- Home

- »

- Pharmaceuticals

- »

-

Specialty Generics Market Size & Share Report, 2026-2033GVR Report cover

![Specialty Generics Market (2026 - 2033)Report]()

Specialty Generics Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Injectables, Oral Drugs), By Indication (Oncology, Inflammatory conditions, Multiple sclerosis, Hepatitis C), By End Use, By Region, And Segment Forecasts

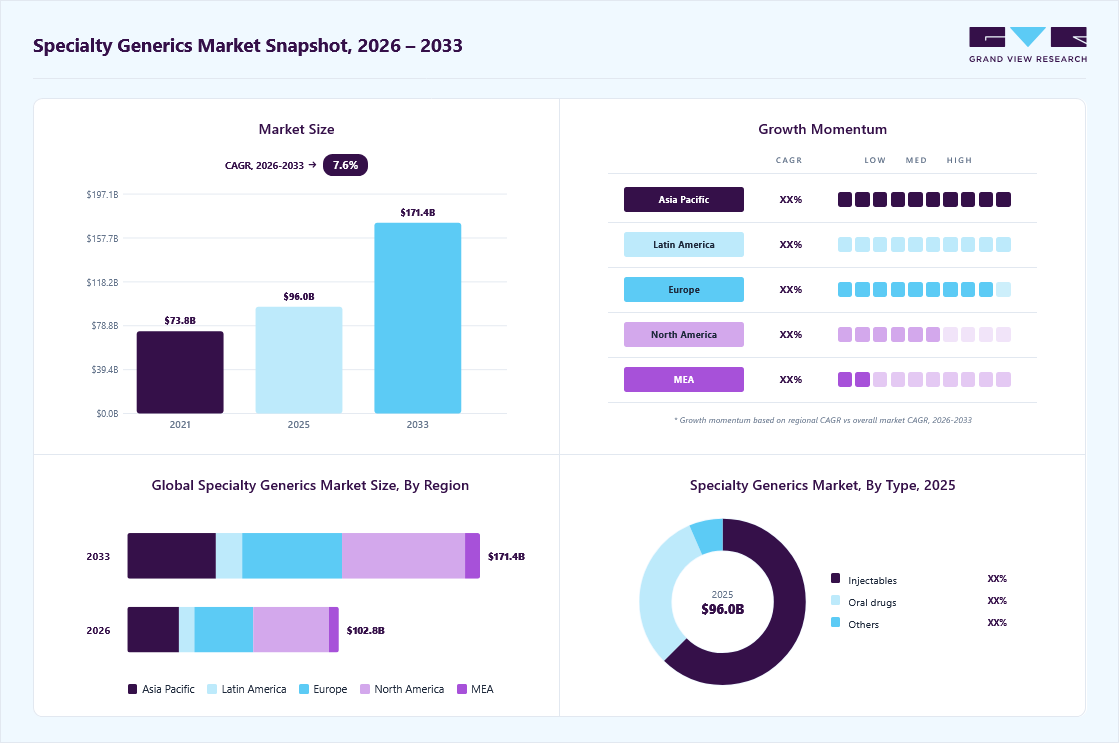

Market Size, 2025

$96.0BMarket Estimate, 2026

$102.8BMarket Forecast, 2033

$172.4BCAGR, 2026–2033

7.6%Specialty Generics Market Summary

The global specialty generics market size was valued at USD 96.0 billion in 2025 and is projected to grow from USD 102.8 billion in 2026 to USD 171.4 billion by 2033, at a CAGR of 7.6% from 2026 to 2033. North America dominated the market, accounting for a revenue share of 35.9% in 2025. The market is witnessing steady growth driven by the rising burden of chronic and rare diseases and the demand for cost-effective treatment alternatives.

Key Market Trends & Insights

- By type: The injectables segment held the largest market share of 62.4% in 2025.

- By indication:The inflammatory conditions segment held the largest market share in 2025.

