- Home

- »

- Medical Devices

- »

-

Artificial Disc Replacement Market Size Report, 2026-2033GVR Report cover

![Artificial Disc Replacement Market (2026 - 2033)Report]()

Artificial Disc Replacement Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material Type (Metal On Polymer, Metal On Metal, Polymer-Based / Elastomeric), By Indication (Cervical, Lumbar), By End Use (Hospitals, Outpatient Facilities), By Region, And Segment Forecasts

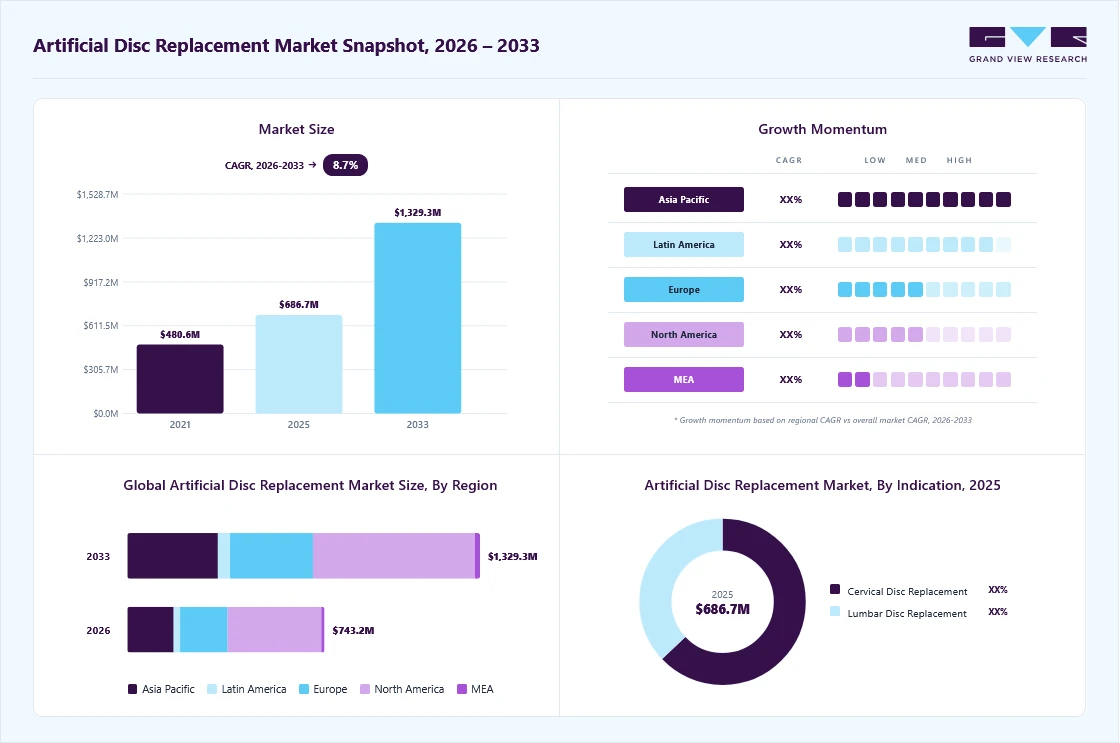

Market Size, 2025

$686.8MMarket Estimate, 2026

$743.2MMarket Forecast, 2033

$1,329.4MCAGR, 2026–2033

8.7%Artificial Disc Replacement Market Summary

The global artificial disc replacement market size was valued at USD 686.8 million in 2025 and is projected to grow from USD 743.2 million in 2026 to USD 1,329.4 million by 2033, at a CAGR of 8.7% from 2026 to 2033. The North America held the largest share of 47.8% of the global market in 2025. The growth is driven by the rising incidence of degenerative spinal disorders, influenced by sedentary lifestyles, obesity, and increasing cases of work-related spinal strain.

Key Market Trends & Insights

- By material type: Metal-on-polymer segment held the largest market share of 53.7% in 2025.

