphone market benefits from stringent sustainability and e-waste regulations, pushing manufacturers toward offering modular designs, recyclability, and extended software support. Consumers are increasingly attracted to eco-conscious brands and mid-range models offering high value at competitive prices. The growth of fintech and the integration of digital ID into smartphones also supports higher adoption across the public and private sectors.

The UK smartphone market is expected to grow rapidly in the coming years as. In the UK, growth is driven by the rapid adoption of 5G networks and demand for budget-friendly 5G-enabled devices among younger consumers. A rising gaming culture, coupled with smartphones optimized for high-performance gaming, supports segment growth. Furthermore, frequent promotional tie-ins with streaming and entertainment services are creating additional incentives for upgrades

The Germany smartphone market held a substantial market share in 2025. Germany’s smartphone market is propelled by a strong demand for data privacy and security-centric devices, encouraging manufacturers to provide enhanced encryption and GDPR-compliant features. The country’s large industrial workforce and SME sector fuel the adoption of rugged and enterprise-grade smartphones. Additionally, growing popularity of dual-SIM and multi-functional devices caters to Germany’s business-travel-heavy consumer base.

Asia Pacific Smartphone Industry Trends

Asia Pacific dominated the global market with the largest revenue share of 47.9% in 2025. The Asia Pacific smartphone market is growing rapidly due to the massive young demographic and rising internet penetration in emerging economies. Local OEMs are aggressively innovating with competitive pricing, advanced features, and localized apps, boosting adoption. Rapid expansion of mobile-first financial services, super apps, and digital entertainment platforms is creating sustained demand, particularly in India and Southeast Asia.

The Japan smartphone market is expected to grow rapidly in the coming years. Japan’s smartphone growth is driven by demand for highly sophisticated, compact, and durable devices that cater to tech-savvy consumers. Integration of smartphones with advanced robotics, IoT-enabled homes, and automotive ecosystems adds unique market traction. Moreover, Japan’s aging population fuels demand for senior-friendly smartphones with larger interfaces, emergency functions, and health monitoring features.

The China smartphone market held a substantial market share in 2025. China’s smartphone market is led by aggressive innovation cycles, with local giants rapidly pushing foldables, high-resolution displays, and AI-driven ecosystems at competitive prices. Domestic manufacturing dominance allows faster adoption of cutting-edge hardware. Government-driven digital initiatives such as e-CNY wallets and smart city applications also encourage deeper smartphone penetration across urban and rural areas.

Key Smartphone Company Insights

Key players operating in the smartphone industry are Apple Inc., Samsung Electronics Co. Ltd., Xiaomi Corporation, Google LLC, and OnePlus. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In July 2025, Apple Inc. launched AppleCare+ One, a unified subscription plan that consolidates coverage for iPhone, Mac, iPad, and Apple Watch into a single package. It simplifies device protection, includes theft and loss coverage, and offers priority support.

-

In January 2025, Google LLC acquired part of HTC’s extended reality (XR) unit for approximately USD 250 million, transferring select VIVE engineering talent and non-exclusive IP rights. This supports Google’s Android XR platform development and deeper partnerships in the XR ecosystem.

-

In July 2024, Xiaomi Corporation partnered with Dixon, DBG, and other EMS companies to assemble smartphones and other devices in India, aiming to reach 55% local component sourcing and double device shipments to 700 M in India over the next decade.

Key Smartphone Companies:

The following key companies have been profiled for this study on the smartphone market.

- Apple Inc.

- Asus

- Google LLC

- Huawei

- HMD Global

- Lenovo Group Limited

- Motorola

- OnePlus

- Oppo

- Realme

- Samsung Electronics Co. Ltd.

- Sony Corporation

- Vivo

- Xiaomi Corporation

- ZTE Corporation

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Apple, Samsung Electronics, Xiaomi, OPPO, vivo

- Focusing heavily on AI-enabled smartphones, premium ecosystem integration, and proprietary software enhancements such as One UI and iOS ecosystem services

- Expanding manufacturing and assembly operations across India, Vietnam, and Southeast Asia to diversify supply chains

- Strengthening omni-channel distribution through telecom operators, branded stores, online marketplaces, and direct-to-consumer platforms

- Investing significantly in foldable smartphones, advanced camera systems, semiconductor optimization, and ecosystem devices such as wearables and tablets.

- Strong brand loyalty and global consumer recognition provide pricing power and high customer retention

- Extensive economies of scale in procurement, manufacturing, and global distribution improve profitability and market reach

- Deep integration of hardware, software, cloud services, and app ecosystems creates strong vendor lock-in

- Broad product portfolios across premium, mid-range, and entry-level devices allow large-scale market penetration.

- High dependence on semiconductor suppliers and global component supply chains increases exposure to shortages and pricing volatility

- Premium-focused vendors face slower unit growth in mature markets due to extended replacement cycles

- Regulatory scrutiny regarding app ecosystems, repairability, data privacy, and market dominance continues increasing globally

- Intense competition in the mid-range and budget segments places pressure on margins and pricing strategies.

