- Home

- »

- Next Generation Technologies

- »

-

SONAR System Market Size And Share Report, 2026-2033GVR Report cover

![SONAR System Market (2026 - 2033)Report]()

SONAR System Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Hull-Mounted, Stern Mounted, Sonobuoy, DDS), By Platform (Ship Type, Airborne), By Application (Defense, Commercial), By Region, And Segment Forecasts

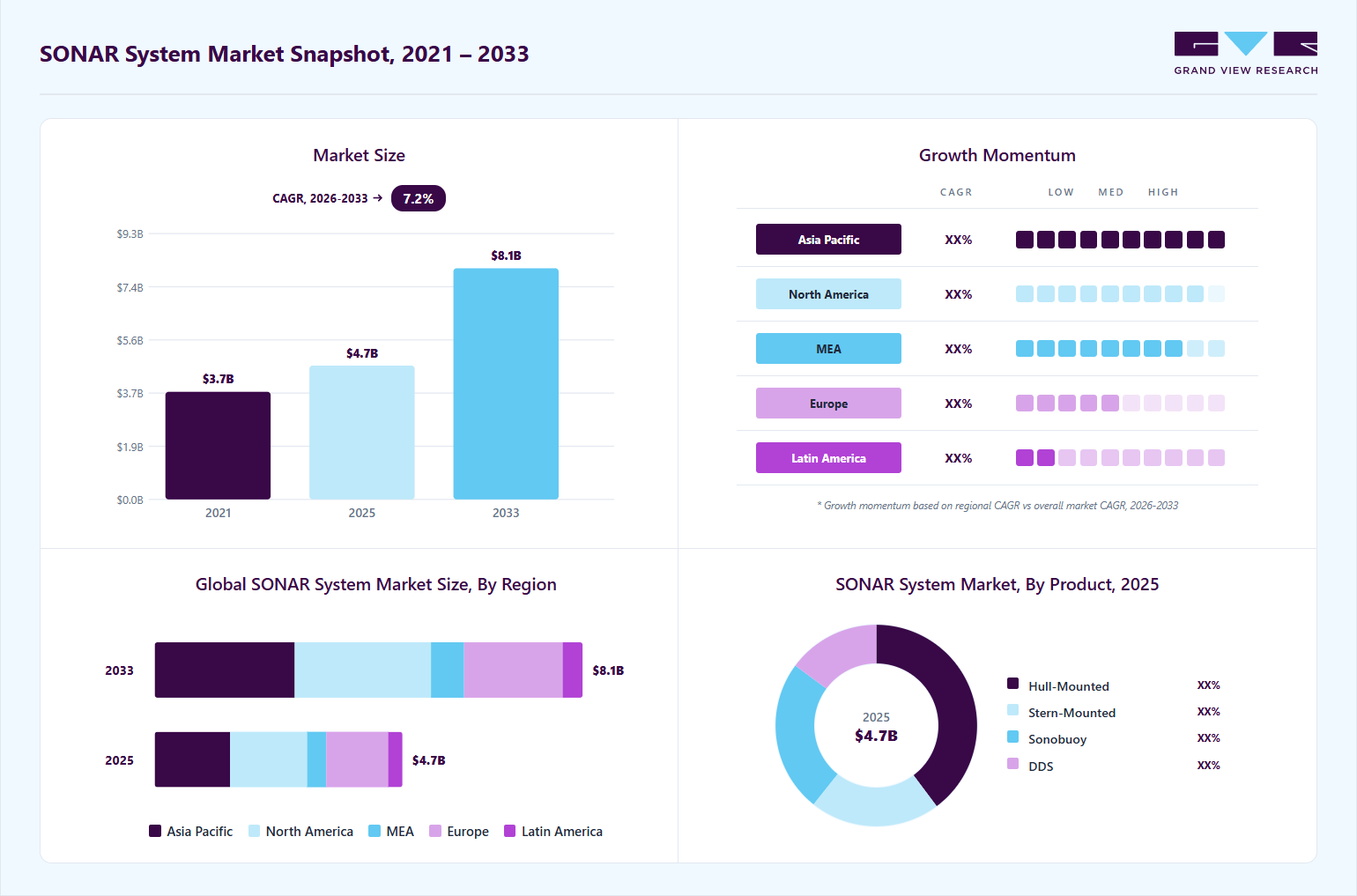

Market Size, 2025

$4.7BMarket Estimate, 2026

$4.9BMarket Forecast, 2033

$8.1BCAGR, 2026–2033

7.2%SONAR System Market Summary

The global SONAR system market size was valued at USD 4.7 billion in 2025 and is projected to grow from USD 4.9 billion in 2026 to USD 8.1 billion by 2033, at a CAGR of 7.2% from 2026 to 2033. The market in North America dominated with a revenue share of 31.1% in 2025. The growth of the SONAR systems is attributed to the increasing national security and defense across the globe.

Key Market Trends & Insights

- By product: Hull-mounted segment held the largest market share of 39.8% in 2025.

- By platform: Ship type segment held the largest market share in 2025.

- By application: Defense segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (31.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 4.7 Billion

- Estimated market size in 2026: USD 4.9 Billion

- Projected market size by 2033: USD 8.1 Billion

- CAGR (2026-2033): 7.2%

SONAR systems enhance a country's ability to monitor and secure its coastal waters and strategic maritime routes. Hence, navies and maritime forces rely on SONAR technology to detect submarines, mines, and underwater threats.Many nations are prioritizing the modernization of their naval fleets, investing in advanced SONAR systems for improved underwater surveillance and threat detection.")

This trend is particularly strong in countries with extensive coastlines and strategic maritime interests, such as the U.S., China, and India. Enhanced detection capabilities of modern SONAR systems are essential for maintaining national security and ensuring maritime dominance.

Countries across the globe are increasingly investing in SONAR technology to bolster their naval capabilities, protect their coastlines, and monitor maritime traffic, thereby enhancing their security posture. Consequently, defense budgets are increasingly allocated toward the development and procurement of sophisticated SONAR technology. Furthermore, the rise of offshore industries, such as oil & gas exploration and renewable energy projects, has led to greater reliance on SONAR for underwater mapping, inspection, and maintenance. As a result, the growing need for maritime security and surveillance has fueled the demand for SONAR systems.

