- Home

- »

- Advanced Interior Materials

- »

-

Precious Metal Market Size And Share Report, 2026-2033GVR Report cover

![Precious Metal Market (2026 - 2033)Report]()

Precious Metal Market (2026 - 2033)

Size, Share & Trends Analysis Report By Metal (Gold, PGM, Silver), By Application (Jewelry, Industrial, Investment), By Region (North America, Europe, Asia Pacific, Central & South Africa, Middle East & Africa), And Segment Forecasts

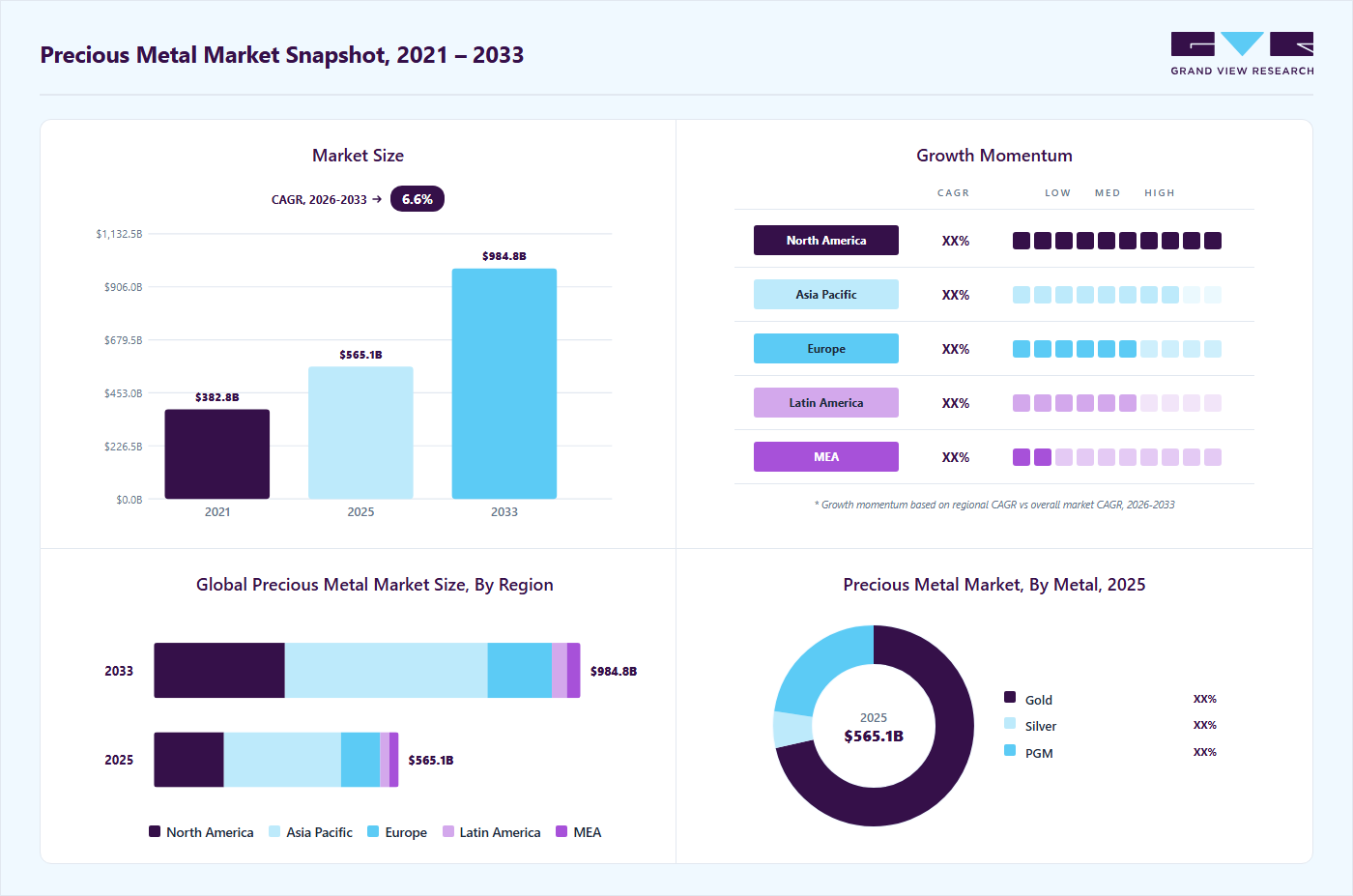

Market Size, 2025

$565.1BMarket Estimate, 2026

$630.0BMarket Forecast, 2033

$984.8BCAGR, 2026–2033

6.6%Precious Metal Market Summary

The global precious metal market size was valued at USD 565.1 billion in 2025 and is projected to grow from USD 630.0 billion in 2026 to USD 984.8 billion by 2033, at a CAGR of 6.6% from 2026 to 2033. The Asia Pacific held the largest share of 47.0% of the global market in 2025. This growth is primarily driven by rising investor demand for safe-haven assets amid economic and geopolitical uncertainties, as well as the increasing use of industrial applications in electronics, automotive catalytic converters, and renewable energy technologies.

Key Market Trends & Insights

- By metal: Gold held the largest market share of over 71.0% in 2025.

- By application: The industrial segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (47.0% revenue share, 2025)

- Fastest-growing regional market: North America (highest CAGR, 2026-2033)

- By country: The U.S. held the dominant position in the global market in 2025.

Market Size & Forecast

- Market size in 2025: USD 565.1 Billion

- Estimated market size in 2026: USD 630.0 Billion

- Projected market size by 2033: USD 984.8 Billion

- CAGR (2026-2033): 6.6%

The precious metals market has increasingly aligned with sustainable practices, driven by environmental, social, and governance (ESG) considerations. Leading companies are focusing on reducing carbon emissions in mining and refining operations, implementing water and energy-efficient processes, and ensuring responsible sourcing of metals through certified supply chains. Recycling and urban mining of precious metals from electronic waste and industrial scrap have become significant contributors to supply, reducing dependence on primary mining while supporting circular economic principles. These initiatives not only mitigate environmental impact but also enhance corporate reputation and compliance with global regulatory standards.")

