- Home

- »

- Organic Chemicals

- »

-

Metalworking Fluids Market Size & Share Report, 2026-2033GVR Report cover

![Metalworking Fluids Market Size, Share & Trends Report]()

Metalworking Fluids Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Mineral, Synthetic, Bio-based), By Application (Neat Cutting Oils, Water Cutting Oils, Corrosion Preventive Oils), By End Use, By Industrial End Use, By Region, And Segment Forecasts

Market Size, 2025

$12.8BMarket Estimate, 2026

$12.3BMarket Forecast, 2033

$16.1BCAGR, 2026–2033

2.7%Metalworking Fluids Market Summary

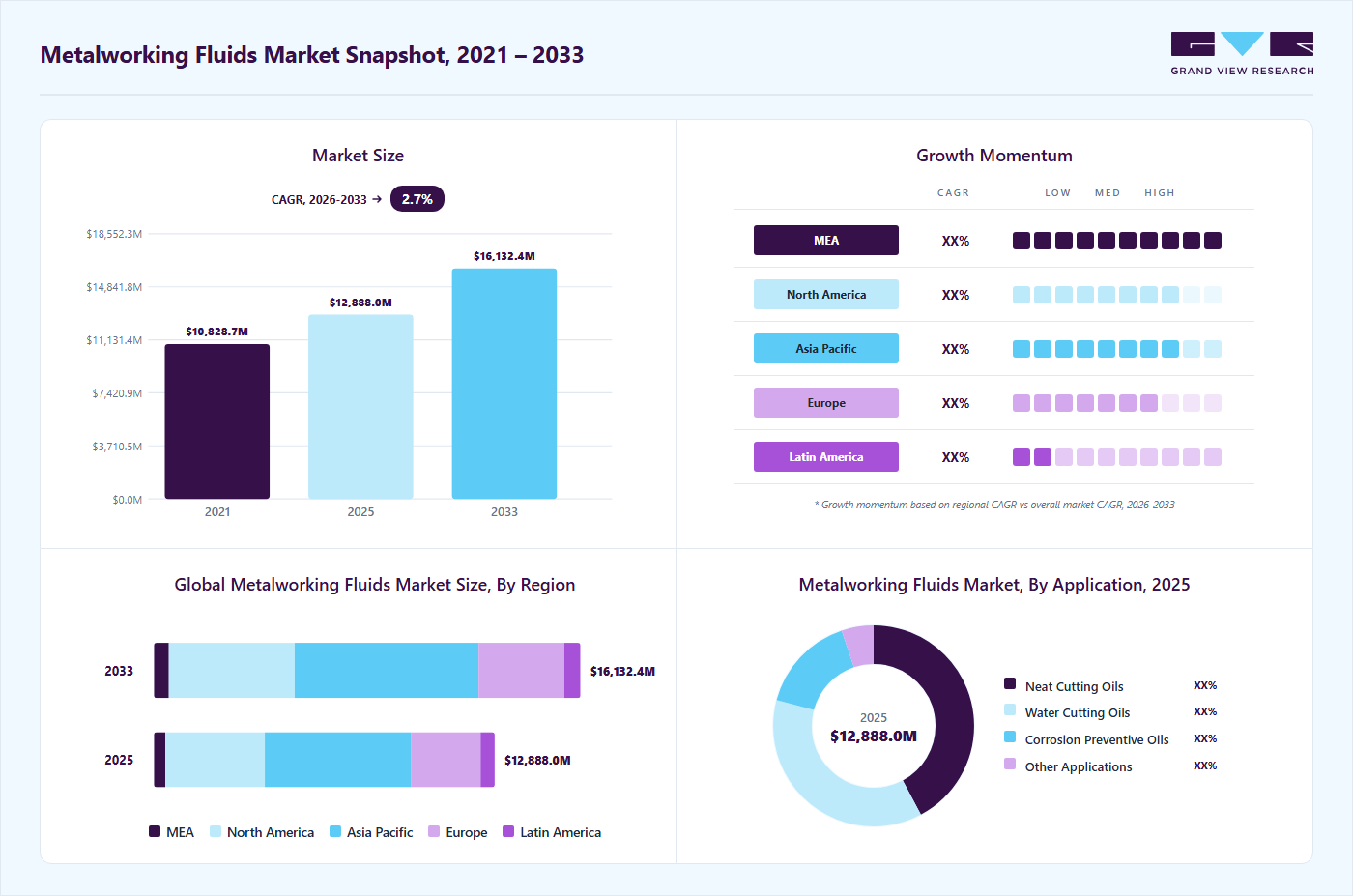

The global metalworking fluids market size was valued at USD 12.8 billion in 2025 and is projected to grow from USD 13.3 billion in 2026 to USD 16.1 billion by 2033, at a CAGR of 2.7% from 2026 to 2033. Asia Pacific dominated the global metalworking fluids market with the largest revenue share of 43.0% in 2025. The market growth is primarily fueled by increasing emphasis on sustainable manufacturing and environmentally responsible practices across industries.

Key Market Trends & Insights

- By product: Mineral-based metalworking fluids segment dominated the market, with a revenue share of 48.0% in 2025.

- By end use: Machinery segment held the largest market share of 41.7% in 2025.

- By industrial use: Construction segment led the market with the largest revenue share of 28.6% in 2025.

- By application: Neat cutting oils segment led the market with the largest revenue share of 42.1% in 2025.

Regional Highlights

- Largest regional market: Largest regional market: Asia Pacific (43.0% revenue share, 2025)

- Fastest-growing regional market: Middle East & Africa (highest CAGR, 2026-2033)

- The metalworking fluids industry in the China held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 12.8 Billion

- Estimated market size in 2026: USD 13.3 Billion

- Projected market size by 2033: USD 16.1 Billion

- CAGR (2026-2033): 2.7%

