- Home

- »

- Animal Health

- »

-

Pet Services Market Size, Share, Trends Report, 2026-2033GVR Report cover

![Pet Services Market (2026 - 2033)Report]()

Pet Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Service (Medical, Non-Medical), By Pet (Dogs, Cats), By Delivery Channel (Commercial Facilities, Mobile), By Service Provider (Hospital & Clinics, Standalone Institutions), By Region, And Segment Forecasts

Market Size, 2025

$65.1BMarket Estimate, 2026

$70.6BMarket Forecast, 2033

$125.8BCAGR, 2026–2033

8.6%Pet Services Market Summary

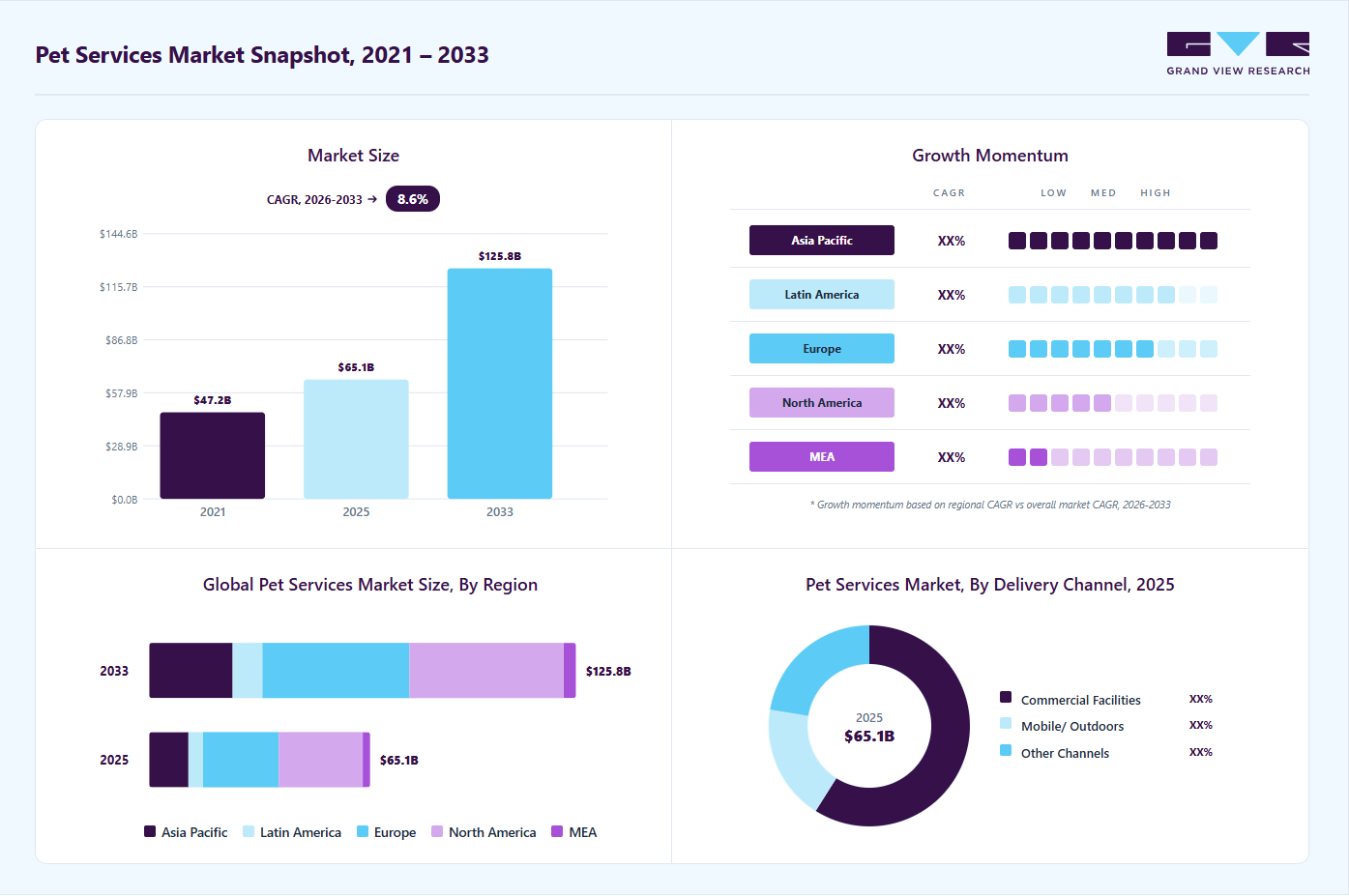

The global pet services market size was valued at USD 65.1 billion in 2025 and is projected to grow from USD 70.6 billion in 2026 to USD 125.8 billion by 2033, at a CAGR of 8.6% from 2026 to 2033. The market in North America dominated with a revenue share of 38.0% in 2025. Some of the key factors driving market growth are rising disposable income and premiumization, expanding urbanization and the growth of nuclear households, and increased fundraising and investment in pet service startups.

