- Home

- »

- Plastics, Polymers & Resins

- »

-

Advanced Packaging Market Size, Growth Report, 2026-2033GVR Report cover

![Advanced Packaging Market (2026 - 2033)Report]()

Advanced Packaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Packaging Type (Flip-Chip, Fan-Out WLP, Embedded-Die, Fan-In WLP, 2.5D/3D), By Application (Automotive, Industrial, Healthcare, Other applications), By Region, And Segment Forecasts

Market Size, 2025

$41.7BMarket Estimate, 2026

$43.9BMarket Forecast, 2033

$66.0BCAGR, 2026–2033

6.0%Advanced Packaging Market Summary

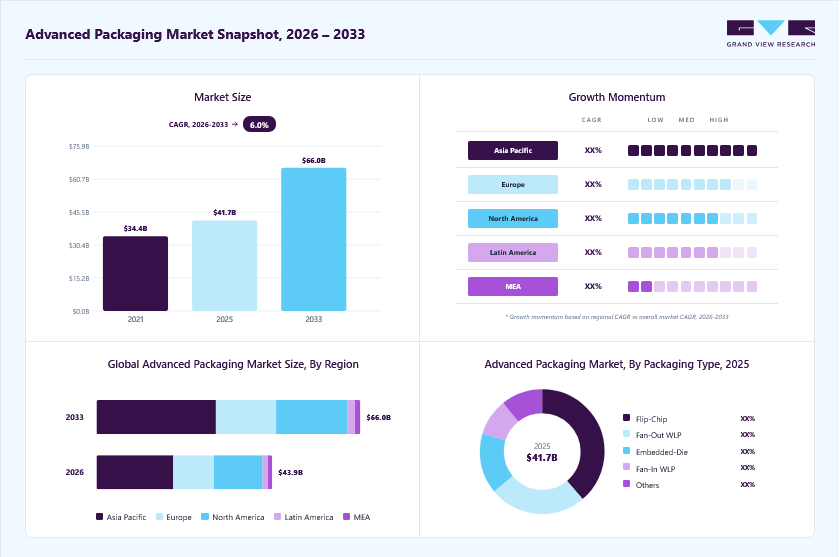

The global advanced packaging market size was valued at USD 41.7 billion in 2025 and is projected to grow from USD 43.9 billion in 2026 to USD 66.0 billion by 2033, at a CAGR of 6.0% from 2026 to 2033. Asia Pacific dominated the global market, accounting for the largest revenue share of 43.5% in 2025. The growth is driven by demand for high-performance computing, AI, and miniaturized devices, enabling higher density, better performance, and improved thermal efficiency across key sectors.

Key Market Trends & Insights

- By packaging type: Embedded-die segment is expected to grow at a CAGR of 6.6% from 2026 to 2033 in terms of revenue.

- By application: Automotive segment is expected to grow at a CAGR of 6.6% from 2026 to 2033 in terms of revenue.

Regional Highlights

- Largest regional market: Asia Pacific (43.5% revenue share, 2025)

- By country: The China advanced packaging industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 41.7 Billion

- Estimated market size in 2026: USD 43.9 Billion

- Projected market size by 2033: USD 66.0 Billion

- CAGR (2026-2033): 6.0%

The shift beyond Moore’s Law toward heterogeneous integration and 3D packaging is further accelerating its role in next-generation semiconductor innovation. The market is experiencing strong growth as semiconductor manufacturers transition from conventional packaging approaches to more advanced solutions that enable higher performance, reduced form factors, and improved power efficiency. This shift is particularly important in high-growth applications such as artificial intelligence, high-performance computing, and data centers, where traditional scaling is reaching its limits. Advanced packaging technologies facilitate greater integration of multiple chips, thereby enhancing overall system functionality and performance.

")

Furthermore, the increasing need for cost optimization and design flexibility is significantly supporting market expansion. Advanced packaging enables the adoption of chiplet architectures, heterogeneous integration, and system-in-package designs, allowing manufacturers to streamline production and improve functional density. These capabilities help reduce overall system costs while delivering enhanced performance, making advanced packaging a critical component in next-generation semiconductor design and manufacturing.

The rising emphasis on energy efficiency and sustainability is also contributing to market growth. Advanced packaging solutions enable improved thermal management and lower power consumption, both essential for modern electronic systems. In addition, efficient material utilization and optimized manufacturing processes help minimize waste, aligning with evolving environmental regulations and corporate sustainability objectives across the semiconductor value chain.

Moreover, the expansion of end-use industries continues to drive demand for advanced packaging technologies. Key sectors such as consumer electronics, automotive, including electric and autonomous vehicles, telecommunications driven by 5G and IoT, and industrial automation are increasingly relying on high-performance, compact, and reliable semiconductor solutions. Ongoing digital transformation, coupled with rising investments in advanced technologies, is expected to sustain the steady growth of the market.