Regulatory bodies, corporations, and consumers are collectively advocating for reduced use of hazardous chemicals, lower carbon emissions, and minimized reliance on fossil-based raw materials. This shift is further supported by stringent environmental regulations, corporate ESG (Environmental, Social, and Governance) commitments, and growing demand for safer, biodegradable, and renewable metalworking fluid solutions in diverse applications.A key application driving the growth of the metalworking fluids industry is the automotive and machinery manufacturing sector. With increasing emphasis on reducing environmental impact, manufacturers are adopting bio-based and biodegradable additives in metalworking fluids to improve process efficiency while minimizing hazardous chemical usage. Companies are incorporating advanced coolant and lubricant formulations that enhance tool life, reduce energy consumption, and enable safer disposal practices. Leading OEMs and component manufacturers are collaborating with chemical producers to support sustainability initiatives and comply with regulations such as REACH in Europe and EPA guidelines in the United States. Consequently, automotive and industrial machining remain among the most dynamic and commercially impactful applications in the metalworking fluids industry.

")

In the aerospace and precision engineering industries, environmentally friendly water-miscible and synthetic fluids are increasingly replacing conventional mineral oil-based fluids. These sustainable alternatives improve corrosion protection, surface finish, and thermal stability while reducing toxic emissions and waste disposal concerns. Their biodegradable, non-toxic, and recyclable properties make them ideal for high-precision metalworking processes. In addition, these fluids support closed-loop recycling systems and circular manufacturing practices, helping industries meet stringent environmental and safety standards.

The energy and heavy machinery sector is also witnessing growth driven by innovations in metalworking fluids that enhance operational efficiency and minimize environmental impact. New formulations with renewable additives and improved heat transfer capabilities enable high-performance machining while reducing energy consumption and waste generation. Furthermore, recycling and reconditioning spent fluids for reuse aligns with circular economy objectives, promoting cleaner, safer, and more sustainable industrial operations. These developments support global efforts to lower carbon emissions and advance eco-friendly manufacturing practices.

