- Home

- »

- Clinical Diagnostics

- »

-

Pharmaceutical Sterility Testing Market Report, 2026-2033GVR Report cover

![Pharmaceutical Sterility Testing Market (2026 - 2033)Report]()

Pharmaceutical Sterility Testing Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Outsourcing, In-house), By Test (Sterility Testing, Bioburden Testing, Bacterial Endotoxin Testing), By Product, By Sample, By End-use, By Region, And Segment Forecasts

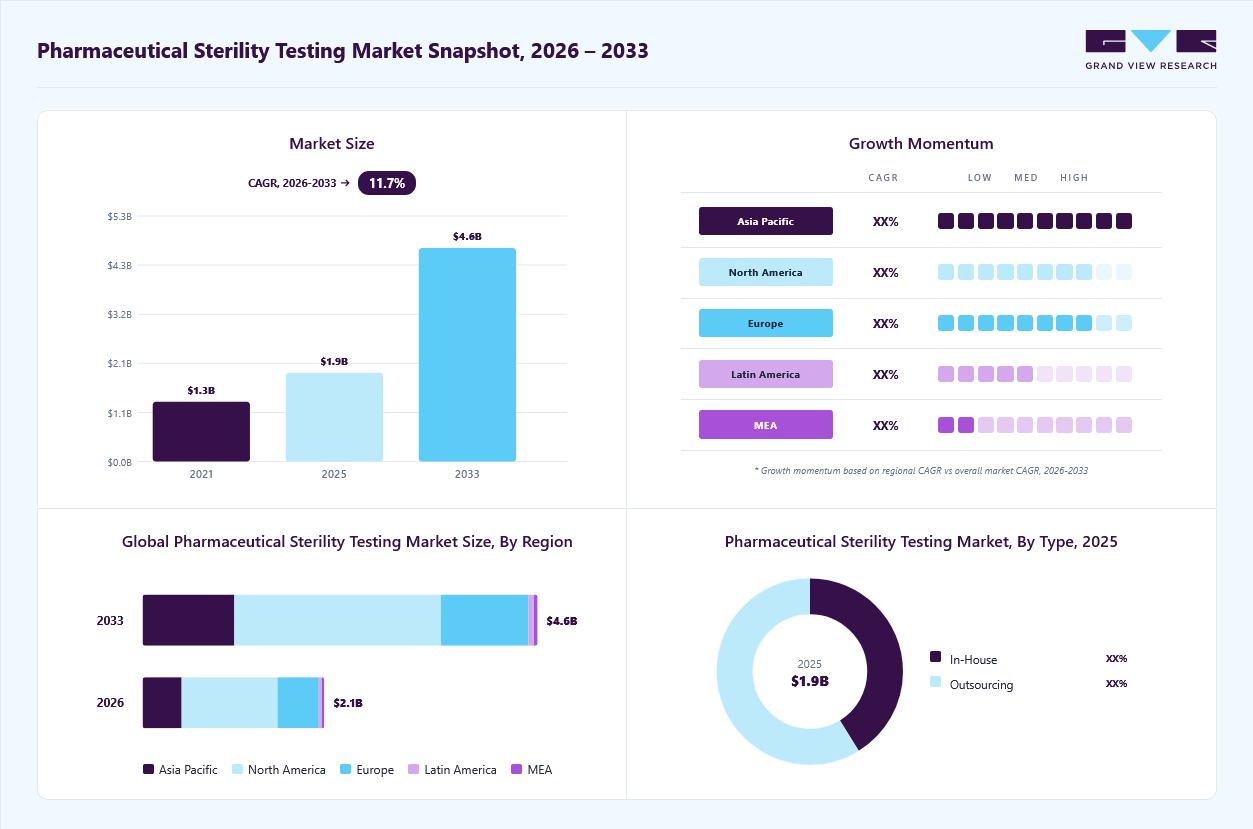

Market Size, 2025

$1.9BMarket Estimate, 2026

$2.1BMarket Forecast, 2033

$4.6BCAGR, 2026–2033

11.7%Pharmaceutical Sterility Testing Market Summary

The global pharmaceutical sterility testing market size was valued at USD 1.9 billion in 2025 and is projected to grow from USD 2.1 billion in 2026 to USD 4.6 billion by 2033, at a CAGR of 11.7% from 2026 to 2033. North America accounted for the largest revenue share of 52.8% in 2025. The development of comprehensive sterility testing procedures is regulated with stringent policies and quality control standards. Governments in developing economies, such as India and China, are increasingly focusing on providing cost-effective, high-quality medications.

