- Home

- »

- Advanced Interior Materials

- »

-

Welding Equipment Market Size, Industry Report, 2033GVR Report cover

![Welding Equipment Market Size, Share & Trends Report]()

Welding Equipment Market (2026 - 2033) Size, Share & Trends Analysis Report By Technology (Arc Welding, Resistance Welding, Laser Beam Welding, Oxy-Fuel Welding), By Type (Automatic, Semi-Automatic, Manual), By End-use, By Region, And Segment Forecasts

Market Size, 2025

$21,658.7MMarket Estimate, 2026

$22,726.4MMarket Forecast, 2033

$32,533.1MCAGR, 2026–2033

5.3%Welding Equipment Market Summary

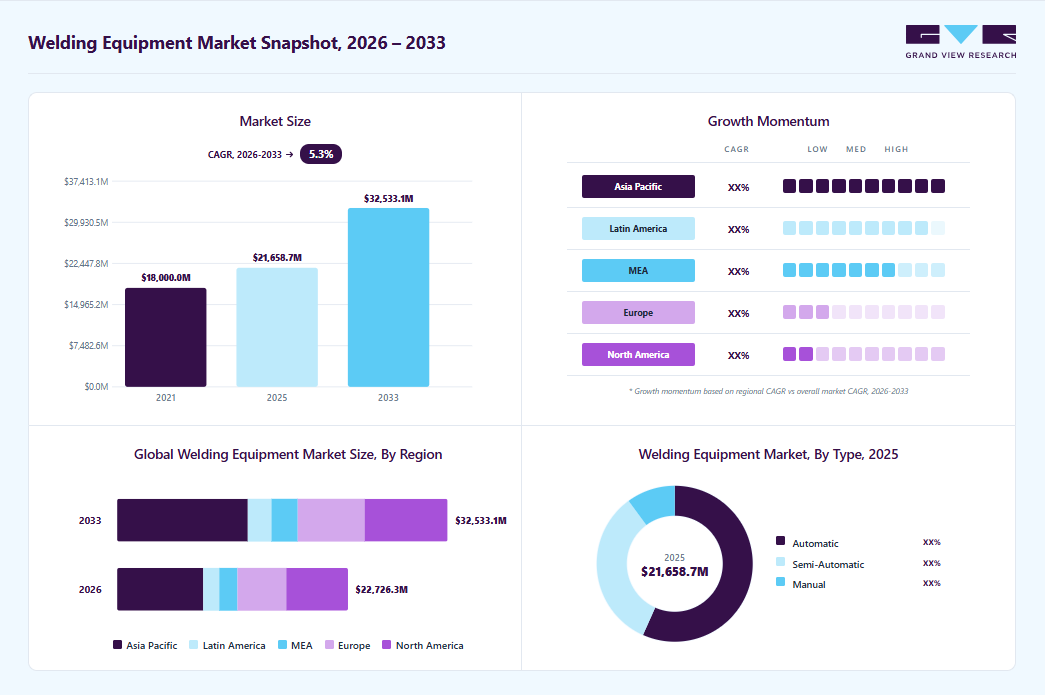

The global welding equipment market size was estimated at USD 21,658.7 million in 2025 and is projected to reach USD 32,533.1 million in 2033, growing at a CAGR of 5.3% from 2026 to 2033. The market growth is driven by rising industrialization and infrastructure development across construction, energy, and heavy manufacturing.

Key Market Trends & Insights

- Asia Pacific dominated the welding equipment market with the largest revenue share of 37.0% in 2025.

- The U.S. welding equipment industry is expected to grow at a substantial CAGR of 4.2% from 2026 to 2033.

- By technology, the laser beam welding segment is expected to grow at a fastest CAGR of 6.6% from 2026 to 2033.

- By type, the automatic welding equipment segment accounting for a 56.7% revenue share in 2025.

- By end-use, the aerospace segment is expected to grow at a fastest CAGR of 6.4% from 2026 to 2033 in terms of revenue.

Market Size & Forecast

- 2025 Market Size: USD 21,658.7 Million

- 2033 Projected Market Size: USD 32,533.1 Million

- CAGR (2026-2033): 5.3%

- Asia Pacific: Largest market in 2025

Large-scale projects in transportation, power generation, and urban infrastructure continue to create steady demand for arc and resistance welding systems. Growth in oil & gas and marine fabrication also supports the need for durable, field-ready welding equipment.")

Another key driver is the shift toward automation and advanced manufacturing, especially in the automotive and aerospace industries. Increasing adoption of automatic, laser, and robotic welding systems helps manufacturers improve productivity, weld quality, and repeatability. The expansion of electric vehicles, lightweight materials, and precision components further boosts demand for high-performance welding technologies. Rising focus on safety, efficiency, and cost optimization continues to accelerate equipment upgrades globally.

