- Home

- »

- Next Generation Technologies

- »

-

5G Security Market Size And Share Report, 2026-2033GVR Report cover

![5G Security Market (2026 - 2033)Report]()

5G Security Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Solution, Services), By Deployment (Cloud, On-premise), By Architecture (5G NR Standalone, 5G NR Non-Standalone), By Network Security By End Use, By Region, And Segment Forecasts

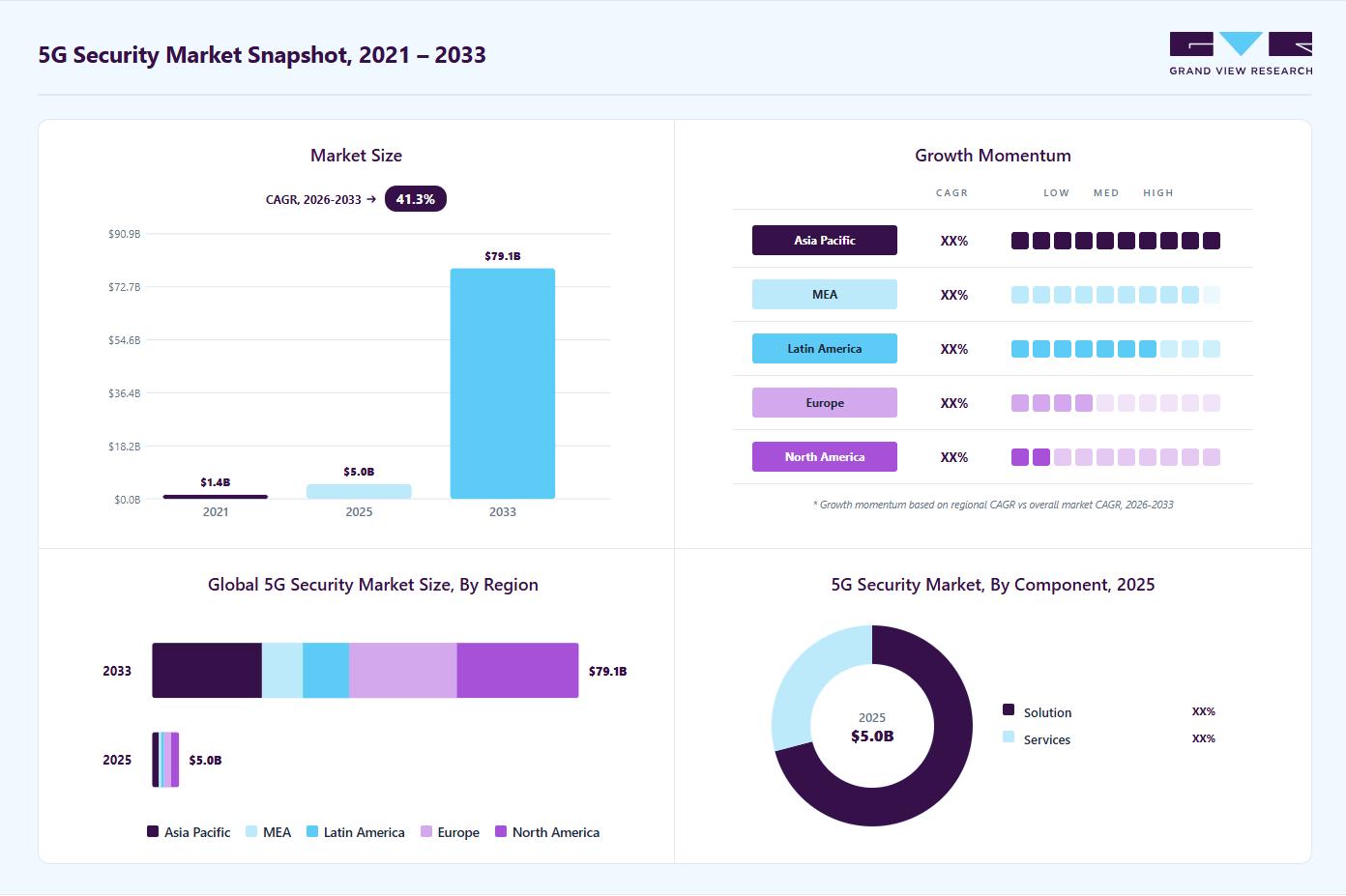

Market Size, 2025

$5.0BMarket Estimate, 2026

$7.0BMarket Forecast, 2033

$79.1BCAGR, 2026–2033

41.3%5G Security Market Summary

The global 5G security market size was valued at USD 5.0 billion in 2025 and is projected to grow from USD 7.0 billion in 2026 to USD 79.1 billion by 2033, at a CAGR of 41.3% from 2026 to 2033. The North America held the largest share of 30.0% of the global market in 2025. The market growth can be attributed to the growing attacks on critical infrastructure, rising ransomware attacks on IoT devices, and growing security concerns in the 5G network.

Key Market Trends & Insights

- By component: Solution segment held the largest market share of 70.9% in 2025.

- By deployment: Cloud segment accounted for the largest market share in 2025.

- By architecture: 5G NR non-standalone segment accounted for the largest revenue share in 2025.

- By network security: RAN security segment accounted for the largest market share in 2025.

- By end use: Telecom operators segment accounted for the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (30.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 5.0 Billion

- Estimated market size in 2026: USD 7.0 Billion

- Projected market size by 2033: USD 79.1 Billion

- CAGR (2026-2033): 41.3%

The fifth-generation (5G) network represents an advanced wireless technology ecosystem encompassing diverse radio frequencies, high-speed data transfer, and complex communication frameworks, all of which require enhanced security measures. The adoption of network slicing and the expansion of security capabilities beyond 4G and LTE are expected to significantly drive demand for 5G security solutions. In addition, the growing complexity of 5G infrastructure increases the need for robust protection against evolving cyber threats. Furthermore, stringent government regulations aimed at preventing data breaches in 5G-enabled applications are anticipated to create substantial growth opportunities for the 5G security industry during the forecast period.")