Marine exploration and scientific research represent additional driving forces in the SONAR system industry. Researchers and oceanographers utilize SONAR systems to study marine biodiversity, map underwater topography, and monitor environmental changes. The growing interest in understanding and preserving marine ecosystems has led to increased funding for oceanographic research and exploration missions. High-resolution SONAR systems provide valuable data that aids in the conservation of marine life and the sustainable management of ocean resources. As environmental awareness and scientific curiosity continue to grow, the demand for advanced SONAR systems in the scientific community is expected to rise.

Technological advancements in SONAR systems, including improved sensor technology, data processing capabilities, and the integration of artificial intelligence, are making these systems more versatile and efficient. As a result, SONAR systems are finding applications beyond the traditional maritime and defense sectors, including underwater archaeology, underwater robotics, and autonomous underwater vehicles. For instance, in November 2022, DRDO (Defense Research and Development Organization), an Indian agency under the Department of Defense Research and Development in the Ministry of Defense of the Government of India, launched the SONAR systems evaluation and test facility named Hull Module of Submersible Platform for Acoustic Characterization and Evaluation (SPACE) for the Indian Navy.

The commercial shipping and fishing industries are contributing to the market's growth by adopting SONAR technology for various applications. Commercial vessels use SONAR for navigation, collision avoidance, and locating fish stocks, improving the efficiency and safety of their operations. The fishing industry, in particular, benefits from SONAR systems that help identify and track fish populations, leading to more sustainable fishing practices. As these industries seek to optimize their operations and comply with stricter environmental regulations, the adoption of advanced SONAR technology is becoming increasingly essential. This trend highlights the diverse applications of SONAR systems beyond defense, underscoring their importance in various maritime activities.