Market Concentration & Characteristics

The welding equipment market is moderately concentrated, with a small group of global manufacturers accounting for a strong share of overall revenue. These players benefit from broad product portfolios, strong dealer networks, and long-term relationships with automotive, aerospace, and industrial customers. At the same time, the market includes a large number of regional and local suppliers serving price-sensitive and application-specific needs.

The welding equipment industry shows a steady to high level of innovation driven by automation, digital controls, and advanced welding processes. Manufacturers are focusing on robotic welding, laser-based systems, and smart power sources to improve precision and productivity. The integration of sensors, software, and real-time monitoring is becoming increasingly common across industrial settings.

Regulations related to worker safety, emissions, and energy efficiency strongly influence the welding equipment market. Compliance with occupational safety standards pushes demand for safer, low-fume, and ergonomically designed welding systems. Environmental regulations also encourage the adoption of cleaner technologies such as laser and advanced arc welding.

End-user demand is moderately concentrated, with automotive, construction, and heavy manufacturing accounting for a major share of equipment consumption. Large industrial buyers often place bulk orders and prefer long-term supplier relationships, especially for automated systems. However, a broad base of small- and medium-sized fabricators continues to support demand for manual and semi-automatic equipment.

Drivers, Opportunities & Restraints

The welding equipment market is driven by strong demand from the construction, automotive, and energy industries worldwide. Ongoing infrastructure development and expansion of manufacturing facilities increase the need for reliable joining solutions. Growth in automotive production, including electric vehicles, supports higher adoption of automated and precision welding systems. Rising replacement demand for aging equipment also contributes to steady market expansion.

Increasing automation and adoption of Industry 4.0 practices create new opportunities for advanced welding equipment. Manufacturers are investing in robotic, laser, and digitally controlled welding systems to improve productivity and quality. Emerging economies offer growth potential due to rapid industrialization and infrastructure spending. Demand for customized, application-specific welding solutions further opens opportunities for technology-driven players.

High initial investment and maintenance costs limit the adoption of advanced welding systems, especially among small and medium enterprises. Skilled labor shortages can slow the effective use of automated and high-precision equipment. Volatility in raw material prices affects manufacturing costs and pricing strategies. In some regions, slow industrial growth and delayed capital expenditure also restrain market momentum.

Technology Insights

Arc welding continues to dominate the welding equipment market, accounting for a 70.3 % share in 2025, due to its versatility, cost-effectiveness, and wide industrial acceptance. It is extensively used across construction, oil & gas, shipbuilding, and general fabrication, where durability and flexibility are critical. The technology performs well in both indoor and outdoor environments, making it suitable for field applications. Strong demand from infrastructure and repair activities keeps arc welding at the core of market revenues.

Laser beam welding segment is expected to grow at a fastest CAGR of 6.6% from 2026 to 2033 in terms of revenue, driven by rising demand for precision, speed, and minimal material distortion. Automotive, aerospace, and electronics manufacturers increasingly adopt this technology for lightweight materials and complex assemblies. Its compatibility with automation and robotic systems supports high-volume, high-quality production. As capital investment in advanced manufacturing increases, the adoption of laser welding continues to accelerate globally.

Type Insights

Automatic welding equipment dominated the welding equipment industry, accounting for a 56.7% share in 2025, due to its ability to deliver high productivity, consistency, and reduced dependence on manual labor. It is widely adopted in automotive, aerospace, and large-scale manufacturing, where repeatable weld quality is essential. Integration with robotic systems and automated production lines further strengthens its adoption. High upfront costs are offset by long-term efficiency gains, supporting a strong revenue share.

Semi-automatic segment is expected to grow at a significant CAGR of 5.1% from 2026 to 2033 in terms of revenue, as it offers a balance between automation and operator control. Small and mid-sized manufacturers prefer these systems for flexibility across varied applications. Lower capital investment compared to fully automatic systems supports wider adoption. Demand is rising in fabrication, repair, and regional manufacturing hubs where productivity improvements are needed without full automation.

End-use Insights

The automotive sector dominated welding equipment demand in 2025, accounting for a 24.9% market share, driven by high production volumes and extensive use of welded components. Resistance, MIG, and laser welding systems are widely deployed across body-in-white, chassis, and powertrain manufacturing. Ongoing investments in electric vehicle production further strengthen demand for equipment. Continuous automation and efficiency upgrades keep automotive as the largest revenue contributor.

Aerospace segment is expected to grow at a fastest CAGR of 4.9% from 2026 to 2033 in terms of revenue, driven by rising aircraft production and demand for lightweight, high-strength structures. Precision welding technologies such as TIG and laser beam welding are increasingly adopted to meet strict quality standards. Growth in defense spending and commercial aviation supports sustained equipment investment. The need for advanced materials and flawless joints continues to accelerate adoption in this sector.