Key Market Trends & Insights

- By type: Outsourcing segment accounted for the largest revenue share of 58.8% in 2025.

- By product: Kits and reagents segment dominated in 2025 with 59.8% share.

- By test type: Bioburden testing segment held the largest revenue share of 41.6% in 2025.

- By sample: pharmaceuticals held the largest share of the pharmaceutical sterility testing industry with 38.7% in 2025.

- By end use: Pharmaceutical companies held the largest market share with 42.3% in 2025.

Regional Highlights

- Largest regional market: North America (52.8% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 1.9 Billion/li>

- Estimated market size in 2026: USD 2.1 Billion

- Projected market size by 2033: USD 4.6 Billion

- CAGR (2026-2033): 11.7%

The Government of India allocated over USD 8.4 billion for the period from 2021-2022 to 2025-2026 to strengthen the country's healthcare infrastructure. Furthermore, the Government of India invested over USD 4.4 billion in the National Health Mission (NHM) for FY 2023-24, reflecting a decrease of 1% from the previous year. The objectives of the NHM are to enhance the public healthcare system and improve efficiency in utilizing all available resources. The NHM has also established state-level targets for reducing the incidence of communicable and noncommunicable diseases. Additionally, since 2014, 100.0% Foreign Direct Investment (FDI) has been permitted in the healthcare sector, attracting significant foreign investment to date. Currently, India boasts the highest number of U.S. FDA-approved manufacturing facilities, with 665 plants located outside the U.S. As a result, demand for sterility testing services and products is expected to rise over the forecast period.")

The increasing emphasis on R&D activities in the pharmaceutical industry profoundly affects the pharmaceutical sterility testing market. As pharmaceutical companies actively engage in the discovering and developing innovative and advanced drug formulations, there is a rising demand for robust sterility testing protocols to ensure the safety and efficacy of these products. R&D efforts drive the development of new pharmaceuticals, biologics, and vaccines, requiring comprehensive sterility testing methodologies to comply with regulatory requirements.

An increasing number of drug launches worldwide is expected to positively impact the market. As pharmaceutical companies bring a wider range of new drugs to market, there is a corresponding rise in the demand for rigorous sterility testing protocols. Each drug must undergo comprehensive testing to comply with strict safety and quality standards, whether for treating existing conditions or tackling new medical challenges. Therefore, the rise in novel drug launches has created unprecedented growth opportunities for the market.

Market Dynamics

The pharmaceutical sterility testing market is experiencing strong growth due to expanding pharmaceutical manufacturing, increasing biologics and injectable drug production, and stringent global regulatory requirements governing product safety. Rising outsourcing activity among pharmaceutical and medical device companies, coupled with growing adoption of rapid microbiological methods and automated contamination detection systems, is reshaping the competitive landscape.

The pharmaceutical sterility testing market is being primarily driven by the increasing production of sterile therapeutics, including biologics, vaccines, biosimilars, cell and gene therapies, and injectable formulations. As these products are highly susceptible to microbial contamination, manufacturers are placing greater emphasis on sterility assurance across the product lifecycle—from development and clinical manufacturing to commercial-scale production. Concurrently, regulatory agencies worldwide are strengthening expectations around contamination control, aseptic processing, and product quality, prompting companies to increase investments in sterility testing infrastructure, validation protocols, and quality assurance programs.

In parallel, the industry is witnessing a shift toward rapid microbiological methods (RMMs), automated environmental monitoring systems, isolator technologies, and AI-enabled quality analytics. These innovations help manufacturers reduce testing turnaround times, enhance contamination detection capabilities, and improve compliance with evolving GMP requirements. As pharmaceutical companies increasingly prioritize faster product release timelines while maintaining stringent quality standards, adoption of advanced sterility testing solutions is expected to accelerate, reinforcing long-term market growth.