Market Dynamics

The increasing need for improved maritime security, underwater threat detection, and situational awareness is a major driver of the SONAR system industry. Navies across the world are investing heavily in anti-submarine warfare (ASW), mine detection, and seabed mapping capabilities, where sonar systems play a critical role. The growing strategic importance of maritime borders, offshore energy assets, and undersea communication infrastructure is further accelerating adoption. Modern sonar technologies, including synthetic aperture sonar, multi-beam sonar, and AI-enabled acoustic imaging systems, are enabling real-time underwater visibility and highly accurate target identification. In addition, the expansion of autonomous underwater vehicles (AUVs) and unmanned naval platforms is significantly boosting demand for compact, high-performance sonar systems integrated with advanced signal processing capabilities.

The market faces constraints due to the high cost and complexity associated with advanced underwater sensing technologies. The development and deployment of sonar systems require significant investment in specialized hardware, signal-processing software, calibration systems, and platform integration, particularly for naval-grade applications. In addition, maintenance in harsh underwater environments, the requirement for skilled operators, and periodic system upgrades further increase lifecycle costs. These challenges are especially limiting for developing economies and smaller naval forces with constrained defense budgets.

The rapid expansion of autonomous underwater vehicles (AUVs), unmanned surface vessels (USVs), and smart naval platforms is creating significant opportunities for the SONAR system industry. These platforms require compact, energy-efficient, and highly sensitive sonar systems for navigation, obstacle avoidance, and target detection. At the same time, the increasing adoption of AI, machine learning, and real-time acoustic data analytics is transforming sonar from a traditional detection tool into an intelligent underwater sensing system. Naval forces are also moving toward networked maritime ecosystems, where sonar systems are integrated with satellite communication, command-and-control systems, and multi-domain surveillance networks.

Market Concentration & Characteristics

The SONAR system industry is moderately consolidated, with a limited number of large global defense contractors and marine technology companies accounting for a significant share of the market. Leading players compete based on technological capabilities, underwater detection accuracy, product reliability, and long-term defense contracts.

Major companies dominate the market through strong R&D investments, advanced sonar integration capabilities, extensive naval partnerships, and established relationships with defense ministries and shipbuilders. However, several regional and niche players continue to operate in specialized segments such as commercial marine sonar, underwater robotics, offshore exploration, and autonomous underwater vehicle (AUV) applications. The presence of emerging players in the Asia Pacific and Europe is contributing to increased innovation and competition in compact, AI-enabled, and modular sonar solutions.

Strategic collaborations, defense partnerships, acquisitions, and long-term naval modernization contracts are common across the industry as companies aim to strengthen their technological capabilities and global presence. Many leading companies are focusing on the development of synthetic aperture sonar (SAS), AI-driven acoustic processing, and integrated underwater surveillance systems to maintain a competitive advantage. Vertical integration through in-house software development, sensor manufacturing, and platform integration also remains an important strategy among established players.

Product Insights

The hull-mounted segment led the market with the largest revenue share of 39.78% in 2025. Key factors driving the use of hull-mounted sensors include enhancing maritime security by detecting submarines and underwater mines, supporting fisheries management by detecting fish, and facilitating underwater mapping and exploration. Advancements in technology, such as improved sensor sensitivity and signal processing capabilities, continue to drive the evolution of hull-mounted systems, making them indispensable for various marine applications.In addition, technological advancements have led to the development of more compact and efficient hull-mounted SONAR systems, making them easier to install and maintain on various types of vessels. As maritime security concerns continue to escalate, both military and commercial fleets are increasingly investing in hull-mounted SONAR systems to ensure safe, effective operations.

The sonobuoy segment is anticipated to grow at a significant CAGR during the forecast period, driven by its critical role in anti-submarine warfare and maritime surveillance. Sonobuoys, which are deployed from aircraft or ships, provide real-time data on underwater acoustic environments, aiding in the detection and tracking of submarines. The increasing need for enhanced maritime security and defense capabilities is a major driver, prompting investments in advanced sonobuoy technology. Innovations such as improved signal processing, longer operational life, and better data transmission have made sonobuoys more effective and reliable. In addition, the rising geopolitical tensions and the strategic importance of maintaining naval dominance in contested waters are further propelling the demand for sophisticated sonobuoy systems.

