- Home

- »

- Advanced Interior Materials

- »

-

Tungsten Market Size, Share & Growth Report, 2026-2033GVR Report cover

![Tungsten Market (2026 - 2033)Report]()

Tungsten Market (2026 - 2033)

Size, Share & Trends Analysis Report By Form (Powder, Mill Products, Tungsten Carbide Components), By End Use (Aerospace & Defense, Construction, Others), By Region, And Segment Forecasts

Market Size, 2025

$2.0BMarket Estimate, 2026

$2.1BMarket Forecast, 2033

$2.8BCAGR, 2026–2033

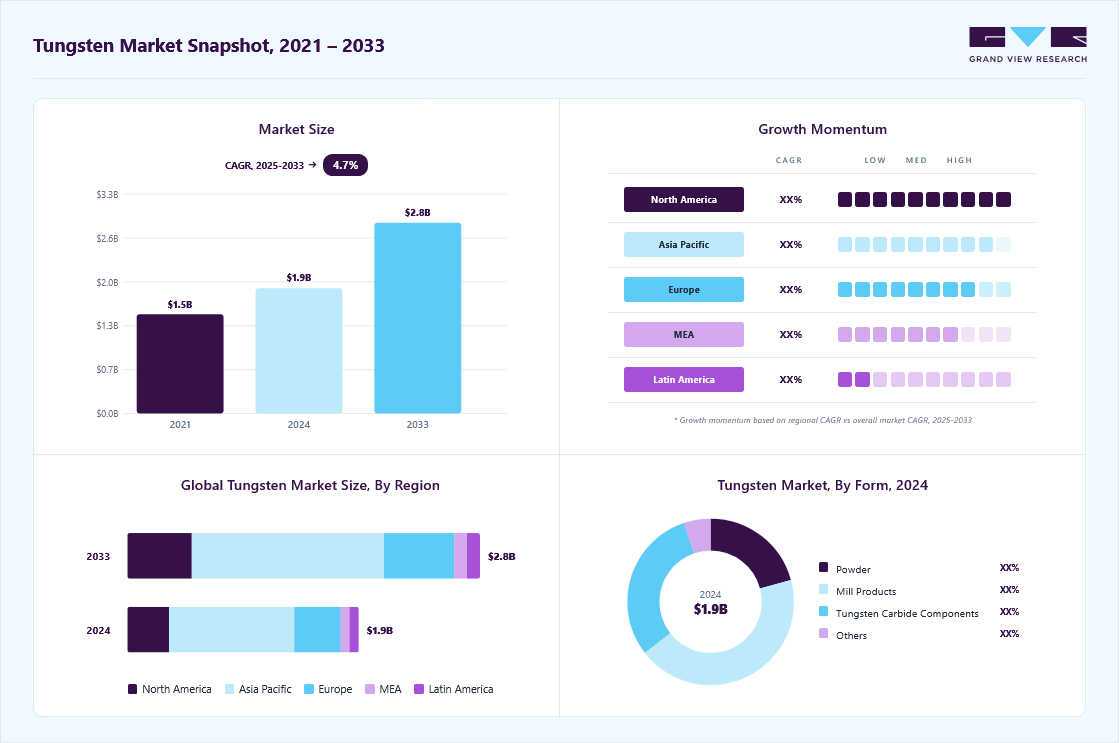

4.7%Tungsten Market Summary

The tungsten market size was valued at USD 2.0 billion in 2025 and is projected to grow from USD 2.1 billion in 2026 to USD 2.8 billion by 2033, growing at a CAGR of 4.7% from 2026 to 2033. Asia Pacific dominated the market with the largest revenue share of 54.2% in 2025. The strong growth is largely driven by the critical use of tungsten in hard metals and tooling applications.

Key Market Trends & Insights

- By form: Mill products segment led the market with the largest revenue share of 43.1% in 2025.

