- Home

- »

- Clinical Diagnostics

- »

-

Anatomic Pathology Market Size & Share Report, 2026-2033GVR Report cover

![Anatomic Pathology Market (2026 - 2033)Report]()

Anatomic Pathology Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product & Services (Instruments, Reagents, Services), By Technology (Histopathology, Immunohistochemistry (IHC)), By Application (Disease Diagnosis), By End Use, By Region, And Segment Forecasts

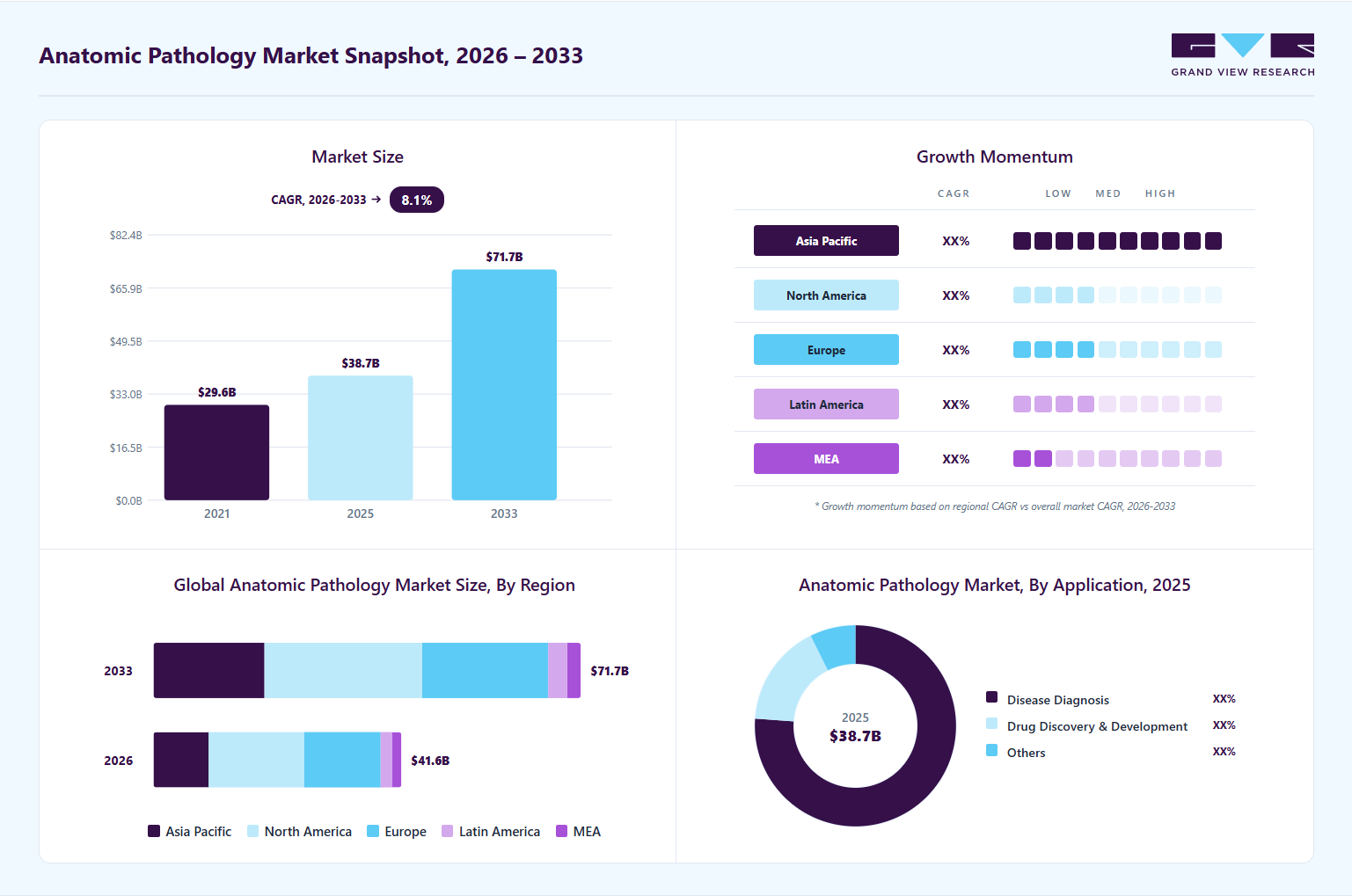

Market Size, 2025

$38.7BMarket Estimate, 2026

$41.6BMarket Forecast, 2033

$71.7BCAGR, 2026–2033

8.1%Anatomic Pathology Market Summary

The global anatomic pathology market size was valued at USD 38.7 billion in 2025, is projected to grow from USD 41.6 billion in 2026 to reach USD 71.7 billion by 2033, growing at a CAGR of 8.1% from 2026 to 2033. North America dominated the global anatomical pathology market with the largest revenue share of 38.8% in 2025. The rising global burden of cancer remains one of the most significant growth drivers of the anatomic pathology industry, primarily due to the growing reliance on tissue-based diagnostics for cancer detection, classification, staging, and therapeutic decision-making.

Key Market Trends & Insights

- By products & services: Reagents & consumables segment led the market with the largest revenue share of 48.9% in 2025.

- By application: Disease diagnosis segment led the market with the largest revenue share of 76.1% in 2025.

- By technology: Histopathology segment accounted for the largest market revenue share in 2025.

- By end use: Hospitals segment led the market with the largest revenue share of 37.3% in 2025.

Regional Highlights

- Largest regional market: North America (38.8% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 38.7 Billion

- Estimated market size in 2026: USD 41.6 Billion

- Projected market size by 2033: USD 71.7 Billion

- CAGR (2026-2033): 8.1%

")

Market Dynamics