- By end use: The specialty pharmacy segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (35.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (fastest CAGR, 2026-2033)

Market Size & Forecast

- Market size in 2025: USD 96.0 Billion

- Estimated market size in 2026: USD 102.8 Billion

- Projected market size by 2033: USD 171.4 Billion

- CAGR (2026-2033): 7.6%

These drugs play a crucial role in improving patient access to complex therapies, particularly in oncology, autoimmune disorders, and infectious diseases. Advancements in drug formulation technologies and regulatory support for generic approvals are further facilitating market expansion. Additionally, the growing focus on biosimilars and high-value injectable generics is reshaping the competitive landscape. As healthcare systems emphasize affordability and accessibility, specialty generics are emerging as a key component of sustainable pharmaceutical care.According to the World Health Organization (WHO), the global geriatric population is expanding rapidly, rising significantly in recent years, and is projected to reach a substantial share of the total population by 2030, with one in six individuals aged 60 years and above. This demographic shift is expected to create significant growth opportunities in the specialty generics market, as older populations are more prone to chronic and complex diseases that require long-term treatment. In addition, leading pharmaceutical companies are increasingly focusing on mergers, acquisitions, and strategic collaborations to strengthen their market presence and expand their specialty generics portfolios. Such initiatives are anticipated to support sustained market growth over the forecast period.

")

However, strong brand loyalty toward innovator drugs, the complex development and manufacturing requirements of specialty generics, and relatively lower profit margins act as significant entry barriers for new market participants. These challenges can contribute to limited competition and pricing pressures in certain segments. Furthermore, patient assistance programs and promotional strategies adopted by branded drug manufacturers often enhance patient retention for original products, thereby impacting the uptake and market penetration of specialty generic alternatives.

Market Characteristics

The specialty generics market demonstrates a moderate to high degree of innovation, driven by the need to replicate complex formulations and delivery mechanisms of branded drugs. Manufacturers are increasingly investing in advanced technologies, such as complex injectables, long-acting formulations, and drug-device combinations. Innovation is also evident in improving bioequivalence, stability, and patient compliance for specialty therapies. Additionally, the development of biosimilars and value-added generics is expanding the scope of innovation within the market. As competition intensifies, companies are focusing on differentiated products to gain a competitive edge.

The specialty generics industry is characterized by high entry barriers due to the complex nature of drug development, manufacturing, and regulatory approval processes. Significant capital investment is required for advanced production facilities, clinical studies, and compliance with stringent quality standards. Additionally, intellectual property challenges and the limited availability of technical expertise further restrict new entrants. Established players benefit from strong distribution networks and long-standing relationships with healthcare providers, making market penetration difficult. These factors collectively limit competition and create a concentrated competitive landscape.

Regulations play a critical role in shaping the market, as manufacturers must comply with stringent guidelines for quality, safety, and bioequivalence. Regulatory frameworks govern the approval of complex generics and biosimilars, often requiring extensive documentation and clinical validation. While supportive policies in certain regions help accelerate approvals and encourage competition, compliance requirements can increase development timelines and costs. Variations in regulatory standards across countries further add complexity for global market participants. Overall, regulations significantly influence market entry, product development, and commercialization strategies.

The specialty generics market faces competition from branded specialty drugs, biosimilars, and alternative therapeutic approaches. Branded products often maintain a strong market presence due to physician preference, perceived efficacy, and patient support programs. Biosimilars are emerging as key substitutes, particularly in biologics, offering relatively lower-cost alternatives with comparable outcomes. In some cases, non-pharmacological treatments or newer innovative therapies may also act as substitutes, depending on the area of disease. The availability and acceptance of these alternatives can influence the adoption and growth of specialty generic products.

The market is witnessing significant geographical expansion as companies target emerging markets with growing healthcare infrastructure and rising demand for affordable therapies. Regions in Asia-Pacific, Latin America, and the Middle East are becoming key growth areas due to increasing disease burden and improved access to treatment. Companies are establishing local manufacturing facilities and forming regional partnerships to strengthen their presence. Additionally, supportive government initiatives and regulatory harmonization in certain regions are facilitating market entry. This expansion strategy enables companies to diversify revenue streams and tap into underserved patient populations.

Type Insights

The Injectables segment dominated the specialty generics industry, accounting for the largest revenue share of 62.35% in 2025. This dominance is primarily driven by the advantages of injectable formulations, including rapid onset of action, higher bioavailability, and long-acting therapeutic effects, which enhance patient compliance, particularly in oncology and chronic disease management. The segment has also witnessed significant regulatory activity, with multiple first-time approvals of generic injectable products in 2025, including dalbavancin and cangrelor injections, expanding access to critical treatments. Recent developments further highlight innovation in this space, such as the approval in 2025 of subcutaneous injectable formulations of blockbuster therapies that reduce administration time and improve patient convenience. Moreover, the growing global burden of cancer and infectious diseases continues to drive demand for injectable therapies, reinforcing the segment’s strong growth trajectory. According to global health estimates published in 2024, cancer cases continue to rise significantly, increasing the need for effective injectable treatments. Additionally, advancements in sterile manufacturing technologies and the expansion of hospital-based care settings are further supporting the growth of this segment.