Platform Insights

The ship type segment accounted for the largest market revenue share in 2025. This dominance can be attributed to the growing need for effective underwater navigation, detection, and communication. These systems enhance maritime safety and security by enabling ships to detect underwater obstacles, map the seabed, locate submarines, and communicate with other vessels or underwater assets. Naval and commercial vessels are increasingly equipped with sophisticated hull-mounted and towed-array SONAR systems, which are essential for navigation, threat detection, and marine research. These systems provide critical data that enhances maritime situational awareness and ensures the safety of vessel operations.

The airborne segment is anticipated to grow at the fastest CAGR during the forecast period, driven by its critical role in rapid, expansive underwater surveillance. Maritime patrol aircraft and helicopters equipped with advanced SONAR systems can quickly deploy and collect real-time data over large ocean areas. This capability is essential for anti-submarine warfare, search and rescue operations, and maritime border security, enabling swift responses to potential threats. Technological advancements have enhanced the efficiency and accuracy of airborne SONAR systems, making them more effective in diverse operational environments.

Application Insights

The defense segment accounted for the largest market revenue share in 2025. The growth of the sector is owing to the growing maritime threats, including submarine activity, which drives the need for advanced underwater surveillance and detection capabilities. Moreover, the rise of Autonomous Underwater Vehicles (AUVs) and unmanned underwater systems has created a demand for improved underwater communication and navigation, further fueling the adoption of SONAR systems. Technological advancements, such as improved signal processing and AI integration, have made defense SONAR systems more effective in detecting and tracking underwater threats. The modernization of naval fleets and the development of new submarines and surface vessels are further driving the demand for cutting-edge SONAR technology. As nations prioritize national security and maritime dominance, the defense segment of the SONAR system industry is expected to continue growing and innovating.

The commercial segment is anticipated to grow at the fastest CAGR during the forecast period, driven by the growing need for advanced underwater navigation, exploration, and resource management. Commercial applications such as oil and gas exploration, commercial fishing, and maritime shipping rely heavily on SONAR technology for safe and efficient operations. Innovations in high-resolution imaging and seabed mapping have significantly improved the accuracy and effectiveness of commercial SONAR systems. In addition, the increasing focus on sustainable fishing practices and environmental monitoring is driving the adoption of SONAR systems in the commercial sector. As global maritime trade and underwater resource exploration continue to grow, the demand for reliable and sophisticated SONAR technology in the commercial segment is set to rise.

Regional Insights

North America dominated the global SONAR system market with the largest revenue share of 31.12% in 2025. The market is driven by robust defense spending and technological innovation. The U.S., in particular, is focused on maintaining its naval superiority through the continuous upgrade of its SONAR capabilities for anti-submarine warfare, mine detection, and underwater surveillance. The presence of major defense contractors and advanced research facilities in North America supports the development of cutting-edge SONAR technology. In addition, the commercial sector, including offshore oil and gas exploration and marine research, is also a significant driver of the SONAR market. The region's emphasis on securing its maritime borders and protecting critical underwater infrastructure further fuels the demand for advanced SONAR systems.

U.S. SONAR System Market Trends

The SONAR system market in the U.S. accounted for the largest market revenue share in North America in 2025. In the U.S. market, technological advancements and innovations in anti-submarine warfare systems are critical to addressing evolving maritime threats. In addition, the commercial sector's demand for advanced SONAR systems in offshore oil and gas exploration and marine research contributes to market growth.

Asia Pacific SONAR System Market Trends

The SONAR system market in the Asia Pacific is anticipated to grow at the fastest CAGR of 8.2% during the forecast period. Countries such as China, India, and Japan are actively modernizing their naval capabilities, with SONAR technology enhancing underwater surveillance, submersible detection, and ensuring maritime domain awareness. In addition, the rapid growth of commercial shipping and the burgeoning offshore energy industry further increase demand for the SONAR system to ensure safe navigation and protection region stability.Technological advancements and regional collaborations are also contributing to the market's expansion, as countries seek to bolster their defense and commercial maritime capabilities.

The China SONAR system market held a substantial market share in the Asia Pacific in 2025. supported by rapid naval expansion, strong domestic defense manufacturing capabilities, and increasing investment in underwater warfare technologies. The country’s focus on developing advanced submarine fleets, integrated naval combat systems, and AI-enabled underwater sensing networks is a key factor driving the adoption of next-generation sonar technologies across both defense and maritime monitoring applications.

