- Home

- »

- Medical Devices

- »

-

Active Pharmaceutical Ingredient CDMO Market Report, 2026-2033GVR Report cover

![Active Pharmaceutical Ingredient CDMO Market (2026 - 2033)Report]()

Active Pharmaceutical Ingredient CDMO Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Traditional API, HP-API, Biologics) By Synthesis (Synthetic, Biotech), By Drug (Innovative, Generics), By Application, By Workflow, By Region, And Segment Forecasts

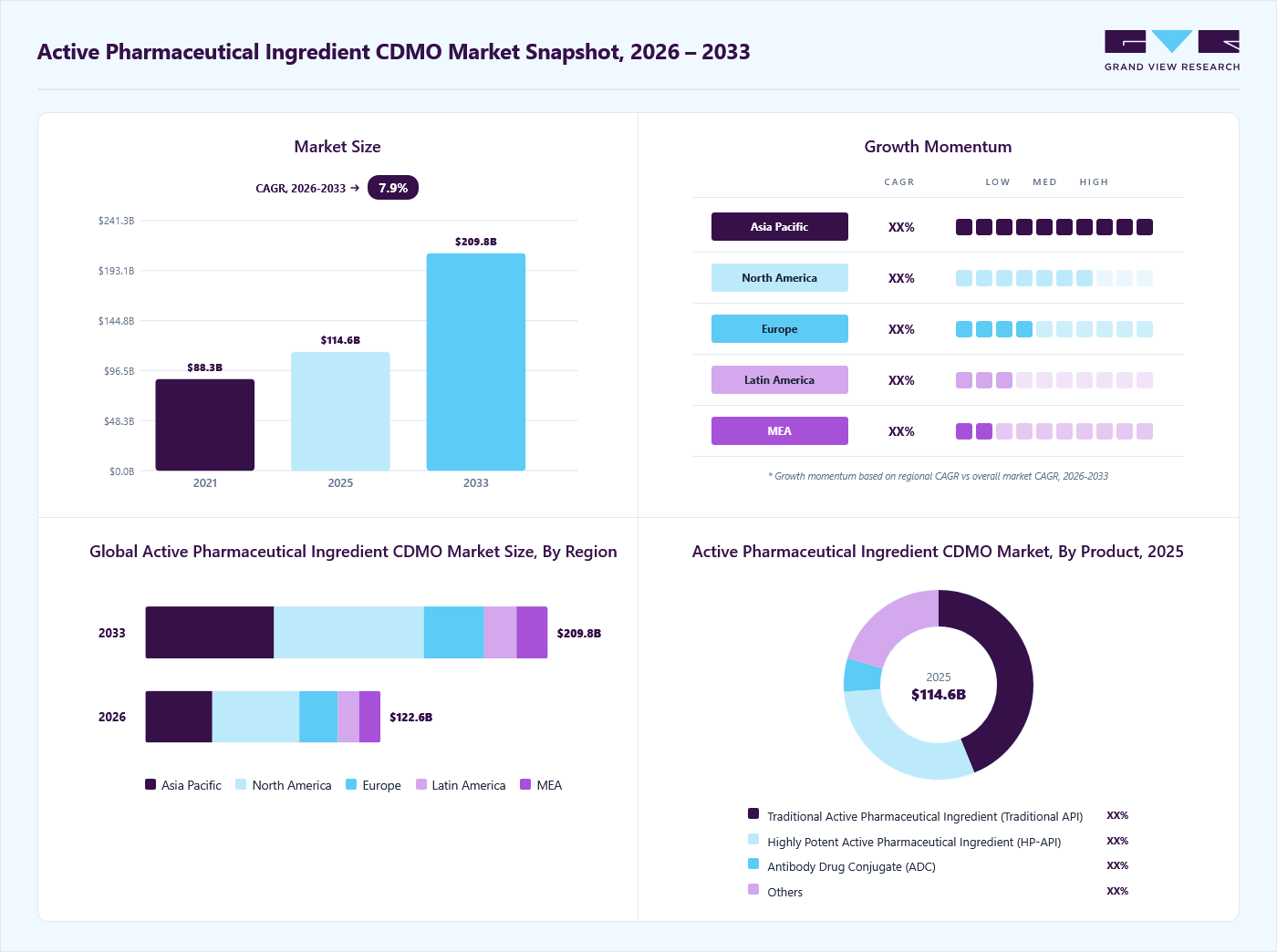

Market Size, 2025

$114.6BMarket Estimate, 2026

$122.6BMarket Forecast, 2033

$209.8BCAGR, 2026–2033

7.9%Active Pharmaceutical Ingredient CDMO Market Summary

The global active pharmaceutical ingredient CDMO market size was valued at USD 114.6 billion in 2025 and is projected to grow from USD 122.6 billion in 2026 to USD 209.8 billion by 2033, at a CAGR of 7.9% from 2026 to 2033. The North America global market accounted for the largest revenue share of 37.0% in 2025. The market is driven due to the increasing demand for scalable and cost-efficient drug development solutions, growing outsourcing trends among pharmaceutical companies to reduce operational costs and focus on core competencies, and increasing R&D activities in specialty and complex APIs.

Key Market Trends & Insights

- By product: Traditional API segment accounted for the largest revenue share of 43.8% in 2025.

- By synthesis: Biotech segment accounted for the largest revenue share of 26.7% in 2025.

- By drug: Generics segment accounted for the largest revenue share of 26.1% in 2025.

Regional Highlights

- Largest regional market: North America (37.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 114.6 Billion

- Estimated market size in 2026: USD 122.6 Billion

- Projected market size by 2033: USD 209.8 Billion

- CAGR (2026-2033): 7.9%

Moreover, the growing biosimilars and biologics segment, increasing prevalence of chronic diseases, patent expirations of blockbuster drugs, and advancements in manufacturing technologies such as continuous manufacturing and high-potency APIs are further contributing to the industry growth. In addition, several pharmaceutical and biotechnology companies are increasingly outsourcing their API manufacturing services to CDMOs, which is also one of the major factors contributing to market growth. The increasing complexity of drug molecules and the cost advantages offered by CDMOs are the major contributors to the shift from in-house capabilities to outsourcing. Furthermore, the increasing prevalence of chronic diseases globally has intensified the demand for innovative therapies, further pushing the CDMOs to focus on large-scale production, faster development, and regulatory compliance.")