The oral drugs segment is projected to grow at a significant CAGR during the forecast period, driven by the launch of complex oral formulations that enhance patient adherence and expand treatment options for chronic conditions, as well as the increasing number of specialty drugs going off-patent, enabling generic entry. Oral specialty generics offer advantages in ease of administration, broad patient acceptance, and efficient distribution through retail and specialty pharmacies, supporting market expansion. Regulatory initiatives and accelerated ANDA approvals are encouraging manufacturers to invest in oral product pipelines targeting high-value therapeutic areas such as oncology, autoimmune disorders, and metabolic diseases. Growing collaborations between generic developers and strategic partners are enhancing formulation expertise and market reach. Additionally, rising healthcare cost pressures are making oral generics more attractive to payers and providers, boosting uptake. For instance, in March 2026, Natco Pharma, through its partner Breckenridge Pharmaceutical, Inc., launched Pomalidomide Capsules, a generic version of Pomalyst in the U.S., gaining market access in a branded segment valued at approximately USD 3.2 billion, highlighting the active expansion of specialty generics.

Indication Insights

The inflammatory conditions segment dominated the specialty generics market, accounting for the largest revenue share of 27.92% in 2025, attributed to the increasing adoption of specialty generics and biosimilars for chronic autoimmune diseases such as rheumatoid arthritis, psoriasis, and inflammatory bowel disease, where long-term therapy is essential. The segment is also benefiting from the growing shift toward biologic-based treatments and their cost-effective biosimilar alternatives, improving patient access and treatment adherence. According to the U.S. Food and Drug Administration, more than 60 biosimilars had been approved as of 2024, targeting multiple chronic conditions, including inflammatory diseases, highlighting strong pipeline expansion. For instance, in May 2025, the FDA approved ustekinumab-based biosimilars, such as Starjemza, for the treatment of plaque psoriasis, psoriatic arthritis, and Crohn’s disease, marking a significant expansion of affordable treatment options for inflammatory disorders. Furthermore, regulatory momentum continued in 2025, with multiple approvals and interchangeability designations for biosimilars, improving patient access and reducing treatment costs for patients with chronic inflammatory conditions. Additionally, the high economic burden of biologic therapies—accounting for over 50% of drug spending despite low prescription volume—continues to drive demand for specialty generics and biosimilars in this segment.

The oncology segment is expected to grow at the fastest CAGR over the forecast period, driven by the increasing shift toward cost-effective treatment alternatives as cancer therapies become more expensive and complex. Specialty generics play a crucial role in improving access to high-value oncology drugs, particularly in emerging markets where affordability remains a key concern. According to GLOBOCAN 2024 estimates, global cancer cases are projected to reach approximately 30 million by 2040, reflecting a substantial rise and reinforcing long-term demand for oncology treatments. Additionally, the expiration of patents for several blockbuster oncology drugs is creating opportunities for the introduction of generic versions, thereby expanding treatment accessibility. For instance, in June 2023, the U.S. FDA approved multiple generic versions of lenalidomide, a widely used therapy for multiple myeloma, significantly increasing patient access to this critical oncology drug. Such approvals highlight the growing pipeline of specialty oncology generics and the focus of manufacturers on complex therapeutic areas. Furthermore, advancements in targeted therapies and combination regimens are encouraging the development of more sophisticated generic alternatives. These factors collectively are expected to accelerate the segment growth.

End Use Insights

The specialty pharmacy segment accounted for the largest revenue share of 77.97% in 2025, attributed to the increasing reliance on specialty pharmacies for the distribution of high-cost and complex therapies, as they offer streamlined logistics, patient support programs, and efficient reimbursement handling. Specialty pharmacies enable manufacturers and insurers to reduce distribution inefficiencies while ensuring safe handling of temperature-sensitive and biologic drugs. Their ability to provide integrated services such as adherence monitoring and home delivery further enhances patient access and treatment continuity. Additionally, the growing complexity of specialty drugs has strengthened the preference for these dedicated channels across the healthcare ecosystem. For instance, in December 2025, MrMed partnered with Eli Lilly and launched a new cold-chain distribution hub in India to strengthen specialty medicine delivery and improve last-mile access to critical therapies, such as oncology and immunology drugs, highlighting the growing reliance on specialty pharmacy networks for efficient distribution.

