- Home

- »

- Plastics, Polymers & Resins

- »

-

Organic Substrate Packaging Material Market Market Report, 2026-2033GVR Report cover

![Organic Substrate Packaging Material Market (2026 - 2033)Report]()

Organic Substrate Packaging Material Market (2026 - 2033)

Size, Share & Trends Analysis Report By Technology (SO Packages, GA Packages, Flat No-leads Packages), By Application (Consumer Electronics, Automotive, Manufacturing, Healthcare), By Region, And Segment Forecasts

Market Size, 2025

$16.9BMarket Estimate, 2026

$17.7BMarket Forecast, 2033

$25.6BCAGR, 2026–2033

5.4%Organic Substrate Packaging Material Market Summary

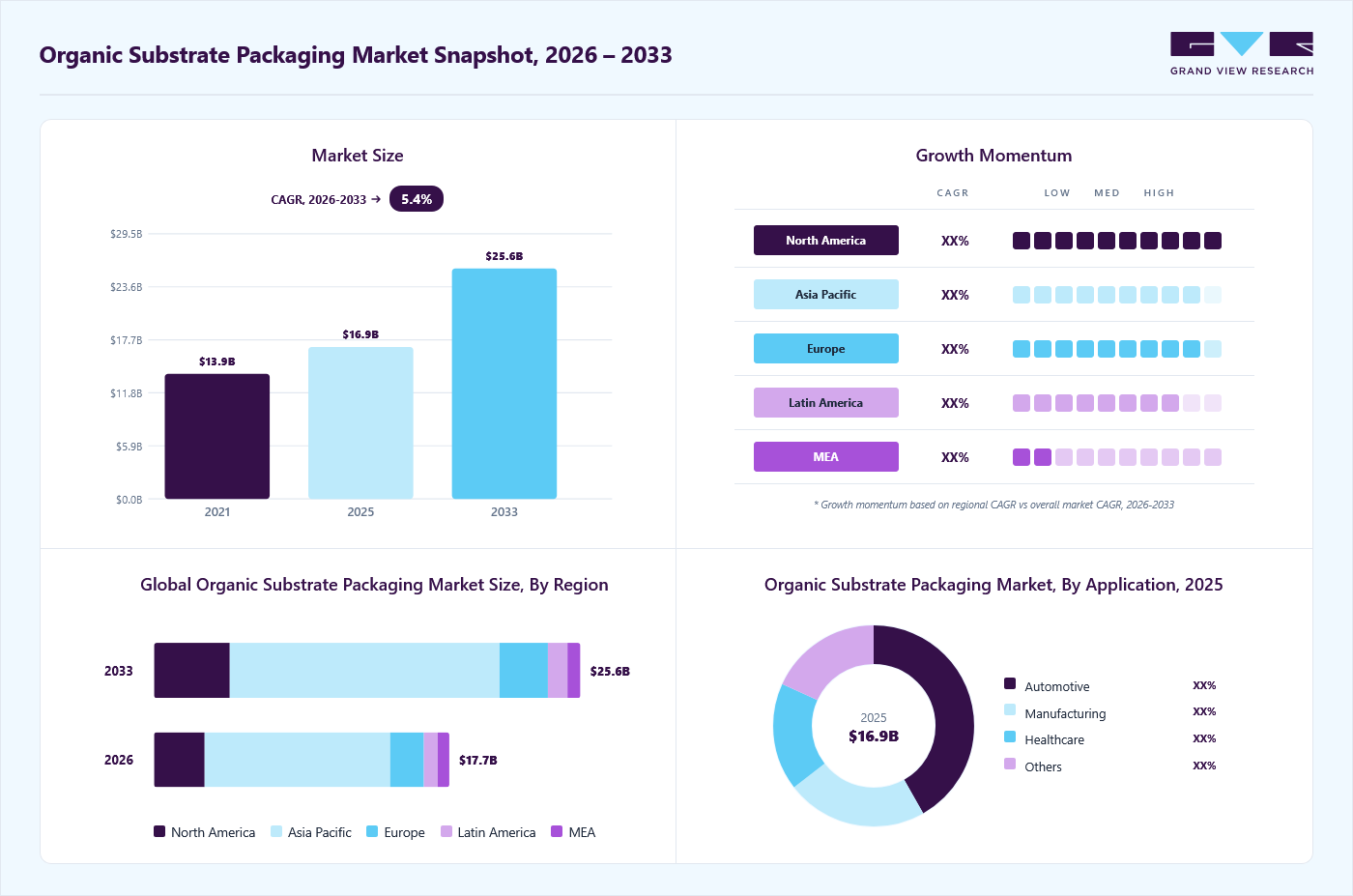

The global organic substrate packaging material market market size was valued at USD 16.9 billion in 2025 and is projected to grow from USD 17.7 billion in 2026 to USD 25.6 billion by 2033, at a CAGR of 5.4% from 2026 to 2033. The Asia Pacific held the largest share of 62.7% of the global market in 2025. The market is driven by the growing demand for compact, high-performance electronic devices and the rapid expansion of the consumer electronics and automotive sectors.

Key Market Trends & Insights

- By technology: SO packages segment held the largest market share of 42.0% in 2025.

- By application: Consumer electronics segment held the largest market share of 45.6% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (62.7% revenue share, 2025)

- Fastest-growing regional market: North America (highest CAGR, 2026-2033)

- By country: China held the largest share in 2025

Market Size & Forecast

- Market size in 2025: USD 16.9 Billion

- Estimated market size in 2026: USD 17.7 Billion

- Projected market size by 2033: USD 25.6 Billion

- CAGR (2026-2033): 5.4%

In addition, advancements in semiconductor packaging technologies are boosting the adoption of organic substrates over traditional materials. One of the primary drivers of the global organic substrate packaging material industry is the growing demand for advanced semiconductor packaging technologies such as System-in-Package (SiP), Flip Chip, and Fan-Out Wafer Level Packaging (FOWLP). These technologies require high-performance substrates that can handle higher I/O densities, miniaturization, and faster signal transmission. Organic substrates, made primarily from resin-coated copper, BT resin, and ABF materials, are cost-effective and offer reliable performance for these next-generation chipsets. For instance, with the rise of 5G base stations and AI accelerators, companies such as Samsung and Intel are increasing their use of organic substrates for multi-die packaging.")