Market Concentration & Characteristics

The metalworking fluids industry is moderately fragmented, with market leadership concentrated among several large, vertically integrated chemical and lubricant manufacturers. These key players leverage economies of scale, internal sourcing of renewable and bio-based raw materials, including natural oils, esters, and functional additives, and extensive global distribution networks to maintain a competitive edge. Their integration across the metalworking fluid value chain, from base oil blending to the formulation of specialized coolants, lubricants, and additive packages, enables improved cost efficiency, consistent product performance, and reliable supply. This strategic positioning allows them to effectively serve a wide range of end-use industries, including automotive, aerospace, industrial machinery, energy, and precision engineering, reinforcing their market influence and supporting broader adoption of sustainable metalworking solutions.

At the same time, emerging players in the Asia-Pacific and Middle East are steadily expanding their presence in the metalworking fluids industry by leveraging abundant renewable feedstock, cost-efficient energy infrastructure, and rising domestic demand for eco-friendly machining solutions. These regional manufacturers are supported by targeted investments in advanced lubricant blending facilities and bio-based additive production hubs strategically located within industrial and economic corridors. Their focus is on delivering cost-effective, scalable fluid solutions across high-demand segments such as automotive, industrial machinery, and precision engineering. This evolving landscape, characterized by global consolidation among established multinationals alongside regional cost-driven expansion, continues to reshape the competitive dynamics of the metalworking fluids industry.

However, the metalworking fluids industry also faces key challenges, including increasing environmental and regulatory scrutiny of specific chemical additives, such as amine derivatives and certain organophosphates. Regulatory authorities in North America and Europe have raised concerns regarding eco-toxicity, persistence, and potential health impacts of some fluid components, even if derived from renewable sources. These factors underscore the importance of compliance, continuous innovation, and transparent risk management in sustaining market growth.

Product Insights

The mineral-based metalworking fluids segment led the market with the largest revenue share of 48.0% in 2025, primarily due to their wide availability, cost-effectiveness, and versatility across various machining and forming processes. These fluids are derived from refined petroleum and are widely used in cutting, grinding, and forming operations, providing excellent lubrication, cooling, and corrosion protection. In addition to mineral-based fluids, synthetic and bio-based metalworking fluids are gaining traction due to their superior environmental profiles and specialized performance characteristics.

The synthetic-based metalworking fluids segment is the fastest-growing segment with a revenue CAGR of 3.0% during the forecast period. Synthetic fluids, formulated from chemical compounds such as esters, polyalkylene glycols, and organophosphates, offer enhanced thermal stability, longer service life, and reduced microbial growth. Bio-based fluids, derived from natural oils, esters, and other renewable feedstocks, are increasingly adopted in sustainable manufacturing practices, providing biodegradable, low-toxicity alternatives that align with corporate ESG goals and regulatory requirements. Together, these diverse fluid types enable manufacturers to optimize machining efficiency, reduce environmental impact, and meet evolving industry standards across sectors, including automotive, aerospace, and industrial machinery.

End Use Insights

The machinery segment led the market with the largest revenue share of 41.7% in 2025, driven by the widespread adoption of metalworking fluids in machine tool operations, heavy equipment manufacturing, and industrial machinery production. These fluids enhance machining efficiency, reduce tool wear, improve surface quality, and support sustainable manufacturing practices in high-demand machinery applications.

The transportation equipment is the fastest-growing segment with a revenue CAGR of 3.2% during the forecast period, driven by the increasing production of automobiles, aerospace components, and electric vehicles. Manufacturers are prioritizing high-performance fluids that enhance machining precision, reduce tool wear, and improve overall operational efficiency. This growth is further fueled by stringent quality and safety standards in the automotive and aerospace industries, encouraging the adoption of specialized metalworking solutions to support complex manufacturing processes.

Industrial End Use Insights

The construction segment led the market with the largest revenue share of 28.6% in 2025, driven by the extensive use of metalworking fluids in machinery, equipment fabrication, and on-site construction processes. These fluids enhance machining, cutting, and forming efficiency while providing corrosion protection and thermal stability for construction tools and components.

