- Home

- »

- Next Generation Technologies

- »

-

Signals Intelligence Market Size & Share Report, 2026-2033GVR Report cover

![Signals Intelligence Market Size, Share & Trends Report]()

Signals Intelligence Market (2026 - 2033) Size, Share & Trends Analysis Report By Solutions (Airborne, Ground, Naval, Space, Cyber), By Type (ELINT, COMINT), By Mobility (Fixed, Portable), By Region, And Segment Forecasts

Market Size, 2025

$18.5BMarket Estimate, 2026

$19.6BMarket Forecast, 2033

$28.5BCAGR, 2026–2033

5.5%Signals Intelligence Market Summary

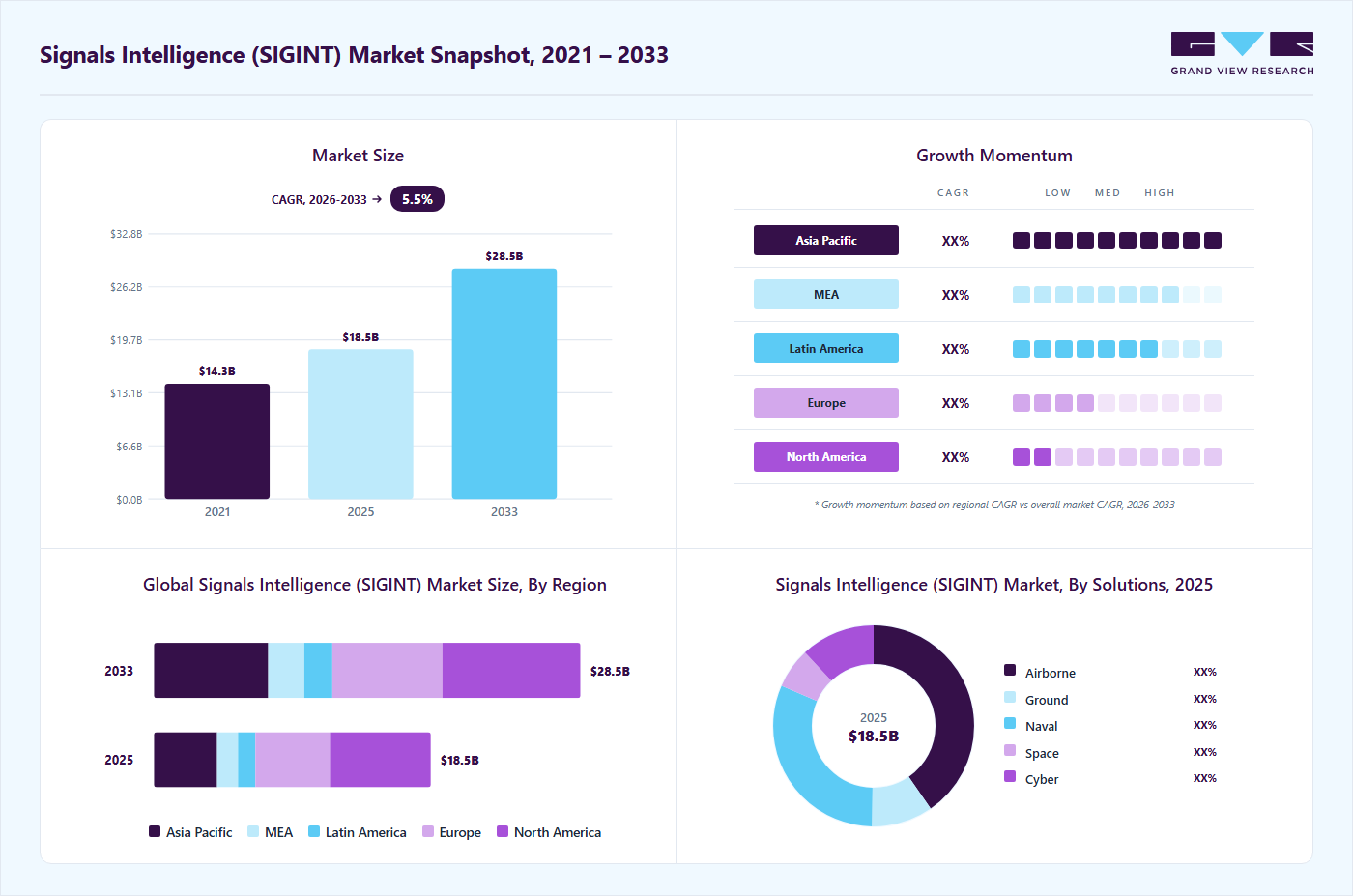

The global signals intelligence market size was valued at USD 18.5 billion in 2025 and is projected to grow from USD 19.6 billion in 2026 to USD 28.5 billion by 2033, at a CAGR of 5.5% from 2026 to 2033. North America held a significant revenue share of 36% of the global market in 2025. The market for signals intelligence is driven by rising geopolitical tensions, increasing global defense spending, accelerating adoption of advanced electronic warfare capabilities, growing integration of AI and big data enabling real-time signal processing, expanding deployment of space-based and airborne signals intelligence (SIGINT) platforms, increasing demand for border security and counterterrorism intelligence solutions, and continuous modernization of intelligence infrastructure for real-time multi-domain operations.

Key Market Trends & Insights

- By solutions: Airborne segment held the largest market share of over 40% in 2025.

- By type: Electronic Intelligence (ELINT) segment held the largest market share of 71% in 2025.

- By mobility: Fixed segment held a significant market share in 2025.

Regional Highlights

- Largest regional market: North America (over 36% market share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR of over 7.0% from 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 18.5 Billion

- Estimated market size in 2026: USD 19.6 Billion

- Projected market size by 2033: USD 28.5 Billion

- CAGR (2026-2033): 5.5%

The global signals intelligence industry is being driven by the rapid integration of artificial intelligence and machine learning, enabling advanced capabilities such as automated classification and faster threat detection. The increasing adoption of software-defined and modular SIGINT architectures is enhancing operational flexibility and enabling rapid platform upgrades for multi-mission requirements. The growing importance of multi domain intelligence fusion is strengthening comprehensive situational awareness across land, air, sea, space, and cyber domains. In addition, the proliferation of portable and network-centric SIGINT platforms is expanding tactical reach and accelerating real-time data dissemination to command centers. Rising defense budgets and escalating geopolitical tensions are further fueling sustained investments in advanced SIGINT capabilities, reinforcing military preparedness against evolving electronic threats.