- By indication: Cervical disc replacement segment held the largest market share in 2025.

- By end use: Hospitals segment held the largest market share of 66.9% in 2025.

Regional Highlights

- Largest regional market: North America (47.8% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest share in 2025

Market Size & Forecast

- Market size in 2025: USD 686.8 Million

- Estimated market size in 2026: USD 743.2 Million

- Projected market size by 2033: USD 1,329.4 Million

- CAGR (2026-2033): 8.7%

Technological advancements in motion-preserving implants, including enhanced biomaterials and minimally invasive surgical approaches, are improving clinical outcomes and accelerating adoption. In addition, there is a growing shift toward motion-preservation procedures over spinal fusion, as both patients and surgeons increasingly prefer treatments that maintain spinal mobility and reduce the risk of adjacent segment degeneration, further supporting the growth of the artificial disc replacement industry.")

The section below outlines the key factors driving the growth of the artificial disc replacement (ADR) market, highlighting the rising burden of degenerative disc disease and spinal disorders, as well as the growing body of long-term clinical evidence. It also highlights technological advancements in artificial disc replacement.

Rising Burden of Degenerative Disc Disease and Spinal Disorders

The global burden of degenerative disc disease (DDD) and related spinal disorders continues to rise, supporting the adoption of artificial disc replacement (ADR). These conditions are increasingly observed beyond elderly populations, extending into middle-aged and younger individuals due to sedentary lifestyles, obesity, and occupational strain, particularly in desk-based and physically repetitive roles. An article published by the Eunice Kennedy Shriver National Institute of Child Health and Human Development (NICHD) in January 2025 reported that about 18,000 new cases of SCIs are reported annually, and about 255,000 to 390,000 people are currently living with an SCI in the U.S.

Growing surgeon & patient preference for minimally invasive disc arthroplasty over spinal fusion

The increasing preference among surgeons and patients for minimally invasive, motion-preserving procedures is a key factor supporting the adoption of artificial disc replacement (ADR) over traditional spinal fusion. This shift aligns with evolving healthcare priorities focused on shorter hospital stays, faster recovery, improved patient throughput, and cost efficiency. An article published by Barker Brooks Communications Ltd in August 2025, a large-scale outpatient study involving 1,043 patients and 1,684 artificial disc implants demonstrated that ADR procedures can be performed safely with same-day discharge, minimal perioperative complications, and no hospital readmissions. These findings indicate increasing surgeon confidence in ADR and its suitability for outpatient settings, whereas spinal fusion continues to require closer postoperative monitoring in many cases.

Increasing long-term clinical evidence boosts adoption of artificial disc replacement

The growing long-term clinical evidence supports the effectiveness of ADR in delivering sustained pain relief, functional improvement, and favorable safety outcomes, strengthening its role as a motion-preserving alternative to spinal fusion in appropriately selected patients. A study published by the National Center for Biotechnology Information in October 2025 reported a retrospective cohort of 130 patients undergoing lumbar total disc replacement, demonstrating significant long-term benefits with a mean follow-up of 13.88 years. Back pain scores (VAS) improved from 8.6 to 1.6, and leg pain from 7.3 to 1.1 (p < 0.001), indicating sustained pain reduction. Functional disability, measured by the Oswestry Disability Index (ODI), improved from 46.12 to 27, reflecting meaningful gains in daily function. In terms of socioeconomic outcomes, 73.84% of patients returned to their original occupation, while only 3.07% required pension support, highlighting long-term productivity benefits.

Market Opportunity Analysis

The artificial disc replacement industry is a high-value, underpenetrated segment of the spine surgery market. Despite strong clinical validation and clear biomechanical advantages over fusion in select patients, its adoption remains limited. This creates a multi-dimensional growth opportunity driven by patient conversion, geographic expansion, and indication broadening.

Untapped Patient Pool

ADR is particularly well-suited for younger, active patients with early-stage degenerative disc disease (DDD), where preservation of spinal motion is clinically beneficial. However, a significant proportion of such patients continue to undergo fusion procedures.