The accelerating adoption of digital pathology and AI-enabled diagnostic workflows is emerging as a major growth driver for the anatomic pathology industry. Pathology laboratories are increasingly transitioning from conventional microscope-based workflows to digitized pathology ecosystems that include whole slide imaging (WSI), cloud-enabled image management, AI-assisted image analysis, and integrated laboratory informatics platforms. This transformation is being driven by the growing need for operational efficiency, remote diagnostic collaboration, workflow standardization, and improved pathology turnaround times amid rising global diagnostic workloads.

The increasing implementation of digital pathology infrastructure is enabling pathology laboratories to enhance image accessibility, improve diagnostic collaboration across geographically dispersed healthcare networks, and support centralized pathology operations. In addition, digital pathology platforms are creating the foundational infrastructure required for the deployment of AI-assisted pathology tools capable of supporting slide triaging, tissue classification, biomarker quantification, and workflow optimization across high-volume pathology laboratories. For instance, in March 2026, Philips expanded its digital pathology portfolio by introducing enhanced AI-enabled pathology workflow capabilities designed to improve pathology image analysis, case management efficiency, and remote pathology collaboration across enterprise laboratory networks. The development reflects the industry's increasing focus on integrating AI-assisted diagnostic support tools into routine pathology workflows to address growing testing complexity and rising pathology case volumes.

Stringent regulatory and validation requirements associated with advanced pathology technologies continue to remain a significant restraint affecting the adoption and commercialization of modern anatomic pathology solutions globally. The increasing integration of digital pathology, molecular pathology, artificial intelligence (AI)-enabled diagnostic tools, companion diagnostics, and biomarker-based testing into pathology workflows has substantially increased the complexity of regulatory compliance and clinical validation processes across pathology laboratories and diagnostic manufacturers. Pathology technologies intended for clinical diagnostic use must undergo extensive analytical validation, performance verification, reproducibility assessment, and workflow standardization prior to routine clinical implementation.

