- Home

- »

- Plastics, Polymers & Resins

- »

-

Smart Plastics Market Size, Share, Trends Report, 2026-2033GVR Report cover

![Smart Plastics Market (2026 - 2033)Report]()

Smart Plastics Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Shape Memory Polymers, Conductive Polymers, Self-Healing Polymers), By End Use (Automotive, Healthcare, Consumer Electronics), By Region, And Segment Forecasts

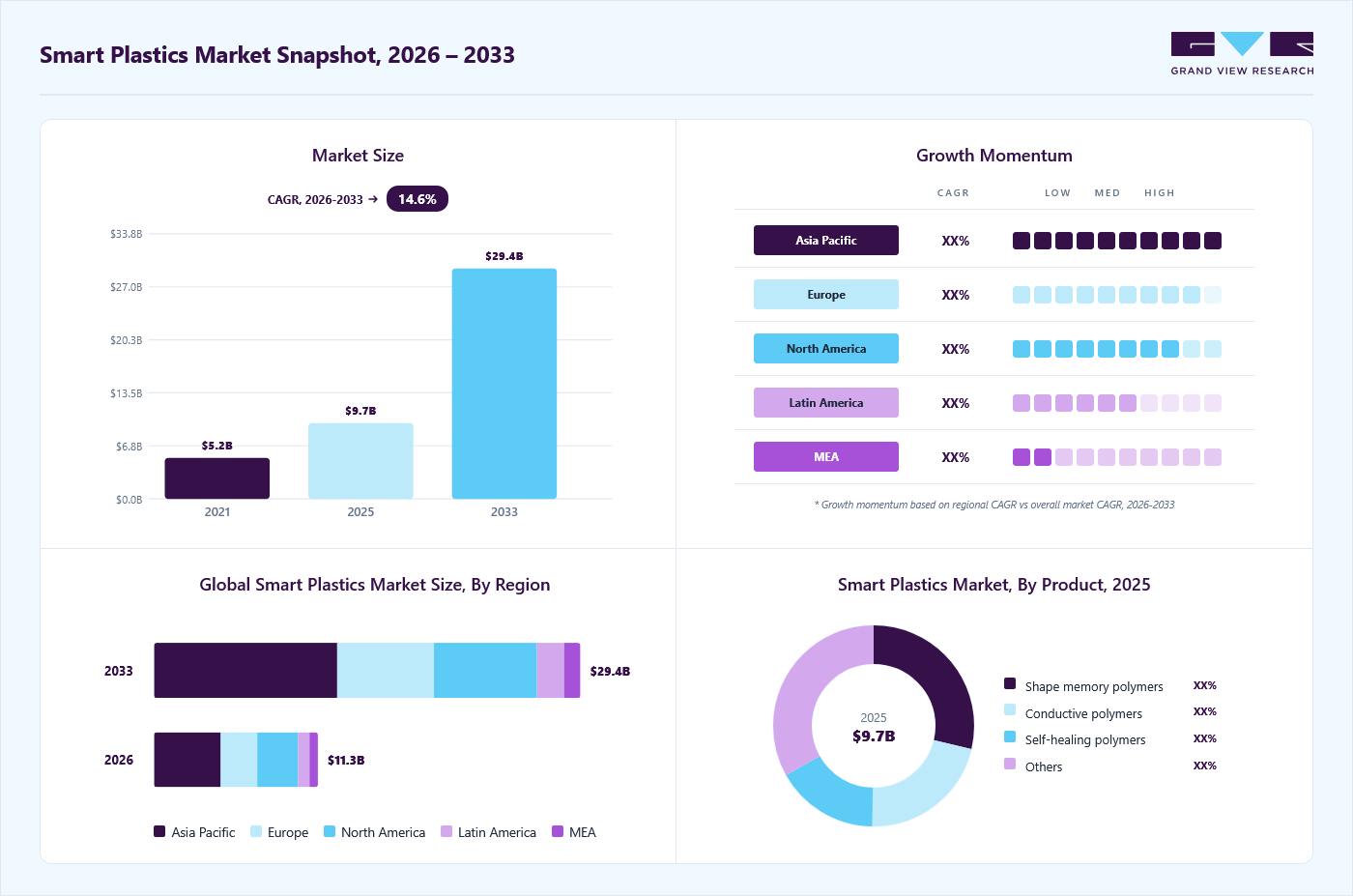

Market Size, 2025

$9.7BMarket Estimate, 2026

$11.3BMarket Forecast, 2033

$29.4BCAGR, 2026–2033

14.6%Smart Plastics Market Summary

The global smart plastics market size was valued at USD 9.7 billion in 2025 and is projected to grow from USD 11.3 billion in 2026 to USD 29.4 billion by 2033, at a CAGR of 14.6% from 2026 to 2033. The Asia Pacific held the largest share of 40.4% of the global market in 2025. Increasing adoption of smart manufacturing and industrial automation is driving demand for smart plastics with sensing and responsive properties.

Key Market Trends & Insights

- By product: Shape memory polymers segment held the largest market share of 28.7% in 2025.

- By end use: Automotive segment held the largest market share of 28.9% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (40.4% revenue share, 2025)

- By country: China held the largest share in 2025

Market Size & Forecast

- Market size in 2025: USD 9.7 Billion

- Estimated market size in 2026: USD 11.3 Billion

- Projected market size by 2033: USD 29.4 Billion

- CAGR (2026-2033): 14.6%

These materials support real-time monitoring, predictive maintenance, and process efficiency, which helps manufacturers reduce downtime and improve production output. Smart plastics are shifting from passive structural parts to multifunctional system components that combine transparency, heat resistance, sensing, and user interaction. Recent development activity points to integrated applications such as heated sensor covers, in-mold electronics, and sensor-enabled furniture, which reduce part count and improve design freedom. The market is increasingly defined by component-level integration, where plastics carry mechanical, optical, and electronic functions in one platform.")

Drivers, Opportunities & Restraints

Demand is being pulled by vehicle lightweighting, electrification, and compact electronics, where materials must deliver impact resistance, dimensional stability, thermal stability, and optical clarity. High-performance thermoplastics are being used in automotive, electrical, industrial automation, and sensing applications because they support thin-wall parts, transparent housings, and durable surfaces in demanding conditions. This makes smart plastics a practical enabler for EV interfaces, charging systems, optical sensors, and connected devices.