Furthermore, increasing pipelines of biologics and biosimilars and a growing demand for HPAPIs contribute to the increasing opportunities. CDMOs have higher levels of expertise and advanced technologies, making them the preferred choice for biotechnology and pharmaceutical companies looking for scalable, compliant, and efficient manufacturing solutions. Moreover, patent expirations of branded and blockbuster drugs are boosting the demand for generic APIs. Thus, these factors are changing the market's competitive landscape, further contributing to the market growth.

Market Dynamics

The API CDMO market is experiencing sustained growth as pharmaceutical and biotechnology companies increasingly outsource development and manufacturing activities to reduce costs, accelerate timelines, and access specialized capabilities. Growing biologics pipelines, rising demand for high-potency APIs (HPAPIs), increasing clinical trial activity, and the need for regulatory-compliant global supply chains are reshaping competitive dynamics.

The primary growth driver for the API CDMO market is the increasing outsourcing of API development and manufacturing by pharmaceutical and biotechnology companies. Drug developers are under pressure to reduce capital expenditure, accelerate product timelines, and improve operational efficiency. As a result, many organizations are shifting from captive manufacturing models toward specialized CDMO partnerships that provide end-to-end development, scale-up, analytical, regulatory, and commercial manufacturing services.

The growing complexity of modern drug pipelines is further accelerating outsourcing adoption. Pharmaceutical innovation is increasingly focused on biologics, antibody-drug conjugates (ADCs), peptide therapeutics, oligonucleotides, and highly potent APIs. Manufacturing these molecules requires specialized containment infrastructure, advanced process development expertise, and regulatory capabilities that are often uneconomical to build internally. Consequently, sponsors are relying on CDMOs with established technological platforms.

Additionally, continuous manufacturing, flow chemistry, single-use bioprocessing systems, and advanced analytical technologies are improving manufacturing efficiency and attracting greater outsourcing spending. As pharmaceutical companies prioritize asset-light operating models, API CDMOs are expected to remain strategic partners throughout the drug lifecycle.

API manufacturing operates within one of the most heavily regulated environments globally, requiring compliance with FDA, EMA, PMDA, MHRA, and numerous country-specific quality standards. Maintaining cGMP compliance across development, scale-up, validation, and commercial production adds substantial operational costs and increases execution risk.