The increasing utilization of targeted therapies and immunotherapy is significantly driving demand for tissue biomarker analysis, immunohistochemistry (IHC), molecular pathology testing, and integrated diagnostic workflows. Pathology laboratories are increasingly required to support personalized treatment selection through advanced biomarker characterization and molecular profiling, thereby creating long-term opportunities for pathology reagents, antibodies, molecular probes, tissue staining systems, and companion diagnostic platforms. In addition, large healthcare systems and centralized diagnostic laboratories are increasingly investing in digital pathology infrastructure to improve operational efficiency, enable remote diagnostics, facilitate image sharing, standardize workflows, and scale pathology. The growing implementation of AI-assisted image analysis platforms for biomarker quantification, slide triaging, and computational pathology is further expanding commercialization opportunities for pathology software providers, AI developers, and digital pathology platform manufacturers.

Market Characteristics & Concentration

The anatomic pathology industry is currently experiencing significant innovation, driven primarily by advances in digital pathology, artificial intelligence (AI), and molecular diagnostics. Companies increasingly incorporate AI-powered image analysis, automated workflows, and cloud-based platforms to boost diagnostic accuracy and efficiency. For instance, in September 2025, Leica Biosystems debuted cutting-edge digital pathology software at ECP 2025, expanding its extensive suite of solutions. Furthermore, Aperio HALO AP, the new clinical image management software, includes a full suite of enterprise-grade digital pathology diagnostic workflows for on-screen diagnosis, multidisciplinary team meetings, consultations, and more. Moreover, the combination of molecular and anatomic pathology enables more personalized, targeted treatment approaches. These innovations are reshaping traditional pathology practices and are expected to accelerate further as R&D investments and collaborations between diagnostics and biopharma companies grow.

Mergers and acquisitions (M&A) in the anatomic pathology industry are moderate, with key players aiming to expand their technological capabilities, geographical footprint, and market share. Moreover, while not as common or large-scale as in other healthcare sectors, recent M&A have focused on bringing together AI startups, digital imaging firms, and specialized pathology labs to broaden service offerings. These activities help companies stay competitive and meet growing demand, but the market is still somewhat fragmented, particularly in emerging markets, limiting the full impact of M&A for the time being.

The regulatory environment for anatomic pathology has a moderate influence on the market. Regulatory bodies such as the FDA, EMA, and other regional agencies play an important role in approving and overseeing diagnostic devices, AI algorithms, and laboratory practices. While widespread support for innovation exists, particularly in digital and companion diagnostics, regulatory pathways can be complicated and time-consuming, particularly for AI-powered tools. Efforts are underway globally to modernize diagnostic regulations and provide clearer guidelines for digital pathology, which may further increase this impact in the future.

The market is expanding moderately across regions, with Asia-Pacific, Latin America, the Middle East, and Africa leading. Furthermore, while North America and Europe remain dominant markets due to advanced infrastructure and widespread adoption of digital tools, companies are increasingly looking to emerging markets to capitalize on rising healthcare investments, expanding diagnostic capacity, and unmet medical needs. However, barriers such as limited infrastructure, reimbursement issues, and labor shortages in some areas slow adoption and expansion.

Product & Services Insights

The reagents & consumables segment led the market with the largest revenue share of 48.9% in 2025, because of its critical and recurring role in diagnostic workflows. Consumables such as reagents, stains, antibodies, fixation solutions, embedding materials, and slides are required for all pathology procedures, making them indispensable in routine and advanced diagnostic tests. Unlike capital equipment, which requires a one-time investment, consumables are used daily, resulting in consistent and high demand in hospitals, diagnostic labs, and research facilities. The growing number of biopsy and histopathology procedures, driven by the rising incidence of cancer and chronic diseases, drives demand for these products. Furthermore, the growing use of automated staining systems and immunohistochemistry (IHC) techniques has boosted demand for specialized reagents and antibodies, reinforcing the consumables segment's market leadership. Furthermore, the growing use of automated staining systems and immunohistochemistry (IHC) techniques has increased demand for specialized reagents and antibodies, bolstering the consumables segment's market dominance.