In practice, this gap exists because clinical decision-making is still heavily influenced by surgeons' familiarity and long-term confidence in fusion rather than by strict patient eligibility criteria. As a result, ADR is often underutilized even when it may offer superior functional outcomes.

Table 1 Patient Opportunity Mapping

Patient Segment

Why ADR is Suitable

Current Reality

Younger patients (<50 years)

Long-term need for mobility and durability

Often directed to fusion due to surgeon preference

Early-stage DDD

Preserved anatomy allows optimal ADR outcomes

Late intervention or conservative bias delays ADR use

Working population

Faster recovery and return to activity

Limited awareness of ADR benefits

Geographic Expansion

ADR adoption varies significantly across regions due to differences in reimbursement systems, healthcare infrastructure, and clinical adoption maturity.

Table 2 Regional Dynamics

Region

Market Situation

Key Constraint

Opportunity Nature

Asia-Pacific

Large patient base, low penetration

Cost sensitivity, limited reimbursement

Volume expansion

Europe

Established adoption, supportive policies

Moderate growth ceiling

Stable expansion

U.S.

Advanced but inconsistent adoption

Payer variability, administrative barriers

High-value, policy-driven growth

Industry Shift in Spine Implants (2021-2026)

The spine implants market has undergone structural realignment, driven by pricing pressure in fusion devices (30-50% discounts in tenders), rising regulatory burden, and a shift toward innovation-led growth. This has positioned ADR as a higher-value, differentiated segment.

Key developments:

-

Portfolio expansion: NuVasive acquired Simplify Medical (2021) to strengthen ADR capabilities.

-

Divestitures: Zimmer Biomet spun off its spine division (ZimVie → Highridge), and Stryker exited traditional spine implants by 2025.

-

Strategic pivot: Medtronic continues ADR presence (e.g., Prestige LP) but shifted investment toward robotics and navigation.

- Product rationalization: Multiple ADR systems (ALTIA TDR C, DISCOCERV, DISCOVER, NUNEC, PHYSIODISC, M6-C) were discontinued due to limited traction or strategic deprioritization.

Market impact:

-

Reduced competition in commoditized fusion creates whitespace for ADR growth

-

Increasing focus on motion preservation and clinical outcomes

-

Rising role of specialized and PE-backed players driving ADR innovation

Market Characteristics & Concentration

The chart below represents the relationship between industry concentration, characteristics, and participants. There is a moderate degree of innovation, a moderately high level of merger & acquisition activities, high impact of regulations, and moderate regional expansion.

The degree of innovation in the artificial disc replacement market is moderate, with numerous companies investing in research and development to create more advanced and efficient products. In February 2025, Highridge Medical initiated a limited U.S. launch of the activL Lumbar Disc, with early procedures completed at leading disc replacement centers.

To improve their market position, several companies participate in mergers and acquisitions. These activities boost their market expertise, diversify their product offerings, and enhance skills. In February 2024, Globus Medical, Inc announced an agreement to acquire NuVasive in an all-stock transaction valued at approximately USD 3.1 billion, aimed at expanding its spine technology portfolio, including cervical total disc replacement (ADR) solutions.

The impact of regulations on the artificial disc replacement industry is high. To bring a new artificial disc replacement product to market, companies must comply with a wide range of regulatory requirements, including conducting clinical trials and obtaining regulatory approvals from bodies such as the FDA. These regulations can be time-consuming and expensive, limiting the number of new products that reach the market. Regulations can also vary by region, creating challenges for companies looking to expand their operations globally.

The product expansion in the artificial disc replacement market is low to moderate. The companies are expanding products and product lines. For instance, in March 2025, Spineway, known for advanced spinal implants, announced that its subsidiary Spine Innovations had obtained GMED approval for a new production line for its LP-ESP and CP-ESP disc prostheses. This milestone strengthens the group’s ability to manufacture and supply its innovative ESP implants.