The integration of artificial intelligence (AI) and machine learning (ML) is transforming the 5G security landscape by enabling more advanced and adaptive defense mechanisms. These technologies facilitate automated threat detection and response, allowing organizations to identify and mitigate risks in real time. AI-driven analytics can process large volumes of data transmitted across 5G networks to detect anomalies and potential breaches at an early stage. As cyber threats continue to evolve in complexity, the adoption of AI- and ML-enabled security solutions has become critical for maintaining robust network protection.

Technological advancements and the expansion of networks beyond 5G Radio Access Networks (RANs) are anticipated to have a substantial impact on security, including edge computing, Network Function Virtualization (NFV), and Software-defined Networking (SDN). Security solutions must evolve to protect vital infrastructure from the rising hazards posed by the nation-states and other sophisticated players, as well as the real dangers they bring to mobile network operators (MNOs) and their suppliers. The 5G 3GPP standard is adaptable enough to support many forms of physical and virtual overlap between the radio access network (RAN) and core network, such as from a remote device to the core network. Rapid technological change, including virtualization, disaggregation, cloud computing, Artificial Intelligence (AI), the Internet of Things (IoT), and Industry 4.0, is affecting telecom networks, which are met by a broad and challenging cybersecurity environment.

Cybersecurity has evolved with the introduction of 5G. International Mobile Subscriber Identity (IMSI) encryption is a feature of a 5G cybersecurity toolbox or solution that enhances network security. To further ensure optimum data security, all traffic data sent over the 5G network is integrated, secured, encrypted, and adheres to a mutual authentication standard. In addition, the deployment of artificial intelligence (AI), the internet of things (IoT), cloud computing, etc., benefits from a stronger foundation in 5G security. It uses deep packet inspection (DPI), which combines hardware and software resources into a single entity, and meticulously examines data delivered over a computer network, as well as network virtualization.