In addition, the rapid expansion of consumer electronics and mobile devices, especially in emerging economies, is contributing to market growth. Smartphones, tablets, wearable devices, and smart home technologies are integrating more complex and compact integrated circuits, which drives the need for high-layer-count organic substrates. With Apple’s ongoing integration of custom SoCs (e.g., M-series chips) and Android device makers pushing AI-enhanced processors, the demand for compact, thermally stable, and cost-effective organic substrate materials is intensifying. These trends are pushing substrate manufacturers to scale up production while investing in advanced materials like Ajinomoto Build-up Film (ABF).

Moreover, the automotive electronics sector is a fast-emerging growth vertical, especially with the global shift towards electric vehicles (EVs) and advanced driver-assistance systems (ADAS). Automotive chips need to be robust, thermally stable, and reliable, making organic substrates an ideal choice for Electronic Control Units (ECUs), battery management systems, and infotainment devices. Major automotive OEMs and Tier-1 suppliers are increasingly collaborating with semiconductor packaging firms to source organic substrates tailored for harsh environmental conditions. For example, Bosch and Continental are driving demand through their focus on EV powertrain electronics and autonomous driving modules, indirectly fueling the global industry.

Market Characteristics & Concentration

The organic substrate packaging material industry is capital-intensive, requiring significant investment in manufacturing facilities, cleanrooms, photolithography, and advanced lamination equipment. Moreover, it is driven by rapid technological evolution, demanding continuous R&D in substrate materials, miniaturization, and thermal/electrical performance. Key players invest heavily in next-gen substrate innovation to meet rising demands from AI, HPC, and 5G chipmakers.

The organic substrate packaging material industry is closely tied to the semiconductor ecosystem, especially OSATs (Outsourced Semiconductor Assembly and Test) and IDM (Integrated Device Manufacturer) companies. Demand fluctuations in end-use industries such as consumer electronics, automotive, and telecom directly affect substrate material consumption. For example, when smartphone makers ramp up new chip production cycles, demand for ABF substrates spikes.