The pharmaceutical sterility testing market faces ongoing challenges from high compliance costs and stringent regulatory requirements. Maintaining GMP-compliant testing environments requires specialized infrastructure, skilled personnel, validated methods, and continuous quality oversight, increasing operational expenditure for both manufacturers and testing providers.

These challenges are particularly significant for small and mid-sized pharmaceutical and biotech companies, many of which rely on outsourced testing services. While outsourcing improves access to expertise, it can create capacity constraints, longer turnaround times, and dependency on external laboratories. Traditional sterility testing methods also involve lengthy incubation periods that may delay product release and increase inventory costs. As regulators continue to tighten contamination-control standards, ongoing investments in technology upgrades, validation, and workforce training remain essential, creating barriers to scalability and new market entry.

Analyst Perspective

The pharmaceutical sterility testing market is expected to witness sustained double-digit growth through 2033, supported by increasing biologics production, rising injectable drug launches, and expanding regulatory scrutiny across global pharmaceutical supply chains. Adoption of rapid microbiological methods, automated sterility assurance systems, and AI-enabled quality monitoring is likely to accelerate as manufacturers seek faster release cycles and improved compliance outcomes. Outsourced testing providers with strong regulatory expertise, advanced testing platforms, and biologics-focused capabilities are expected to gain share as pharmaceutical companies continue to prioritize operational efficiency and quality assurance. Over the long term, the convergence of advanced therapeutics, stricter contamination-control standards, and growing pharmaceutical manufacturing investments in Asia Pacific and other emerging regions will remain key catalysts for market expansion.

Opportunity Analysis

The growing demand for injectable drugs, biologics, and personalized medicines presents new growth opportunities in the pharmaceutical sterility testing market. Laboratories that expand their capabilities in rapid testing, regulatory documentation support, and environmental monitoring integration can transition from being vendors to strategic partners. There is also significant potential in regional markets like Southeast Asia and Latin America, where infrastructure gaps exist but regulatory compliance is becoming stricter. Furthermore, CROs and CDMOs that invest in technology-driven, full-spectrum sterility assurance can position themselves as premium players meeting global GMP standards.

Technological Advancements

The pharmaceutical sterility testing market is undergoing a significant shift toward automation, rapid methods, and contamination-free systems. Closed-vial sterility testing platforms, isolators, and robotic environmental sampling tools are minimizing human error and enhancing consistency in aseptic validation. Technologies like rapid microbial detection (RMMs), real-time particle monitoring, and AI-supported trend analytics are improving quality assurance while adhering to strict global regulatory expectations. As biologics, cell therapies, and complex injectables grow, these advanced systems are no longer optional but essential for labs aiming to efficiently oversee modern sterile products.

Pricing Analysis

Pricing in sterility testing is evolving beyond traditional per-test fees into more flexible, client-driven frameworks. Labs now offer fixed-fee packages for routine GMP testing, project-based pricing for validation services, and premium value-based pricing for high-risk or expedited batches. Retainer models are emerging in long-term CDMO alliances to guarantee testing capacity for fast-moving sterile drug pipelines. These pricing innovations help contract labs differentiate in a commoditized space and align better with the operational pressures of pharma and biotech sponsors.

Type Insights

Based on type, the pharmaceutical sterility testing industry is categorized into in-house and outsourcing. The outsourcing segment accounted for the largest revenue share of 58.8% in 2025. Outsourcing sterility testing is considered an attractive option for several small- and medium-sized pharmaceutical and medical device companies, which may lack the infrastructure to conduct quality sterility testing. Consequently, most of these companies prefer to outsource sterility testing services to meet the FDA requirements, which is expected to drive the segment’s growth.

The in-house pharmaceutical sterility testing segment is anticipated to grow during the forecast period. The growth is driven by increasing demands for product safety and a rising need for testing services that assess the compatibility and validation of products with routine quality testing and control. Additionally, in-house sterility testing necessitates high levels of control regarding Good Laboratory Practices (GLP), Good Manufacturing Practices (GMP), and employee and environmental practices.