Europe SONAR System Market Trends

The SONAR system market in Europe is propelled by the need to enhance maritime security and maintain strategic maritime interests. Countries such as the UK, Germany, and France are investing in advanced SONAR technologies to support their naval modernization programs and bolster underwater surveillance capabilities. The region's focus on anti-submarine warfare and the protection of maritime borders is a key driver of market growth. In addition, Europe's extensive involvement in marine research and environmental monitoring activities necessitates the use of high-resolution SONAR systems. Collaborative defense initiatives within the European Union and with NATO allies further stimulate the demand for state-of-the-art SONAR technology in the region.

The UK SONAR system market is expected to grow rapidly during the forecast period. Government initiatives focused on strengthening coastal defense, anti-submarine warfare (ASW), and critical infrastructure protection are driving the adoption of advanced sonar technologies.

The SONAR system market in Germany held a substantial market share in Europe in 2025. The country’s focus on high-precision engineering and advanced underwater detection systems supports the widespread deployment of hull-mounted sonar, towed-array sonar, and mine-detection systems.

Key SONAR System Company Insights

Some of the key players operating in the market include Raytheon Systems International Company, Thales, Lockheed Martin Corporation, and others. Organizations in the sonar system industry are increasingly focusing on expanding their customer base and strengthening their technological capabilities to gain a competitive advantage.

As demand rises across naval defense, offshore exploration, and underwater surveillance applications, key players are actively pursuing strategic initiatives, including mergers and acquisitions, partnerships, and long-term collaborations.

-

Raytheon Technologies (now part of RTX) is a major U.S.-based aerospace and defense company specializing in advanced radar, sonar, missile systems, and electronic warfare technologies. In the sonar and underwater domain, it develops naval combat systems, anti-submarine warfare (ASW) sensors, and integrated shipborne sonar suites used by the U.S. Navy and allied forces. The company is strongly focused on multi-domain defense systems that combine sensors, AI-enabled analytics, and networked battle management capabilities.

-

Thales Group is a French multinational company known for its expertise in defense electronics, underwater systems, and naval sonar technologies. It is one of the global leaders in sonar systems for submarines, surface ships, and autonomous underwater vehicles (AUVs), including hull-mounted sonar, towed arrays, and AI-based underwater detection systems. Thales focuses heavily on advanced signal processing, stealth detection, and integrated maritime surveillance solutions, supporting navies across Europe, Asia, and the Middle East.

Key SONAR System Companies:

The following key companies have been profiled for this study on the SONAR system market.

- Raytheon Systems International Company

- Thales

- Atlas Elektronik

- Sonardyne

- L3Harris Technologies, Inc.

- Ultra Electronics Group

- KONGSBERG

- Lockheed Martin Corporation

- Teledyne Technologies Incorporated

- Furuno Electric Co., Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Thales; Lockheed Martin Corporation; Raytheon Systems International Company; KONGSBERG

- Mature players in the sonar system market adopt a set of well-defined operating strategies focused on strengthening technological leadership and expanding defense contracts.

- A key strategy is heavy investment in research and development (R&D) to enhance sonar performance.

- Mature players in the sonar system market gain a strong competitive edge through extensive global naval and defense program networks, established underwater testing and manufacturing infrastructure, and advanced real-time acoustic data processing capabilities.

- Their long-standing expertise enables them to deliver highly reliable and mission-critical sonar solutions for complex applications such as submarine detection, mine countermeasures, and deep-sea surveillance.

- Despite their strong technological capabilities and global presence, mature players in the sonar system market face several inherent weaknesses. One key limitation is the high dependency on defense and government contracts, which exposes them to fluctuations in national defense budgets, procurement delays, and shifting geopolitical priorities.

- This heavy reliance on a limited set of buyers can restrict revenue diversification and increase long-term business uncertainty.

Emerging Players: Atlas Elektronik; Sonardyne International Ltd

- Emerging players in the sonar system market focus on delivering specialized, cost-effective, and application-specific underwater sensing solutions tailored to niche requirements

- Emerging players in the sonar system market gain a competitive edge through operational agility, faster innovation cycles, and the ability to deliver highly customized underwater sensing solutions for specific mission requirements.