The hospital pharmacy segment is projected to grow at a significant CAGR over the forecast period, supported by expanding hospital formularies, centralized procurement contracts, and the increasing use of complex generics in inpatient care. Hospital pharmacies benefit from volume-purchasing agreements and integrated clinical protocols that favor the adoption of specialty generics for oncology, autoimmune, and chronic conditions, thereby enhancing operational efficiency and cost‑effectiveness. Growth is further fueled by the increasing prevalence of chronic diseases and the need for affordable, high‑quality therapeutics within hospital systems. Regulatory support for generic approvals and hospital initiatives to improve medication access are also driving demand in this distribution channel. Additionally, investments in pharmacy infrastructure and technology are enabling quicker integration of complex generics into hospital workflows. For instance, in February 2026, Breckenridge Pharmaceutical, Inc. announced a strategic collaboration with Medichem Solutions S.L. to expand its injectable generic product offerings used across critical care and emergency medicine, underscoring active partnerships that enhance hospital pharmacy inventories and specialty generics accessibility.

Regional Insights

The North America specialty generics market held the largest share of 35.94% in 2025, due to the strong presence of leading generic drug manufacturers, a well-established regulatory framework, and high adoption of complex generics and biosimilars. The region benefits from robust healthcare infrastructure and favorable reimbursement systems, which support the uptake of cost-effective specialty therapies. Additionally, the increasing focus on reducing drug costs and improving access to high-value treatments is driving demand for specialty generics across the U.S. and Canada. The growing pipeline of Abbreviated New Drug Application (ANDA) approvals and patent expirations of blockbuster drugs further strengthen market expansion. For instance, in February 2025, the U.S. Food and Drug Administration approved Amneal Pharmaceuticals’ generic lenalidomide capsules for multiple strengths, with commercialization planned from 2026, expanding access to a key oncology therapy in the U.S. Furthermore, in 2024, the FDA approved multiple complex generics, including injectable and specialty drugs, indicating a strong regulatory push toward increasing generic availability in the region. These developments highlight North America’s leadership in specialty generics innovation and commercialization, contributing significantly to overall market growth.

U.S. Specialty Generics Market Trends

The U.S. specialty generics industry’s growth is driven by the strong presence of established pharmaceutical manufacturers and a highly structured regulatory environment that supports the approval of complex generics and biosimilars. The country continues to witness increasing adoption of specialty generics as healthcare systems focus on reducing treatment costs while maintaining clinical effectiveness. Growth is further supported by the rising number of patent expirations of high-value specialty drugs, creating opportunities for generic competition. Additionally, the expansion of specialty pharmacy networks and improved reimbursement frameworks are enhancing patient access to advanced therapies. Technological advancements in drug delivery systems and formulation capabilities are also contributing to market expansion. Overall, the U.S. remains a key hub for innovation and commercialization in the specialty generics space.

Europe Specialty Generics Market Trends

Europe held a significant share of the specialty generic industry, driven by strong government initiatives promoting the use of generic medicines to control escalating healthcare expenditures. The region benefits from centralized regulatory pathways and well-established pricing and reimbursement policies that encourage generic substitution. Increasing emphasis on sustainable healthcare systems and cost-containment strategies is accelerating the adoption of specialty generics across key countries such as Germany, France, and the UK. Additionally, the presence of a mature pharmaceutical manufacturing base supports the development and supply of complex generics. The rising focus on biosimilar uptake, supported by physician awareness and policy incentives, is further strengthening market growth. Overall, Europe continues to lead in the widespread integration of specialty generics into routine clinical practice.

The UK specialty generics market is experiencing steady growth, driven by strong government support for cost-effective medicines and increasing adoption of biosimilars within the National Health Service (NHS). A key growth driver is the high penetration of generic and biosimilar medicines, which account for nearly 85% of NHS prescriptions, significantly improving patient access while reducing healthcare costs. Additionally, regulatory agility from the Medicines and Healthcare Products Regulatory Agency (MHRA) is facilitating faster approvals and market entry for complex generics. The country is also witnessing increased focus on supply chain resilience and domestic manufacturing capabilities to ensure consistent drug availability. For instance, in May 2023, the biosimilar ranibizumab (Ximluci), developed by STADA and Xbrane, was made available through the UK NHS, expanding access to cost-effective ophthalmology treatments and supporting wider adoption of specialty generics in the country.