Key Market Trends & Insights

- By service: Medical services segment held the largest market share of 67.6% in 2025.

- By pet: Dogs segment held the largest market share in 2025.

- By delivery channel: Commercial facilities segment held the largest market share in 2025.

- By service provider: Hospitals and clinics segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (38.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 65.1 Billion

- Estimated market size in 2026: USD 70.6 Billion

- Projected market size by 2033: USD 125.8 Billion

- CAGR (2026-2033): 8.6%

As disposable incomes rise, pet owners are more willing to spend on premium, customized services that enhance their pets’ comfort and quality of life. This growing financial capacity fuels demand for luxury grooming, boutique boarding, and personalized training programs. According to the American Pet Products Association (APPA) 2025 State of the Industry Report, revealed that U.S. pet industry spending reached USD 152 billion in 2024 and is projected to rise to USD 157 billion in 2025, reflecting continued market growth. In addition, according to a Redseer report, pet spending in India surged from USD 1.6 billion in 2019 to USD 3.6 billion in 2024, driven by rising demand for pet boarding, insurance, and specialized veterinary care. As a result, pet service providers are expanding high-end offerings with superior amenities and specialized care packages. The shift toward premiumization also drives innovation in service quality, technology integration, and customer experience.")

As urbanization accelerates and households shift toward smaller, nuclear family structures, the demand for structured and reliable pet services has intensified. The busier schedules and limited living space, pet owners depend on professional support in large numbers for daily care needs. This lifestyle shift has fueled rapid growth in urban pet service ecosystems, including grooming studios, veterinary care centers, pet-sitting networks, and mobile service models. In addition, apartment living, particularly, is driving strong demand for dog walking, daycare, enrichment programs, and behavioral training, as pets require stimulation and supervision beyond what owners can provide at home. The rise of tech-enabled service platforms offering app-based bookings, smart monitoring, and personalized care plans further reflects the market’s shift toward convenience, transparency, and premium service expectations. Thus, these trends show how evolving urban lifestyles are transforming pets into integral parts of people's lives.

Moreover, the market growth is also driven by the rapid growth of the pet care startup ecosystem. Some of the emerging startups are introducing innovative, tech-enabled solutions such as mobile grooming, on-demand vet consultations, and digital pet wellness platforms. For instance, in June 2025, Pawzeeble, India based startup, has been building a tech-driven pet care ecosystem connecting pet parents, services, and brands. It aims to enhance responsible pet parenting through community engagement and digital solutions. In addition, in May 2026, AnimalsLover expanded its digital ecosystem with AI-enabled pet community services, nationwide dog hostel networks, and integrated commerce platforms, strengthening digital service penetration and supporting steady market growth. These startups utilize AI, IoT, and data analytics to enhance service personalization and convenience. They are supported by strong investor interest and consumer adoption that are expanding market accessibility through subscription models, doorstep delivery, and integrated care networks. Thus, the influx of entrepreneurial activity is intensifying competition, improving service quality, and accelerating market growth.

Market Concentration & Characteristics

The pet services industry is moderately fragmented, and the pace is accelerating, with numerous regional and local players alongside emerging tech-driven startups. The global brands such as Petco and Rover dominate the mature industry, and India and other developing regions remain highly competitive, driven by niche providers offering personalized grooming, boarding, and wellness services.

The pet services market is witnessing strong innovation through AI-powered health monitoring, tele-veterinary apps, smart grooming tools, and personalized wellness plans. Companies are adopting data-driven insights and subscription-based service models to enhance convenience. Innovation is centered on pet well-being. For instance, in March 2026, Pilo Tech launched AI-enabled pet care solutions integrating smart feeding and health monitoring systems, advancing digital pet care ecosystems, increasing demand for tech-enabled pet services, personalized monitoring, and data-driven veterinary support, thereby accelerating industry expansion.