The instruments segment is anticipated to grow at the fastest CAGR of 8.44% over the forecast period, owing to rising demand for automation, digitalization, and high-throughput diagnostic capabilities. For instance, in September 2025, StatLab Leads Pathology innovation with the U.S. launch of Diapath equipment. Moreover, this milestone fulfills the strategic vision behind StatLab’s 2024 acquisition of Diapath, bringing differentiated histology instrumentation to U.S. laboratories and delivering a comprehensive end-to-end pathology workflow solution.

Technology Insights

The histopathology segment accounted for the largest market revenue share in 2025, driven by the rising global incidence of cancer and other chronic diseases that require detailed tissue-based diagnosis. The increasing demand for early and accurate disease detection has led to greater adoption of advanced histopathology techniques across hospitals, diagnostic laboratories, and academic institutions. The integration of digital pathology, automation, and molecular-based tools is further enhancing workflow efficiency and diagnostic precision. In addition, growing adoption of AI-assisted image analysis and the expansion of personalized medicine are supporting segment growth. Continuous need for routine tissue examination for disease confirmation ensures stable and sustained demand, reinforcing the dominance of histopathology within the anatomic pathology landscape.

The digital pathology segment is expected to grow at the fastest CAGR over the forecast period, driven by the rapid shift from conventional microscopy to digitally enabled diagnostic workflows. Increasing adoption across hospitals, reference laboratories, and pharmaceutical research organizations is being supported by the growing need for remote diagnostics, workflow automation, and improved collaboration among pathologists. Rising investments in drug discovery, precision oncology, and biomarker research are further accelerating demand, as digital pathology enables efficient tissue analysis, data sharing, and advanced image-based quantification for clinical and research applications. In addition, the integration of artificial intelligence and machine learning is significantly enhancing diagnostic accuracy, reducing turnaround time, and improving reproducibility.

Application Insights

The disease diagnosis segment led the market with the largest revenue share of 76.1% in 2025, owing to the growing global burden of chronic diseases, cancer prevalence, and increased demand for early and precise diagnostic testing. Hospitals and diagnostic centers are increasingly implementing advanced pathology technologies, such as digital pathology and molecular diagnostics, to improve disease detection accuracy and speed. Furthermore, the growing emphasis on personalized medicine and the integration of AI-driven diagnostic tools are strengthening this segment's dominance. The ongoing demand for routine tissue and organ analysis for disease confirmation ensures that this category generates consistent revenue.

The drug discovery and development segment is expected to grow at the fastest CAGR over the forecast period, owing to the increasing use of pathology techniques in pharmaceutical and biotechnology research. The increase in R&D investments in novel therapeutics and precision oncology has increased the demand for tissue-based studies and biomarker analysis. Anatomic pathology is critical for identifying disease mechanisms, validating drug targets, and assessing treatment efficacy at both the preclinical and clinical stages. Furthermore, advancements in digital imaging, automation, and AI-assisted analysis are increasing efficiency and hastening the growth of this segment within the broader market. For instance, in April 2024, PathAI partnered with Google Cloud to transform drug discovery and precision medicine through AI-powered pathology, helping biopharma companies and anatomic pathology (AP) labs accelerate the adoption of AI and digital pathology.

End Use Insights

The hospitals segment led the market with the largest revenue share of 37.3% in 2025, driven by high patient footfall, comprehensive diagnostic infrastructure, and the integration of multidisciplinary services. They serve as primary centers for disease diagnosis, surgical pathology, and cancer screening, driving consistent demand for pathological examinations. The availability of advanced laboratory facilities, skilled pathologists, and access to cutting-edge technologies such as immunohistochemistry and molecular pathology further enhances their diagnostic capabilities. In addition, hospitals are investing in digital pathology to expand it. For instance, in September 2025, HSE announced plans to establish a USD 52.27 million digital pathology solution across 22 hospitals nationwide. Moreover, the technology was introduced in 22 histopathology laboratories, including eight HSE centers of excellence and 14 general hospital laboratory centers.