For businesses, technology offers enormous opportunities by enabling novel use cases. The development of smart infrastructures, the rising demand to revolutionize the mobile broadband experience, and the rise of the worldwide 5G services industry are the key drivers for expanding the market. On the other hand, there are sizable growth prospects for 5G security solutions providers. The future of the 5G security market is expected to be shaped by the increasing demand for high-reliability, low-latency networks, the emergence of a massive IoT ecosystem, the expansion of critical communications services, and the growing demand for private 5G networks across governments, industries, and sectors. However, high costs associated with deploying 5G services and a lack of awareness in developing economies are expected to hinder the growth of the market during the coming years.

Market Dynamics

Increasing adoption of private 5G networks across industrial and enterprise environments is driving the growth of the 5G security market by enabling organizations to deploy dedicated, high-performance communication infrastructure tailored to mission-critical operations. Enterprises across manufacturing, energy, logistics, healthcare, mining, and defense sectors are increasingly investing in private 5G networks to support industrial automation, real-time analytics, connected machinery, and autonomous systems. While these networks offer enhanced speed, low latency, and improved operational control, they also significantly expand the cybersecurity surface area, creating strong demand for advanced security solutions.

The deployment of private 5G networks introduces complex security challenges due to the convergence of IT and operational technology (OT) environments, as well as the increasing use of IoT devices, edge computing systems, and cloud-native applications. These interconnected ecosystems require robust protection against unauthorized access, data breaches, and sophisticated cyberattacks targeting critical infrastructure. As a result, organizations are increasingly adopting advanced 5G security frameworks, including zero-trust architectures, network slicing security, identity and access management, and AI-driven threat detection systems.

High deployment costs and integration complexity of 5G security solutions are restraining the growth of the market by creating financial and operational challenges for telecom operators and enterprises. Securing 5G networks requires significant investment in advanced cybersecurity infrastructure, including encryption technologies, AI-driven threat detection systems, secure network slicing, and continuous monitoring tools. In addition, organizations must frequently upgrade their legacy security systems to align with the dynamic and cloud-native nature of 5G architectures, further increasing overall implementation costs.

The expansion of Industry 4.0 and connected industrial ecosystems is creating significant growth opportunities for the 5G security market by accelerating the deployment of smart factories, autonomous systems, and IoT-enabled industrial environments. Industries such as manufacturing, energy, transportation, healthcare, and logistics are increasingly adopting 5G-enabled automation to enhance productivity, operational efficiency, and real-time decision-making. However, this growing connectivity also increases exposure to cyber threats, driving strong demand for robust and intelligent security solutions.

The integration of industrial IoT devices, robotics, edge computing, and cloud-based platforms within 5G networks is expanding the attack surface, making advanced security frameworks essential. Organizations are increasingly investing in zero-trust architectures, AI-powered threat intelligence, identity and access management, and secure network slicing to safeguard mission-critical operations. In addition, the convergence of IT and OT environments in industrial settings is further increasing the need for comprehensive cybersecurity strategies tailored to complex operational ecosystems.

Market Concentration & Characteristics

The 5G security market is moderately fragmented, with a growing trend toward consolidation driven by increasing demand for integrated and advanced cybersecurity solutions. Fragmentation is primarily observed at the lower and mid-tier levels, where numerous cybersecurity vendors, niche technology providers, and regional players operate. These companies typically focus on specific aspects of 5G security such as network monitoring, endpoint protection, encryption, identity and access management, or IoT security. Lower entry barriers in software-based security solutions and the rapid evolution of cybersecurity technologies have enabled a wide range of specialized firms to enter the market, particularly in emerging digital economies.

Market is further accelerated by mergers, acquisitions, and strategic partnerships aimed at expanding 5G security capabilities and geographic reach. Larger players are acquiring niche cybersecurity startups to enhance capabilities in areas such as AI-based threat detection, zero-trust architecture, and edge security. In addition, collaborations between telecom operators, hyperscale cloud providers, and security vendors are shaping integrated security ecosystems for 5G networks.

Component Insights

The solution segment dominated the 5G security market in 2025, accounting for the largest share of 70.9%. One of the main factors driving the segment's growth is the rapid adoption of 5G security solutions by end-user companies to protect their personal networks. To secure the networks, major market competitors are concentrating on developing 5G security solutions to further protect the enterprise network architecture. In addition, the rise in edge computing and virtualized network functions has further pushed organizations to adopt comprehensive, integrated security solutions to ensure network integrity and resilience across multiple points of connectivity.