Organic substrate production is highly concentrated in East Asia (Japan, South Korea, Taiwan, China), making the supply chain susceptible to geopolitical tensions, trade restrictions, and raw material availability. In addition, upstream dependency on high-performance resins and copper foils adds another layer of vulnerability.

Technology Insights

The SO packages segment led the market with the largest revenue share of 42.0% in 2025 and is expected to grow at the fastest CAGR of 5.9% during the forecast period. They are commonly used for integrated circuits in consumer electronics, automotive, and industrial applications due to their cost efficiency and space-saving design. The growth of the consumer electronics and automotive sectors, especially with the rise of compact electronic control units (ECUs), is driving demand for SO packages. Their ease of assembly on printed circuit boards (PCBs) and cost-effective production make them the preferred choice in high-volume applications, particularly in smartphones, infotainment systems, and household electronics.

The GA packages, including Ball Grid Array (BGA) and Chip Grid Array (CGA), offer higher input/output (I/O) density and better electrical performance than traditional leaded packages. These are widely used in high-performance computing, telecommunications, and gaming systems. The demand for high-speed data processing and miniaturization in advanced computing devices is a significant driver. GA packages allow for more connections and better thermal performance, aligning with industry needs for AI chips, 5G infrastructure, and data center equipment. The push for enhanced signal integrity in densely populated circuits further boosts adoption.

Application Insights

The consumer electronics segment led the market with the largest revenue share of 45.6% in 2025. Consumer electronics is the dominant application segment for organic substrate packaging materials. These materials are extensively used in smartphones, tablets, laptops, wearables, and gaming devices due to their compact size, high wiring density, and thermal performance. The increasing demand for miniaturized, multifunctional, and high-speed consumer electronic devices is a key driver. The rollout of 5G, advancements in AI and IoT, and higher performance expectations in mobile computing are pushing manufacturers toward high-density packaging substrates.

The automotive segment is projected to grow at the fastest CAGR of 6.0% during the forecast period. In the automotive sector, organic substrate packaging materials are utilized in electronic control units (ECUs), infotainment systems, ADAS, and electric powertrain modules. With the growing adoption of electric vehicles (EVs) and autonomous driving technologies, the integration of electronics in vehicles is rapidly expanding. The shift toward connected and electric vehicles is significantly increasing the electronic content per vehicle. As EVs require high-performance power electronics and battery management systems, the demand for thermally stable, reliable, and compact packaging solutions, such as organic substrates, is rising. Government policies on emission reductions and the development of smart mobility are further accelerating this trend.

Regional Insights

Asia Pacific dominated the organic substrate packaging material market with the largest revenue share of 62.7% in 2025. This positive outlook is due to rapid industrialization, booming electronics manufacturing, and strong demand for advanced packaging solutions. Countries such as China, Japan, South Korea, and Taiwan are major hubs for semiconductor and consumer electronics production, driving the need for high-performance organic substrates. For example, the proliferation of 5G technology, IoT devices, and AI chips in China and South Korea has increased demand for substrates with superior thermal and electrical properties. In addition, government initiatives such as China’s "Made in China 2025" and India’s semiconductor incentives further boost local manufacturing, accelerating market growth.

North America Organic Substrate Packaging Material Market Trends

The organic substrate packaging material market in North America is expected to grow at the fastest CAGR of 5.9% over the forecast period, driven by technological innovation, robust R&D investments, and strong demand from the automotive and aerospace sectors. The U.S. and Canada are home to leading semiconductor companies such as Intel and AMD, which require advanced organic substrates for high-performance computing (HPC) and AI applications. The growing adoption of electric vehicles (EVs) in the U.S. also fuels demand for reliable packaging materials in power electronics. Furthermore, defense and aerospace applications in the region require robust substrates for harsh environments, driving advancements in materials such as polyimide and liquid crystal polymer (LCP).

Europe Organic Substrate Packaging Material Market Trends

The organic substrate packaging material market in Europe is driven by the automotive industry’s shift toward electrification and by stringent environmental regulations that promote the use of sustainable materials. Germany, France, and the Netherlands lead in automotive electronics, with companies such as Bosch and Infineon requiring high-reliability substrates for EV power modules and ADAS (Advanced Driver Assistance Systems). In addition, Europe’s strong medical device industry demands biocompatible organic substrates for implantable electronics. The EU’s focus on reducing electronic waste also drives innovation in recyclable and halogen-free substrate materials, giving European manufacturers a competitive edge in eco-friendly packaging solutions.

