- Home

- »

- Clothing, Footwear & Accessories

- »

-

Back To School Market Size & Share, Industry Report, 2033GVR Report cover

![Back To School Market Size, Share & Trends Report]()

Back To School Market (2025 - 2033) Size, Share & Trends Analysis Report By Product (Clothing & Accessories, Stationery Supplies, Electronics), By Distribution Channel (Offline, Online), By Region, And Segment Forecasts

Market Size, 2024

$172.4BMarket Estimate, 2026

$181.8BMarket Forecast, 2033

$259.7BCAGR, 2025–2033

4.6%Back To School Market Summary

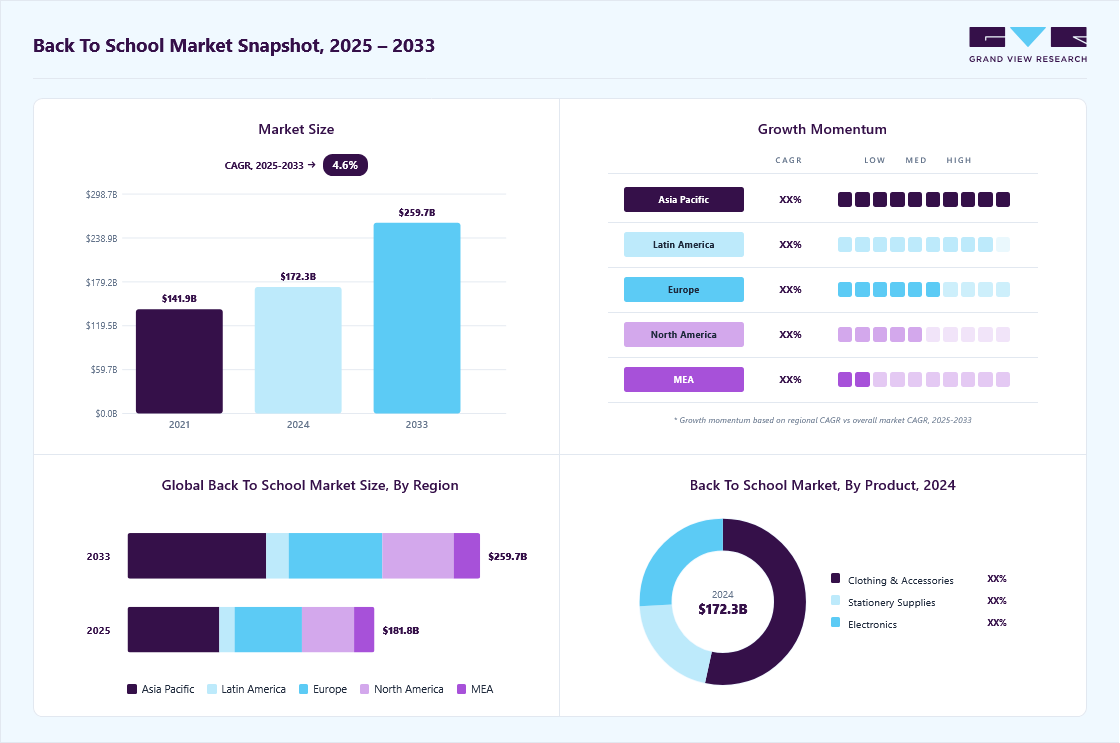

The global back to school market size was estimated at USD 172.35 billion in 2024 and is projected to reach USD 259.71 billion in 2033, growing at a CAGR of 4.6% from 2025 to 2033. Each year, as summer draws to a close, parents and students prepare for the new academic year, leading to a surge in demand for school supplies, apparel, electronics, and other essential items.

Key Market Trends & Insights

- Asia Pacific dominated the global back to school market with a revenue share of 36.88% in 2024.

- The China back to school industry reflects a rapidly changing landscape heavily influenced by digitalization and consumer technology.

- Based on product, the clothing & accessories segment accounted for a share of 53.35% in 2024.

- By distribution channel, the offline segment dominated the global back to school industry, accounting for a share of 61.54% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 172.35 Billion

- 2033 Projected Market Size: USD 259.71 Billion

- CAGR (2025-2033): 4.6%

- Asia Pacific: Largest market in 2024

Recent data indicate a growing inclination towards eco-friendly products, spurred by heightened environmental awareness among consumers. This trend is particularly prevalent among younger generations, who prioritize sustainability in their purchasing decisions. Moreover, retailers are responding to this demand by incorporating more environmentally friendly products into their campaigns, showcasing biodegradable materials, recycled notebooks, and sustainably sourced clothing.The increasing need for digital tools in education has heightened the demand for laptops, tablets, and educational software, especially in the wake of the COVID-19 pandemic, which accelerated the adoption of remote learning. As hybrid learning models become more commonplace, parents are investing in high-quality electronic devices that can facilitate both in-person and online learning environments. Moreover, the rise of e-learning has also prompted retailers to expand their product offerings to include educational apps and digital subscriptions, making technology a central pillar of back to school shopping lists for many families.

")

Another trend influencing the back to school market is the shift towards personalization and customization. Brands are recognizing that students seek unique products that express their style or identity. This trend has led to a surge in personalized school supplies, ranging from custom-printed backpacks to monogrammed lunchboxes. Retailers are leveraging digital technologies to offer customization options that cater to personal preferences, providing a more engaging shopping experience. The strategy not only boosts customer loyalty but also allows retailers to command higher prices for tailored products, enhancing their overall profitability during the peak back to school season.

With inflationary pressures affecting household budgets, many families are more budget-conscious than ever when it comes to back to school spending. Prominent discount retailers and online marketplaces are increasingly becoming preferred shopping destinations as parents seek value without compromising on quality. In addition, the rise of 'back to school' sales events and promotions indicates a shift in consumer expectations; parents are looking for cost savings and deals that can ease the financial burden of preparing for a new school year. As a result, brands and retailers need to strategically align their pricing and marketing efforts to resonate with budget-conscious consumers while delivering the quality and innovation they demand.