The diagnostic laboratories segment is projected to grow at the fastest CAGR over the forecast period, driven by the growing trend of outsourcing pathology tests to specialized labs and the rapid adoption of automation and digital pathology systems. These laboratories offer high-throughput testing capabilities, faster turnaround times, and cost-effective services, attracting both patients and healthcare providers. The rise in independent pathology labs, coupled with advancements in AI-driven image analysis and remote diagnostics, has expanded their reach and efficiency. Furthermore, the growing healthcare demand in emerging economies and the shift toward decentralized diagnostic models are fueling the rapid growth of this segment.

Regional Insights

North America dominated the global anatomic pathology market with the largest revenue share of 38.8% in 2025, owing to several key factors. The area benefits from a well-established healthcare infrastructure, with widespread access to advanced diagnostic laboratories and state-of-the-art pathology equipment. High healthcare expenditure and strong government support for cancer screening and chronic disease management programs drive consistent demand for pathological services. In addition, North America is a hub for technological innovation, rapidly adopting digital pathology, AI-powered diagnostic tools, and molecular pathology techniques. The presence of significant market players, robust R&D activities, and favorable reimbursement policies further fuel market growth. Moreover, increasing awareness among patients and healthcare professionals about the importance of early diagnosis and personalized medicine continues to boost the region's demand for anatomic pathology solutions.

U.S. Anatomic Pathology Market Trends

The anatomic pathology industry in the U.S. is driven by rising cancer prevalence, greater healthcare spending, and a strong emphasis on early and precise diagnosis. The presence of advanced healthcare infrastructure, significant R&D investments, and a high clinical awareness all contribute to rapid market expansion. For instance, in August 2025, Agilent Technologies Inc. launched its Dako Omnis family of instruments with three new models: Agilent Dako Omnis 110, 165, and 165 Duo, designed to meet the evolving needs of pathology laboratories of all sizes. These new instruments enable labs the ability to tailor their staining solutions based on volume, workflow, and diagnostic needs. Favorable payment schemes and the rapid adoption of new technology, such as molecular diagnostics and biologic drugs, drive demand even higher. Furthermore, FDA regulations help enable faster product approvals and market entry.

Europe Anatomic Pathology Market Trends

The anatomic pathology market in Europe's growth is driven by the rising cancer rates, more investments in healthcare infrastructure, and the expanding use of AI and digital pathology technologies. Across Europe, countries are prioritizing precision medicine and early disease detection with the help of strong government initiatives and favorable reimbursement policies. The area is also well known for the extensive collaborations that pathology labs and pharmaceutical companies have established to speed up the development of biomarkers and diagnostics. However, regulatory complexity and differences across national healthcare systems impede consistent market growth. Despite these challenges, advances in molecular pathology and heightened patient and clinician awareness are driving an increase in the demand for advanced diagnostic services.

The UK anatomic pathology market is evolving, with a focus on combining AI and digital pathology to enhance patient outcomes and diagnostic workflows. Innovative pathology solutions are being actively promoted by the National Health Service (NHS) to enhance cancer diagnosis and control the rising burden of chronic illnesses. Personalized medicine initiatives and increased government funding are propelling the use of companion and molecular diagnostics. For instance, in September 2023, the Data to Early Diagnosis and Precision Medicine initiative is a USD 281.00 million investment that aims to advance precision medicine, allowing for earlier diagnosis and more effective treatment of major diseases. The program had already committed all funding and assisted UK businesses and academia in harnessing research and health data to drive innovation, improve health outcomes, and stimulate economic growth. UK Research and Innovation (UKRI) led the initiative, with Innovate UK as the primary delivery partner. A highly qualified workforce and a reputable research ecosystem that supports clinical trials and translational studies are additional advantages for the UK market. Rapid expansion, however, might be hampered by financial constraints and the need for infrastructure improvements in some areas.