The SIGINT solutions industry is being driven by the increasing demand for end-to-end mission support as governments and commercial operators expand their satellite fleets. This shift is accelerating the adoption of integrated ground infrastructures that combine control, communications, navigation, and data processing to enhance mission resilience and reduce operational silos. The growing deployment of satellite based intelligence systems is further enabling real-time data acquisition, seamless processing, and faster dissemination across mission-critical environments. For instance, in June 2025, Indra Group launched enhanced ground-segment capabilities through its newly established Indra Space business unit, offering comprehensive solutions across satellite command and control, data downlinking, mission operations, control centers, earth stations, and integrated communication and navigation systems. This initiative strengthens Indra’s position as a full-value space solutions provider by reducing reliance on external partners and enhancing competitiveness across defense, civil, and commercial space applications.

")

The signals intelligence industry is increasingly influenced by growing requests for real-time data processing and AI-enabled space-domain awareness in response to a more contested and congested operational environment. Stakeholders are showing heightened interest in developing integrated ground, space, and on-orbit signal processing capabilities that leverage AI to detect, classify, and track objects, enabling anticipatory decision-making and effective threat response. For instance, in June 2024, Voyager Space announced a partnership with Palantir Technologies to integrate Palantir’s advanced AI tools across Voyager’s space and defense operations. The collaboration applies Palantir’s AI platform to payload management systems for the International Space Station and the Starlab commercial space station, with the objective of reducing data processing burdens and mission operations complexity. This partnership establishes a new benchmark for AI-powered signal intelligence in space, allowing Voyager to deliver more advanced, responsive, and comprehensive capabilities to both defense and commercial customers.

Solutions Insights

The airborne segment accounted for the largest revenue share of over 40% in 2025 and is expected to continue to dominate the industry over the forecast period. This growth is driven by rising demand from defense and intelligence agencies for faster AI-enabled intelligence collection to counter evolving electronic threats. There is also increasing preference for modular, compact SIGINT systems that can be rapidly integrated into unmanned platforms, accelerating industry partnerships and platform upgrades. For instance, in December 2025, TEKEVER partnered with Avantix to integrate advanced tactical SIGINT and electronic warfare payloads with AI-powered unmanned aerial systems, strengthening next-generation airborne ISR capabilities for defense and homeland security missions.