Mergers and acquisitions are transforming the industry as leading players consolidate to expand service portfolios and geographic reach. Large veterinary chains and pet care brands are acquiring grooming, training, and telehealth startups to build integrated ecosystems. For instance, in 2026, Covetrus and MWI Animal Health announced a USD 3.5 billion merger integrating distribution, software, and pharmacy services, enhancing service accessibility, streamlining veterinary workflows, and supporting cost efficiencies.

Regulations increasingly emphasize animal welfare, professional licensing, and hygiene standards in grooming, boarding, and veterinary practices. Governments are tightening compliance for service quality, waste management, and health certification. Regulatory scrutiny also promotes transparency in online pet services and veterinary teleconsultations, encouraging formalization and quality assurance across the pet services ecosystem.

Service expansion in the pet services industry is driven by the integration of clinical care, diagnostics, pharmacy, and digital platforms within unified ecosystems. Companies are broadening offerings to include telehealth, preventive care plans, grooming, and behavioral services. Furthermore, partnerships between distributors and technology providers enhance service delivery efficiency, improve client engagement, and support continuity of care, thereby increasing service utilization across companion animal settings.

The market is expanding rapidly across emerging regions, driven by rising pet ownership, urbanization, and disposable income. International brands are entering the Middle East and Asia industry through franchising and partnerships, while local entrepreneurs develop customized offerings.

Service Insights

The medical services segment dominated the pet services market, accounting for the largest revenue share of 67.6% in 2025. This segment comprises diagnosis, preventative care, and treatment. The segment is driven by increasing pet ownership, rising awareness of preventive care, and the humanization of pets. The growing prevalence of pet obesity, diabetes, and age-related conditions further boosts demand for medical services. In addition, veterinary consultations, diagnostics, surgeries, vaccinations, and specialized treatments contribute significantly to revenue. For instance, in February 2026, Mars Incorporated launched a grant program in India with Humane World for Animals to expand veterinary access, vaccination, and sterilization services, strengthening service infrastructure. Furthermore, pet parents are prioritizing health and wellness, opting for regular check-ups, advanced therapies, and chronic disease management for their pets. Tele-veterinary consultations, mobile clinics, and digital health monitoring are enhancing accessibility and convenience, accelerating market growth.

The non-medical services, such as grooming, daycare, boarding, training, and pet walking, represent the fastest-growing segment over the forecast period. The rising urbanization, dual-income households, and busy lifestyles are driving demand for convenient, professional care solutions. Moreover, innovations such as mobile grooming vans, tech-enabled booking platforms, and subscription-based daycare services enhance accessibility and customer convenience. These services grow faster because they involve recurring, high-frequency use, unlike medical visits, creating consistent demand throughout the year. In addition, they are more discretionary and trend-driven, allowing providers to quickly introduce new offerings and scale them without regulatory constraints, accelerating market expansion.

Pet Insights

The dogs segment dominated the pet services industry, accounting for the largest revenue share in 2025. The segment comprises small, medium, and large breed dogs. This segment is driven by their widespread ownership, strong human-animal bonds, and high expenditure on health, grooming, and lifestyle services. Pet parents increasingly treat dogs as family members, investing in premium grooming, daycare, boarding, training, and medical care. In the U.S., the average dog owner spends approximately USD 2,524 annually, or about USD 210 per month, on regular pet-related expenses. Other factors include a rise in nuclear households, a declining birth rate in key markets, and an increase in pet insurance adoption. In addition, rising awareness of canine health, behavior, and nutrition fuels demand for specialized offerings.

The cats segment is projected to grow at the fastest CAGR from 2026 to 2033. The market’s expansion is fueled by increasing adoption in urban households and the rise of single-person and dual-income families. According to a World Animal Foundation report from July 2025, U.S. animal shelters received 5.8 million animals,marking a 0.4% increase from 2023, accompanied by 17,153 additional adoptions compared to the previous year. Furthermore, owners are investing more in feline-specific services, including grooming, boarding, daycare, veterinary care, and enrichment activities, highlighting the growing humanization of cats.

Delivery Channel Insights

Thecommercial facilities segment accounted for the largest market revenue share in 2025. The segment growth is driven by urbanization and dual-income households, which drive demand for professional, convenient, and safe environments for pets. In addition, technological integration, including app-based bookings, smart monitoring, and digital health tracking, enhances operational efficiency and customer experience. For instance, in August 2025, Bengaluru-based PawSpace startup offered pet sitting, boarding, grooming, and pet taxi services through an asset-light, Urban Company-style model, aiming to simplify safe, convenient pet care. Such initiatives play a critical role in meeting the evolving needs of modern pet owners.