The level of regional expansion is low. While several established players already exist, there are still opportunities for growth and expansion in certain regions. For instance, in September, 2025, SpineArt announced a USD 31 million (CHF 25 million) capital increase backed by investors to accelerate global expansion, including scaling its motion-preserving technologies, such as the BAGUERA disc platform, and strengthening its international market presence.

Material Type Insights

The metal-on-polymer (MoP) segment dominated the artificial disc replacement market, accounting for a share of 53.7% in 2025, driven by their ability to combine mechanical strength with enhanced flexibility and motion preservation. The market growth is supported by the expansion of product portfolios and strategic initiatives by key players to strengthen their presence in motion-preserving spinal solutions. Companies are increasingly focusing on licensing agreements, product launches, and manufacturing scale-up to enhance their offerings and cater to a broader patient population. For instance, in July 2025, Highridge Medical announced that it had licensed the U.S. rights to the activL lumbar disc and planned to commence production for its commercial launch. This addition, alongside its existing Mobi-C cervical disc, significantly expands the company’s motion preservation portfolio and strengthens its position in the lumbar disc replacement market.

The polymer-based / elastomeric segment is projected to grow at the fastest CAGR over the forecast period. Surgeons are increasingly adopting advanced materials that support better clinical outcomes, reduced adjacent segment degeneration, and faster recovery. In July 2025, Spineway’s subsidiary Spine Innovations received GMED approval for a new production line in La Rochelle dedicated to LP-ESP and CP-ESP intervertebral disc prostheses. This enabled the company to initiate the first production of LP-ESP implants, double its manufacturing capacity, and secure its supply chain for innovative spinal implant solutions.

Indication Insights

The cervical disc replacement segment held the largest share of the artificial disc replacement industry in 2025 and is anticipated to grow at the fastest CAGR over the forecast period. Key factors contributing to this share include increasing regulatory approvals and the introduction of technologically advanced artificial disc systems designed to improve clinical outcomes. Innovations focused on motion preservation, spinal alignment, and enhanced patient outcomes are expanding the scope of cervical disc replacement and increasing its adoption as a preferred alternative to spinal fusion. For instance, in February 2026, Synergy Spine Solutions received U.S. FDA Premarket Approval for the Synergy Disc for single-level cervical indications, supported by an IDE study demonstrating superior clinical outcomes compared to fusion, including improved alignment, motion preservation, pain reduction, and patient-reported satisfaction.

The lumbar disc replacement segment is anticipated to grow significantly during the forecast period. Increasing surgeon adoption and early-stage commercialization of advanced artificial disc technologies are driving the market for lumbar disc replacement. Strategic product launches, with positive initial clinical feedback, are accelerating market penetration and expanding access to motion-preserving treatment options. For instance, in February 2026, Highridge Medical initiated a limited U.S. launch of the activL lumbar disc, with early procedures performed across multiple centers, demonstrating strong surgeon adoption, positive clinical feedback, and expanding access to motion-preserving solutions for patients with lumbar disc degeneration.

End Use Insights

The hospitals segment dominated the artificial disc replacement industry, accounting for the largest revenue share of 66.9% in 2025. This can be attributed to the rising demand for treatments for degenerative disc diseases and spinal disorders. The push for adopting advanced technologies and procedures, coupled with improvements in surgical techniques and implant materials, has made artificial disc replacement more popular. This led to increased patient volumes at hospitals offering the innovative procedure, highlighting a positive market trend.

The outpatient facilities segment is expected to grow significantly over the forecast period. The outpatient setting for artificial disc replacement (ADR) is driven by its demonstrated safety, efficiency, and potential to reduce hospital stays, surgical costs, and recovery time. In July 2025, new findings demonstrated that artificial disc replacement could be performed safely and efficiently in the outpatient setting. Analysis of 1,684 cervical ADR procedures at DISC Surgery Centers showed zero immediate complications, rapid discharge, and preserved spinal motion.