Market Concentration & Characteristics

The advanced packaging market is characterized by high innovation intensity and strong demand driven by AI, high-performance computing (HPC), and data center applications. Technologies such as 2.5D/3D packaging, chiplet integration, and fan-out packaging are gaining rapid adoption, enabling improved performance, power efficiency, and miniaturization beyond traditional scaling limits. The industry is currently facing capacity constraints due to surging demand for AI chips, prompting significant investments in advanced packaging facilities. For instance, Taiwan Semiconductor Manufacturing Company (TSMC) highlighted the increased demand for advanced packaging capacity to support AI workloads. In April 2026, TSMC announced to open a chip packaging plant in Arizona by 2029.

The advanced packaging industry is also witnessing rising consolidation and strategic collaborations aimed at strengthening supply chains and technological capabilities. Companies are expanding capacity through partnerships and regional investments, aligning with government initiatives to localize semiconductor manufacturing. For example, in October 2024, Amkor Technology Inc. and TSMC expanded their partnership to improve capabilities in the U.S., reflecting a shift toward supply chain resilience and regulatory alignment. Overall, the industry is defined by rapid technological advancements, increasing partnerships, and growing regulatory influence on geographic expansion strategies.

Packaging Type Insights

The flip-chip segment dominated the advanced packaging market, accounting for a 38.7% share in 2025, driven by its superior electrical performance, high interconnect density, and efficient thermal management capabilities. This packaging type is widely adopted across high-performance applications such as processors, GPUs, and AI chips due to its ability to support faster signal transmission and reduced power consumption. Flip-Chip technology enables direct connection of the die to the substrate, minimizing interconnect length and enhancing overall device performance. Its compatibility with advanced nodes and ability to handle high I/O density further strengthen its position in applications such as data centers, high-performance computing, and advanced consumer electronics.

The embedded-die segment is gaining momentum due to its ability to achieve high integration density, improved electrical performance, and better thermal management by embedding chips directly into the substrate. This reduces interconnect length, enabling faster signal transmission and lower power consumption, making it suitable for applications such as automotive electronics, wearables, IoT, and high-performance computing. The segment is driven by increasing demand for miniaturized, high-reliability devices, with companies such as ASE Technology Holding Co., Ltd. and Amkor Technology Inc. expanding their capabilities in advanced substrate integration. Overall, growth is supported by its performance advantages and rising adoption in next-generation electronics.

Application Insights

The consumer electronics segment dominated the advanced packaging industry in 2025, accounting for 51.4%, driven by the widespread adoption of smartphones, tablets, wearables, and other connected devices. The segment benefits from the increasing need for compact, high-performance, and energy-efficient semiconductor solutions, where advanced packaging enables higher integration density, improved thermal management, and enhanced electrical performance. Growing consumer demand for multifunctional devices, coupled with rapid product innovation cycles, has further accelerated the adoption of technologies. Additionally, the expansion of 5G-enabled devices and IoT applications continues to strengthen demand, as manufacturers seek to deliver thinner, faster, and more reliable electronic products.

The automotive segment is a significant application area of the market, driven by the growth of electric vehicles (EVs), ADAS, and connected car technologies. Advanced packaging solutions such as system-in-package (SiP) and 2.5D/3D integration enable higher performance, reliability, and thermal efficiency required for automotive environments. Increasing semiconductor content in vehicles, including sensors, power devices, and AI chips, is fueling demand for compact and high-density packaging. Companies like Infineon Technologies AG and NXP Semiconductors N.V. are actively utilizing these technologies to support electrification and autonomous driving trends, driving steady segment growth.

Regional Insights

Asia Pacific dominated the advanced packaging market in 2025, driven by the strong presence of semiconductor manufacturing hubs, rapid adoption of advanced technologies, and increasing investments in electronics production. The region benefits from a well-established supply chain, cost-effective manufacturing capabilities, and high demand from key end-use industries such as consumer electronics, automotive, and telecommunications. Countries such as China, Taiwan, South Korea, and Japan play a critical role in driving regional growth, supported by the expansion of data centers, 5G infrastructure, and AI applications, which continue to accelerate the adoption of advanced packaging solutions.

The Chinaadvanced packaging market is expected to grow significantly, driven by its strong semiconductor manufacturing base and expanding electronics production. The country benefits from a well-established supply chain, cost advantages, and rising demand across consumer electronics, telecommunications, and automotive sectors. Growth is further supported by the rapid expansion of 5G infrastructure, data centers, and AI applications. Additionally, government initiatives focused on semiconductor self-sufficiency are accelerating adoption and strengthening China’s role in the global market.

North America Advanced Packaging Market

North America accounted for 27.8% of the advanced packaging industry in 2025, supported by strong demand for high-performance computing, AI, and cloud-based applications. The region benefits from advanced technological capabilities, a robust semiconductor ecosystem, and significant investments in research and development. Growth is further driven by increasing adoption across key sectors such as data centers, automotive electronics, telecommunications, and defense, as well as a rising focus on next-generation packaging technologies to enhance performance and efficiency.