Circularity is creating a new opening for smart plastics designed around recovery, recyclability, and recycled-content integration. Research on catalytic pyrolysis and other chemical recycling routes shows a path to reclaim raw materials from plastic waste and return them into production cycles. At the same time, major material developers are prioritizing alternative raw materials and new recycling methods, which can support higher-value smart plastic platforms in automotive, electronics, and industrial use cases.

The market still faces cost and end-of-life barriers because smart plastic parts often require custom formulations, multi-step processing, and tight performance tolerances. Embedded electronics, conductive layers, and multi-material structures make separation and recycling difficult, especially in electrical and electronic equipment, where recovery remains technically complex. Development cycles are also longer because producers must balance mechanical, thermal, optical, and electrical performance in one part, which limits scale-up beyond premium applications.

Market Concentration & Characteristics

The market growth stage is high, and growth is accelerating. The market exhibits fragmentation, with key players dominating the industry landscape. Major companies such as Covestro, SMP Technologies Inc., Shape Memory Medical Inc., Evonik Industries AG, Heraeus Group, DuPont de Nemours, Inc., Arkema, Mitsubishi Chemical Group, SABIC, Lubrizol Corporation, and others play a significant role in shaping the market dynamics. These leading players often drive innovation in the market, introducing new products, technologies, and product types to meet the industry's evolving demands.

The degree of innovation in the smart plastics market is high as the material set is moving beyond passive lightweighting into integrated sensing, display, and functional surface platforms. Current development work shows plastic substrates being used for in-mold electronics and flexible printed electronics, while self-healing films add autonomous repair capability. This raises the functional load carried by each part and reduces assembly steps. It also expands use cases in automotive interiors, wearables, healthcare sensors, and building-envelope materials.