Regional Insights

The North America artificial disc replacement industry accounted for 47.8% share in 2025. The growth is driven by factors such as the rising prevalence of spinal disorders, including cervical and lumbar disc degeneration, and increasing adoption of minimally invasive, motion-preserving procedures. The region benefits from a well-established healthcare infrastructure, high patient awareness of advanced spinal treatments, and access to skilled orthopedic and neurosurgeons, contributing to market growth. Leading companies, including Medtronic, Globus Medical, and SpineArt SA, have a strong presence in the U.S., Canada, and Mexico, offering a wide range of cervical and lumbar disc replacement devices and competing for regulatory approvals and clinical adoption.

U.S. Artificial Disc Replacement Market Trends

The artificial disc replacement industry in the U.S. held the largest share of North America in 2025 and is expected to grow rapidly over the forecast period. FDA approvals for next-generation motion-preserving cervical discs are driving growth in the U.S. market by expanding treatment options and increasing physician and patient confidence in ADR procedures. In February 2026, Synergy Spine Solutions received FDA Premarket Approval (PMA) for its Synergy Disc for 1-level cervical indications (C3-C7). Clinical studies demonstrated superiority over fusion, with 87.1% composite clinical success, improved Neck Disability Index scores, and higher overall patient satisfaction, highlighting the device’s safety, effectiveness, and alignment-preserving capabilities.

Europe Artificial Disc Replacement Market Trends

The Europe artificial disc replacement industry was a lucrative region in 2025, significantly driven by the rapidly aging population and rising median age across the region, which is increasing the prevalence of degenerative spinal conditions. For instance, according to Eurostat data published in February 2026, the median age in the European Union reached 44.9 years in 2025, with 22% of the population aged 65 and above, and projections indicating this could exceed 32% by 2100.

The UK artificial disc replacement market is witnessing a steady growth momentum due to the growing demand for minimally invasive spine surgeries and improved patient outcomes. The significant number of new and existing spinal cord injuries in the UK drives demand for advanced spinal treatments, including artificial disc replacement (ADR), as patients seek solutions to reduce pain, restore function, and improve quality of life. As of 2024, it is estimated that around 4,400 people experience a new spinal cord injury each year in the UK, and approximately 105,000 individuals are living with a spinal cord injury.

The artificial disc replacement market in France is expected to grow rapidly during the forecast period. Expansion of domestic manufacturing capabilities and regulatory approvals for production facilities are driving the growth of the artificial disc replacement (ADR) market in France by strengthening supply chain reliability, increasing production capacity, and supporting the availability of advanced spinal implants. In July 2025, Spineway received GMED approval for a new production line dedicated to LP-ESP and CP-ESP intervertebral disc prostheses. This enabled the company to initiate the first production of LP-ESP implants, double its manufacturing capacity, and secure the supply of innovative disc replacement devices.

Asia Pacific Artificial Disc Replacement Market Trends

The Asia Pacific region has a rapidly aging population in countries such as Japan, China, and South Korea, which is leading to a higher prevalence of degenerative spinal disorders and increased demand for motion‑preserving surgical solutions. Improving healthcare infrastructure, rising healthcare expenditure, and growing patient awareness of advanced spine treatments are expected to help manufacturers and healthcare providers capitalize on these opportunities. In addition, expanding access to specialized spine centers and investments in clinical training are improving adoption rates of ADR procedures across the region.

The China artificial disc replacement market is expected to grow during the forecast period. The increasing burden of traumatic spinal cord injuries and long‑term disability in China underscores a growing clinical need for advanced spinal care solutions, including motion‑preserving surgeries and regeneration‑oriented therapies, which in turn support investment and innovation in the spinal health market. A study conducted by the Global Burden of Disease in March 2023, China experienced substantial increases in the absolute number of spinal cord injury cases, with 232,656 incident cases in 2023, an approximately 43.6% rise since 1990, alongside growing prevalence and years lived with disability, highlighting a significant public health burden that may drive demand for advanced spine interventions.