Product Insights

Based on product, the market is divided into kits and reagents, instruments, and services. The kits and reagents segment dominated in 2025 with 59.8% share. In pharmaceuticals and medical devices, a new, fresh kit is required each time for performing sterility testing. This segment is driven by increasing consumption of kits and reagents used in sterility testing, a rising prevalence of diseases, growing R&D investments, the development of advanced and cost-effective technologies, and expanding applications of sterility and molecular testing. Additionally, the rising demand for new therapeutics globally is expected to further bolster market growth.

The service segment is anticipated to grow at the second fastest CAGR over the forecast period. The increasing prevalence of diseases, heightened R&D activities, growing government investments in the healthcare industry, expanding drug pipelines, and an increasing emphasis on quality and sterility are projected to drive the market growth.

Test Type Insights

Based on test type, the market is segregated into sterility testing, bioburden testing, and bacterial endotoxin testing. Sterility testing is further bifurcated into membrane filtration, direct inoculation, and product flush. The bioburden testing segment held the largest revenue share of 41.6% in 2025. The bioburden testing segment is driven by strict quality control processes and the demand for testing that quantifies microbial contamination of a product at various stages of production, from initial manufacturing to final distribution. The pharmaceutical and medical industries for quality control of pharmaceutical and medical products. It is conducted for sterile drugs, biologics, and all medical devices, including classes I, II, and III. This ensures that pharmaceuticals and medical devices comply with the stringent health and safety regulations established by Title 21 of the Code of Federal Regulations in the USA and by ISO 11737.

Additionally, the sterility testing segment of the pharmaceutical sterility testing industry is anticipated to witness the fastest CAGR during the forecast period. Sterility testing is commonly employed to verify the sterility of products in the pharmaceutical, biopharmaceutical, and medical device industries. The segment's growth can be attributed to the industry's need for sterility testing during the sterilization validation process, as well as for routine release testing.

Sample Insights

Based on sample, the market is segmented into pharmaceuticals, medical devices, and biopharmaceuticals. Pharmaceuticals held the largest share of the pharmaceutical sterility testing industry with 38.7% in 2025. The pharmaceutical industry is subject to strict regulatory requirements, and sterility testing is crucial to ensure compliance with standards such as Good Manufacturing Practices (GMP). Outsourcing sterility testing to specialized laboratories enables pharmaceutical companies to meet these stringent regulatory requirements without heavily investing in specialized facilities and personnel. Pharmaceuticals include various dosage forms, such as parenteral solutions, aerosols, ointments, eye drops, and other formulations.

The biopharmaceuticals segment is expected to grow at the fastest CAGR over the forecast period. The biopharmaceutical sector, including biologics and biosimilars, has been expanding. These products often require specialized testing services, including sterility testing. There is a growing demand for biologics and biosimilar drugs in the U.S. as they are highly effective in treating serious diseases like cancer, autoimmune diseases, neurological disorders, and others. The COVID-19 pandemic increased the demand for vaccines in the country, and due to this, in July 2022, the U.S. government secured 3.2 million doses of the Novavax COVID-19 Vaccine. Such initiatives drive the demand for biopharmaceutical sterility testing.

End-use Insights

Based on end use, the market is divided into compounding pharmacies, medical device companies, pharmaceutical companies, and others. The pharmaceutical companies held the largest market share with 42.3% in 2025. By outsourcing noncore activities like sterility testing, medical device companies can concentrate on their core competencies, such as research, development, and manufacturing. This focus can lead to increased efficiency and innovation. Furthermore, sterility testing for medical devices can be complex, requiring specialized expertise and facilities. Outsourcing to specialized testing laboratories with experienced personnel and advanced technologies ensures accurate and reliable results. It can also help mitigate risks associated with contamination and ensure that testing is conducted by experts focusing on quality assurance.

The compounding pharmacies are expected to grow at the fastest CAGR over the forecast period. These pharmacies prepare customized dosages of sterile drugs, which must meet the stringent requirements and standards of sterility. Sterility testing helps compounding pharmacies maintain control and consistency while reducing risks associated with manufacturing in an aseptic environment.