The other segment, comprising at-home and online pet service channels, is expected to grow at the fastest CAGR from 2026 to 2033, driven by convenience, urban lifestyles, and rising demand for personalized care. Some of the services, such as mobile grooming, in-home veterinary visits, dog walking, and tele-veterinary consultations, allow pet owners to access professional care without leaving their homes. Online platforms and apps facilitate easy booking, real-time tracking, and subscription-based models, enhancing engagement.

Service Provider Insights

The hospitals and clinics was the largest service provider segment in 2025, owing to rising awareness of preventive care, and growing expenditure on pet health. Veterinary consultations, diagnostics, surgeries, vaccinations, and chronic disease management are key revenue contributors. The segment also benefits from the rising prevalence of chronic conditions, senior pets, and exotic breeds. In addition, growing awareness regarding animal health and higher spending on premium pet care services continue to drive patient visits to veterinary hospitals and multi-specialty clinics. These facilities also benefit from advanced diagnostic infrastructure, skilled veterinary professionals, and the availability of specialized services such as rehabilitation, dental care, and chronic disease management.

The standalone institutions, which include clinical and nonclinical institutions like diagnostic laboratories, boarding/sitting/grooming institutions, among others; represents the fastest growing segment over the forecast period due to their rapid expansion fueled by urbanization, rising disposable incomes, and increasing pet humanization, prompting owners to seek personalized, high-quality care. They offer flexibility, customized services, and niche expertise, catering to specific breed needs, behavioral training, or wellness preferences, unlike large hospital chains.

Regional Insights

North America dominated the pet services industry with the largest revenue share of 38.0% in 2025. The market growth is driven by rising pet humanization, increased spending on premium care, and growing demand for convenience-based offerings like mobile grooming and daycare. Major players such as PetSmart, Rover, and Wag!, alongside niche startups offering specialized wellness and training services. The regulatory landscape emphasizes animal welfare, sanitation, and licensing standards for boarding and grooming facilities.

In addition, technological advancements such as AI-driven health monitoring, tele-veterinary platforms, and app-based booking systems are enhancing service quality and customer experience. For instance, in November 2025, DocuPet launched the National Pet Registry and National Animal Shelter Network, launching North America’s first unified pet registration system to streamline shelter operations and improve lost pet recovery through real-time, connected data.

U.S. Pet Services Market Trends

The U.S. pet services industry accounted for the largest share of North America in 2025, owing to an aging pet population, increasing millennial and GEN Z pet ownership, and the expansion of e-commerce and DTC services. According to a report, in the U.S., the proportion of senior pets has increased notably, with senior dogs rising from 42% to 52% and senior cats from 46% to 52% between 2012 and 2022. Furthermore, technological advancements are transforming service delivery. In addition, in April 2026, 24Pet launched 24PetShelter, a cloud-based platform that streamlines shelter operations from intake to adoption, enhancing operational efficiency, supporting digital transformation, and improving service delivery, thereby strengthening technology integration in the market.

The Canada pet services market is expected to grow at a significant CAGR during the forecast period. The region is transforming due to increasing disposable income and rising awareness of pet health and wellness. For instance, in September 2025, PetSmart Charities of Canada marked Pet Hunger Awareness Day by awarding a USD 100,000 grant to The Food Bank of York Region, supporting pets of families experiencing food insecurity. They partnered with Feed Ontario, an initiative that ensures pets receive the nutrition they need alongside their owners.

Europe Pet Services Market Trends

The Europe pet services industry is expanding rapidly, supported by increasing pet humanization, increasing technological integration, rising urbanization, and busy lifestyles. Some of the major players, such as AniCura, Mars Petcare, and VetPartners, alongside numerous local and regional service providers offering specialized and tech-enabled solutions. For instance, in April 2026, PetPivot Inc launched the AutoScooper 12 in Europe, an offline automated litter system with no app or subscription. This supports privacy-focused innovation, expands smart pet care adoption, and enhances accessibility of tech-enabled services in the market.

The pet services market in the UK is expected to grow significantly over the forecast period. The market is expanding rapidly, driven by growing pet adoption, technological and digital platform innovations, and rising collaborations among emerging players. For instance, in March 2026, Fi expanded into the UK and the EU with its AI-powered dog collar, which offers GPS tracking and health monitoring. This expansion increases adoption of connected pet care solu tions, enhancing preventive services and digital engagement within the market.