The anatomic pathology market in Germany held a significant share of the European market in 2025 due to its high healthcare expenditures and sophisticated medical infrastructure. Automated pathology tools and AI-powered digital platforms are increasingly used to meet the nation's expanding diagnostic needs, especially in oncology. Robust regulatory frameworks and reimbursement support for innovative diagnostics encourage molecular pathology innovation and adoption. Another significant contribution comes from Germany's thriving biopharmaceutical sector, which collaborates with diagnostic labs on clinical validation studies and biomarker research. Also driving market expansion are the aging population and the growing incidence of diseases linked to sedentary lifestyles.

Asia Pacific Anatomic Pathology Market Trends

The anatomic pathology market in the Asia Pacific is anticipated to grow at the fastest CAGR during the forecast period, driven by the growing incidence of cancer, the expansion of healthcare infrastructure, and the growing use of advanced diagnostic technologies. Significant investments are being made by nations like China, Japan, India, and South Korea to update pathology labs and incorporate AI and digital pathology. The scope of diagnostic services is being extended beyond urban areas through government initiatives to increase healthcare affordability and accessibility. But issues such as a shortage of qualified pathologists and inconsistent reimbursement practices persist. Notwithstanding these obstacles, the need for supplies, equipment, and molecular diagnostic testing is being driven by rising interest in early detection and personalized medicine.

The Japan anatomic pathology market is distinguished by its well-developed healthcare system, which places a premium on R&D. Thanks to government incentives and innovative regulatory frameworks, the country is aggressively deploying AI and digital pathology to improve diagnostic efficiency and accuracy. For instance, in August 2024, BostonGene, a leading provider of AI-driven molecular and immune profiling solutions, showcased its AI-powered multiomics platform at the 22nd Annual Meeting of the Japanese Society of Digital Pathology at Meio University in Nago, Japan. Two of the company's abstracts were accepted for presentation at the event, highlighting BostonGene's ongoing efforts to advance precision diagnostics through the integration of AI and multiomics technologies. Japan's high cancer incidence and rapidly aging population drive the country's ongoing demand for pathology services. Moreover, clinical practice is increasingly reliant on the integration of companion and molecular diagnostics, particularly for targeted therapies. Partnerships between pharmaceutical companies and diagnostic labs not only advance precision medicine but also strengthen Japan's position as a significant regional market.

The anatomic pathology market in China is rapidly expanding, fostering by rising cancer rates, government initiatives to modernize diagnostic infrastructure, and increased healthcare spending. Also, China is seeing an increase in the use of digital pathology, artificial intelligence-based diagnostic tools, and molecular pathology to aid personalized medicine. Efforts to improve rural healthcare access and insurance coverage are driving demand away from major cities. Moreover, local manufacturing of pathology instruments and consumables is also becoming more popular, lowering costs and increasing accessibility. Also, challenges such as a lack of skilled pathologists and regulatory complexities may stymie expansion. Overall, China remains a high-potential market with exciting growth prospects.

Latin America Anatomic Pathology Market Trends

The anatomic pathology market in Latin America is gradually expanding, driven by rising cancer and chronic disease prevalence and increased healthcare investment in countries such as Brazil, Mexico, and Argentina. Adoption of digital pathology and automation is growing, albeit at a slower pace than in developed regions due to infrastructure and economic constraints. Government initiatives to improve diagnostic services and broaden insurance coverage are creating new opportunities. Collaborations between local labs and international companies also help to facilitate technology transfer and skill development. Despite challenges such as limited reimbursement and labor shortages, rising disease awareness and healthcare modernization efforts are expected to drive consistent market growth.