The automobile sector is driving significant growth with a revenue CAGR of 3.6% during the forecast period, as manufacturers increasingly adopt advanced machining technologies for engines, chassis, and precision components. Rising production of electric vehicles, stringent emission regulations, and a push for lightweight yet durable materials are accelerating demand for specialized metalworking fluids that enhance cutting efficiency, reduce tool wear, and ensure superior surface finish. Strategic investments by OEMs in high-precision manufacturing and automation are further reinforcing this segment as a key growth engine within the industrial end-use landscape.

Application Insights

The neat cutting oils segment led the market with the largest revenue share of 42.1% in 2025, driven by their extensive use in precision machining and high-performance cutting operations. These oils, which are typically undiluted and free from water, provide excellent lubrication, reduce tool wear, and improve surface finish, making them ideal for demanding metalworking processes such as turning, milling, and threading.

Water cutting oils represent the fastest growing segment in the global metalworking fluids industry, with a revenue CAGR of 3.1% during the forecast period, driven by their superior cooling, lubrication, and heat dissipation properties in high-speed machining operations. These emulsifiable oils are widely used in precision cutting, milling, grinding, and turning processes across automotive, aerospace, and industrial machinery manufacturing. Their water-based formulations reduce friction, minimize thermal deformation, and improve surface finish, while also lowering microbial growth and extending tool life.

Regional Insights

The metalworking fluids market in North America is witnessing robust growth in 2025, driven by stringent environmental regulations, rising corporate sustainability initiatives, and increasing adoption of eco-friendly fluid solutions across industries. Regulatory oversight from agencies such as the U.S. Environmental Protection Agency (EPA) and Environment and Climate Change Canada is encouraging the shift toward bio-based, biodegradable, and low-toxicity metalworking fluids. These sustainable solutions are widely used in automotive, aerospace, industrial machinery, and precision engineering sectors, where they support emission reduction, improve operational safety, and enhance manufacturing efficiency. The automotive and machinery industries remain key contributors, driven by the adoption of green fluids for high-performance machining, cutting, and forming operations. In addition, strong investments in R&D, green manufacturing technologies, and circular economy initiatives are accelerating commercialization. Growing demand for environmentally responsible products and transparent supply chains further reinforces North America’s position as a major market for sustainable metalworking fluids.

U.S. Metalworking Fluids Market Trends

The metalworking fluids market in the U.S. has witnessed notable growth, driven by stringent environmental regulations, growing awareness of sustainable manufacturing, and the automotive and industrial sectors’ shift toward eco-friendly practices. Biodegradable and low-toxicity metalworking fluids are increasingly adopted in machining, cutting, and finishing operations, providing effective lubrication, cooling, and corrosion protection while minimizing environmental and health risks. Products such as bio-based cutting oils, synthetic lubricants, and eco-friendly corrosion preventives offer safe, high-performance alternatives to conventional petroleum-based fluids, enabling manufacturers to comply with EPA and OSHA standards.

In addition, the expansion of electric vehicles (EVs), advanced industrial machinery, and green manufacturing initiatives is further accelerating demand for sustainable metalworking fluid solutions. As sustainability becomes a core requirement for both enterprises and regulators, eco-friendly fluids are playing a pivotal role in regulatory compliance, operational efficiency, and reducing the environmental footprint of U.S. manufacturing operations.

Asia Pacific Metalworking Fluids Market Trends

The metalworking fluids market in the Asia Pacific led the global market in 2025 with a 43.0% revenue share, driven by a growing manufacturing base and rising adoption of sustainable, bio-based fluids. Eco-friendly solutions are increasingly used across automotive, industrial machinery, aerospace, and precision engineering sectors to enhance efficiency while minimizing environmental impact.

Government initiatives, regulatory reforms, and innovation in China, Japan, and India such as biodegradable fluids and closed-loop recycling are accelerating adoption and reinforcing the region’s leadership in sustainable industrial practices.

China metalworking fluids marketled the Asia Pacific in 2025, fueled by its strong automotive, industrial machinery, and precision engineering sectors. Increasing adoption of eco-friendly, biodegradable fluids across machining, forming, and finishing operations is driven by their superior performance, reduced toxicity, and regulatory compliance. Leading manufacturers are integrating bio-based additives to enhance tool life, reduce waste, and promote safer workplaces, reinforcing China’s role as a hub for sustainable industrial practices in the region.