Regional Insights

North America welding equipment market is expected to show steady growth at a 4.3% CAGR over the forecast period, supported by advanced manufacturing and strong adoption of automated welding systems. Automotive, aerospace, and energy sectors continue to invest in productivity-enhancing technologies. Replacement of aging equipment and focus on worker safety drive upgrades. Technological innovation remains a key growth enabler across the region.

U.S. Welding Equipment Market Trends

The U.S. dominates the North America welding equipment industry, driven by its strong industrial base and advanced manufacturing ecosystem. High demand from automotive, aerospace, construction, and energy sectors supports consistent equipment sales. Widespread adoption of automated and robotic welding systems enhances productivity and quality standards. Ongoing replacement of legacy equipment further sustains market leadership.

The Canada welding equipment market is witnessing steady growth driven by infrastructure development and expansion in energy and manufacturing sectors. Oil & gas projects, transportation infrastructure, and metal fabrication activities support demand for welding equipment. Increasing focus on automation and worker safety encourages equipment upgrades. Government-backed industrial investments continue to support market expansion.

Europe Welding Equipment Market Trends

The Europe welding equipment industry grows on the back of automotive innovation and industrial modernization. Strict safety and environmental regulations encourage the adoption of efficient and low-emission welding technologies. Demand for laser and robotic welding systems is rising across advanced manufacturing hubs. Ongoing focus on quality and sustainability supports long-term growth.

The Germany welding equipment market dominates Europe, driven by its strong automotive, machinery, and industrial manufacturing base. The country’s leadership in automation and precision engineering drives high adoption of advanced welding technologies. Strong demand for robotic, laser, and resistance welding systems supports market stability. Continuous investment in industrial modernization reinforces Germany’s leading position.

The welding equipment market in France is experiencing steady growth, supported by the aerospace, defense, and transportation industries. Increasing aircraft production and maintenance activities drive demand for high-precision welding solutions. Infrastructure upgrades and energy projects further support equipment adoption. Rising focus on automation and quality standards continues to accelerate market growth.

Asia Pacific Welding Equipment Market Trends

Asia Pacific dominated the welding equipment industry in 2025, accounting for a 37.0% share, driven by strong manufacturing activity and rapid infrastructure development. Countries such as China, India, and Southeast Asian nations drive high demand across construction, automotive, and heavy industries. The presence of large fabrication hubs and cost-competitive manufacturing supports sustained equipment sales. Rising investments in industrial automation further strengthen regional market leadership.

The China welding equipment market dominates Asia Pacific, driven by its large-scale manufacturing base and extensive infrastructure development. High demand from automotive, construction, shipbuilding, and heavy industries drives continuous equipment consumption. Strong domestic production and competitive pricing support widespread adoption across manual and automated systems. Ongoing investments in smart manufacturing further reinforce China’s market leadership.

The welding equipment market in India is growing rapidly, supported by expanding infrastructure, industrialization, and government-led manufacturing initiatives. Rising demand from construction, railways, automotive, and energy sectors fuels equipment adoption. Increasing investments in fabrication capacity and localized manufacturing boost market potential. Gradual shift toward semi-automatic and automated welding systems supports sustained growth.

Middle East & Africa Welding Equipment Market Trends

The Middle East and Africa welding equipment industry is growing with the investments in oil & gas, power, and large-scale construction projects. Welding equipment demand is supported by pipeline installation, structural fabrication, and maintenance activities. Governments are investing in infrastructure diversification beyond hydrocarbons. This creates steady opportunities for both heavy-duty and portable welding solutions.

The Saudi Arabia welding equipment market is emerging as a key growth region in Middle East & Africa. Large-scale investments in oil & gas, petrochemicals, and power infrastructure drive sustained demand for heavy-duty welding systems. Ongoing megaprojects and industrial diversification initiatives increase fabrication and construction activity. Rising focus on local manufacturing and infrastructure development continues to support market growth.

Latin America Welding Equipment Market Trends

Latin America is experiencing gradual growth driven by infrastructure development and the expansion of manufacturing. Brazil and Argentina lead regional demand across automotive, construction, and energy sectors. Investment in industrial equipment remains selective but improving. Growth is supported by increasing focus on local fabrication and repair work.

The Brazil welding equipment market is growing, supported by expanding construction and manufacturing activities. Automotive production, infrastructure projects, and energy sector investments drive demand. Increasing focus on local fabrication and industrial maintenance boosts equipment usage. Gradual adoption of semi-automatic and automated welding systems supports steady market growth.

Key Welding Equipment Company Insights

Some of the key players operating in the market include The Lincoln Electric Company, ESAB, and Miller Electric Mfg. LLC

-

The company holds a strong leadership position in arc welding equipment with deep penetration across automotive, construction, energy, and heavy fabrication. Its strength lies in integrated solutions that combine power sources, consumables, automation, and digital weld management. High adoption of robotic and automated welding cells supports large-volume manufacturing customers. The firm benefits from long-term contracts, aftermarket sales, and service-driven revenues. Continuous investment in process efficiency and weld quality keeps it competitive in high-spec applications.