The growing shift toward biologics, HPAPIs, and complex synthetic molecules further amplifies these challenges. Such products require specialized containment facilities, advanced process controls, highly trained personnel, and extensive quality monitoring systems. Any deviation in manufacturing processes can result in regulatory observations, production delays, or supply disruptions.

Analyst Perspective

The API CDMO market is expected to remain one of the fastest-growing segments within pharmaceutical outsourcing, supported by rising biologics adoption, increasing API complexity, and continued movement toward asset-light operating models. Demand for HPAPIs, biologics, and advanced manufacturing technologies is likely to drive significant investment in specialized production infrastructure and integrated service platforms. Companies capable of providing end-to-end development, regulatory support, and commercial-scale manufacturing across multiple modalities will be best positioned to capture market share. Over the next decade, capacity expansion, technological differentiation, and supply-chain resilience initiatives are expected to emerge as the primary competitive determinants shaping market leadership.

Opportunity Analysis

Increasing adoption of targeted therapies, monoclonal antibodies, and advanced biologics drugs is fueling the demand for CDMOs, with large-scale biomanufacturing capabilities and biologics expertise. CDMOs are increasingly investing in advanced facilities to meet the growing demand for these specialized therapies, equipped with advanced cell culture platforms, enabling them to offer high-quality and scalable solutions for biotechnology and pharmaceutical companies. Besides, increasing demand for HPAPIs in the field of immunology, oncology, and rare disease treatments further boosts the demand for APIs, contributing to market growth.

Furthermore, patent expirations of blockbuster drugs are driving the demand for APIs in the generics market, as several pharmaceutical companies are increasingly considering cost-effective solutions. Emerging regions such as the Asia Pacific, Latin America, and the Middle East are creating significant opportunities, further supported by government initiatives and local demand for affordable medicines.

Technological Advancements

Technological advancements are enhancing quality, scalability, and efficiency across development and manufacturing stages. Furthermore, flow chemistry and continuous manufacturing are increasingly being adopted to reduce costs, enable faster production cycles, and improve reproducibility. Moreover, advanced bioprocessing platforms such as single-use bioreactors, perfusion systems, and high-density cell culture technologies are accelerating manufacturing of large-scale biologics and complex APIs. Thus, constant advancement in this field is creating significant competitive advantages for CDMOs, enabling them to offer higher quality and more flexible services to meet the growing demand of pharmaceutical companies.

Product Insights

On the basis of product, the market is classified into traditional API, HP-API, and biologics. The traditional API segment accounted for the largest revenue share of 43.8% in 2025. The segment's growth is attributed to significant applications of these APIs in the generic drug manufacturing, a growing number of patent expirations, and increasing demand for small-molecule drugs. In addition, the relatively lower production cost and cost-effectiveness are further driving the adoption of traditional APIs.

The biologics segment is anticipated to grow at the fastest CAGR during the forecast period. The growth outlook is driven due to the increasing adoption of targeted cancer therapies, the growing pipeline of oncology-based biologics, and the increasing approvals of innovative drugs. Moreover, CDMOs are increasingly investing in advancing their specialized facilities with high containment capabilities, advanced bioconjugation technologies, and scalable manufacturing platforms to support complex biological development, further accelerating the segment growth.

Synthesis Insights

In terms of synthesis, the market is segregated into synthetic and biotech. The biotech segment is anticipated to grow at the fastest rate with 8.0% CAGR, from 20026 to 2033. The growth of the segment comes in the wake of increasing use of chemical synthesis to manufacture small molecule APIs, along with the established infrastructure and technical expertise available with CDMOs. Furthermore, the increasing demand for generic drugs, coupled with growing reliance on small molecules to treat chronic conditions, including diabetes, cardiovascular diseases, and infectious diseases, further contributes to the segment’s dominance.

The biotech segment is anticipated to grow at the fastest CAGR during the forecast period. The segment growth is mainly due to the increasing demand for biosimilars and biologics, increasing prevalence of chronic diseases such as autoimmune disorders and cancers, and the growing shift of pharmaceutical companies towards extensive molecule development. Moreover, several CDMOs are heavily investing to advance their existing facilities, installing single-use bioprocessing technologies, advanced fermentation systems, and cell culture, which may drive the segment's market growth in the upcoming years.