Product substitutes remain available, but they are usually weaker in system integration. Conventional engineering plastics, metals, glass, ceramics, and discrete electronic assemblies can replace smart plastics in cost-sensitive designs, yet they often add weight, part count, and assembly complexity. In applications that do not require sensing, self-repair, or flexible form factors, buyers can still choose standard materials. The substitution risk is therefore moderate and concentrated in low-value applications, while connected and adaptive products continue to favor smart plastics.

Product Insights

Shape memory polymers segment dominated the market, accounting for a revenue share of 28.7% in 2025, and is projected to grow at a 14.2% CAGR from 2026 to 2033. Demand is rising as shape memory polymers let device makers build parts that are compact during delivery and then recover to a programmed shape when triggered by heat, fluid uptake, or mechanical force. That behavior supports less invasive insertion, lower deployment force, and better fit in confined anatomical spaces. Commercial validation is also improving as FDA-cleared devices built on shape memory polymer technology move into broader clinical use, which strengthens confidence in the platform for vascular and bone-fixation applications.

The self-healing polymers segment is anticipated to grow at the fastest CAGR of 16.3%over the forecast period. The main driver is the need to extend product life in coatings, sealants, and barrier films where small defects quickly reduce performance. Government-backed work shows that self-healing films can keep insulation barriers intact after cuts or punctures, while self-healing coatings can repair scratches and preserve water and wear resistance. This lowers maintenance burden and replacement frequency. For manufacturers, the value lies in longer service intervals, stronger durability claims, and better lifecycle economics in high-wear applications.

End Use Insights

Automotive segment dominated the market in terms of revenue, accounting for a 28.9% market share in 2025, and is projected to grow at a 14.7%CAGR from 2026 to 2033. Lightweighting remains the core demand engine for smart plastics in automotive applications. The Department of Energy notes that lightweight materials are especially important in hybrid and electric vehicles because they offset the weight of batteries and motors, improve efficiency, and extend driving range. It also highlights the need to integrate advanced emission systems, safety devices, and electronics without adding mass. This directly favors smart plastic parts that combine low weight with functional integration, durability, and design flexibility.

The healthcare segment is expected to expand at a robust 15.9% CAGR over the forecast period in the automotive smart plastics glazing market. Healthcare demand is being shaped by the shift toward minimally invasive care, continuous monitoring, and higher-performance wound management. NIBIB has highlighted flexible sensors that can measure temperature and strain separately for wound monitoring, while implantable soft robots can detect and respond to physiological stimuli. At the same time, FDA biocompatibility requirements keep material compatibility central to device design. This supports smart plastics that can serve in wearables, implantables, and advanced wound care formats.

Regional Insights

The Asia Pacific smart plastics industry held the largest share, accounting for 40.4% of the revenue in 2025, and is expected to grow at the fastest CAGR of 15.5% over the forecast period. Asia Pacific is gaining momentum from its leadership in semiconductors, data-heavy electronics, and supply chain integration. WSTS reported 45.4% year-on-year semiconductor sales growth in the region in 2025, which reinforces demand for smart plastics in sensor covers, flexible electronics, and device enclosures. ASEAN’s long-term plan also positions the region as a more competitive production center with deeper intra-regional trade and stronger global supply chain linkages.

Smart plastic market in China is scaling up due to new materials base alongside faster industrial upgrading. The new materials industry is expected to grow rapidly, and the government is building a big data center plus innovation centers to digitalize the raw materials chain. Industrial production also remained solid in 2024, with manufacturing up 6.1%, automobiles up 17.7%, and computers and communication equipment up 8.7%, as per the State Council of China. This supports broad adoption of smart plastics in high-growth end markets.

North America Smart Plastics Market Trends

North America is being supported by a stronger shift toward advanced manufacturing and flexible electronics. The regional semiconductor market rose sharply in 2025, while Canadian research institutions are printing functional components for sensors, transparent conductive films, antennas, and other low-cost electronic parts. That is expanding the use case for smart plastics in housings, interfaces, and embedded device surfaces. The region is also prioritizing supply chain resilience and healthcare-focused manufacturing.

U.S. Smart Plastics Market Trends

In the U.S., demand is driven by the push to combine lightweighting, connected mobility, and healthcare innovation in one manufacturing base. Federal strategy now explicitly targets advanced manufacturing technologies, stronger supply chains, and improved healthcare outcomes. In parallel, NIST work on microprinting on curved surfaces points to new possibilities in electronics, optics, and biomedical engineering. This supports smart plastics that can carry structural, sensing, and functional roles in compact designs.