-

ESAB maintains a broad footprint across welding and cutting equipment with balanced exposure to manual, semi-automatic, and automated systems. The company is well positioned in industrial fabrication, shipbuilding, and energy-related projects. Strong demand for its advanced arc and cutting technologies supports stable revenue streams. Its diversified product mix helps manage cyclicality across end-use industries. Focus on process reliability and productivity improvements to strengthen global customer retention.

Key Welding Equipment Companies:

The following key companies have been profiled for this study on the welding equipment market.

- The Lincoln Electric Company

- ACRO Automation Systems, Inc

- Miller Electric Mfg. LLC

- Ador Welding Limited

- Mitco Weld Products Pvt. Ltd.

- voestalpine Böhler Welding Group GmbH

- Carl Cloos Schweisstechnik GmbH

- OTC DAIHEN Inc.

- Illinois Tool Works Inc.

- Panasonic Industry Co., Ltd.

- Coherent, Inc.

- ESAB

- Polysoude S.A.S.

- Kemppi Oy.

- Cruxweld Industrial Equipment Pvt. Ltd.

Recent Developments

-

In September 2025, The Lincoln Electric Company introduced the Flex Lase handheld laser welding system to support faster and more precise welding applications. The system is designed to deliver higher welding speeds with lower heat input compared to conventional methods. It helps reduce distortion and post-weld finishing across common industrial materials. The solution targets productivity improvements in fabrication, automotive, and precision manufacturing environments.

-

In December 2025, Miller Electric Mfg. LLC introduced the Auto Elite wire drive designed specifically for use with the Auto Deltaweld system. The solution supports smooth integration into automated and robotic welding lines. It improves arc consistency while simplifying maintenance and changeovers. The design helps manufacturers increase uptime in high-volume production environments.

Welding Equipment Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 22,726.4 million

Revenue forecast in 2033

USD 32,533.1 million

Growth rate

CAGR of 5.3% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Technology, type, end-use, region.

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Spain; Italy; China; Japan; India; Australia; South Korea; Brazil; Argentina; Saudi Arabia; South Africa

Key companies profiled

The Lincoln Electric Company; ACRO Automation Systems, Inc.; Miller Electric Mfg. LLC; Ador Welding Limited; Mitco Weld Products Pvt. Ltd.; voestalpine Böhler Welding Group GmbH; Carl Cloos Schweisstechnik GmbH; OTC DAIHEN Inc.; Illinois Tool Works Inc.; Panasonic Industry Co., Ltd.; Coherent, Inc.; ESAB; Polysoude S.A.S.; Kemppi Oy.; Cruxweld Industrial Equipments Pvt. Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Welding Equipment Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global welding equipment market report based on technology, type, end-use, and region:

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Arc Welding

-

Shielded Metal/Stick Arc Welding

-

MIG

-

TIG

-

Plasma Arc Welding

-

Others

-

-

Resistance Welding

-

Laser Beam Welding

-

Oxy-Fuel Welding

-

Others

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Automatic

-

Semi-Automatic

-

Manual

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Aerospace

-

Building & Construction

-

Automotive

-

Energy

-

Oil & Gas

-

Marine

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

Italy

-

Spain

-

UK

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global welding equipment market size was estimated at USD 21,658.7 million in 2025 and is expected to be USD 22,726.4 million in 2026.

The global welding equipment market, in terms of revenue, is expected to grow at a compound annual growth rate of 5.3% from 2026 to 2033 to reach USD 32,533.1 million by 2033.

Asia Pacific region dominated the market in 2025 by accounting for a share of 37.0% of the market. Shifting consumer preferences toward customization and maintaining the ride quality and fuel efficiency of vehicles are likely to heighten the frequency of vehicle maintenance and repair activities, which, in turn, is expected to drive the demand for welding equipment.

The majority of the demand for welding equipment is associated with end-use industries such as automotive, aerospace, transportation, and construction, which are also experiencing operational difficulties owing to the macro-economic factors.

Some of the key players operating in the welding equipment market include The Lincoln Electric Company; ACRO Automation Systems, Inc.; Miller Electric Mfg. LLC; Ador Welding Limited; Mitco Weld Products Pvt. Ltd.; voestalpine Böhler Welding Group GmbH; Carl Cloos Schweisstechnik GmbH; OTC DAIHEN Inc.; Illinois Tool Works Inc.; Panasonic Industry Co., Ltd.; Coherent, Inc.; ESAB; Polysoude S.A.S.; Kemppi Oy.; Cruxweld Industrial Equipments Pvt. Ltd.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.