The services segment is expected to grow at the fastest CAGR over the forecast period. The widespread adoption of 5G services is driving the expansion of the services market. Applications that support the Internet of Things (IoT), real-time communications (RTC), ultra-reliable communications, and broadcast-like services are accessible to businesses using 5G services. Fifth-generation services also satisfy rising consumer demand for in-vehicle services and support vehicle diagnostics and autonomous driving applications integrated into mobile on-the-go vehicles.

Deployment Insights

The cloud segment accounted for the largest share of the 5G security industry in 2025 and is expected to grow at the fastest CAGR over the forecast period. Cloud-based deployments have become increasingly popular in recent years for delivering security services remotely. Significant performance improvements across applications such as cloud-based resources, network slicing, virtualization, and other emerging technologies are just a few of the advantages 5G security offers. The cloud deployment model also provides advantages for managing DNS, rerouting traffic, and protecting website traffic. In addition, cloud services are implemented the meet the client's needs, based on the volume of cloud-based 5G security services. Such factors bode well for the growth of the segment during the forecast period.

The on-premise segment is expected to grow at a notable CAGR during the forecast period. The ability of the on-premise 5G security solutions to verify and protect the 5G network connections in an organization's premises is a significant factor driving the segment growth. On-premise solutions make it easier for businesses to check any possible dangers on their site. Along with offering fast speeds for 5G networks, 5G security solutions also help to ensure better privacy of the client data. For these reasons, businesses are adopting on-premises 5G security solutions to prevent fraud on 5G networks.

Architecture Insights

The 5G NR non-standalone segment dominated the market in 2025. The growing demand for 5G mobile services, the need for fast, reliable networks, and rising investments in 5G services are the major factors driving the segment's growth. Market players across the globe are implementing 5G NR non-standalone technology on existing LTE infrastructure to meet increased customer demand for better, more reliable network connectivity. Manufacturers of mobile phones are now focusing more on creating 5G-enabled smartphones. Hence, the 5G NR non-standalone architecture has expanded due to the rising adoption of smartphones with 5G capabilities.

The 5G NR standalone segment is expected to grow at the fastest CAGR during the forecast period. The benefits offered by the 5G NR standalone architecture to offer higher speeds, wider coverage, ultra-low latency, higher stability, and better services compared to 5G NR non-standalone are driving the segment growth. Standalone 5G uses a 5G New Radio access network, which incorporates standards that replace the LTE network 4G wireless communications standard. The end-to-end core 5G network serves as the foundation of the independent 5G architecture. Hardware and network features for the 5G architecture were developed with 5G requirements in mind.

Network Security Insights

The RAN security segment accounted for the largest share of the 5G security market in 2025 and is expected to grow at the fastest CAGR over the forecast period. The ability of the RAN (Radio Access Network) component to connect devices to auxiliary network components via radio connection is a major factor driving the segment growth. Mobile network operators (MNOs) and network service providers are increasingly implementing centralized RAN and virtual RAN (VRAN) to minimize overall infrastructure costs and network complexity. Furthermore, the RAN enables corporations and mobile network operators to deploy private 5G to offer network slicing solutions by allocating network resources to separate network utilization within a public mobile network. As RAN offers the capability of network slicing, providing security is also of utmost importance, which in turn creates lucrative growth opportunities for the 5G security solution providers during the coming years.

The core security segment is expected to grow at a notable CAGR during the forecast period. The broad use of modern technologies such as machine learning and artificial intelligence, along with the quick advancement of the networks for machine-to-machine communication, is a significant factor driving the growth of the segment. 5G core has the capability to perform a variety of tasks, including subscriber data management, authentication & authorization, connection & mobility management, and policy management. As the 5G core is responsible for various functions, 5G security solutions for the core would help prevent potential security threats to the end users.