The artificial disc replacement market in Japan is expected to grow over the forecast period, driven by an aging population and the rising prevalence of degenerative disc diseases. The government’s focus on promoting advanced healthcare technologies is driving the adoption of artificial disc replacements in this country. Moreover, cultural factors such as a preference for minimally invasive procedures are shaping the market trends in Japan. Recent data shows that Japan has one of the highest rates of spinal surgeries globally, indicating a significant demand for artificial disc replacements.

Latin America Artificial Disc Replacement Market Trends

Latin American countries, particularly Brazil, are actively improving regulatory efficiency and prioritizing the adoption of innovative medical technologies. Faster approval timelines and dedicated innovation committees are enabling quicker clinical validation and commercialization of advanced spine solutions, including artificial disc replacement. Governments and academic institutions across the region are investing in spinal disorder research, regenerative therapies, and biomaterials. This growing R&D ecosystem supports long-term adoption of advanced motion-preserving technologies.

The artificial disc replacement market in Brazil is expected to grow over the forecast period, driven by the country’s improving economic conditions, which have led to higher healthcare spending among its population, thereby increasing demand for advanced medical procedures such as artificial disc replacements. Brazil is significantly investing in next-generation healthcare infrastructure, including smart hospitals equipped with digital technologies such as AI, telemedicine, and advanced surgical capabilities. These developments are enhancing access to high-complexity care, improving surgical efficiency, and creating a favorable environment for the adoption of advanced spine procedures such as artificial disc replacement.

MEA Artificial Disc Replacement Market Trends

The MEA artificial disc replacement industry is expected to grow significantly. The region is witnessing a steady increase in musculoskeletal conditions due to aging populations, sedentary lifestyles, and rising obesity rates, all of which contribute to degenerative disc disease. In 2023, a study published in The Lancet Rheumatology (Global Burden of Disease analysis) highlighted that low back pain remains one of the leading causes of disability globally, including across the Middle East and Africa, with a consistently high prevalence and years lived with disability, emphasizing the growing clinical need for effective spine interventions.

The Saudi Arabia artificial disc replacement market’s growth is driven by significant healthcare system transformation, infrastructure expansion, and increased investment in advanced medical technologies. Governments in the region, particularly Saudi Arabia, are focusing on improving access to specialized care and modernizing healthcare delivery. A report published by the Health Sector Transformation Report in 2024 under Vision 2030 highlights that Saudi Arabia is actively developing integrated healthcare clusters, expanding hospital infrastructure, increasing private sector participation, and strengthening workforce capacity.

Key Artificial Disc Replacement Company Insights

This market is highly competitive. Companies implement strategic initiatives, such as product development & launches, expansion of their distribution networks, and expansion of their global footprint through subsidiaries and partnerships. Key companies are also involved in portfolio diversification and mergers & acquisition.

Key Artificial Disc Replacement Companies:

The following key companies have been profiled for this study on the artificial disc replacement market.

- Medtronic, Inc.

- Normmed Medical.

- Globus Medical, Inc.

- Dymicron, Inc.

- HIGHRIDGE MEDICAL

- AxioMed LLC

- Neuro France Implants

- SpineArt SA

- Synergy Spine Solutions Inc.

- Centinel Spine, LLC

- Aditus Medical

- B Braun Melsungen

- Spineway Group

- Prodorth Spine

- SIGNUS Medizintechnik GmbH

Recent Developments

-

In February 2026, Highridge Medical initiated a limited U.S. launch of the activL Lumbar Disc, with early procedures successfully completed at leading disc replacement centers. This marks a major expansion of its motion-preservation portfolio beyond the Mobi-C cervical disc, improving access to artificial lumbar disc replacement for patients and surgeons.

-

In January 2026, Dymicron announced the first patient enrollment in its U.S. IDE clinical trial for the Triadyme -C cervical disc, marking the transition from regulatory approval to active clinical validation. The study is being conducted across multiple U.S. centers and aims to generate data supporting future FDA approval and market entry.