The specialty generics market in Germany is witnessing steady growth, supported by strong pricing and reimbursement frameworks that promote the use of cost-effective medicines. A key growth driver is the country’s structured biosimilar substitution policies, which encourage pharmacies to dispense the most economical alternatives, thereby accelerating generic uptake. Additionally, Germany’s well-established healthcare system and high pharmaceutical expenditure are driving sustained demand for affordable specialty therapies. The market is further benefiting from a robust pipeline of complex generics and biosimilars, particularly in oncology and immunology segments. For instance, in September 2024, STADA Arzneimittel reported a 14% growth in its specialty segment, driven by the expansion of its biosimilars portfolio and new product launches across Europe, including Germany. This reflects the increasing adoption of specialty generics and biosimilars in the country, supported by favorable regulatory policies and strong market demand.

The France specialty generics market is experiencing steady growth, supported by the country’s strong pharmaceutical manufacturing base and increasing focus on complex drug formulations. A key growth driver is the rising demand for cost-effective alternatives to high-priced specialty medicines, particularly in the treatment of chronic and rare diseases. France’s emphasis on healthcare cost containment and generic substitution policies is further encouraging the adoption of specialty generics. Additionally, the growing use of biosimilars across therapeutic areas such as oncology and immunology is strengthening market expansion. For instance, in September 2025, Sanofi highlighted expansion in its pharmaceutical production capabilities in France, supporting increased drug manufacturing output and reinforcing the demand for specialty generics. Furthermore, increasing collaborations between domestic manufacturers and global pharmaceutical companies are enhancing product availability and technological capabilities. The continued focus on improving patient access to advanced therapies is expected to further drive market growth in the coming years.

Asia Pacific Specialty Generics Market Trends

The Asia Pacific specialty generics industry is expected to grow at the fastest CAGR during the forecast period, driven by expanding healthcare access and strong government initiatives promoting the use of cost-effective medicines across countries such as India, China, Japan, and South Korea. A key growth driver is the increasing adoption of biosimilars, supported by favorable regulatory frameworks and rising investments in biopharmaceutical manufacturing capabilities across the region. Governments are actively encouraging local production and reducing dependency on imports, further strengthening market expansion. The growing burden of chronic diseases and the region’s large patient population are accelerating demand for affordable specialty therapies, particularly in oncology, autoimmune disorders, and diabetes care. Additionally, improving awareness among healthcare providers and patients about the efficacy and safety of specialty generics supports greater adoption. Furthermore, increasing collaborations between regional pharmaceutical companies and global players are facilitating technology transfer and enhancing product pipelines. The rapid expansion of hospital infrastructure and specialty care centers across emerging economies is also contributing to improved access and distribution of specialty generic drugs.

The specialty generics market in Japan is experiencing steady growth, driven by government policies aimed at controlling healthcare costs and promoting the use of generic and biosimilar medicines. A key growth driver is the increasing adoption of biosimilars in oncology and autoimmune therapies, supported by incentives for hospitals and pharmacies to prescribe cost-effective alternatives. Additionally, Japan’s aging population and rising prevalence of chronic diseases are creating sustained demand for specialty generics, particularly in areas such as cardiovascular, metabolic, and neurological disorders. The country’s well-established regulatory framework and strong domestic manufacturing capabilities further facilitate the development and commercialization of complex generics.

Moreover, ongoing collaborations between Japanese pharmaceutical companies and global specialty drug developers are fostering innovation and enabling faster access to advanced generic formulations, enhancing patient outcomes and market penetration.

The China specialty generics market is witnessing rapid growth, driven by government initiatives to improve access to affordable medicines and reduce healthcare expenditure. A key growth driver is the implementation of the centralized “Volume-Based Procurement” policy, which encourages the adoption of cost-effective specialty generics in hospitals and public healthcare facilities. Additionally, the rising prevalence of chronic diseases, cancer, and rare disorders is fueling demand for high-value generic therapies. China’s expanding pharmaceutical manufacturing capabilities and growing focus on biosimilars and complex generics are further supporting market growth. Increased awareness among healthcare providers and patients regarding the efficacy of specialty generics is also enhancing adoption rates. For instance, in October 2025, Hansoh Pharmaceutical Group launched a generic version of lenalidomide in China, offering a cost-effective treatment option for multiple myeloma patients and expanding access to essential oncology therapies.