- By end use: Automotive segment led the market with the largest revenue share of 25.5% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (54.2%% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 2.0 Billion

- Estimated market size in 2026: USD 2.1 Billion

- Projected market size by 2033: USD 2.8 Billion

- CAGR (2026-2033): 4.7%

Tungsten carbide, a compound made by combining tungsten with carbon, is one of the hardest known materials and is widely used in manufacturing cutting tools, drill bits, mining equipment, and industrial machinery. These tools are essential in the automotive, aerospace, construction, and general manufacturing sectors.")

Its superior density, hardness, and high melting point make tungsten indispensable in the defense and aerospace sectors. In 2024, increased global defense spending, particularly by the U.S., China, and India, amplified the demand for tungsten-based armor-piercing projectiles, missile components, and aircraft counterweights. For instance, India's Ministry of Defence allocated higher funds for indigenous ammunition production, which includes tungsten carbide-based penetrators. Similarly, the aerospace sector in 2025 saw a surge in aircraft manufacturing, with Boeing and Airbus increasing deliveries, further boosting demand for tungsten alloys in control surfaces, engine components, and balance weights.

In the automotive industry, especially in high-performance and electric vehicles, tungsten usage is expanding due to its exceptional thermal and wear resistance. In 2024, global electric vehicle (EV) production reached 17.3 million units, marking a 25% increase compared to the previous year. China remained dominant, accounting for over 70% of global EV production, with around 12.4 million electric cars manufactured. This surge significantly boosted the need for tungsten-based components such as electrodes for precision welding, electrical contacts, and vibration-damping parts. Notably, Tesla expanded its use of tungsten alloys in motor assemblies and battery connectors. In 2025, luxury and performance vehicle manufacturers, including Porsche, BMW, and NIO, further integrated tungsten-heavy materials into brake systems and turbochargers to meet the growing demand for high-performance EVs across Europe and East Asia.

Tungsten is also vital for manufacturing drill bits, wear parts, and cutting tools used in mining and oil & gas exploration. In 2024, with oil prices stabilizing and exploration activities picking up, tungsten carbide tools saw a revival in demand, especially in North America and the Middle East. For example, Saudi Aramco's intensified deep drilling activities relied on advanced tungsten-based tools to withstand extreme temperatures and pressures. In 2025, the mineral exploration boom in South America, particularly for lithium and copper, further lifted demand for these durable tools used in rock fragmentation and ore extraction.

Carbide tools dominate the cutting tools industry due to their superior hardness and wear resistance. The resurgence of industrial manufacturing in 2024, especially in countries like China, Germany, and Vietnam, spurred tooling demand. For instance, China's push toward advanced manufacturing under its "Made in China 2025" policy led to increased consumption of tungsten-based inserts and end mills. In 2025, additive manufacturing also began using tungsten powders for precision components, further diversifying applications and adding a new growth dimension to the market.

Market Dynamics

The growth of the tungsten market is primarily driven by the rising demand for tungsten carbide in industrial machining, mining, construction, and manufacturing applications. Tungsten carbide is widely used in cutting tools, drill bits, wear-resistant components, and metalworking equipment due to its exceptional hardness, durability, and high-temperature resistance. As industrial production and infrastructure development continue to expand across emerging economies, manufacturers are increasingly adopting tungsten-based tools to improve operational efficiency, precision, and equipment lifespan. The growing emphasis on automation and advanced manufacturing technologies is further accelerating tungsten consumption across industrial sectors.

The aerospace and defense industry is a significant driver of tungsten demand due to the metal's exceptional density, high melting point, strength, and resistance to extreme temperatures. Tungsten is extensively used in aircraft engine components, turbine blades, counterweights, radiation shielding systems, missile parts, kinetic energy penetrators, and aerospace tooling. As commercial aviation continues to recover and defense modernization programs accelerate globally, manufacturers are increasing production of next-generation aircraft and military equipment, creating sustained demand for tungsten-based materials. The growing focus on fuel-efficient aircraft and advanced defense technologies further strengthens the need for high-performance metals capable of operating under severe conditions.