Regional Insights

North America accounted for the largest revenue share of 52.8% in the pharmaceutical sterility testing market in 2025. This is attributed to the increasing number of pharmaceutical industries and the presence of a number of major market players within the U.S. and Canada. The market expansion can be ascribed to the existence of technologically advanced CROs & CDMOs and an upsurge in the allocation of grants. The increasing prevalence of diverse diseases has led to additional investments in clinical research throughout the projected period. Furthermore, heightened drug development endeavors, strategic measures like innovation & acquisitions, the presence of pharmaceutical and biotech firms, and a surge in the number of clinical trials in the region are key factors propelling market growth.

U.S. Pharmaceutical Sterility Testing Market Trends

The pharmaceutical sterility testing industry in the U.S. held the largest revenue share in 2025. An increase in R&D activities and a rise in the number of drug approvals in the country are among the major factors supporting market growth.

Europe Pharmaceutical Sterility Testing Market Trends

The pharmaceutical sterility testing industry in Europe is expected to grow significantly due to growing regulations. These regulatory bodies regularly conduct inspections to ensure compliance with the manufacturing units and contract manufacturing units with quality standards, which are expected to contribute to the increasing demand for pharmaceutical sterility testing in this region.

The pharmaceutical sterility testing market in Germany held the largest share in 2024, due to the increased demand for improved product designs and related services. Technological advancements and high-quality clinical resources are among the key factors driving market growth during the forecast period.

The UK pharmaceutical sterility testing market is anticipated to grow over the forecast period. The UK is of prime importance for pharmaceutical companies, which is expected to contribute to extensive R&D initiatives and clinical trials being undertaken to address the challenges posed by various diseases.

Asia Pacific Pharmaceutical Sterility Testing Market Trends

The Asia Pacific pharmaceutical sterility testing industry is expected to grow the fastest over the forecast period, driven by numerous developed countries investing in Asia Pacific nations and various amendments made by regulatory agencies to facilitate local manufacturing and contract services. The increasing healthcare demand due to a rising population is also anticipated to accelerate the drug approval process, indirectly supporting the market growth. Furthermore, the harmonization of regulatory standards in these regions with the International Council for Harmonization of Technical Requirements for Pharmaceuticals for Human Use (ICH) standards is expected to fuel market growth.

The pharmaceutical sterility testing market in China held the largest share in 2024. Additionally, the country has become an appealing destination for outsourcing clinical trials due to its large population, diverse patient demographics, and cost-effectiveness. Consequently, domestic and international pharmaceutical companies outsource their clinical trials to Contract Research Organizations (CROs) in China, which is driving the demand for sterility testing services.

The Japan pharmaceutical sterility testing market is expected to grow over the forecast period due to the commencement of development and manufacturing services for messenger ribonucleic acid pharmaceuticals, biopharmaceuticals produced through gene & cell therapies, and mammalian cell cultures.

The pharmaceutical sterility testing market in India is anticipated to grow at a significant CAGR over the forecast period. This growth can be attributed to low costs, the availability of industry experts, and the presence of WHO-cGMP-compliant facilities. Additionally, increasing government funding for R&D aimed at accelerating new product development is likely to enhance the number of new drugs, thereby promoting the demand for pharmaceutical sterility testing in India.

Key Pharmaceutical Sterility Testing Company Insights

Several key players are pursuing various strategic initiatives to enhance their market position, providing diverse services to customers. The main strategies adopted by companies include service launches, mergers & acquisitions, joint ventures, partnerships, and agreements, along with expansions, to increase market presence and revenue while gaining a competitive edge that drives the market growth.

Key Pharmaceutical Sterility Testing Companies:

The following are the leading companies in the pharmaceutical sterility testings market. These companies collectively hold the largest market share and dictate industry trends.

-

Pacific Biolabs

-

Steris Plc

-

Boston Analytical

-

Sotera Health Company (Nelson Labs)

-

Sartorius Ag

-

Solvias Ag

-

SGS SA

-

Labcorp

-

Pace Analytical

-

Charles River Laboratories

-

Thermo Fisher Scientific, Inc.

-

Rapid Micro Biosystems, Inc.

-

Almac Group

-

Labor LS SE & Co. KG

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Steris plc, Sartorius AG, Labcorp, SGS SA)

• Expand global laboratory networks and GMP-compliant testing capabilities.