Latin America Specialty Generics Market Trends

The Latin America specialty generics industry is experiencing steady growth, driven by increasing healthcare expenditure and the expansion of public and private insurance coverage across countries such as Brazil, Mexico, and Argentina. A key growth driver is the rising demand for affordable alternatives to high-cost specialty medicines, particularly in the management of chronic and complex diseases. Additionally, regional initiatives to strengthen local pharmaceutical manufacturing capabilities and reduce dependence on imported branded drugs are supporting market expansion. The growing prevalence of non-communicable diseases, coupled with improved awareness among healthcare providers and patients about generic alternatives, is further boosting adoption. Increasing investments in cold-chain logistics and specialty pharmacy networks are also enhancing accessibility and distribution efficiency. Overall, these factors are contributing to sustained market growth.

The Brazil specialty generics market is witnessing significant growth, driven by increasing government initiatives to expand access to affordable medicines and the growing prevalence of chronic and complex diseases. A key growth driver is the country’s national policy promoting the use of generics and biosimilars within public healthcare programs, which encourages broader adoption of cost-effective therapies. Additionally, expanding specialty pharmacy networks and improved distribution infrastructure are facilitating patient access to high-value medications. Rising awareness among healthcare providers and patients regarding the efficacy and safety of specialty generics is further supporting market penetration. For instance, in June 2024, Eurofarma Laboratórios launched a generic version of trastuzumab in Brazil, enhancing access to oncology treatments and strengthening the specialty generics segment in the country.

Middle East & Africa Specialty Generics Market Trends

The Middle East & Africa specialty generics industry is experiencing steady growth, driven by increasing healthcare spending and expanding access to modern healthcare facilities across key countries such as Saudi Arabia, the UAE, and South Africa. A key growth driver is the rising government focus on cost containment and the adoption of generic substitution policies to make high-value specialty therapies more affordable. Additionally, the growing prevalence of chronic and lifestyle-related diseases is increasing demand for long-term, cost-effective treatments. The expansion of specialty pharmacy networks and improvements in cold-chain logistics are enhancing drug availability and patient access. Regional partnerships between domestic manufacturers and international pharmaceutical companies are strengthening the supply chain and technology transfer. Overall, these factors are creating favorable conditions for the sustained regional market growth.

The Saudi Arabia specialty generics market is witnessing strong growth, driven by government initiatives to expand access to affordable medicines and reduce the economic burden of high‑cost specialty therapies. A key growth driver is the increasing regulatory support for generic versions of complex and high‑value drugs, enabling wider availability through public and private healthcare channels. Additionally, the rising prevalence of chronic conditions such as diabetes and cardiovascular diseases is boosting demand for cost‑effective treatment options. Expansion of pharmaceutical distribution infrastructure and specialty pharmacy networks is further enhancing patient access across the Kingdom. The market is also supported by efforts to localize drug manufacturing under Saudi Vision 2030, improving self‑sufficiency in pharmaceutical supply. For instance, in February 2026, OneSource Specialty Pharmacy received approval from the Saudi Food and Drug Authority (SFDA) to commercialize its generic version of semaglutide (Ozempic) in Saudi Arabia through a partnership with Hikma Pharmaceuticals PLC, expanding access to an affordable complex therapy in the region.

Key Specialty Generics Company Insights

Teva Pharmaceutical Industries Ltd.; Viatris Inc.; Novartis AG (Sandoz); Hikma Pharmaceuticals PLC; Mallinckrodt; Dr. Reddy’s Laboratories Ltd.; Endo Pharmaceuticals Inc.; Apotex Corp.; Sun Pharmaceutical Industries Ltd.; and Bausch Health Companies Inc. are the key players shaping the specialty generics market. These companies focus on complex formulations, biosimilars, and advanced drug delivery systems to enhance efficacy and patient adherence. Teva and Viatris lead in complex generics, while Novartis drives biosimilars innovation. Hikma and Mallinckrodt emphasize injectables, and Dr. Reddy’s and Endo advance controlled-release technologies. Apotex promotes sustainable excipients, Sun Pharma strengthens scalability, and Bausch Health expands specialty portfolios. Collectively, they drive innovation, accessibility, and competitive growth.