Technological innovation is transforming the precious metals market, enhancing the efficiency of extraction, processing, and application. Advanced metallurgical techniques, automation, and digital mine management systems are improving yield, reducing operational costs, and optimizing resource utilization. In addition, the integration of precious metals in high-tech applications such as automotive catalytic converters, hydrogen fuel cells, electronics, and renewable energy systems is driving demand for high-purity materials. Cutting-edge refining, micronization, and nanotechnology processes are enabling companies to produce metals with precise particle size, composition, and performance characteristics, supporting both industrial growth and emerging technology sectors.

Market Dynamics

Growing investment interest and steady jewelry consumption are supporting expansion in the global precious metals market. Gold demand continues to rise as investors increasingly prefer defensive assets amid economic uncertainty, inflation concerns, and geopolitical instability. During 2026, international gold prices surpassed USD 5,000 per troy ounce in January, while prices in India exceeded INR 1,60,000 per 10 grams in May, highlighting strong buying activity from investors, financial institutions, and central banks. Despite historically high prices, demand for gold jewelry remains resilient across major markets such as India, China, and the Middle East, where gold maintains strong cultural and long-term wealth preservation value. Continued central bank accumulation and wedding-related purchases are expected to support market growth over the forecast period.

The global precious metals market continues to face challenges associated with supply instability and changing industrial demand patterns for metals such as palladium, platinum, and silver. Supply availability for platinum group metals (PGMs) remains highly dependent on mining activities in regions such as Russia and South Africa, making the market vulnerable to geopolitical tensions, regulatory developments, and operational disruptions. In addition, fluctuations in automotive production and the evolution of emission-control technologies continue to influence palladium and platinum consumption in catalytic converter applications. The ongoing transition toward electric vehicles is also expected to gradually affect long-term demand for certain PGMs, as battery electric vehicles require lower autocatalyst levels.