• Offer integrated microbiology, sterility, endotoxin, and validation services through long-term contracts.- Strong regulatory track record and established relationships with pharmaceutical and medical device manufacturers.

- Broad service portfolios supported by advanced automation and global quality systems.

- Higher operating costs and slower implementation of niche technologies due to organizational scale.

- Greater exposure to pricing pressure in mature markets.

Emerging Players (Rapid Micro Biosystem, Boston Analytical, Pacific BioLabs, Solvias AG)

• Focus on rapid microbiological methods, specialized sterility testing, and customized service offerings.

• Build growth through partnerships with biotech firms, CDMOs, and emerging therapy developers.• Faster adoption of innovative testing technologies and flexible customer engagement models.

• Strong expertise in high-growth segments such as biologics, cell & gene therapies, and advanced therapeutics.• Limited geographic presence and lower brand recognition versus global incumbents.

• Capacity constraints may restrict participation in large multinational contracts.Recent Developments

-

In January 2024, Rapid Micro Biosystems, Inc. announced the launch of the Growth Direct Rapid Sterility application by mid-2024.

-

In August 2023, Pace Analytical Services improved its capabilities by adding advanced hydrocarbon analytical support and expanding sediment & tissue testing with the acquisition of Alpha Analytical.

-

In May 2023, Thermo Fisher Scientific, Inc. announced the launch of a sterile drug facility in Singapore. It would help deliver new vaccines and medicines in the Asia Pacific market.

Pharmaceutical Sterility Testing Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 1.9 billion

Estimated market size in 2026

USD 2.1 billion

Projected market size by 2033

USD 4.6 billion

Growth rate

CAGR of 11.7% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, product, test type, sample, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; Russia; Iceland; Finland; China; Japan; India; South Korea; Australia; Thailand; Singapore; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait; Israel

Key companies profiled

Pacific Biolabs; Steris Plc; Boston Analytical; Nelson Laboratories, LLC (Sotera Health); Sartorius AG; SOLVIAS AG; SGS SA; Labcorp; Pace Analytical; Charles River Laboratories; Thermo Fisher Scientific, Inc.; Rapid Micro Biosystems; Almac Group;Labor LS SE & Co. KG

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Pharmaceutical Sterility Testing Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global pharmaceutical sterility testing market report based on type, product, test type, sample, end-use, and region:

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

In-House

-

Outsourcing

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Kits and Reagents

-

Instruments

-

Services

-

-

Test Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Sterility Testing

-

Membrane Filtration

-

Direct Inoculation

-

Product Flush

-

-

Bioburden Testing

-

Bacterial Endotoxin Testing

-

-

Sample Outlook (Revenue, USD Million, 2021 - 2033)

-

Pharmaceuticals

-

Medical Devices

-

Biopharmaceuticals

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Compounding Pharmacies

-

Medical Device Companies

-

Pharmaceutical Companies

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Norway

-

Sweden

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

Segment Definition

Segment - Type

Definition

In-House

Revenue generated from sterility testing conducted within pharmaceutical, biotechnology, or medical device companies using internal laboratories and quality control infrastructure.

Outsourcing

Revenue generated from third-party CROs, CDMOs, and specialized microbiology laboratories providing sterility testing services on a contract basis

Phase IV

Revenue generated from post-marketing and long-term follow-up studies assessing real-world effectiveness, durability, and long-term safety of approved therapies. Includes patient registries, observational studies, and post-approval surveillance programs.

Segment - Indication

Definition

Oncology

Revenue from CGT clinical trials targeting hematologic malignancies and solid tumors, including CAR-T, TCR-T, tumor-infiltrating lymphocyte (TIL), and gene-edited cancer therapies.

Cardiology

Revenue from trials evaluating gene therapies, regenerative cell therapies, and stem cell-based interventions for heart failure, myocardial infarction, cardiomyopathies, and other cardiovascular disorders.

CNS (Central Nervous System)

Revenue from trials focused on neurological and neurodegenerative disorders such as Parkinson’s disease, Alzheimer’s disease, ALS, spinal muscular atrophy, and other CNS conditions.