- Their leaner organizational structures enable quicker development and deployment of sonar technologies tailored for small-scale naval platforms.

- Emerging players in the sonar system market gain a competitive edge through operational agility, faster innovation cycles, and the ability to deliver highly customized underwater sensing solutions for specific mission requirements.

- Their leaner organizational structures enable quicker development and deployment of sonar technologies tailored for small-scale naval platforms.

Recent Developments

-

In May 2026, Meteksan Defense unveiled the MİLSAS Synthetic Aperture Sonar (SAS) system at SAHA Expo 2026, developed under Türkiye’s Secretariat of Defense Industries with Meteksan as the main contractor. The system transfers synthetic-aperture imaging expertise from airborne radar (MİLSAR) to underwater sonar applications. It is designed to produce high-resolution seabed imagery of less than 4 cm resolution, enabling advanced underwater detection and classification. MİLSAS supports AI-based automatic target detection and offers a range of up to 300 meters, with operations at depths of 0-600 meters.

SONAR System Market Report Scope

Report Attribute

Details

Market size in 2025

USD 4.7 billion

Estimated market size in 2026

USD 4.9 billion

Projected market size by 2033

USD 8.1 billion

Growth rate

CAGR of 7.2% from 2026 to 2033

Base year for estimation

2025

Historical Data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share, competitive landscape, growth factors, and trends

Segments covered

Product, platform, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Raytheon Systems International Company; Thales; Atlas Elektronik; Sonardyne; L3Harris Technologies, Inc.; Ultra Electronics Group; KONGSBERG; Lockheed Martin Corporation; Teledyne Technologies Incorporated; Furuno Electric Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global SONAR System Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global SONAR system market report based on product, platform, application and region.

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Hull-Mounted

-

Stern Mounted

-

Sonobuoy

-

DDS

-

-

Platform Outlook (Revenue, USD Million, 2021 - 2033)

-

Ship Type

-

Airborne

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Defense

-

Commercial

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

Kingdom of Saudi Arabia (KSA)

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cross-Segmentation Analysis for the SONAR System Market

Criss-cross market analysis by type, application

Demand and adoption assessment across key segments

Segment attractiveness and growth potential benchmarking

Identified high-potential market segments

Supported targeted product positioning and marketing strategy

Improved customer and segment prioritization

Competitive Benchmarking and Strategic Positioning in the SONAR System Market

Benchmarking of key competitors across products, partnerships, and innovation

Comparative assessment of market share, capabilities, and strategies

Analysis of competitive strengths, gaps, and differentiation areas

Identified competitive white spaces and growth gaps

Supported strategic positioning and differentiation

Enabled data-driven competitive strategy development

Regional SONAR System Market Opportunity Assessment

Country/region-wise market sizing and forecasts

Analysis of demand, adoption trends, and regulatory landscape

Identification of high-growth regions and investment hotspots

Identified region-specific growth opportunities

Supported expansion and go-to-market strategy

Enabled informed regional investment decisions

Frequently Asked Questions About This Report

North America dominated with a 31.1% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include RAYTHEON SYSTEMS INTERNATIONAL COMPANY Thales; ATLAS ELEKTRONIK; Sonardyne; L3Harris Technologies, Inc.; Ultra Electronics Group; KONGSBERG; Lockheed Martin Corporation.; Teledyne Technologies Incorporated; and FURUNO ELECTRIC CO., LTD.

Key factors that are driving the market growth include growth in the deliveries of military vessels and increasing defense expenditures in emerging economies.

The hull-mounted segment led with a 39.8% revenue share in 2025.

The ship type segment held the largest revenue share in 2025, while the airborne segment is the fastest-growing.

The defense segment held the largest revenue share in 2025, while the commercial segment is the fastest-growing.

The global SONAR system market size was valued at USD 4.7 billion in 2025 and is estimated at USD 4.9 billion for 2026.

The global SONAR system market is expected to grow at a CAGR of 7.2% from 2026 to 2033, reaching USD 8.1 billion by 2033.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.