The high production and processing costs of tungsten products act as a key restraint on market growth. Tungsten extraction involves complex mining, beneficiation, and refining processes due to its low concentration in most ores and its exceptionally high melting point. The production of high-purity tungsten powders, tungsten carbide, and specialized alloys requires significant energy consumption, advanced processing technologies, and stringent quality control measures, thereby elevating manufacturing costs. In addition, rising energy prices, labor costs, and environmental compliance expenses further increase producers' overall cost structure. These factors can limit the adoption of tungsten-based materials in price-sensitive industries, encouraging some end users to consider lower-cost alternatives where performance requirements permit.

Tungsten is widely used in semiconductor devices for interconnects, contacts, vias, and thin film applications due to its excellent electrical conductivity, thermal stability, and resistance to electromigration. The rapid expansion of semiconductor fabrication facilities across regions such as North America, Europe, and Asia Pacific, supported by government incentives and private sector investments, is driving demand for high purity tungsten materials. Furthermore, the increasing production of advanced consumer electronics, artificial intelligence hardware, data center equipment, 5G infrastructure, and automotive electronics is expected to strengthen tungsten consumption. As chip manufacturers continue to develop smaller and more powerful semiconductor nodes, the need for high performance materials such as tungsten is anticipated to create substantial growth opportunities for market participants.

Analyst Perspective

The tungsten market is poised for steady growth due to its critical role in high-performance industrial applications, particularly across the automotive, aerospace & defense, mining, electronics, and advanced manufacturing sectors. Tungsten's unique combination of exceptional hardness, high density, superior wear resistance, and the highest melting point among all metals makes it an irreplaceable material in cutting tools, drilling equipment, semiconductors, and defense systems. Rising global manufacturing activity, increasing electric vehicle production, expanding aerospace programs, and growing investments in semiconductor fabrication are expected to support long-term demand growth.

Form Insights

Based on form, mill products segment led the market with the largest revenue share of 43.1% in 2025. The segment is witnessing steady growth due to its essential role in high-performance industrial and engineering applications. Mill products refer to semi-finished tungsten materials like rods, bars, plates, sheets, wires, and electrodes, which are widely used across industries for their high strength, durability, and heat resistance. These products are especially important in aerospace, electronics, automotive, and oil & gas sectors, where components are exposed to extreme conditions. The ability of tungsten to retain its strength at high temperatures and its excellent thermal conductivity make mill products highly valuable for tools, structural parts, and heat-resistant components.

Tungsten carbide components is anticipated to register the fastest CAGR over the forecast period. Tungsten carbide components are experiencing strong market growth primarily due to their unmatched hardness, wear resistance, and durability. These components are widely used in industries that involve abrasive environments or high-stress operations, such as mining, oil & gas, metalworking, and construction. Products like drill bits, cutting tools, nozzles, and wear plates made from tungsten carbide significantly outperform traditional steel-based tools in terms of lifespan and performance. As industrial operations become more demanding and efficiency-focused, the shift toward tungsten carbide components becomes more apparent, driving the segment’s steady expansion across global markets.

End Use Insights

Based on end use, automotive segment led the market with the largest revenue share of 25.5% in 2025. It is a major end use industry for tungsten, driven by the metal’s superior properties such as high density, hardness, heat resistance, and wear durability. Tungsten-based products, particularly tungsten carbide components, are integral to automotive manufacturing processes, especially for tools used in machining, cutting, and shaping vehicle parts. As global vehicle production continues to rise steadily, particularly in emerging economies like India, Mexico, and Indonesia, the demand for tungsten tooling and parts used in engine components, transmission systems, and turbochargers has significantly increased. The push for improved vehicle performance and durability further enhances tungsten’s relevance in this sector.