The cyber segment is expected to experience a significant CAGR over the forecast period, driven by accelerating investments from national security agencies in advanced data collection and analytics to counter increasingly sophisticated threat environments. Growing demand for modernized SIGINT architectures is encouraging multi-year commitments toward system upgrades, analytics platforms, and mission-support services across global intelligence organizations. For instance, in April 2025, Leidos secured a contract valued at up to USD 390 million from the National Security Agency to enhance and sustain next-generation signals intelligence capabilities. The award covers advanced system development, analytical and reporting tool upgrades, and end-to-end engineering, integration, testing, deployment, training, and lifecycle sustainment services, reinforcing the market’s shift toward long-term, capability-driven cyber intelligence modernization.

Type Insights

The ELINT segment is expected to hold a significant share of global revenue in 2025, driven by rising military demand for advanced detection and analysis capabilities in increasingly complex electronic warfare environments. Armed forces are shifting toward turnkey, end-to-end ELINT solutions that integrate sensing, data processing, real-time analytics, and emitter-database management for faster and more cost-efficient deployment. Global investments, particularly from NATO members, are accelerating the adoption of flexible ELINT systems that can be integrated across ground, naval, airborne, and vehicle-based platforms to support multi-domain operations. Advancements in automation, remote operability, wideband receivers, digital signal processing, and software analytics are further enhancing threat detection while reducing manpower requirements and improving decision-making speed.

The COMINT segment is expected to grow significantly during the forecast period, owing to defense organizations’ increasing focus on realistic, simulation-driven training to prepare operators for complex and congested electromagnetic threat environments. Growth is further driven by the shift toward software-based EW and CEMA training solutions that enable full-cycle intelligence practice without live RF emissions, improving safety, scalability, and cost efficiency. For instance, in October 2025, MASS introduced the NEWTS IQ platform to deliver immersive classroom and field-realistic COMINT training through digitally replicated contested electromagnetic scenarios. Such platforms enhance operational readiness by strengthening detection, analysis, and reporting capabilities while providing a scalable, technology-led training infrastructure for modern electronic warfare missions.

Mobility Insights

The fixed segment is expected to hold a significant share of global revenue in 2025, driven by the shift toward multi-sensor fusion that integrates COMINT, ELINT, cyber intelligence, and real-time analytics to deliver comprehensive electromagnetic situational awareness. The expansion of the communications intelligence market is further supporting the deployment of high-capacity, fixed SIGINT infrastructures for persistent monitoring. The integration of electronic warfare intelligence systems is enhancing advanced signal classification, threat detection, and adaptive response capabilities against evolving adversary signals. Strong naval investments in next-generation SIGINT vessels with low-noise propulsion, extended endurance, and higher payload capacities are enabling continuous maritime surveillance. In addition, the growing adoption of satellite-linked intelligence dissemination is reinforcing fixed platforms as critical network-centric assets for national-level early warning, wide-area surveillance, and continuous monitoring.

The portable segment is expected to grow significantly during the forecast period, driven by demand for mobile, rapidly deployable SIGINT systems that support frontline and remote intelligence operations. Growth in the signals intelligence systems segment is supported by increasing integration of AI-enabled emitter identification, automated geolocation, and hybrid ground-drone configurations that enhance operational efficiency. The adoption of advanced surveillance systems is further extending sensing range and improving real-time situational awareness in complex environments. The shift toward modular, software-defined architectures is enabling compact platforms to execute COMINT, ELINT, and direction-finding missions with greater flexibility. In addition, advancements in battery efficiency, ruggedized designs, and low-SWaP components are improving endurance and reliability, accelerating adoption across infantry, border security, and special forces operations.

Regional Insights

The North America signals intelligence industry dominated global revenues with a share of over 36% in 2025, driven by sustained increases in defense spending and rapid advancements in AI capabilities. The signals intelligence industry trends indicate strong regional focus on enhancing intelligence, surveillance, and reconnaissance capabilities amid escalating geopolitical tensions. The integration of AI in signals intelligence is significantly improving signal processing efficiency, deep analytics, and real-time decision-making accuracy. In addition, the presence of leading defense contractors, technology firms, and research institutions is accelerating innovation. This ecosystem continues to reinforce North America’s leadership in next-generation SIGINT capabilities.