End Use Insights

The telecom operators segment dominated the 5G security industry in 2025. Segment growth can be attributed to the growing number of mobile users, the skyrocketing demand for high-speed data connectivity, and the rising demand for value-added managed services. Over the past few decades, the global communication network has clearly been one of the most significant areas for continuing technical breakthroughs. Telecom operators are using multi-vendor networks based on cloud-native technology to accelerate and cost-effectively roll out 5G services and improve user experience. Moreover, to enhance 5G security, telecom operators are leveraging network slicing, dividing a single network into multiple independent logical networks with distinct features.

The industries segment is expected to grow at the fastest CAGR over the forecast period. The segment includes industries such as manufacturing, healthcare, retail, automotive and transportation, public safety, and others. The growing demand for 5G security among these industries for better machine-to-machine network connectivity is a major factor driving the segment growth. As the deployment of IoT-based devices is increasing day by day in industries, the demand to keep the data secure over the 5G networks is also growing, thereby creating an opportunity for the 5G security solution providers. At the same time, as industries focus more on identifying potential attacks on 5G networks, they are increasingly seeking 5G security solutions.

Regional Insights

North America dominated the 5G security market, accounting for a share of 30.0% in 2025. Palo Alto Networks, A10 Networks, Inc., and AT&T are among the leading participants driving the regional growth. The increasing use of 5G security solutions by the manufacturing companies, to prevent potential threats on 5G networks, offers growth prospects for 5G solutions providers in the area, supporting the market growth of North America. Furthermore, the increasing inclination for digitalization is expected to fuel demand for the novel solutions from retail, healthcare, and other financial organizations. Over the foreseeable term, these variables are expected to boost regional growth.

U.S. 5G Security Market Trends

The U.S. 5G security industry held a dominant regional position in 2025. As 5G technology becomes the backbone of critical infrastructure spanning industries such as healthcare, finance, manufacturing, and transportation, there is an increasing emphasis on securing these networks from evolving cyber threats. U.S. enterprises and government agencies are investing heavily in advanced security solutions such as encryption, threat intelligence, and network monitoring tools to protect against sophisticated attacks.

Europe 5G Security Market Trends

The Europe 5G security industry is expected to register a moderate CAGR from 2026 to 2033. European countries are prioritizing the security of their 5G networks amid rising concerns about cyberattacks and data breaches, as 5G enables more complex digital ecosystems with a vast number of connected devices. Regulatory bodies, such as the European Union Agency for Cybersecurity (ENISA), are enforcing stringent guidelines to ensure robust 5G security frameworks across member states. European telecom operators are increasingly adopting advanced security solutions, such as network segmentation, encryption, and AI-driven threat detection, to protect their networks.

The UK 5G security market is expected to grow at the fastest CAGR during the forecast period. With the UK’s emphasis on digital transformation across industries such as healthcare, finance, and transportation, securing the 5G ecosystem has become a national priority. Government initiatives, such as the National Cyber Security Centre’s (NCSC) guidelines, play a pivotal role in shaping the country’s approach to 5G security, focusing on threat mitigation, data protection, and safeguarding network integrity.

The 5G Security market in Germany held a substantial revenue share in 2025. Germany’s ambition to lead in Industry 4.0 and connected technologies underscores the critical need for secure, high-performance 5G networks. The rapid deployment of IoT devices and real-time communication systems across industrial and urban environments is driving demand for advanced security solutions to mitigate cyber threats and ensure data integrity.

Asia Pacific 5G Security Market Trends

The Asia Pacific 5G Security industry is expected to grow at the fastest CAGR during the forecast period. The geographic expansion might be ascribed to the growing awareness of 5G security solutions in emerging economies such as India and Japan. Simultaneously, growing 5G connections and strict government rules requiring 5G security processes are projected to boost regional growth.

India’s 5G security market is expected to grow at the fastest growth rate during the forecast period. The rapid rollout of 5G networks and the growing adoption of digital services across sectors such as healthcare, manufacturing, finance, and smart cities can be attributed to the growth of the market.

The 5G security market in China held a significant revenue share in 2025. China’s rapid expansion of 5G across industries such as manufacturing, transportation, and smart cities is driving a heightened need for advanced security solutions. The growing number of connected devices and the increased reliance of critical systems on 5G networks are amplifying concerns about data privacy, cyber threats, and network integrity.