Emerging Players: HONOR, realme, Nothing, Transsion Holdings, ASUS ROG

- Leveraging aggressive pricing strategies and online-first smartphone launches to rapidly capture younger consumer segments

- Differentiating through gaming smartphones, fast charging technologies, AI photography, and design-focused devices

- Expanding presence in emerging markets across India, Africa, Southeast Asia, and Latin America

- Using social media-driven marketing, influencer partnerships, and flash-sale models to improve brand visibility.

- Greater flexibility in adopting new technologies and responding quickly to market trends

- Strong value-for-money positioning attracts cost-sensitive and first-time smartphone buyers

- Focused product strategies help address niche segments such as gaming, creator-focused, or youth-centric smartphones

- Lower operating structures allow faster market entry and pricing competitiveness.

- Limited brand recognition and weaker premium ecosystem positioning compared to global leaders

- Lower control over semiconductor sourcing and supply chain infrastructure

- Heavy dependence on online channels may restrict offline retail penetration in some regions

- Smaller R&D budgets and patent portfolios compared to established smartphone manufacturers.

Smartphone Market Report Scope

Report Attribute

Details

Market size in 2025

USD 537.6 billion

Estimated market size in 2026

USD 556.4 billion

Projected market size by 2033

USD 749.1 billion

Growth rate

CAGR of 4.3% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Operating System, distribution channel, price range, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Apple Inc.; Asus; Google LLC; Huawei; HMD Global; Lenovo Group Limited; Motorola; OnePlus; Oppo; Realme; Samsung Electronics Co. Ltd.; Sony Corporation; Vivo; Xiaomi Corporation; ZTE Corporation

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Smartphone Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the smartphone market report based on operating system, distribution channel, price range, and region.

-

Operating System Outlook (Revenue, USD Billion, 2021 - 2033)

-

Android

-

iOS

-

Others

-

-

Distribution Channel Outlook (Revenue, USD Billion, 2021 - 2033)

-

Online

-

Offline

-

-

Price Range Outlook (Revenue, USD Billion, 2021 - 2033)

-

Entry Level

-

Mid-Range

-

Premium

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Customized cross-segmentation analysis for the smartphone market by price range, OS, and distribution channel

Conducted cross-segmentation analysis by operating system, price band, and sales channel

Evaluated major categories such as Android smartphones, iOS smartphones, foldables, gaming smartphones, and smart feature phones

Assessed online vs offline distribution trends across regions

Identified high-adoption device categories and consumer preferences

Highlighted premiumization and replacement cycle trends

Supported strategic understanding of regional purchasing behavior and channel penetration

Smartphone shipment and unit analysis

Provided smartphone shipment volume estimates (Units) across regions, and operating systems

Analyzed historical and forecast unit shipment trends by smartphone category and price segment

Evaluated ASP trends alongside unit growth patterns

Identified attractive regional expansion markets

Supported GTM and channel partnership strategy

Enabled strategic expansion into high-growth smartphone ecosystems

Conducted consumer behavior analysis for smartphone operating systems (Android vs iOS)

Conducted primary research and consumer surveys to evaluate smartphone purchasing preferences between Android and iOS users

Analyzed factors including brand loyalty, app ecosystem preference, pricing sensitivity, camera preference, and switching behavior

Assessed regional and demographic differences in OS adoption trends

Identified key consumer decision-making factors and ecosystem lock-in trends

Highlighted differences in premium vs value-driven consumer segments

Supported customer targeting, marketing strategy, and ecosystem positioning initiatives

Frequently Asked Questions About This Report

The global smartphone market size was valued at USD 537.6 billion in 2025 and is estimated at USD 556.4 billion for 2026.

The global smartphone market is expected to grow at a CAGR of 4.3% from 2026 to 2033, reaching USD 749.1 billion by 2033.

Asia Pacific dominated with a 47.9% revenue share in 2025.

Key players include Apple Inc.; Asus; Google LLC; Huawei; HMD Global; Lenovo Group Limited; Motorola; OnePlus; Oppo; Realme; Samsung Electronics Co. Ltd.; Sony Corporation; Vivo; Xiaomi Corporation; ZTE Corporation

Key drivers include the proliferation of AI-powered functionalities such as on-device generative AI, enhanced mobile photography, and real-time language translation, as well as growing integration with IoT ecosystems.

The android segment led with a 60.8% revenue share in 2025.

The offline segment held the largest revenue share in 2025, while the online segment is the fastest-growing.

The mid-range segment held the largest revenue share in 2025, while the premium segment is the fastest-growing.

About the Author(s)

Electronic Devices Research Team

Semiconductors & Electronics · Electronic DevicesThis report was authored by the electronic devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the electronic devices segment of the semiconductors & electronics industry. All findings are based on proprietary semiconductors & electronics databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.