Key Specialty Generics Companies:

The following key companies have been profiled for this study on the specialty generics market.

- Teva Pharmaceuticals Industries Ltd

- Viatris Inc.

- Novartis AG (Sandoz International GmbH)

- Hikma Pharmaceuticals PLC

- Mallinckrodt

- Bausch Health Companies Inc. (Valeant Pharmaceuticals International, Inc.)

- Dr. Reddy’s Laboratories Ltd.

- Endo Pharmaceuticals Inc.

- Apotex Corp.

- Sun Pharmaceutical Industries Ltd

Recent Developments

-

In March 2026, Teva Pharmaceutical Industries Ltd. and funds managed by Blackstone Life Sciences announced they entered into a USD 400 million strategic growth capital agreement to support the continued clinical development of duvakitug, a human monoclonal antibody targeting TL1A that is currently in Phase 3 clinical trials for ulcerative colitis and Crohn’s disease. The funding will be provided over approximately four years and includes potential regulatory and commercial milestone payments and low single‑digit royalties on worldwide sales.

-

In November 2025, Hikma Pharmaceuticals PLC launched STARJEMZA in the US, a biosimilar to STELARA, significantly broadening its specialty injectable portfolio and enhancing access to complex biologic generics for immune‑mediated diseases.

-

In April 2025, Hikma Pharmaceuticals PLC acquired the FDA‑approved ANDA for trametinib tablets from Novugen and secured the U.S. commercial rights, enabling Hikma to launch an oncology specialty generic with 180‑day exclusivity, expanding its complex generics pipeline in cancer treatments.

Specialty Generics Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 102.77 billion

Revenue forecast in 2033

USD 171.36 billion

Growth rate

CAGR of 7.58% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, trends

Segments covered

Type, indication, end use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key company profiled

Teva Pharmaceuticals Industries Ltd; Viatris Inc.; Novartis AG (Sandoz International GmbH); Hikma Pharmaceuticals PLC; Mallinckrodt; Bausch Health Companies Inc. (Valeant Pharmaceuticals International, Inc.); Dr. Reddy’s Laboratories Ltd.; Endo Pharmaceuticals Inc.; Apotex Corp.; Sun Pharmaceutical Industries Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Specialty Generics Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global specialty generics market report based on type, indication, end use, and region:

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Injectables

-

Oral drugs

-

Others

-

-

Indication Outlook (Revenue, USD Billion, 2021 - 2033)

-

Oncology

-

Inflammatory conditions

-

Multiple sclerosis

-

Hepatitis C

-

Others

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Specialty pharmacy

-

Retail pharmacy

-

Hospital pharmacy

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

Based on type, the injectables segment dominated the market with the largest revenue share of 62.35% in 2025, driven by the increasing demand for complex injectable therapies in oncology, autoimmune disorders, and infectious diseases. The segment’s growth is further supported by advancements in sterile manufacturing technologies, higher bioavailability, and rising approvals for specialty injectable generics.

Key players operating in the market are Teva Pharmaceutical Industries Ltd., Viatris Inc., Novartis AG (Sandoz International GmbH), Hikma Pharmaceuticals PLC, Mallinckrodt, Bausch Health Companies Inc., Dr. Reddy’s Laboratories Ltd., Endo Pharmaceuticals Inc., Apotex Corp., and Sun Pharmaceutical Industries Ltd.

The global specialty generics market size was estimated at USD 95.98 billion in 2025 and is expected to reach USD 102.77 billion in 2026.

The global specialty generics market is expected to grow at a compound annual growth rate (CAGR) of 7.58% from 2026 to 2033 to reach USD 171.36 billion by 2033.

Key factors driving market growth include the increasing prevalence of chronic and rare diseases, rising demand for affordable alternatives to branded specialty drugs, and growing adoption of biosimilars and complex generics. Advancements in drug formulation technologies, increasing patent expirations of blockbuster drugs, and supportive regulatory frameworks for generic approvals are also contributing to market expansion.

About the Author(s)

Pharmaceuticals Research Team

Healthcare · PharmaceuticalsThis report was authored by the pharmaceuticals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the pharmaceuticals segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.