Drug Insights

Based on drug, the market is segregated into innovative and generic. The generics segment is anticipated to grow at the fastest rate with 9.7% CAGR, from 20026 to 2033. The growth is largely attributed to increasing investment in novel drug development coupled with growing demand for specialty medicines and biologics. Besides, the growing pipeline of innovative drugs, continuous R&D activities, and favorable regulatory approvals have further solidified the dominance of this segment, as pharmaceutical companies increasingly rely on specialized expertise.

The generics segment is poised to grow at the fastest CAGR during the forecast period. This growth stems against the backdrop of the increasing number of branded drug patent expirations, growing demand for affordable treatment options, and increasing cost-containment pressures in healthcare systems. Moreover, rising government initiatives, expanding access to healthcare in emerging markets, and the significant role of CDMOs in providing cost-efficient large-scale API production would boost the adoption of generic drugs.

Application Insights

With respect to application, the market is segregated into oncology, hormonal, glaucoma, cardiovascular disease, diabetes, and others. The oncology segment registered the largest market share in 2025 with 35.7% share, due to the increasing burden of cancer globally, rising demand for personalized medicines, and growing investments by pharmaceutical companies in oncology research and development.

The glaucoma segment is expected to grow at the second fastest CAGR during the forecast period. The projection comes on the back of the increasing cases of glaucoma, which is driving the demand for advanced therapies for long-term management. In essence, the rising geriatric population is leading to higher cases of glaucoma, which is further increasing the demand for effective treatment options and driving the need for large-scale manufacturing support from the CDMOs.

Workflow Insights

With regards to workflow, the market is segregated into clinical and commercial. The clinical segment is anticipated to grow at the fastest rate with 8.4% CAGR, from 20026 to 2033, owing to the large-scale production requirements of approved drugs, rising demand for contract manufacturing of generics and biosimilars, and the cost advantages that pharmaceutical companies gain. In addition, the presence of well-established manufacturing facilities, advanced technologies for high-volume production, and the ability of CDMOs to ensure regulatory compliance and global supply chain distribution is also contributing to market growth.

The clinical segment is anticipated to grow at the fastest CAGR over the forecast period. The segment growth is driven by the growing number of drug candidates entering clinical trials, increasing investments in research and development activities by pharmaceutical companies, and growing reliance on CDMOs for early-stage development and small-batch manufacturing. Moreover, increasing demand for CDMOs in clinical workflows, which offer specialized services such as formulation development, analytical testing, and regulatory support, is also projected to contribute to the segment's growth.

Regional Insights

The North America active pharmaceutical ingredient CDMO industry accounted for the largest revenue share of 37.0% in 2025. This is attributed to the regions advanced manufacturing facilities, higher concentration of clinical trials, and growing spending in research and development activities by the pharmaceutical companies.

U.S. Active Pharmaceutical Ingredient CDMO Market Trends

The active pharmaceutical ingredient CDMO market in the U.S. held the largest share in the North America region in 2025. The country’s growth is due to high R&D spending, strong venture funding, and rapid commercialization of CAR-T and gene therapies. The country’s robust network of CDMOs, along with early regulatory approvals, fuels consistent outsourcing demand.

Europe Active Pharmaceutical Ingredient CDMO Market Trends

The Europe active pharmaceutical ingredient CDMO industry is expected to grow significantly due to the region’s favorable policies, such as the EMA’s PRIME designation and strong academic-industry collaborations. The region is witnessing steady growth in clinical pipelines, with CDMOs investing heavily in capacity expansion.

The active pharmaceutical ingredient CDMO industry in Germany captured a notable share in 2024, owing to the country’s strong biopharma R&D, clinical trial activity, and government incentives for advanced therapies. Its manufacturing base and skilled workforce make it a preferred hub for CDMO expansion.

The UK active pharmaceutical ingredient CDMO industry held a significant share in 2024. The growth of the market is due to investments in advanced therapy medicinal products (ATMP) infrastructure.

Asia Pacific Active Pharmaceutical Ingredient CDMO Market Trends

The Asia Pacific active pharmaceutical ingredient CDMO industry is anticipated to witness the fastest CAGR over the estimated timeline. The regional growth is attributed to rising biotech investments, expanding patient pools, and lower manufacturing costs. Governments in countries such as China, Japan, and South Korea are actively supporting local ATMP manufacturing hubs.

The active pharmaceutical ingredient CDMO industry in China held the largest share in 2024. The growth is due to the country’s surge in clinical trials, growing domestic biotech companies, and government-backed funding for cell and gene therapy infrastructure. Strategic alliances with international CDMOs are further boosting the market’s scale-up capacity.