-

In July 2025, Dymicron received U.S. FDA Investigational Device Exemption (IDE) approval for its Triadyme-C artificial cervical disc, allowing the company to initiate a multi-center pivotal clinical trial in the U.S. This milestone enables evaluation of the device’s safety and effectiveness compared to fusion procedures and represents a key step toward future commercialization.

-

In March 2025, SpineArt revealed a USD 31 million (CHF 25 million) capital increase backed by investors to accelerate global expansion, including scaling its motion-preserving technologies such as the BAGUERA disc platform and strengthening international market presence

-

In February 2024, NGMedical GmbH announced the sales launch and completion of the first surgery using their MOVE-C cervical artificial disc replacement in the UAE. This followed the approval of the MOVE-C device in Mexico, marking a significant step in NGMedical's global commercialization efforts. The first MOVE-C disc was implanted in Abu Dhabi.

Artificial Disc Replacement Market Report Scope

Report Attribute

Details

Market size in 2025

USD 686.8 million

Estimated market size in 2026

USD 743.2 million

Projected market size by 2033

USD 1,329.4 million

Growth rate

CAGR of 8.7% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material type, indication, end use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; South Korea; Thailand; Australia; Brazil; Argentina; South Africa;Saudi Arabia; UAE; Kuwait

Key companies profiled

Medtronic, Inc.; Normmed Medical.; Globus Medical, Inc.; Dymicron, Inc.; HIGHRIDGE MEDICAL ; AxioMed LLC; Neuro France Implants; SpineArt SA; Synergy Spine Solutions, Inc.; Centinel Spine, LLC;Aditus Medical; B Braun Melsungen; Spineway Group; Prodorth Spine; SIGNUS Medizintechnik GmbH

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Artificial Disc Replacement Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global artificial disc replacement market report based on material type, indication, end use, and region:

-

Material Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Metal-on-Polymer (MoP)

-

Metal-on-Metal (MoM)

-

Polymer-Based / Elastomeric

-

Others (Ceramic / Hybrid)

-

-

Indication Outlook (Revenue, USD Million, 2021 - 2033)

-

Cervical Disc Replacement

-

Lumbar Disc Replacement

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals

-

Outpatient Facilities

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

Kuwait

-

UAE

-

-

Frequently Asked Questions About This Report

Key factors that are driving the rising incidence of degenerative spinal disorders, influenced by sedentary lifestyles, obesity, and increasing cases of work-related spinal strain. Technological advancements in motion-preserving implants, including enhanced biomaterials and minimally invasive surgical approaches, are improving clinical outcomes and accelerating adoption.

Asia Pacific is the fastest-growing region over the forecast period.

The metal-on-polymer (MoP) segment led with a 53.7% revenue share in 2025, while the polymer-based/elastomeric segment is the fastest-growing.

The cervical disc replacement segment held the largest revenue share in 2025, while the lumbar disc replacement segment is anticipated to grow significantly.

The hospitals segment led with a 66.9% revenue share in 2025, while the outpatient facilities segment is is expected to grow significantly.

The global artificial disc replacement market size was estimated at USD 686.8 million in 2025 and is expected to reach USD 743.2 million in 2026.

The global artificial disc replacement market is expected to grow at a compound annual growth rate of 8.7% from 2026 to 2033 to reach USD 1,329.4 million in 2033.

North America dominated the artificial disc replacement market with a share of 47.8% in 2025. This is attributable to the rising prevalence of spinal disorders, including cervical and lumbar disc degeneration, and increasing adoption of minimally invasive, motion-preserving procedures

Some key players operating in the artificial disc replacement market include Medtronic, Inc; Orthofix Medical, Inc.; Globus Medical, Inc; Dymicron, Inc; HIGHRIDGE MEDICAL ; AxioMed LLC; Neuro France Implants; SpineArt SA; Synergy Spine Solutions, Inc.; Centinel Spine, LLC; Johnson & Johnson; B Braun Melsungen; Spineway Group; Prodorth Spine,SIGNUS Medizintechnik GmbH

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.