U.S. Signals Intelligence (SIGINT) Market Trends

The U.S. signals intelligence industry is expected to witness a significant CAGR over the forecast period, owing to sustained defense modernization initiatives focused on strengthening intelligence and surveillance capabilities. The expansion of the SIGINT technology market is supported by increasing investments in automation, AI, and machine learning for faster threat detection and response. The growing adoption of SIGINT data analytics is further enhancing real-time signal processing and intelligence accuracy. Rising concerns around cyber warfare, electronic attacks, and multi-domain threats are accelerating demand for advanced solutions. Continuous upgrades of legacy systems and integration across space, cyber, and terrestrial domains are further driving long-term market growth.

Europe Signals Intelligence (SIGINT) Market Trends

The Europe signals intelligence industry is expected to witness a significant CAGR over the forecast period, primarily driven by rising defense budgets and the need to strengthen electronic warfare capabilities. The defense signals intelligence industry in the region is benefiting from increased investments in advanced surveillance and border security systems. The adoption of software defined SIGINT systems is enhancing flexibility, scalability, and interoperability across defense networks. Collaborative defense initiatives and NATO-led programs are further modernizing intelligence infrastructure. These developments are collectively improving situational awareness and strengthening regional security frameworks.

Asia Pacific Signals Intelligence (SIGINT) Market Trends

The Asia Pacific signals intelligence industry is expected to achieve the fastest CAGR of over 7.0% during the forecast period, driven by rising geopolitical tensions and increasing defense expenditures across key economies. The growth of the signals intelligence platforms segment is supported by expanding investments in advanced surveillance and intelligence systems. The deployment of electronic warfare intelligence systems is enabling improved threat detection and response capabilities in complex environments. Rapid military modernization and increasing focus on indigenous defense manufacturing are further accelerating market expansion. These factors are positioning Asia Pacific as a high-growth region in the global SIGINT landscape.

Key Signals Intelligence Company Insights

Some of the key players operating in the market include Lockheed Martin Corporation, BAE Systems, Northrop Gruman Corporation, L3Harris Technologies, Inc, Thales Group, and RTX Corporation.

-

Lockheed Martin Corporation offers a comprehensive range of advanced intelligence, surveillance, and reconnaissance (ISR) solutions. These include ground and airborne radar systems, electronic warfare capabilities, satellite and sensor technologies for remote intelligence collection, and integrated C4ISR platforms for real-time data fusion and analytics. Its SIGINT products, such as the Terrestrial Layer System-Brigade Combat Team (TLS-BCT) and Terrestrial Layer System-Echelons Above Brigade (TLS-EAB), are designed to improve situational awareness and operational decision-making across tactical, operational, and multi-domain environments. These solutions provide scalable, interoperable capabilities that support complex military operations and enhance real-time intelligence processing for defense and allied partners.

-

BAE Systems provides a broad range of intelligence and security solutions, with strong capabilities across cyber intelligence, counterintelligence, signals intelligence, and electronic warfare. Its portfolio includes advanced communications and data networks, along with intelligence-gathering sensors deployed on ground vehicles, aircraft, and maritime platforms. Key offerings include unmanned SIGINT and electronic warfare systems, airborne and maritime SIGINT and electronic support solutions, and the Eclipse RF product line, supporting scalable and mission-critical intelligence operations.

Key Signals Intelligence Companies:

The following key companies have been profiled for this study on the signals intelligence market.

- Lockheed Martin Corporation

- BAE Systems

- Thales Group

- Northrop Grumman Corporation

- L3Harris Technologies, Inc.

- Raytheon Technologies

- General Dynamics Corporation

- HENSOLDT AG

- Elbit Systems Ltd.

- Saab AB

- Mercury Systems

Recent Developments

-

In January 2026, Saab launched Poland’s second signals intelligence (SIGINT) ship, ORP Henryk Zygalski, in Gdańsk, marking a key milestone in the DELFIN programme. The vessel is designed to enhance Poland’s maritime intelligence and situational awareness capabilities across the Baltic Sea region. Equipped with advanced reconnaissance and mission systems, the ship will undergo further testing before entering operational service. This development strengthens regional defense capabilities and reflects Europe’s growing focus on advanced naval intelligence infrastructure amid evolving security threats.