Musculoskeletal

Revenue from clinical studies investigating regenerative therapies, stem-cell therapies, and gene therapies for orthopedic, bone, cartilage, muscle, and connective tissue disorders.

Infectious Diseases

Revenue generated from CGT trials aimed at treating viral, bacterial, and chronic infectious diseases through gene-modified immune therapies, vaccines, and novel cell-based approaches.

Dermatology

Revenue from trials targeting inherited and acquired skin disorders using gene replacement, gene editing, and regenerative cell therapies.

Endocrine, Metabolic & Genetic Disorders

Revenue from studies addressing inherited metabolic disorders, endocrine diseases, and monogenic genetic conditions through gene replacement, gene editing, and cell-based therapeutic approaches.

Immunology & Inflammation

Revenue generated from CGT trials focused on autoimmune diseases, inflammatory disorders, and immune-mediated conditions utilizing engineered immune cells and gene-modified therapies.

Ophthalmology

Revenue from trials investigating gene and cell therapies for inherited retinal diseases, retinal degeneration, vision loss, and other ocular disorders.

Hematology

Revenue from studies targeting blood disorders such as sickle cell disease, beta-thalassemia, hemophilia, and other hematological conditions through genetic modification and cell-based interventions.

Gastroenterology

Revenue generated from trials focused on gastrointestinal diseases, liver disorders, inflammatory bowel disease, and related conditions using advanced gene and cell therapies.

Others

Revenue from CGT trials conducted across less-established therapeutic areas not separately classified, including respiratory, renal, reproductive, and rare disease indications.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Pharmaceutical Sterility Testing Market Trends & Opportunity Assessment

Detailed assessment of testing demand by product type, test type, sample category, outsourcing trends, biologics manufacturing growth, rapid microbial technologies, regulatory developments, and regional opportunities.

Identifies high-growth testing segments, outsourcing opportunities, emerging technologies, investment hotspots, and unmet quality assurance needs.

Competitive Landscape & Market Share Assessment

Benchmarking of established and emerging testing providers based on service capabilities, geographic footprint, technology adoption, regulatory expertise, partnerships, and market positioning.

Highlights competitive intensity, white-space opportunities, differentiation strategies, partnership potential, and expansion pathways.

Technology, Innovation & Regulatory Landscape Review

Evaluation of rapid microbial methods (RMMs), automated sterility platforms, endotoxin detection technologies, environmental monitoring systems, AI-enabled quality analytics, FDA/EMA guidance, and GMP compliance trends.

Supports technology prioritization, regulatory preparedness, operational excellence initiatives, and long-term strategic planning.

Frequently Asked Questions About This Report

The global pharmaceutical sterility testing market size was estimated at USD 1.9 billion in 2025 and is expected to reach USD 2.1 billion in 2026.

The global pharmaceutical testing sterility market is expected to grow at a compound annual growth rate of 11.7% from 2026 to 2033 to reach USD 4.6 billion by 2033.

Key factors that are driving the market growth include increasing government investments in the healthcare industry, increasing R&D activities, increasing the number of drug launches, and increasing focus on quality and sterility.

Some key players operating in the pharmaceutical testing sterility market include Pacific Biolabs, Steris Plc, Boston Analytical, Nelson Laboratories, LLC (Sotera Health), Sartorius AG, SOLVIAS AG, SGS SA, Labcorp, Pace Analytical, and others.

Asia Pacific is the fastest-growing region over the forecast period.

Kits & reagents dominated the pharmaceutical sterility testing with 59.8% share in 2025.

Bioburden testing dominated the pharmaceutical sterility testing with 41.6% share in 2025.

Pharmaceutical companies dominated the pharmaceutical sterility testing with 42.3% share in 2025.

North America dominated the pharmaceutical sterility testing market with a share of 52.8% in 2025. This is attributed to the increasing number of pharmaceutical industries within the U.S. & Canada, and the increasing presence of the number of major market players this region is expected to contribute significantly to the market growth.

About the Author(s)

Clinical Diagnostics Research Team

Healthcare · Clinical DiagnosticsThis report was authored by the clinical diagnostics research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clinical diagnostics segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.