U.S. Advanced Packaging Market Trends

The U.S. plays a central role in regional market growth, driven by the presence of leading semiconductor companies, advanced manufacturing infrastructure, and continuous innovation in packaging technologies. The country is witnessing increasing investments in AI, high-performance computing, and domestic semiconductor production, supported by government initiatives to strengthen supply chain resilience. Additionally, the growing demand for advanced electronics across consumer, automotive, and industrial applications continues to support the market expansion.

Europe Advanced Packaging Market Trends

Europe accounted for 23.2% of the advanced packaging industry in 2025, supported by a strong focus on sustainability, advanced manufacturing, and regulatory compliance. The region is witnessing increasing adoption of energy-efficient, high-performance semiconductor solutions across the automotive, industrial, and telecommunications sectors, driven by ongoing digital transformation, the expansion of electric vehicles, and advancements in 5G and IoT. Additionally, the presence of established automotive and industrial players, along with growing investments in semiconductor innovation, is further supporting market growth. At the same time, the emphasis on reducing carbon footprint and improving energy efficiency continues to encourage the adoption of the latest technologies.

Key Advanced Packaging Company Insights

The competitive environment of the advanced packaging market is moderately consolidated, characterized by the presence of leading semiconductor companies, outsourced semiconductor assembly and test (OSAT) providers, and technology-focused solution providers. Key players compete based on technological innovation, integration capabilities, performance efficiency, and advanced manufacturing processes. The market is witnessing increasing consolidation through strategic partnerships, capacity expansions, and investments in next-generation packaging technologies such as 2.5D/3D integration and chiplet architectures, which continue to shape the competitive dynamics.

-

In April 2026, Innolux Corporation announced the expansion into the advanced semiconductor packaging sector, to utilize the display technology as its core platform to accelerate integration with semiconductor and IoT technologies.

-

In March 2026, Intel Corporation announced to expand its advanced packaging capabilities, including Foveros and EMIB technologies, to support high-performance AI and data center chips.

-

In February 2026, Amkor Technology, Inc. announced the expansion of its advanced packaging capacity to meet growing demand in automotive and 5G sectors, strengthening their portfolio in flip-chip and wafer-level packaging to support high-performance computing (HPC) and autonomous vehicles.

Key Advanced Packaging Companies:

The following key companies have been profiled for this study on the advanced packaging market.

- Amkor Technology Inc.

- Advanced Semiconductor Engineering (ASE)

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Intel

- Samsung Electronics

- JCET Group

- ASMPT SMT Solutions

- IPC International, Inc.

- SEMICON

- Yole Group

- Prodrive Technologies B.V.

Advanced Packaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 41.7 billion

Estimated Market size in 2026

USD 43.9 billion

Projected Market size by 2033

USD 66.0 billion

Growth rate

CAGR of 6.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Packaging type, application, region

Regional Scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Key companies profiled

Amkor Technology Inc.; Advanced Semiconductor Engineering (ASE); Taiwan Semiconductor Manufacturing Company (TSMC); Intel; Samsung Electronics; JCET Group; ASMPT SMT Solutions; IPC International, Inc.; SEMICON; Yole Group; Prodrive Technologies B.V.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail of customized purchase options to meet your exact research needs. Explore purchase options

Global Advanced Packaging Market Report Segmentation

This report forecasts revenue growth at the global, regional & country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the advanced packaging market report based on packaging type, application, and region:

-

Packaging Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Flip-Chip

-

Fan-Out WLP

-

Embedded-Die

-

Fan-In WLP

-

2.5D/3D

-

Other packaging types

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Consumer Electronics

-

Automotive

-

Industrial

-

Healthcare

-

Aerospace & Defense

-

Other applications

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global advanced packaging market size was valued at USD 41.7 billion in 2025 and is estimated at USD 43.9 billion for 2026.

The global advanced packaging market is expected to grow at a CAGR of 6.0% from 2026 to 2033, reaching USD 66.0 billion by 2033.

The consumer electronics segment led the advanced packaging market in 2025 with a 51.4% share, driven by rising demand for compact, high-performance devices like smartphones and wearables, supported by 5G adoption and AI integration.

The advanced packaging market is driven by rising demand for AI and high-performance computing, increasing semiconductor content in automotive and consumer electronics, and the need for miniaturization, higher performance, and energy efficiency.

Asia Pacific dominated with a 43.5% revenue share in 2025.

The flip-chip segment led with a 38.7% revenue share in 2025.

Key players include Amkor Technology Inc.; Advanced Semiconductor Engineering (ASE); Taiwan Semiconductor Manufacturing Company (TSMC); Intel; Samsung Electronics; JCET Group; ASMPT SMT Solutions; IPC International, Inc.; SEMICON; Yole Group; Prodrive Technologies B.V.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.