Key 5G Security Company Insights

Some of the key companies in the 5G security industry include Telefonaktiebolaget LM Ericsson, Palo Alto Networks, and Thales. These companies are focusing on providing 5G security solutions that may help industries increase operational efficiency and improve working conditions. Market players are focusing on methods such as collaboration and product launch to expand their product offerings. The product launch aims to validate security in the 5G networks. The firms operating in the 5G security industry are seeking to combine advanced technologies such as AI low latency, and others in their 5G security solutions. This integration of advanced technology allows businesses to strengthen their competitive advantage and customer experience. The use of network slicing in 5G solutions provides a more reliable, dependable, and highly dynamic network with faster speeds and connectivity.

-

Telefonaktiebolaget LM Ericsson is a prominent player in the 5G security market, focusing on integrating security features into its telecommunications infrastructure. The company offers advanced solutions, including secure network slicing, encrypted communications, and robust cybersecurity controls, tailored for 5G environments. Ericsson's commitment to end-to-end security ensures comprehensive protection for data across networks, devices, and cloud systems, making it essential for operators seeking to deploy secure and resilient 5G networks.

-

Palo Alto Networks offers specialized cybersecurity solutions designed to address the unique challenges posed by 5G networks. The company leverages its expertise in advanced threat detection, AI-driven analytics, and comprehensive security frameworks to protect against a wide array of cyber threats.

Key 5G Security Companies:

The following key companies have been profiled for this study on the 5G security market.

- Telefonaktiebolaget LM Ericsson

- Palo Alto Networks

- Thales

- A10 Networks, Inc.

- Allot

- AT&T, Inc.

- F5, Inc.

- Check Point Software Technologies Ltd.

- Fortinet, Inc.

- Spirent Communications

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Ericsson; Palo Alto Networks; Thales; Check Point Software Technologies; Fortinet; AT&T

- Mature players focus on delivering integrated 5G security ecosystems combining network infrastructure security, cloud-native protection, and enterprise cybersecurity capabilities.

- They also leverage strong partnerships with telecom operators, and governments to deploy large-scale secure 5G networks.

- Strong global presence with extensive telecom and enterprise client relationships.

- Ability to provide fully integrated, end-to-end security solutions across complex 5G architectures and multi-cloud environments.

- High solution complexity and deployment costs may limit adoption among smaller operators and SMEs.

- Long sales and procurement cycles, especially in telecom and government contracts.

Emerging Players: A10 Networks; Allot; Spirent Communications

- Emerging players focus on specialized 5G security functions such as DDoS mitigation, traffic analytics, network visibility.

- Strategies emphasize cloud-native, software-defined, and modular security solutions that can be rapidly deployed within telecom operator ecosystems.

- Emerging players focus on specialized 5G security functions such as DDoS mitigation, traffic analytics, network visibility, performance assurance, and signaling security.

- Strategies emphasize cloud-native, software-defined, and modular security solutions that can be rapidly deployed within telecom operator ecosystems.

- Limited end-to-end 5G security portfolios compared to global cybersecurity leaders.

- Smaller global footprint and lower brand recognition in enterprise and government markets

Recent Developments

-

In February 2025, NTT DATA, a global provider of digital business and technology services, announced a managed security service designed to strengthen private 5G security in industrial and operational technology environments. The solution leverages advanced technologies from Palo Alto Networks to deliver enhanced protection and network visibility. Offered as a turnkey managed service, it enables enterprises to deploy private 5G networks with integrated security capabilities tailored to modern OT requirements.

-

In February 2024, Palo Alto Networks launched comprehensive end-to-end private 5G security solutions in collaboration with key Private 5G partners, such as Druid, Celona, Ataya, NVIDIA, NETSCOUT, and NTT DATA, to help organizations secure their 5G networks from deployment to operation. These solutions address growing security risks in complex 5G environments, driven by the increasing use of 5G-connected devices, which 70% of executives identify as a rising threat. The ecosystem approach integrates Palo Alto Networks' enterprise-grade 5G security with partner technologies, offering enhanced visibility, secure access, AI-powered applications, and threat detection for private 5G networks. This collaboration ensures robust protection of mission-critical 5G infrastructures, supporting industries' digital transformation.