The electronics & robotics segment is anticipated to register the fastest CAGR over the forecast period. Tungsten is employed in smartphones, laptops, tablets, and display panels in consumer electronics. For instance, tungsten is a key material in electrodes for LCDs and OLEDs and in X-ray targets for imaging devices. The proliferation of smart devices and increasing Internet of Things (IoT) penetration drive demand for more robust and compact electronic components, further accelerating the need for tungsten-based materials. With over 1.4 billion smartphones shipped globally in 2024, the rising production volume continues to fuel demand for high-performance materials like tungsten that support heat management and miniaturization.

Regional Insights

Asia Pacific dominated the tungsten market with the largest revenue share of 54.2% in 2025. The tungsten market in the China held the largest share in the Asia Pacific region in 2025. Ongoing infrastructure development and smart city projects primarily drive the growth. As urbanization accelerates across emerging economies such as India, Vietnam, and Indonesia, substantial investments are being made in roads, bridges, railways, and smart urban infrastructure. These developments require durable, high-performance materials, and tungsten, known for its exceptional hardness and high melting point, is increasingly used in construction tools, electrical systems, and structural applications supporting these transformative projects.

North America Tungsten Market Trends

The North America tungsten industry experienced substantial growth. With the increasing shift towards electric vehicles in the region, the demand for tungsten is also increasing. In 2024, the U.S. electric vehicle market continued its upward trajectory, with EVs (battery electric vehicles and plug-in hybrids combined) accounting for approximately 8.1% to 9.9% of all new light-duty vehicle sales, up from 7.8% in 2023. According to the U.S. Department of Energy and Argonne National Laboratory, over 1.3 million EVs were sold yearly, with BEVs representing the majority. The U.S. and Canadian governments are offering incentives to boost EV production and adoption, directly supporting the market growth. As vehicle production increases, so will the need for reliable, high-performance materials like tungsten.

U.S. Tungsten Market Trends

The U.S. tungsten industry is witnessing robust growth, largely driven by rising concerns over national security and supply chain vulnerabilities. The country has relied heavily on China for its tungsten needs for years, as China dominates global production. However, the Biden administration's recent geopolitical tensions and the 25% tariff on Chinese tungsten imports have accelerated the U.S. government's efforts to diversify sources and reduce this dependence. Measures such as the Department of Defense's plan to phase out procurement of Chinese and Russian tungsten by 2027 and support for allied mining operations in Canada and South Korea reflect a shift toward ensuring a more secure and independent supply chain. These policy changes are directly boosting demand for domestic and allied tungsten sources.

Europe Tungsten Market Trends

The tungsten industry in Europe is witnessing steady growth due to the continent's increased focus on securing critical raw materials. Tungsten has been classified as a strategic material by the European Union because of its importance in various industries and the risks associated with import dependency, especially from China, which dominates global production. To reduce this reliance, the EU supports domestic mining projects and streamlines regulations to promote local production. For example, efforts to revive tungsten mining in countries like the UK, Spain, and Austria reflect this policy shift. These initiatives are expected to increase Europe's self-sufficiency and stabilize the tungsten supply.

Latin America Tungsten Market Trends

The Latin America tungsten industry is anticipated to grow significantly over the forecasted period. As economies like Brazil and Mexico recover from recent downturns and invest in infrastructure development, the need for wear-resistant tools, high-strength alloys, and drilling components is surging, sectors where tungsten plays a critical role. Additionally, the shift toward energy transition and renewable projects, particularly geothermal and wind energy, is increasing the use of tungsten-based components due to their high temperature and corrosion resistance. Combined with a growing focus on industrial self-reliance, these trends are expected to drive robust growth of the regional market.

Middle East & Africa Tungsten Market Trends

The tungsten industry in Middle East & Africa (MEA) is witnessing growth primarily due to increasing infrastructure development, industrial diversification, and mining sector investments across key countries such as South Africa, Saudi Arabia, and the UAE. With its established mining base, South Africa is exploring opportunities to expand into strategic and rare metals, including tungsten, to support domestic use and export potential. Meanwhile, the Gulf countries are rapidly diversifying their economies under national transformation plans (such as Saudi Arabia’s Vision 2030), boosting demand for high-performance materials in defense, oil & gas, and heavy manufacturing sectors, key end use areas for tungsten-based products.