The Japan active pharmaceutical ingredient CDMO industry is expected to grow over the forecast period due toits accelerated regulatory approval system for regenerative medicines. The country’s focus on stem cell and gene-modified therapies, along with partnerships with global CDMOs, is driving rapid market growth.

The active pharmaceutical ingredient CDMO industry in India is anticipated to grow at the lucrative CAGR over the forecast period. The country’s market growth is due to the lower operational costs, skilled scientific workforce, and growing R&D investments from both domestic and multinational companies.

Key Active Pharmaceutical Ingredient CDMO Company Insights

The major players operating across the market are focused on adopting inorganic strategic initiatives such as mergers & acquisitions and partnerships. Moreover, companies have emphasized technological innovations to augment their market position. For instance, in November 2023, Hovione expanded its nasal drug delivery through a partnership with IDC (Industrial Design Consultancy), introducing innovative nasal powder devices for local, systemic, and nose-to-brain drug delivery. The partnership enhanced Hovione's integrated nasal drug development and manufacturing services.

Key Active Pharmaceutical Ingredient CDMO Companies

The following key companies have been profiled for this study on the active pharmaceutical ingredient CDMO market.

-

Cambrex Corporation

-

Recipharm AB

-

Thermo Fisher Scientific Inc.

-

CordenPharma International

-

Samsung Biologics

-

Lonza

-

Catalent, Inc

-

Siegfried Holding AG

-

Piramal Pharma Solutions

-

Boehringer Ingelheim International GmbH

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Lonza, Thermo Fisher Scientific Inc., Catalent, Inc., Samsung Biologics)

- Expand integrated development-to-commercial manufacturing capabilities across small molecules, biologics, and HPAPIs.

- Pursue strategic acquisitions and capacity expansion to strengthen global manufacturing footprints.

- Established regulatory track record with proven inspection readiness across major markets.

- Broad technology platforms and ability to support large-scale commercial supply.

- Higher operating costs and longer decision-making cycles compared to niche providers.

- Capacity utilization pressures may reduce flexibility for smaller or early-stage projects.

Emerging Players (Cambrex Corporation, Recipharm AB)

- Focus on niche technologies such as HPAPIs, complex chemistry, flow chemistry, and specialized biologics.

- Build flexible, customer-centric models targeting emerging biotech innovators.

- Faster project onboarding and greater operational agility.

- Specialized expertise in complex molecules and high-value therapeutic segments.

- Limited global manufacturing scale and commercial supply capabilities.

- Greater dependence on a concentrated customer base and project pipeline.

Recent Developments

-

In June 2025, Recipharm announced that it had secured several major product development contracts, which aimed to further strengthen the company’s leadership in Blow-Fill-Seal (BFS) technology.

-

In December 2024, Cambrex inked an agreement with Lilly which aimed to deliver faster access to clinical development capabilities for Lilly’s biotech collaborators.

Active Pharmaceutical Ingredient CDMO Market Report Scope

Report Attribute

Details

Market size in 2025

USD 114.6 billion

Estimated market size in 2026

USD 122.6 billion

Projected market size by 2033

USD 209.8 billion

Growth rate

CAGR of 7.9% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, synthesis, drug, application, workflow, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; China; Japan; India; South Korea; Australia; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait

Key companies profiled

Cambrex Corporation, Recipharm AB, Thermo Fisher Scientific Inc., CordenPharma International, Samsung Biologics, Lonza, Catalent, Inc, Siegfried Holding AG, Piramal Pharma Solutions, Boehringer Ingelheim International GmbH

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Active Pharmaceutical Ingredient CDMO Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global active pharmaceutical ingredient CDMO market report based on product, synthesis, drug, application, workflow, and region:

-

Product Outlook (Revenue, USD Billion, 2021 - 2033)

-

Traditional Active Pharmaceutical Ingredient (Traditional API)

-

Highly Potent Active Pharmaceutical Ingredient (HP-API)

-

Biologics

-

-

Synthesis Outlook (Revenue, USD Billion, 2021 - 2033)

-

Synthetic

-

Biotech

-

-

Drug Outlook (Revenue, USD Billion, 2021 - 2033)

-

Innovative

-

Generics

-

-

Workflow Outlook (Revenue, USD Billion, 2021 - 2033)

-

Clinical

-

Commercial

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Oncology

-

Hormonal

-

Glaucoma

-

Cardiovascular disease

-

Diabetes

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Norway

-

Sweden

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

Oman

-

Qatar

-

-

Research Methodology

Segment Definition

Segment

Definition

Product

Traditional API

Small-molecule APIs manufactured using conventional chemical synthesis processes. Revenue includes process development, scale-up, and commercial production.