5G Security Market Report Scope

Report Attribute

Details

Market size in 2025

USD 5.0 billion

Estimated market size in 2026

USD 7.0 billion

Projected market size by 2033

USD 79.1 billion

Growth rate

CAGR of 41.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, deployment, architecture, network security, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Telefonaktiebolaget LM Ericsson; Palo Alto Networks; Thales; A10 Networks, Inc.; Allot; AT&T, Inc.; F5, Inc.; Check Point Software Technologies Ltd.; Fortinet, Inc.; Spirent Communications

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global 5G Security Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global 5G security market report based on component, deployment, architecture, network security, end use, and region:

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Solution

-

Next Gen Firewall

-

Antivirus/Antimalware

-

Security Gateway

-

Distributed Denial of Service Protection (DDoS)

-

Sandboxing

-

Others

-

-

Services

-

Consulting

-

Implementation

-

Support & Maintenance

-

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud

-

On-premise

-

-

Architecture Outlook (Revenue, USD Million, 2021 - 2033)

-

5G NR Standalone

-

5G NR Non-Standalone

-

-

Network Security Outlook (Revenue, USD Million, 2021 - 2033)

-

RAN Security

-

Core Security

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Industries

-

Manufacturing

-

Healthcare

-

Retail

-

Automotive And Transportation

-

Public Safety

-

Others

-

-

Telecom Operators

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

5G Security Opportunity Assessment

Country/region-wise 5G security market sizing and growth forecasts across North America, Europe, Asia Pacific, and Rest of World

Assessment of regulatory frameworks impacting 5G security (data privacy laws, telecom security mandates, critical infrastructure protection guidelines)

Identification of high-growth segments such as private 5G networks, IoT security, edge security, and cloud-native security solutions

Identified region-specific growth opportunities in high-risk and high-adoption markets

Supported telecom operator and enterprise security investment strategies

5G Security Technology & Deployment Behavior Study

Analysis of enterprise and telecom operator security adoption patterns across industries and network types

Evaluation of cloud-based vs on-premise 5G security deployment preferences

Improved segmentation of security solution demand by use case and network architecture

Supported product positioning for cloud-native and hybrid security solutions

Competitive Benchmarking and Strategic Positioning in the 5G Security Market

Benchmarking of key players across solution portfolios, AI/ML capabilities, threat detection technologies, and managed security services

Comparative assessment of market share, partnerships with telecom operators, and cloud ecosystem integration

Identified competitive white spaces in AI-driven and edge security solutions

Supported strategic positioning and partnership development with telecom operators

Frequently Asked Questions About This Report

The solution segment led with a 70.9% revenue share in 2025, while the services segment is expected to grow at the fastest CAGR during the forecast period.

The cloud segment held the largest share in 2025 and is expected to grow at the fastest CAGR during the forecast period.

The 5G NR non-standalone segment held the largest revenue share in 2025, while the 5G NR standalone segment is expected to grow at the fastest CAGR during the forecast period.

The RAN security segment accounted for the largest market share in 2025 and is expected to grow at the fastest CAGR during the forecast period.

North America dominated with a 30.0% revenue share in 2025.

The global 5G security market size was valued at USD 5.0 billion in 2025 and is estimated at USD 7.0 billion for 2026.

The global 5G security market is expected to grow at a CAGR of 41.3% from 2026 to 2033, reaching USD 79.1 billion by 2033.

Asia Pacific is the fastest-growing region over the forecast period.

Some of the key players operating in the 5G security market include Telefonaktiebolaget LM Ericsson, Palo Alto Networks, Thales, A10 Networks, Inc., Allot, AT&T, Inc., F5, Inc., Check Point Software Technologies Ltd., Fortinet, Inc., and Spirent Communications.

Key factors driving the 5G security market include growing attacks on critical infrastructure, rising ransomware attacks on IoT devices, increasing security concerns in 5G networks, expanding adoption of private 5G networks, rising deployment of IoT devices and edge computing systems, increasing demand for network slicing security, and the growing need for AI-driven threat detection and advanced cybersecurity solutions.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.