Key Tungsten Company Insights

Some of the key players operating in the market include China Minmetals Corporation and Kennametal Inc.

-

China Minmetals Corporation is a major Chinese state-owned enterprise founded in 1950 and headquartered in Beijing. Directly controlled by the State Council’s SASAC, it has grown into a global metals and minerals powerhouse in over 30 countries, with 38 mines (15 overseas). In the metals and minerals segment, China Minmetals is a world leader in tungsten, owning some of the largest tungsten reserves globally. Its diversified portfolio covers non-ferrous and ferrous metals, copper, nickel, zinc, iron, antimony, molybdenum, tungsten, chromium, manganese, and more, accounting for roughly 70% of China’s strategic mineral catalogue.

-

Kennametal Inc. is a U.S.-based global manufacturing company that produces advanced tooling and industrial materials. Its key products include metal-cutting tools, wear-resistant components, ceramics, and coatings, which are sold under its core brand, as well as WIDIA and Stellite. Kennametal is also recognized for its commitment to innovation and sustainability, often receiving industry recognition for ethical practices, worker safety, and product development.

Key Tungsten Companies:

The following key companies have been profiled for this study on the tungsten market.

-

China Minmetals Corporation

-

Cleveland Tungsten, Inc.

-

Almonty Industries Inc.

-

TUNGSTEN WEST

-

Kennametal Inc.

-

Sandvik AB

-

Element Six UK Ltd.

-

Buffalo Tungsten Inc.

-

BETEK GMBH & CO. KG

-

EQ Resources Limited

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (e.g. Almatis, Inc., Baikowski, CoorsTek Inc.)

- Mature participants in the tungsten market primarily focus on securing long term access to tungsten concentrates, expanding downstream processing capabilities, and maintaining strong positions across the value chain from mining to tungsten carbide and specialty alloys.

- These companies emphasize vertical integration to ensure supply security and reduce exposure to raw material price volatility.

- Established players possess significant competitive advantages through their integrated supply chains, advanced processing expertise, and extensive production capacities.

- Their control over mining, refining, and downstream manufacturing operations enables greater cost efficiency, stable supply, and consistent product quality.

- Despite their strong market positions, mature players face challenges related to high capital intensity and dependence on the availability of tungsten ores and concentrates.

- Mining and processing operations require substantial investments in extraction equipment, refining facilities, and environmental management systems.

Emerging & Regional Players (e.g., Altech Chemicals Ltd., Alpha HPA)

- Emerging participants in the tungsten market generally focus on developing new mining projects, advancing resource exploration activities, and establishing alternative supply chains.

- Their strategies emphasize securing resource ownership, attracting strategic investments, and targeting regions seeking greater supply diversification.

- Emerging companies benefit from operational flexibility and the ability to implement modern mining and processing technologies from the beginning of project development.

- Without extensive legacy infrastructure, they can design operations around current efficiency, sustainability, and regulatory requirements.

- Emerging participants face significant challenges related to financing, project development timelines, and commercialization risks.

- Developing tungsten mining and processing operations requires substantial capital investment, extensive permitting activities, and technical validation before commercial production can begin.

Recent Development

-

In November 2024, Kazakhstan inaugurated its first tungsten processing plant in the Almaty Region, marking a significant advancement for the country's mining industry and enhancing its role in the global rare earth metals market. The USD 300 million facility is expected to create up to 1,000 jobs for local specialists. At full capacity, it will process 3.3 million tons of ore annually, producing tungsten concentrate with a purity of 65%.

Tungsten Market Report Scope

Report Attribute

Details

Market definition

The tungsten market represents the apparent consumption of tungsten-based materials in tungsten powder, mill products, and tungsten carbide components.