Key Organic Substrate Packaging Material Company Insights

The competitive environment of the global organic substrate packaging material industry is moderately fragmented, with a mix of established players and emerging companies competing based on material innovation, sustainability, and performance efficiency. Key players are leveraging advanced R&D capabilities to develop lightweight, environmentally friendly, and thermally stable substrates to meet rising demand from electronics, automotive, and healthcare sectors. The market is also seeing increased collaboration between substrate manufacturers and semiconductor firms to develop tailored packaging solutions, particularly for 5G, IoT, and wearable device applications.

Key Organic Substrate Packaging Material Companies:

The following key companies have been profiled for this study on the organic substrate packaging material market.

- Amkor Technology Inc.

- Kyocera Corporation

- Microchip Technology Inc.

- Texas Instruments Incorporated

- ASE Kaohsiung

- Simmtech Co., Ltd

- LG Innotek Co. Ltd

- AT&S

- Daeduck Electronics Co., Ltd

Recent Development

-

In July 2024, Japan’s Shin-Etsu Chemical launches advanced equipment for semiconductor packaging that leverages a novel dual damascene method, utilizing excimer laser technology to directly form interposer functions within package substrates. This innovation eliminates the need for a separate interposer in chiplet assembly, significantly simplifying the process, enabling finer microfabrication than current mainstream methods, and reducing both costs and capital investment by removing the photoresist step.

-

In September 2024, Onto Innovation Inc. announced the opening of its Packaging Applications Center of Excellence (PACE) in Wilmington, Massachusetts, marking the first facility of its kind in the U.S. dedicated to advancing panel-level packaging (PLP) technologies for 2.5D and 3D chiplet architectures and AI packages.

Organic Substrate Packaging Material Market Report Scope

Report Attribute

Details

Market size in 2025

USD 16.9 billion

Estimated market size in 2026

USD 17.7 billion

Projected market size by 2033

USD 25.6 billion

Growth rate

CAGR of 5.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Technology, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; China; India; Japan; Australia; South Korea; Brazil; Argentina; South Africa; Saudi Arabia; UAE

Key companies profiled

Amkor Technology Inc.; Kyocera Corporation; Microchip Technology Inc.; Texas Instruments Incorporated; ASE Kaohsiung; Simmtech Co., Ltd; Shinko Electric Industries Co., Ltd.; LG Innotek Co., Ltd; AT&S; Daeduck Electronics Co., Ltd

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional, and segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Organic Substrate Packaging Material Market Report Segmentation

This report forecasts revenue growth at a global level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global organic substrate packaging material market report based on technology, application, and region:

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

SO packages

-

GA packages

-

Flat no-leads packages

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Consumer Electronics

-

Automotive

-

Manufacturing

-

Healthcare

-

Others

-

-

Region Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

The key players in the organic substrate packaging material market include Amkor Technology Inc; Kyocera Corporation; Microchip Technology Inc.; Texas Instruments Incorporated; ASE Kaohsiung; Simmtech Co., Ltd; Shinko Electric Industries Co. Ltd; LG Innotek Co. Ltd; AT&S; and Daeduck Electronics Co., Ltd

The market is driven by the growing demand for compact, high-performance electronic devices and the rapid expansion of the consumer electronics and automotive sectors. Additionally, advancements in semiconductor packaging technologies are boosting the adoption of organic substrates over traditional materials.

The global organic substrate packaging material market is expected to grow at a compound annual growth rate of 5.4% from 2026 to 2033 to reach around USD 25.6 billion by 2033.

Asia Pacific dominated with a 62.7% revenue share in 2025.

North America is the fastest-growing region over the forecast period.

The SO packages segment led with a 42.0% revenue share in 2025 and is expected to grow at the fastest CAGR of 5.9% during the forecast period.

The global organic substrate packaging material market was estimated at around USD 16.9 billion in the year 2025 and is expected to reach around USD 17.7 billion in 2026.

Consumer electronics dominated the end-use segment in 2025 with over 45.6% value share due to the increasing demand for compact, high-performance devices and the rapid advancement in semiconductor integration.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.