Metal Insights

The gold segment dominated the market with a revenue share of over 71.0% in 2025, due to its long-standing role as a store of value, a safe-haven asset, and a key component of jewelry demand. The strong cultural significance in major consuming regions, such as India and China, along with sustained central bank purchases, continues to support gold’s dominance. In addition, heightened geopolitical tensions and macroeconomic uncertainty have reinforced investor preference for gold-backed assets, ensuring stable demand across investment and reserve management applications.

Silver is expected to register the fastest CAGR over the forecast period, driven by its expanding industrial applications alongside investment demand. The metal’s extensive use in solar photovoltaics, electronics, electric vehicles, and advanced electrical components is accelerating consumption, particularly amid global energy transition initiatives. Compared to gold, silver’s lower price point also attracts retail investors, further supporting volume growth and contributing to its faster rate of expansion.

Application Insights

The industrial segment accounts for the largest share of the precious metals market and is expected to grow at the fastest CAGR of 7.1% over the forecast period. This dominance is attributed to the widespread use of precious metals in electronics, automotive catalytic converters, chemical processing, medical devices, and renewable energy technologies. Platinum group metals play a critical role in emission control systems, while silver’s conductivity properties make it indispensable in electrical and electronic applications.

The industrial segment’s strong growth outlook is further supported by rising adoption of electric vehicles, expansion of renewable energy infrastructure, and increasing demand for high-performance materials in advanced manufacturing. Technological advancements, coupled with stricter emission regulations and sustainability-driven innovation, are expected to sustain long-term demand for industrial precious metals, reinforcing both market share and growth momentum.

Jewelry and investment applications continue to support market growth, though they hold a smaller share compared to industrial usage. Jewelry demand is concentrated in countries with strong cultural and traditional preferences for gold, whereas investment demand is driven by economic uncertainty, hedging inflation, and central bank accumulation. Coins, bars, and ETFs remain popular investment vehicles for retail and institutional investors. Despite slower growth than industrial applications, these segments provide stability and liquidity to the overall precious metals market.

Regional Insights

The North America precious metal market is expected to grow at the fastest CAGR of 7.4% over the forecast period, driven by strong investment demand and a mature industrial base. The region benefits from high consumption of gold and silver in jewelry, electronics, and automotive applications, particularly in the U.S. and Canada. The adoption of technological innovations, such as electric vehicles and renewable energy infrastructure, is further supporting industrial demand for PGMs and silver. Favorable regulatory frameworks, advanced mining infrastructure, and investor confidence in safe-haven assets contribute to steady market growth in this region.

U.S. Precious Metal Market Trends

The U.S. represents the largest single-country market in North America, fueled by both investment and industrial applications. Gold remains the preferred choice for investors during periods of economic uncertainty, while silver and PGMs see extensive use in electronics, automotive catalytic converters, and healthcare devices. Rising adoption of green technologies and government incentives for renewable energy projects are increasing industrial demand for silver and platinum, driving growth in the U.S. precious metals market.

Asia Pacific Precious Metal Market Trends

Asia Pacific dominated the precious metal market with a revenue share of over 47.0% in 2025, driven by rapid industrialization, increasing disposable income, and cultural affinity for gold jewelry. Countries such as China and India dominate jewelry consumption, while industrial demand for silver, gold, and PGMs is rising due to electronics manufacturing, renewable energy projects, and automotive applications.

Growing investments in EVs, solar panels, and digital technologies, combined with supportive government policies, are fueling regional market expansion, making the Asia Pacific a key growth hub.

Europe Precious Metal Market Trends

Europe holds a substantial share of the global precious metals market, primarily driven by industrial applications in the automotive, electronics, and chemical processing sectors. Platinum group metals are particularly important in Europe due to strict emission norms, while gold continues to attract investment demand through coins, ETFs, and jewelry. The presence of major mining and refining companies, coupled with strong technological adoption and ESG-focused initiatives, is strengthening both the industrial and investment segments in the region.