Market size in 2025

USD 2.0 billion

Estimated market size in 2026

USD 2.1 billion

Projected market size by 2033

USD 2.8 billion

Growth rate

CAGR of 4.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Form, end use, and region.

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S., Canada, Mexico, Germany, UK, France, Italy, Spain, India, China, Japan, South Korea, Brazil, Saudi Arabia, UAE

Key companies profiled

Almatis, Inc., Altech Chemicals Ltd., Alpha HPA, Baikowski, CoorsTek Inc., FYI Resources, Honghe Chemical, Nippon Light Metal Holdings Co., Ltd., Orbite Technologies Inc., Polar Sapphire Ltd., Sumitomo Chemical Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Tungsten Market Report Segmentation

This report forecasts revenue and volume growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global tungsten market report based on form, end use, and region:

-

Form Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Powder

-

Mill Products

-

Tungsten Carbide Components

-

Others

-

-

End Use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Aerospace & Defense

-

Construction

-

Automotive

-

Mining & Energy

-

Electronics & Robots

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Italy

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Research Methodology

The tungsten market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each tungsten segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Form

Revenue Capture Definition

Powder

This segment includes raw tungsten powder obtained through reduction processes, which serves as the base material for further manufacturing. It is widely used in powder metallurgy, additive manufacturing (3D printing), and alloy production. The powder’s purity and particle size are critical in end-use performance. It acts as a feedstock for sintering into various solid forms.

Mill Products

Mill products refer to semi-finished or finished tungsten items such as rods, bars, wires, foils, plates, tubes, and ribbons. These are typically fabricated from pure or tungsten alloys and used in electronics, aerospace, furnace components, and medical applications. The segment focuses on high-density, corrosion-resistant, and heat-resistant attributes of tungsten. They often undergo forging, rolling, or extrusion.

Tungsten Carbide Components

This segment comprises tungsten carbide (WC)-based products like inserts, dies, drill bits, wear-resistant parts, and cutting tips. These cemented carbide tools are widely utilized in mining, oil & gas, automotive, and metalworking industries due to their extreme hardness and durability.

Others

This category includes non-standard or specialty tungsten forms such as granules, precision balls, pellets, and ballast weights. These forms are used in niche applications including aerospace counterweights, radiation shielding, vibration dampening, and military-grade products.

End Use

Revenue Capture Definition

Aerospace & Defense

The aerospace and defense segment utilizes tungsten primarily for its high density, strength, and heat resistance. Applications include counterweights in aircraft, radiation shielding, kinetic energy penetrators in ammunition, rocket nozzles, and high-temperature structural parts.

Construction

In the construction industry, tungsten is used in the manufacturing of high-performance tools, such as drill bits, cutting tools, and saw blades. These tools, often made with tungsten carbide, provide superior wear resistance and hardness, essential for cutting, drilling, and mining operations in building projects.

Automotive

The automotive segment employs tungsten for both structural and functional components. It is commonly found in engine components, crankshaft weights, electrical contacts, and as part of tungsten carbide tools used to produce vehicle parts.

Mining & Energy

Tungsten plays a critical role in the mining and energy industries due to its durability and resistance to abrasion. It is widely used in mining drills, boring tools, wear parts, and energy exploration equipment, especially in harsh geological environments.

Electronics & Robotics

In electronics and robotics, tungsten is favored for its excellent electrical conductivity and thermal stability. It is used to produce semiconductors, filaments, contact materials, heat sinks, and X-ray tubes.

Others

The others segment in the tungsten market comprises a variety of specialized and emerging applications spanning the medical, energy, and consumer durable sectors.

Estimation Model

Layer Name

Key Question

Description

Industrial Demand Base Layer

What forms the demand base?

Identify global demand from major tungsten consuming industries including automotive, aerospace & defense, mining, metalworking, electronics, energy, and industrial manufacturing. Assess production volumes of tools, machinery, electronic components, and wear resistant products that utilize tungsten materials. This layer establishes the total addressable demand for tungsten globally.