-

In January 2026, HawkEye 360 successfully launched its Cluster 13 satellite trio and established initial communications, expanding its space-based signals intelligence capabilities. The satellites were deployed into a sun-synchronous orbit, enabling consistent and enhanced radio-frequency (RF) data collection across key global regions. Equipped with advanced RF detection and geolocation technologies, the cluster improves signal capture accuracy and overall intelligence output. This development strengthens the company’s ability to deliver mission-critical intelligence and reinforces its position in the global SIGINT ecosystem.

-

In November 2025, Thales Group received two PERSEUS awards from the French Navy and defense authorities for its innovations in electronic warfare and AI-enabled intelligence systems. The awards recognized CURCO, a compact radar detection payload for real-time electromagnetic spectrum monitoring, and Golden AI, an advanced tool that accelerates analysis of electronic support measures data. These solutions improve threat detection, situational awareness, and decision-making in contested electromagnetic environments. The recognition further establishes Thales as a leader in next-generation EW and SIGINT technologies for modern defense operations.

-

In November 2025, HENSOLDT AG launched TAERVUS as a fully integrated Electromagnetic Warfare system combining radio direction finders, receivers, jammers, and signal processing for COMINT (communications intelligence) and ELINT (electronic intelligence) across HF/VHF/UHF to microwave bands, enabling spectrum dominance and threat disruption.

-

In October 2025, Raytheon, a subsidiary of RTX Corporation, began initial production of its SharpSight multi-domain surveillance radar. The system delivers high-altitude, real-time, high-resolution imaging for land and maritime missions. It integrates proven radar technologies and can be deployed on manned or unmanned platforms to improve search, tracking, and situational awareness. Its open, upgradeable architecture enhances ISR capabilities, operational flexibility, and mission adaptability across various defense scenarios. This milestone demonstrates Raytheon’s commitment to advancing multi-domain radar solutions for global defense and allied partners.

Signals Intelligence Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 18.5 billion

Estimated Market size in 2026

USD 19.6 billion

Projected Market size by 2033

USD 28.5 billion

Growth rate

CAGR of 5.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Solutions, type, mobility, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; UAE; South Africa

Key companies profiled

Lockheed Martin Corporation; BAE Systems; Thales Group; Northrop Grumman Corporation; L3Harris Technologies, Inc.; Raytheon Technologies; General Dynamics Corporation; HENSOLDT AG; Elbit Systems Ltd.; Saab AB; Mercury Systems

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional, and segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Signals Intelligence Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the signals intelligence marketreport based on, solutions, type, mobility, and region:

-

Solutions Outlook (Revenue, USD Million, 2021 - 2033)

-

Airborne

-

Ground

-

Naval

-

Space

-

Cyber

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Electronic Intelligence (ELINT)

-

Communications Intelligence (COMINT)

-

-

Mobility Outlook (Revenue, USD Million, 2021 - 2033)

-

Fixed

-

Portable

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global signals intelligence market size was estimated at USD 18.5 billion in 2025 and is expected to reach USD 19.6 billion in 2026

The global signals intelligence market is expected to grow at a compound annual growth rate of 5.5% from 2026 to 2033 to reach USD 28.5 billion by 2033

North America dominated the SIGINT market, accounting for over 36% share in 2025. Factors such as the increasing defense budget and the rising innovations in artificial intelligence (AI) are propelling market growth in the region.

Some key players operating in the signals intelligence market include Lockheed Martin Corporation; BAE Systems; Thales; Northrop Grumman; L3Harris Technologies; Raytheon Technologies; General Dynamics; HENSOLDT AG; Elbit Systems; Saab; Mercury Systems.

Key factors that are driving the market growth include rising demand for advanced digital solutions across industries, increasing adoption of cloud-based and AI-driven technologies, growing need for operational efficiency and automation, and expanding investments in infrastructure and innovation.

Asia Pacific is expected to be the fastest-growing regional market over the forecast period, with a CAGR of over 7.0% from 2026 to 2033.

The airborne segment led the market with a revenue share of over 40% in 2025, while the cyber segment is expected to witness significant growth over the forecast period.

The Electronic Intelligence (ELINT) segment held the largest revenue share of over 71% in 2025, while the Communications Intelligence (COMINT) segment is expected to grow significantly during the forecast period.

The fixed segment held the largest market share in 2025, while the portable segment is expected to grow at the fastest CAGR of over 8%.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.