Key Precious Metal Company Insights

Some of the key players operating in the market include Newmont Corporation, Barrick Gold Corporation, and Anglo-American Platinum Limited, among others.

-

Newmont Corporation, founded in 1921 and headquartered in the U.S., is the world’s largest gold mining company with a diversified portfolio of gold and silver assets across North America, South America, Australia, and Africa. The company focuses on large-scale, long-life mining operations supported by advanced extraction technologies and strong ESG frameworks. Newmont emphasizes operational efficiency, responsible mining practices, and disciplined capital allocation to sustain long-term production of precious metals.

-

Barrick Gold Corporation, established in 1983 and based in Canada, is a leading global gold producer with additional exposure to copper through integrated mining operations. The company operates Tier-1 assets across the Americas, Africa, and the Middle East, enabling stable output and cost optimization. Barrick prioritizes digital mine management, reserve expansion, and sustainability-driven operations to strengthen its competitive position in the precious metals market.

-

Anglo American Platinum Limited, incorporated in 1946 and headquartered in South Africa, is the world’s largest primary producer of platinum group metals. The company operates vertically integrated mining and processing facilities, producing platinum, palladium, rhodium, and associated metals for automotive, industrial, and jewelry applications. Anglo American Platinum focuses on operational resilience, supply reliability, and low-carbon initiatives to support long-term demand growth for PGMs.

Key Precious Metal Companies:

The following are the leading companies in the precious metal market. These companies collectively hold the largest Market share and dictate industry trends.

- Anglo American Platinum Limited

- Barrick Gold Corporation

- First Quantum Minerals Ltd.

- Fresnillo plc

- Glencore plc

- Impala Platinum Holdings Limited

- Newmont Corporation

- MMC Norilsk Nickel

- Pan American Silver Corp.

- Sibanye-Stillwater Limited

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Anglo American Platinum Limited, Barrick Gold Corporation, Glencore plc, Newmont Corporation, Impala Platinum Holdings Limited, MMC Norilsk Nickel

- Strengthen long-term supply agreements with jewelry, automotive, electronics, and industrial sectors while expanding ESG-focused mining initiatives.

- Invest heavily in automation, advanced extraction technologies, sustainable mining practices, and resource expansion projects to improve operational efficiency and reserve life.

- Extensive mining assets, strong refining infrastructure, and diversified geographic presence support large-scale production capabilities.

- Strong financial stability, established global supply chains, and long-standing customer relationships provide a significant competitive advantage.

- Operational challenges related to declining ore grades, labor shortages, and concentration of mining activities in select regions.

- Exposure to geopolitical risks, mining regulations, environmental compliance costs, and energy price volatility.

Emerging Players: Sibanye-Stillwater Limited, Fortuna Mining Corp., The Metals Company, Aya Gold & Silver Inc., G Mining Ventures Corp.

- Pursue strategic acquisitions and project developments to strengthen production capacities and reserve portfolios.

- Increasing focus on responsible sourcing and sustainability initiatives enhances attractiveness among ESG-focused investors.

- Limited financial flexibility for large-scale mine expansion and long-term infrastructure investments.

Recent Developments

-

In October 2025, Newmont Corporation announced third-quarter 2025 results reporting approximately 1.4 million attributable gold ounces produced and a record free cash flow of about USD 1.6 billion, along with improved cost and capital guidance for the full year. The company also continued to optimize its portfolio through divestitures, strengthening its balance sheet while advancing key Tier 1 asset operations and cost-saving initiatives to support long-term production growth.

-

In June 2025, Anglo American Platinum Limited’s business was demerged from Anglo American plc to form Valterra Platinum Limited, with approximately 51 percent of the PGM business separated and listed independently. This strategic demerger unlocked shareholder value and established Valterra as a standalone entity focused on platinum group metals production in the global market.

-

In May 2025, Barrick Mining Corporation (formerly Barrick Gold Corporation) completed a corporate rebranding reflecting its evolution into a diversified gold and copper producer and announced it is evaluating an initial public offering (IPO) of its North American gold assets to highlight their value. The contemplated IPO would include interests in Nevada Gold Mines and the Fourmile gold discovery, with Barrick retaining a controlling majority stake while unlocking shareholder value in the strong precious metals market.