The Germany Pet services market held a significant revenue share in 2025. The market is expanding rapidly, supported by growing pet humanization and increased spending on grooming, daycare, and wellness services. In addition, innovations such as digital booking platforms, tele-veterinary consultations, and subscription-based services are gaining momentum. For instance, in April 2026, AlphaPet Ventures acquired Tierliebhaber in Germany, expanding into preventive pet health products, strengthening premiumization trends, broadening service portfolios, and enhancing integration of nutrition and wellness offerings in the market.

Asia Pacific Pet Services Market Trends

Asia Pacific is expected to grow at the fastest CAGR over the forecast period. The regional market is expanding due to a rising pet population, expanding service providers, and increasing disposable incomes. Key players include India’s Petsfolio, offering training, grooming, walking, and boarding services, and Australia’s Pet Care Association INC, established in 1992 to support businesses in daycare, pet resorts, kennels, and dog training. These factors create significant opportunities for market expansion across the region.

The pet services market in Japanaccounted for a significant revenue share in 2025 and is poised for further growth as pet humanization and demand for luxury, convenience, and wellness-focused offerings rise. For instance, in June 2025, Japan’s luxury pet market is booming, as demonstrated at Interpets Asia Pacific 2025, where 980 exhibitors and 78,000 visitors explored innovations in pet food, fashion, grooming, wellness, and accessories, highlighting the nation’s growing demand for premium pet services and products.

The India pet services market is emerging, supported by an expanding middle class and disposable income, a booming pet startup ecosystem, and rising awareness of pet health and wellness. Some of the emerging startups are introducing innovative, tech-enabled solutions such as mobile grooming, on-demand vet consultations, and digital pet wellness platforms. In 2026, India’s pet startups secured significant funding across grooming, veterinary care, food, and technology sectors, driving innovation and reshaping the rapidly growing pet care industry. For instance, in April 2026, Benny’s Bowl raised USD 1.4 million to expand R&D, product portfolio, and distribution in India, supporting innovation in clinical pet nutrition, enhancing service integration, and increasing accessibility, thereby driving growth in the market.

Latin America Pet Services Market Trends

The growth of the Latin America pet services industry is driven by rising pet ownership, urbanization, and the humanization of pets, prompting demand for grooming, daycare, boarding, and wellness services. Expanding disposable incomes and the rise of dual-income households further support spending on premium and convenient care options. The competitive landscape includes local chains, independent service providers, and emerging startups offering specialized and tech-enabled solutions. Consumers increasingly prioritize quality, safety, and health-focused services, driving differentiation and innovation.

The Brazil Pet services market is gaining momentum due to rising pet ownership, increasing pet humanization, and growing demand for convenient, health-focused services such as grooming, daycare, boarding, and tele-veterinary care. In addition, in April 2026, PEDIGREE launched an AI-driven platform in Brazil to support responsible dog adoption through compatibility matching, enhancing digital engagement, increasing adoption rates, and expanding technology-enabled services within the market. In addition, consumers value convenience, quality, and wellness, driving service differentiation, digital adoption, and steady growth across Brazil’s expanding pet services sector.

Middle East & Africa Pet Services Market Trends

The MEA pet services industry’s growth is propelled by rising pet adoption and growing awareness amongst the owners, supported by government initiatives enhancing animal healthcare. For instance, in March 2026, StraySpotter, a digital platform, was launched, connecting abandoned animals with rescue networks in the UAE. This initiative improves rescue coordination, enhances digital service accessibility, and strengthens community-driven engagement within the market.

The South Africa pet services market held the largest revenue share in 2025 and is expanding, fueled by rising consumer awareness of prioritizing convenience, quality, and health-focused offerings, and theincreasing adoption of digital platforms. For instance, in April 2026, the Eastern Cape government, with support from the Food and Agriculture Organization of the United Nations, funded animal health technicians to establish local care facilities. This initiative decentralizes services, improves accessibility, and strengthens primary veterinary support.

The pet services market in the UAE is driven by high disposable incomes, which fuel demand for premium grooming, daycare, boarding, and wellness services. Some of the global brands, regional chains, and niche startups offer specialized and tech-enabled solutions in the UAE. For instance, in April 2026, PetCentral UAE expanded operations to Oman and Qatar, enhancing access to premium pet food and supplies across the GCC. This regional expansion improves distribution reach, strengthens e-commerce adoption, and supports service accessibility within the market.