Middle East and Africa Anatomic Pathology Market Trends

The anatomic pathology market in the Middle East and Africa is driven by rising cancer incidence, increased government focus on non-communicable diseases, and growing investments in healthcare infrastructure. Furthermore, countries such as Saudi Arabia, the UAE, Egypt, and South Africa are investing in modern diagnostic facilities and adopting digital pathology platforms to improve service delivery. However, the region faces challenges such as limited trained pathology personnel, varying regulatory environments, and budget constraints in some areas. Apart from these challenges, collaborations and initiatives aimed at capacity building are enhancing market prospects. Growing awareness of early diagnosis, as well as the adoption of personalized medicine approaches, are further supporting the market’s upward trajectory.

Key Anatomic Pathology Company Insights

The anatomic pathology industry is highly competitive, with market players engaging in strategic collaborations, new product launches, acquisitions, technological advancements, and regional expansion. These companies collectively hold the largest market share and dictate industry trends.

Key Anatomic Pathology Companies

The following key companies have been profiled for this study on the anatomic pathology market.

-

Danaher

-

PHC Holdings Corporation

-

Quest Diagnostics Incorporated

-

Laboratory Corporation of America Holdings

-

F. Hoffmann-La Roche AG

-

Agilent Technologies, Inc.

-

Sakura Finetek USA, Inc.

-

NeoGenomics Laboratories, Inc.

-

BioGenex

-

Bio SB

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Danaher Corporation; Agilent Technologies, Inc; Labcorp; F. Hoffmann-La Roche Ltd.; Sakura Finetek USA, Inc.; PHC Holdings Corporation; Quest Diagnostics Incorporated; Thermo Fisher Scientific Inc.

- Mature players focus on integrated pathology ecosystems combining instruments, consumables, digital pathology, and companion diagnostics.

- Their strategy emphasizes global distribution, recurring reagent revenue, workflow automation, acquisitions, regulatory approvals, and partnerships with hospitals, laboratories, and pharmaceutical companies to strengthen market penetration and customer retention.

- Mature companies benefit from strong brand recognition, extensive installed bases, broad pathology portfolios, global service infrastructure, and high regulatory credibility.

- Their ability to provide end-to-end pathology solutions-including tissue processing, staining, imaging, digital pathology, and diagnostics-creates high switching costs and long-term customer relationships.

- Matured players often face slower innovation cycles, high operational complexity, and dependence on legacy systems. Premium pricing can limit adoption in cost-sensitive laboratories.

- Additionally, large organizational structures may reduce agility in responding quickly to emerging technologies such as AI-driven pathology and decentralized diagnostics.

Emerging Players: NeoGenomics Laboratories; BioGenex

- Emerging players typically focus on niche specialization such as digital pathology, AI-assisted diagnostics, molecular pathology, or oncology-focused tissue testing.

- They rely on strategic collaborations, targeted product innovation, flexible commercialization models, and partnerships with established healthcare providers to gain market visibility and competitive positioning.

- Emerging companies often possess stronger innovation capabilities, faster product development cycles, and greater flexibility in adopting advanced technologies such as AI, multiplex pathology, and precision diagnostics. Their focused expertise enables differentiation in high-growth segments where large incumbents may be slower to respond.

- Emerging players generally face limitations in global distribution, installed base, financial resources, and regulatory capabilities. Narrow product portfolios and lower brand recognition can restrict market penetration. They may also depend heavily on partnerships, external funding, or niche applications for sustained commercial growth.

Recent Developments

-

In March 2026, Leica Biosystems and Bio-Techne launched automated RNAscope in situ hybridization (ISH) on the BOND-PRIME staining platform to improve molecular pathology workflows and tissue biomarker analysis.

-

In September 2025, Labcorp collaborated with Roche to advance digital pathology capabilities. The investment enables pathologists to diagnose patients using digital images and supports future integration of artificial intelligence (AI). Moreover, Labcorp is committed to advancing its diagnostic capabilities through the adoption of innovative technologies.

-

In May 2024, Quest Diagnostics and PathAI collaborated to accelerate the adoption of digital and AI pathology innovations to improve quality, speed, and efficiency in diagnosing cancer and other diseases. Quest licensed PathAI's AISight digital pathology image management system to support its pathology laboratories and customer sites in the US. The two companies may also explore ways for Quest to help PathAI develop its algorithmic products, leveraging Quest's extensive pathology expertise.