Europe Smart Plastics Market Trends

Europe is being driven by regulation that rewards recyclable, repairable, and resource-efficient material systems. The Packaging and Packaging Waste Regulation entered into force in February 2025, the right to repair took effect in July 2024, and the Circular Plastics Alliance is pushing design-for-recycling guidelines for priority products. This is increasing the appeal of smart plastics that can deliver sensing or adaptive performance without compromising recyclability, especially in packaging, electronics, and automotive components.

Key Smart Plastics Company Insights

The smart plastics industry is highly competitive, with several key players dominating the landscape. Major companies include Covestro, SMP Technologies Inc., Shape Memory Medical Inc., Evonik Industries AG, Heraeus Group, DuPont de Nemours, Inc., Arkema, Mitsubishi Chemical Group, SABIC, and Lubrizol Corporation. The smart plastics industry is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their products.

Key Smart Plastics Companies:

The following key companies have been profiled for this study on the smart plastics market.

- Covestro

- SMP Technologies Inc.

- Shape Memory Medical Inc.

- Evonik Industries AG

- Heraeus Group

- DuPont de Nemours, Inc.

- Arkema

- Mitsubishi Chemical Group

- SABIC

- Lubrizol Corporation

Recent Developments

-

In December 2025, Shape Memory Medical secured EU MDR certification for its IMPEDE Embolization Plug product family, which uses proprietary shape memory polymer technology for endovascular applications. The approval strengthens European market access for a commercially proven smart plastic platform and supports broader adoption in vascular care, where self-expanding, catheter-delivered polymer devices are gaining clinical traction.

-

In March 2025, Evonik partnered with 3DChimera to distribute its INFINAM selective laser sintering powders in the U.S. The agreement broadens access to high-flexibility, high-temperature-resistance, and high-stiffness polymer powders for industrial 3D printing, which supports demand for advanced plastic parts in prototyping, medical, and lightweight functional component applications.

Smart Plastics Market Report Scope

Report Attribute

Details

Market size in 2025

USD 9.7 billion

Estimated market size in 2026

USD 11.3 billion

Projected market size by 2033

USD 29.4 billion

Growth rate

CAGR of 14.6% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Product, end use, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; South Korea; Australia; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

Covestro; SMP Technologies Inc.; Shape Memory Medical Inc.; Evonik Industries AG; Heraeus Group; DuPont de Nemours, Inc.; Arkema; Mitsubishi Chemical Group; SABIC; Lubrizol Corporation

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Smart Plastics Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the smart plastics market report based on product, end use, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Silk Smart Plastics

-

Polyester Smart Plastics

-

Nylon Smart Plastics

-

Blended / Specialty Smart Plastics

-

-

End use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Automotive

-

Healthcare

-

Consumer electronics

-

Aerospace and Defense

-

Building and Construction

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

Frequently Asked Questions About This Report

Asia Pacific dominated with a 40.4% revenue share in 2025.

The automotive segment led with a 28.9% revenue share in 2025, while the healthcare segment is the fastest-growing.

The global smart plastics market size was estimated at USD 9.7 billion in 2025 and is expected to reach USD 11.3 billion in 2026.

Shape memory polymers dominated the market across all product segments in terms of revenue, accounting for a 28.7% market share in 2025, and is forecasted to grow at a 14.2% CAGR from 2026 to 2033.

Some key players operating in the smart plastics market include Covestro, SMP Technologies Inc., Shape Memory Medical Inc., Evonik Industries AG, Heraeus Group, DuPont de Nemours, Inc., Arkema, Mitsubishi Chemical Group, SABIC, and Lubrizol Corporation

Increasing adoption of smart manufacturing and industrial automation is driving demand for smart plastics with sensing and responsive properties. These materials support real-time monitoring, predictive maintenance, and process efficiency, which helps manufacturers reduce downtime and improve production output.

The global smart plastics market is expected to grow at a compound annual growth rate of 14.6% from 2026 to 2033 to reach USD 29.4 billion by 2033.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.