Europe Metalworking Fluids Market Trends

The metalworking fluids market in Europe is steadily growing, driven by strict environmental regulations, sustainability initiatives, and the adoption of bio-based, low-toxicity fluids. Policies such as REACH, the EU Green Deal, and the Circular Economy Action Plan are prompting manufacturers to replace petroleum-based fluids with biodegradable alternatives. Widely used across automotive, packaging, industrial machinery, aerospace, and construction sectors, these green fluids support emission reduction, workplace safety, and efficient manufacturing. Strong R&D, supportive policies, and industry-research collaborations reinforce Europe’s leadership in sustainable metalworking fluid practices globally.

Germany metalworking fluids market is witnessing steady growth, driven by stringent environmental regulations, strong industrial sustainability commitments, and the automotive and machinery sectors’ shift toward low-emission, resource-efficient practices. Germany’s robust manufacturing base is increasingly adopting bio-based metalworking fluids, green cutting oils, and low-toxicity lubricant formulations across machining, forming, finishing, and surface treatment applications. Eco-friendly fluid solutions are gaining traction in automotive production, component processing, and industrial maintenance, providing high performance.

Middle East & Africa Metalworking Fluids Market Trends

The metalworking fluids market in the MEA is projected to grow at the fastest CAGR of 3.3% during the forecast period, driven by sustainability initiatives, regulatory focus, and industrial expansion. Adoption of bio-based and low-toxicity fluids is rising across automotive, construction, machinery, and precision engineering sectors. In the Middle East, cost-competitive energy and feedstocks support scalable production, while in Africa, growing demand for sustainable manufacturing and industrial services is boosting market uptake. Foreign investment, technology partnerships, and circular economy practices are expected to further accelerate the adoption of eco-friendly metalworking fluids in the region.

Latin America Metalworking Fluids Market Trends

The metalworking fluids market in Latin America is steadily growing, driven by abundant renewable feedstocks like biomass and sugarcane, expanding sustainability initiatives, and stricter environmental regulations. Brazil and Mexico lead adoption through bio-refinery programs, industrial decarbonization, and export-oriented manufacturing. Increasing use of biodegradable and eco-friendly fluids across automotive, agriculture, packaging, and industrial sectors, along with investments and collaborations between local and global producers, is strengthening the region’s role in the global metalworking fluids industry.

Key Metalworking Fluids Company Insights

Some of the key players operating in the metalworking fluids industry include Dow and Evonik.

-

ExxonMobil Corporation, headquartered in Irving, Texas, is a leading and well-established player in the global metalworking fluids industry, leveraging decades of expertise in base oils, lubricants, and specialty chemical formulations. The company offers a comprehensive portfolio of high-performance metalworking fluids, including mineral, synthetic, and bio-based solutions, designed for diverse industrial and precision machining applications. These fluids provide critical functionalities such as lubrication, cooling, corrosion protection, anti-wear performance, and thermal stability, serving a wide range of end-use industries, including automotive, aerospace, industrial machinery, construction, and metal fabrication.

ExxonMobil’s vertically integrated production network and extensive global supply chain enable the delivery of reliable, scalable, and high-quality fluid solutions with strong regional adaptability. Its advanced R&D facilities across the U.S., Europe, and Asia focus intensively on innovation in sustainable metalworking fluid technologies, driving the development of eco-friendly, low-toxicity, and biodegradable formulations that meet stringent environmental and regulatory standards.

Key Metalworking Fluids Companies:

The following key companies have been profiled for this study on the metalworking fluids market.

- Houghton International, Inc.

- Blaser Swisslube AG

- BP plc

- Total S.A.

- FUCHS

- Chevron Corporation

- China Petroleum & Chemical Corporation

- Kuwait Petroleum Corp.

- Idemitsu Kosan Co., Ltd.