Precious Metal Market Report Scope

Report Attribute

Details

Market definition

Apparent consumption of precious metals such as gold, silver, and PGMs refers to the total volume utilized across various sectors, including jewelry, investment products (bars and coins), and industrial applications such as electronics, automotive catalysts, and renewable energy technologies.

Market size in 2025

USD 565.1 billion

Estimated market size in 2026

USD 630.0 billion

Projected market size by 2033

USD 984.8 billion

Growth rate

CAGR of 6.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Volume forecast, revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Metal, application, region

Regional scope

North America; Europe; Asia Pacific; Central & South Africa; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Russia; Switzerland; China; India; Japan; South Korea; Vietnam; Brazil; Argentina; Saudi Arbia; UAE; Qatar

Key companies profiled

Anglo American Platinum Limited; Barrick Gold Corporation; First Quantum Minerals Ltd.; Fresnillo plc; Glencore plc; Impala Platinum Holdings Limited (Implats); Newmont Corporation; MMC Norilsk Nickel; Pan American Silver Corp.; Sibanye-Stillwater Limited

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Precious Metal Market Report Segmentation

This report forecasts global, country, and regional revenue growth and analyzes the latest trends in each sub-segment from 2021 to 2033. For this study, Grand View Research has segmented the global precious metal market report by Metal, application, and region.

-

Metal Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Gold

-

Silver

-

PGM

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Jewelry

-

Industrial

-

Investment

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Russia

-

Switzerland

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

Qatar

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Precious Metals E-Waste Recovery Market

Dedicated assessment of the precious metals e-waste recovery market with segmentation by metal type, along with source-wise analysis across household appliances, IT & telecommunication, consumer electronics, and other e-waste categories. The study included market sizing, movement analysis, and market share evaluation for key recovery segments.

Enabled understanding of precious metal recovery opportunities from electronic waste streams, source-wise recycling potential, and emerging trends in sustainable precious metals recovery and circular economy initiatives.

Indonesia Precious Metals Market Assessment

Country-specific assessment of the Indonesia precious metals market with segmentation by product type and application. The study included market sizing, demand analysis, application outlook, and evaluation of key industry trends influencing precious metal consumption across the Indonesian market.

Supported understanding of Indonesia’s product-wise demand structure, application trends, and growth opportunities within the regional precious metals industry.

Jamaica Precious Metals Market Assessment

Market estimates and a detailed assessment of the Jamaica precious metals market, including analyses of key players, market dynamics, the regulatory framework, entry barriers for new participants, and the competitive environment.

Enabled evaluation of market attractiveness, competitive intensity, regulatory challenges, and potential expansion opportunities within the Jamaica precious metals industry.

Frequently Asked Questions About This Report

The global precious metal market size was valued at USD 565.1 billion in 2025 and is estimated at USD 630.0 billion for 2026.

The global precious metal market is expected to grow at a CAGR of 6.6% from 2026 to 2033, reaching USD 984.8 billion by 2033.

North America is expected to be the fastest-growing regional market during the forecast period.

Some of the key players operating in the precious metal market include Anglo American Platinum Limited, Barrick Gold Corporation, First Quantum Minerals Ltd., Fresnillo plc, Glencore plc, Impala Platinum Holdings Limited, Newmont Corporation, MMC Norilsk Nickel, Pan American Silver Corp., and Sibanye-Stillwater Limited.

Key factors driving the precious metal market include rising investor demand for safe-haven assets amid economic and geopolitical uncertainties, as well as the increasing use of industrial applications in electronics, automotive catalytic converters, and renewable energy technologies.

The gold segment dominated the market with a revenue share of over 71.0% in 2025, while silver is expected to register the fastest CAGR over the forecast period.

The industrial segment accounted for the largest share of the market in 2025 and is expected to grow at the fastest CAGR during the forecast period.

Asia Pacific dominated the market with a revenue share of over 47.0% in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.