Key Pet Services Company Insights

The global pet services market is led by major players such as PetSmart, Rover, Mars Petcare, AniCura, and Banfield Pet Hospital. These companies dominate through extensive service networks, premium offerings, and technological integration, while numerous regional and niche providers compete by focusing on specialized, personalized, and tech-enabled pet care solutions.

Key Pet Services Companies:

The following key companies have been profiled for this study on the pet services market.

- CVS Group Plc

- Mars Incorporated

- National Veterinary Associates

- Pets at Home Group PLC

- Greencross Vets

- Fetch! Pet Care

- IVC Evidensia

- A Place for Rover, Inc.

- PetSmart LLC

- Airpets International

- Pooch Dog SPA

- Animals at Home Ltd.

Recent Developments

-

In April 2026, Pets at Home partnered with Rithum to launch a dropship program. This collaboration expands product assortment, accelerates digital innovation, and enhances omnichannel service capabilities in the pet services market.

-

In March 2026, Emirates SkyCargo introduced dedicated pet travel support services to manage bookings and logistics. This initiative improves service reliability, enhances customer experience, and strengthens specialized pet transportation services in the market.

-

In February 2026, Allpets launched its flagship “Clinic & Beyond” in Hyderabad with plans for national expansion. This development strengthens integrated care delivery, increases service accessibility, and supports organized growth in the pet services industry.

Pet Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 65.1 billion

Estimated market size in 2026

USD 70.6 billion

Projected market size by 2033

USD 125.8 billion

Growth rate

CAGR of 8.6% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Service, pet, delivery channel, service provider, regional

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Thailand; South Korea; Australia; Brazil; Argentina; South Africa; UAE; Saudi Arabia; Kuwait; Qatar; Oman

Key companies profiled

CVS Group Plc; Mars Incorporated; National Veterinary Associates; Pets at Home Group PLC; Greencross Vets; Fetch! Pet Care; IVC Evidensia; A Place for Rover, Inc.; PetSmart LLC; Airpets International; Pooch Dog SPA; Animals at Home Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Pet Services Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the pet services market report based on service, pet, delivery channel, service provider, and region:

-

Service Outlook (Revenue, USD Million, 2021 - 2033)

-

Medical Services

-

Diagnosis

-

In-Vitro Diagnosis

-

In-Vivo Diagnosis

-

-

Preventive Care

-

Treatment

-

Consultation

-

Surgery

-

Others

-

-

-

Non-Medical Services

-

Boarding

-

Training

-

Grooming

-

Transportation

-

Sitting & Walking

-

End-of-Life

-

Other Non-Medical Services

-

-

-

Pet Outlook (Revenue, USD Million, 2021 - 2033)

-

Dogs

-

Small Breeds

-

Medium Breeds

-

Large Breeds

-

-

Cats

-

Other Pets

-

-

Delivery Channel Outlook (Revenue, USD Million, 2021 - 2033)

-

Commercial Facilities

-

Mobile/ Outdoors

-

Other Channels

-

-

Service Provider Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospital & Clinics

-

Standalone Institutions

-

Other Providers

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

UAE

-

Saudi Arabia

-

Kuwait

-

Qatar

-

Oman

-

-

Frequently Asked Questions About This Report

The global pet services market size was valued at USD 65.1 billion in 2025 and is estimated at USD 70.6 billion for 2026.

The global pet services market is expected to grow at a CAGR of 8.6% from 2026 to 2033, reaching USD 125.8 billion by 2033.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include CVS Group Plc; Mars Incorporated; National Veterinary Associates; Pets at Home Group PLC; Greencross Vets; Fetch! Pet Care; IVC Evidensia; A Place for Rover, Inc.; PetSmart LLC; Airpets International; AirPets International; Pooch Dog SPA; Animals at Home Ltd.

Key factors that are driving the pet services market growth include the increasing population of companion animals, pet humanization, strategies implemented by key companies, and expenditure on pets.

The medical services segment led with a 67.6% revenue share in 2025, while the non-medical services segment is the fastest-growing.

The dogs segment held the largest revenue share in 2025, while the cats segment is the fastest-growing.

The commercial facilities segment held the largest revenue share in 2025.

The hospitals and clinics segment held the largest revenue share in 2025, while the standalone institutions segment is the fastest-growing.

North America dominated with a 38.0% revenue share in 2025.

About the Author(s)

Animal Health Research Team

Healthcare · Animal HealthThis report was authored by the animal health research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the animal health segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.