HP-API

Highly potent APIs requiring specialized containment facilities. Revenue includes high-containment manufacturing and handling services.

Biologics

Biologically derived APIs such as proteins, antibodies, and recombinant products. Revenue reflects biologic process development and manufacturing contracts.

Synthesis

Synthetic

APIs produced through chemical synthesis routes. Revenue includes process chemistry and manufacturing services.

Biotech

APIs produced through fermentation, cell culture, or recombinant technologies. Revenue includes upstream and downstream bioprocessing services.

Drug Type

Innovative

APIs supporting novel drug candidates and patented therapeutics. Revenue driven by development-intensive programs.

Generics

APIs supporting off-patent drugs. Revenue derived from cost-efficient large-scale manufacturing contracts.

Workflow

Clinical

Services supporting preclinical through clinical-stage manufacturing, including small-batch production and process development.

Commercial

Large-scale manufacturing services supporting approved products and market supply.

Application

Oncology

APIs used in cancer therapies including targeted therapies and cytotoxic drugs.

Hormonal

APIs used in endocrine and hormone-related treatments.

Glaucoma

APIs incorporated into ophthalmic therapies for glaucoma management.

Cardiovascular Disease

APIs utilized in cardiac and vascular disease treatments.

Diabetes

APIs used in anti-diabetic therapeutics and metabolic disease management.

Others

APIs serving infectious diseases, neurology, respiratory, immunology, and additional therapeutic categories.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

API CDMO Market Trends & Opportunity Assessment

Assessment of outsourcing trends, API demand by product type, synthesis platform, drug category, therapeutic area, clinical/commercial workflows, capacity expansion activities, and regional growth opportunities.

Identifies high-growth outsourcing segments, investment hotspots, emerging technologies, unmet manufacturing needs, and expansion opportunities.

Competitive Landscape & Market Share Assessment

Evaluation of established and emerging CDMOs based on manufacturing scale, technology capabilities, regulatory track record, geographic reach, partnerships, and service integration.

Highlights competitive intensity, white-space opportunities, differentiation strategies, partnership potential, and market entry pathways.

Technology, Capacity & Regulatory Landscape Review

Analysis of HPAPI manufacturing, biologics platforms, continuous manufacturing, flow chemistry, digital manufacturing, containment technologies, FDA/EMA compliance trends, and supply chain resilience initiatives.

Supports investment prioritization, capacity planning, technology roadmap development, regulatory readiness, and long-term growth strategies.

Frequently Asked Questions About This Report

The global active pharmaceutical ingredient CDMO market size was estimated at USD 114.6 billion in 2025 and is expected to reach USD 122.6 billion in 2026.

The global active pharmaceutical ingredient CDMO market is expected to grow at a compound annual growth rate of 7.9% from 2026 to 2033 to reach USD 209.8 billion by 2033

Some of the key market players include Lonza, LabCorp, Thermo Fisher Scientific, Inc., Recipharm AB, Catalent, Inc., Siegfried Holding AG, Samsung Biologics, Piramal Pharma Solutions, WuXi AppTec, Inc., Bushu Pharmaceuticals Ltd., CordenPharma International, Cambrex Corporation, Boehringer Ingelheim International GmbH

Key factors that are driving the market growth include increasing pharmaceutical R&D investments, demand for genetic drugs, biologic innovations, and the rise in the prevalence of cancer and age-related disorders.

North America dominated the active pharmaceutical ingredient CDMO market and accounted for the largest revenue share of 37.0% in 2025. The regions growth is attributed to the strong presence of leading pharmaceutical and biotechnology companies, well-established manufacturing infrastructure, and significant investments in advanced technologies such as continuous manufacturing and high-potency API production.

Traditional API dominated the product segment with 43.8% share in 2025.

Based on drug, the market is segregated into innovative and generic. The generics segment is anticipated to grow at the fastest rate with 9.7% CAGR, from 20026 to 2033.

Oncology dominated the application segment with 35.7% share in 2025.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.