Anatomic Pathology Market Report Scope

Report Attribute

Details

Market size in 2025

USD 38.7 billion

Estimated Market size in 2026

USD 41.6 billion

Projected Market size by 2033

USD 71.7 billion

Growth rate

CAGR of 8.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product & service, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Danaher; PHC Holdings Corporation; Quest Diagnostics Incorporated; Laboratory Corporation of America Holdings; F. Hoffmann-La Roche AG; Agilent Technologies, Inc.; Sakura Finetek USA, Inc.; NeoGenomics Laboratories, Inc.; BioGenex; Bio SB

Customization scope

Free report customization (equivalent to up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Anatomic Pathology Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global anatomic pathology market report based on product & service, application, end use, and region:

-

Product & Service Outlook (Revenue, USD Billion, 2021 - 2033)

-

Instruments

-

Microtomes & Cryostat

-

Tissue Processors

-

Automatic Stainers

-

Whole Slide Imaging (WSI) Scanners

-

Other Products

-

-

Consumables

-

Reagents & Antibodies

-

Probes & Kits

-

Others

-

-

Services

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Histopathology

-

Cytopathology

-

Immunohistochemistry (IHC)

-

In Situ Hybridization (ISH)

-

Digital Pathology

-

Molecular Pathology

-

AI-enabled Pathology

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Disease Diagnosis

-

Drug Discovery and Development

-

Others

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hospitals

-

Diagnostic Laboratories

-

Research Laboratories

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cancer & Disease Diagnosis Trend Analysis

Assessment of cancer incidence, biopsy volumes, chronic disease burden, and pathology testing demand across hospitals and diagnostic centers.

Helps identify high-growth disease segments and future diagnostic demand trends.

Laboratory Workflow & Digital Pathology Assessment

Evaluation of tissue processing, slide preparation, digital pathology adoption, workflow automation, and reporting efficiency across laboratories.

Supports operational optimization and transition toward digital pathology solutions.

Hospital, Reference Lab & Academic Adoption Trends

Analysis of anatomic pathology utilization across hospitals, reference laboratories, academic institutes, and cancer centers.

Identifies major end-user demand centers and expansion opportunities.

Advanced Technology & Innovation Landscape

Assessment of AI-assisted pathology, whole slide imaging, molecular pathology integration, companion diagnostics, and next-generation imaging platforms.

Highlights emerging technologies and future innovation opportunities in precision diagnostics.

Frequently Asked Questions About This Report

Histopathology held the largest revenue share in 2025.

The reagents & consumables segment led with a 48.9% revenue share in 2025, while the instrument is the fastest-growing segment.

Disease diagnosis held the largest share (over 76.1%) in 2025 and drug discovery is the fastest-growing market.

North America dominated with a 38.8% revenue share in 2025.

Some of the key players in this industry are Danaher, PHC Holdings Corporation, Quest Diagnostics Incorporated, Laboratory Corporation of America Holdings, F. Hoffmann-La Roche AG, Agilent Technologies, Inc., Sakura Finetek USA, Inc., NeoGenomics Laboratories, Inc., BioGenex, and Bio SB.

The global anatomic pathology market size was estimated at USD 38.7 billion in 2025 and is expected to reach USD 41.6 billion in 2026.

The global anatomic pathology market is expected to grow at a compound annual growth rate of 8.1% from 2026 to 2033 to reach USD 71.7 billion by 2033.

Some of the major factors driving the market are rising global burden of cancer continues to remain one of the most significant growth drivers for the anatomic pathology market, primarily due to the increasing dependence on tissue-based diagnostics for cancer detection, classification, staging, and therapeutic decision-making.

About the Author(s)

Clinical Diagnostics Research Team

Healthcare · Clinical DiagnosticsThis report was authored by the clinical diagnostics research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clinical diagnostics segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.