Tungsten Application Penetration Layer

Where is tungsten utilized?

Estimate the penetration of tungsten across key applications such as cemented carbides, high speed steels, mill products, alloys, chemicals, electronics, and defense equipment. Analyze adoption trends across end use industries and evaluate the role of tungsten in high performance and high temperature applications.

Tungsten Consumption Intensity Layer

How much tungsten is consumed?

Analyze tungsten consumption intensity based on industrial production levels, tooling requirements, mining activities, manufacturing output, and electronics production. Evaluate the utilization of tungsten concentrates, tungsten carbide, tungsten alloys, and tungsten chemicals across applications. Consumption intensity varies according to technological requirements, durability standards, and industrial growth patterns.

Revenue Layer

How is market revenue generated?

Market revenue is quantified through the production and sale of tungsten concentrates, tungsten carbide, ferro tungsten, tungsten alloys, powders, chemicals, and fabricated products. Revenue generation is driven by demand from tooling, aerospace, automotive, mining, electronics, and defense industries. Market value is influenced by tungsten ore availability, processing costs, product grade premiums, technological applications, and regional supply demand dynamics.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

Detailed regional analysis of the tungsten market across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Included evaluation of tungsten mining activities, concentrate production, refining capacities, industrial manufacturing output, defense spending, automotive production, aerospace investments, and government initiatives related to critical minerals and supply chain security.

Identified key production hubs, import dependent regions, and emerging demand centers. Enabled strategic expansion planning based on industrial growth, defense investments, and advanced manufacturing trends. Supported regional demand forecasting and supply chain optimization.

Pricing Analysis

Detailed pricing assessment of tungsten products by form, purity, and region, including concentrate prices, ammonium paratungstate pricing, tungsten carbide costs, processing margins, energy expenses, logistics costs, and downstream value addition. Included historical price volatility analysis, supply demand balance assessment, and long term pricing outlook through 2033.

Enabled understanding of profitability drivers, cost structures, and pricing dynamics throughout the value chain. Supported procurement planning, pricing strategy development, contract negotiations, and investment decision making.

Opportunity Assessment

Identification of high growth opportunities across aerospace components, defense systems, electric vehicles, semiconductor manufacturing, industrial automation, mining equipment, oil & gas drilling tools, and renewable energy technologies. Assessed future demand potential driven by advanced manufacturing growth, critical mineral strategies, electrification trends, and increasing adoption of high performance tungsten based materials.

Enabled prioritization of high return growth segments and emerging regional opportunities. Supported long term investment planning, capacity expansion decisions, and strategic business development initiatives aligned with industrial modernization and energy transition trends.

Frequently Asked Questions About This Report

Based on form, mill products accounted for largest revenue share of 43.1% in 2025, while tungsten carbide compound registered a CAGR of 4.9% over the forecast period.

Based on end use, automotive accounted for largest revenue share of 25.5% in 2025, while electronics registered a CAGR of 5.0% over the forecast period.

The key players operating in the tungsten market are Almatis, Inc., Altech Chemicals Ltd., Alpha HPA, Baikowski, CoorsTek Inc., FYI Resources, Honghe Chemical, Nippon Light Metal Holdings Co., Ltd., Orbite Technologies Inc., Polar Sapphire Ltd., Sumitomo Chemical Co., Ltd.

The global tungsten market's growth is the increasing demand for hard metals and alloys in automotive, aerospace, defense, and industrial machinery applications due to tungsten’s exceptional hardness, high melting point, and durability.

The tungsten market size was estimated at USD 2.0 billion in 2025 and is expected to reach USD 2.1 billion in 2026.

The tungsten market is expected to grow at a compound annual growth rate of 4.7% from 2026 to 2033 to reach USD 2.8 billion by 2033.

Asia Pacific dominated the market with revenue share of 54.2% in 2025.

China dominated the Asia Pacific market with revenue share of 65.4% in 2025.

North America is anticipated to register the fastest CAGR over the forecast period.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.