- Exxon Mobil corporation

Recent Developments

-

In February 2025, Zavenir Daubert, a leading specialty chemicals manufacturer renowned for corrosion protection and metalworking fluid solutions, inaugurated India’s first integrated, future-ready manufacturing facility in Binola, Haryana. The facility represents a key milestone in the company’s growth strategy, with a targeted revenue of approximately USD 120 million over the next five years. This expansion enhances production capacity, improves supply chain efficiency, and strengthens regional presence in the Asia Pacific market. Such developments are expected to drive market growth by increasing the availability of advanced metalworking fluids, supporting the adoption of sustainable and high-performance solutions across automotive, industrial machinery, and construction sectors.

Metalworking Fluids Market Report Scope

Report Attribute

Details

Market size in 2025

USD 12.8 Billion

Market size value in 2026

USD 13.3 Billion

Revenue forecast in 2033

USD 16.1 Billion

Growth rate

CAGR of 2.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2018 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, Volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, end use, industrial end use, region

Regional scope

North America; Europe; Asia Pacific; MEA; Latin America

Country scope

U.S.; Canada; Mexico; Germany; Russia; France; Spain; Italy; UK; Switzerland; Denmark; Norway; Belgium; Poland; Czech Republic; Turkey; Sweden; Finland; China; India; Japan; South Korea; Singapore; Malaysia; Thailand; Australia; New Zealand; Brazil; Argentina; Saudi Arabia; South Africa

Key companies profiled

Exxon Mobil Corp.; Houghton International, Inc.; Blaser Swisslube AG; BP plc; Total S.A.; FUCHS; Chevron Corporation; China Petroleum & Chemical Corporation; Kuwait Petroleum Corp.; Idemitsu Kosan Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Metalworking Fluids Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2033. For this study, Grand View Research has segmented the global metalworking fluids market report based on product, application, end use, industrial end use, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Mineral

-

Synthetic

-

Bio-based

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Neat Cutting Oils

-

Water Cutting Oils

-

Corrosion Preventive Oils

-

Other Applications

-

-

End Use Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Metal fabrication

-

Transportation equipment

-

Machinery

-

Other End-Use

-

-

Industrial End Use Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Construction

-

Electrical & Power

-

Agriculture

-

Automobile

-

Aerospace

-

Rail

-

Marine

-

Telecommunication

-

Healthcare

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

Russia

-

France

-

Spain

-

Italy

-

UK

-

Switzerland

-

Denmark

-

Norway

-

Belgium

-

Poland

-

Czech Republic

-

Turkey

-

Sweden

-

Finland

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Singapore

-

Malaysia

-

Thailand

-

Australia

-

New Zealand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global metalworking fluids market is expected to grow at a compound annual growth rate of 2.7% from 2026 to 2033 to reach USD 16.1 billion by 2033.

The mineral segment held the largest share of over 48.0% in 2025. The high share has been attributed to the consumption of mineral-based oils owing to their low cost. Due to price-conscious consumers, small- and medium-scale manufacturers typically use mineral oil-based MWFs. Over the forecast period, this is expected to impact the market growth.

Key factors that are driving the metalworking fluids market growth include the growth of the heavy machinery industry in the developing economies of Asia Pacific and Latin America.

Some of the key players operating in the metalworking fluids market include Exxon Mobil Corp., Houghton International, Inc., Blaser Swisslube AG, BP plc, Total S.A., FUCHS, Chevron Corporation, China Petroleum & Chemical Corporation, Kuwait Petroleum Corp., Idemitsu Kosan Co., Ltd.

Asia Pacific dominated the global metalworking fluids market with the largest revenue share of 43.0% in 2025.

Middle East & Africa is the fastest-growing region over the forecast period.

Machinery segment held the largest revenue share of 41.7% in 2025, driven by the widespread adoption of metalworking fluids in machine tool operations, heavy equipment manufacturing, and industrial machinery production.

Construction segment led the market with the largest revenue share of 28.6% in 2025

The global metalworking fluids market size was estimated at USD 12.8 billion in 2025 and is expected to reach USD 13.3 billion in 2026.

About the Author(s)

Organic Chemicals Research Team

Bulk Chemicals · Organic ChemicalsThis report was authored by the organic chemicals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the organic chemicals segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.