The rise of e-commerce has further facilitated this trend by providing consumers with a broader range of options and price comparisons, empowering them to make more informed purchasing decisions. Laptops and tablets provide the portability and functionality necessary for students to attend virtual classes, complete assignments, and participate in group projects. Furthermore, enhanced features such as high-definition cameras, improved battery life, and lightweight designs are influencing purchasing decisions, as parents seek out products that can support diverse learning environments.

Consumer Insights

According to the NRF 2025 press release, the U.S. back to school shopping season is being defined by early purchase behavior driven by price sensitivity. Nearly 67% of families had already started buying school items by early July, compared to 55% a year earlier, a direct reflection of tariff-related price concerns influencing purchase timing. Yet, even with this early start, 84% of shoppers still had half or more of their lists left to buy, indicating deliberate pacing as parents wait for price drops, finalize school supply lists, or spread their spending across pay cycles.

For K-12 households, the average budget is set at USD 858, with the largest allocations going to electronics, USD 296; clothing, USD 249; footwear, USD 169; and supplies, USD 144. While this is slightly below last year’s per-family average, total spend is projected to rise to USD 39.4 billion, indicating growth in participation rather than inflation in individual spending.

Shopping behavior reflects a pragmatic balancing of convenience and cost. More than half of K-12 consumers anticipate making online purchases, while discount chains, department stores, and apparel retailers remain popular for price-driven purchases. College shoppers, meanwhile, are leaning more heavily into discount formats this year, with value stores seeing a five-point jump in preference, the strongest shift across all back-to-college retail channels.

Seasonality Trends

The back to school market consistently represents a major seasonal peak in the retail calendar, akin to other key retail occasions, and brands and retailers align their launches, logistics, and campaigns accordingly. In India, for example, the new academic-year cycle triggers a significant uptick in demand in the April-June window. One report noted that the stationery and writing-instrument categories spike by roughly 30% during this period as parents and students complete their shopping before the term begins. Meanwhile, in the United States, large retailers schedule their largest back to school initiatives in the late July to early August timeframe. For example, Target’s “Back to School Days” promotional week, which ran from July 27 to August 2, featured deep discounts and experiential in-store events. Because of these predictable windows, brands know to ramp up production, adjust their supply chains, deploy seasonal assortments, and provide omnichannel support well ahead of the actual school-opening date.

As these seasonal peaks approach, consumer behaviour and channel dynamics shift in ways that brands must anticipate. One clear trend is that consumers begin planning and “list building” weeks earlier in the summer, often through social media and digital content. For instance, social video platform content is playing a growing role in back to school campaigns, as brands utilize influencer-led challenges, user-generated content, and tag-driven formats to capture early intent. In terms of channels, traditional physical retail still handles the bulk of the essentials, but online and omnichannel fulfilment are escalating dramatically. Even in India, e-commerce volumes increasingly mirror brick-and-mortar peaks as platforms run dedicated “Back to School” playlists and verticals.

Brand and retailer responses to this season-specific rhythm are now highly sophisticated, involving product innovation, experiential marketing, and multi-channel orchestration. For example, Target introduced “Personalization Stations” in-store and online from July 28 through September 8, enabling students to customise backpacks, lunchboxes, and water bottles with pins, patches, and other adornments. The retailer thereby transformed what might have been a commodity purchase into an experience, increasing engagement and in-store dwell time. Similarly, in India, home-ware brand Milton launched its “Milton Liya Kya?” (Did You Take Milton?) campaign ahead of the academic season. The brand rolled out over 75 colour variants of tiffins and bottles, tied a viral jingle, and activated across OOH, metro branding, social media, and on-ground displays. These campaigns reflect how brands leverage the season as a “fresh start” moment, cueing parents and students to upgrade gear, express identity, and switch brands.

Product Insights

The clothing & accessories segment accounted for a 53.35% share of the global revenue in 2024. As students return to school in late summer and early autumn, they need versatile clothing that can adapt to fluctuating temperatures. This need encourages the purchase of layered clothing, such as long-sleeve tops, jackets, and comfortable shoes. Furthermore, most schools have specific dress codes or uniform requirements, making it necessary for parents to shop for compliant attire. This combination of practicality and school regulations has a significant impact on purchasing behavior, prompting families to allocate budgets specifically for back to school clothing.

The electronics segment is expected to grow at a CAGR of 5.6% from 2025 to 2033. As classrooms shift towards digital learning environments, students require various electronic devices, including laptops, tablets, and smartphones, to facilitate their studies. This trend is particularly pronounced in higher education and hybrid learning models, where students are expected to engage with online platforms for assignments and collaboration. Consequently, brands that offer innovative, high-performance electronics that cater to educational needs are well-positioned to capitalize on this surge in demand.

Distribution Channel Insights

The sales of back to school products through offline channels accounted for a revenue share of 61.54% in 2024. Parents and students favor physical stores for several reasons, including the ability to inspect products firsthand, which is particularly crucial when it comes to items such as clothing, backpacks, and school supplies. This hands-on interaction helps customers feel confident in their purchases, knowing they are selecting items that meet their specific needs and preferences. Moreover, seasonal promotions and discounts play a significant role in driving demand through offline channels. Retailers typically ramp up marketing efforts leading up to the back to school period, offering exclusive in-store sales, bundle deals, and loyalty rewards. These promotions can create an inviting atmosphere that encourages customers to shop early and often, fostering a sense of urgency.

The sales of back to school through online channels are expected to grow at a CAGR of 5.8% from 2025 to 2033. Online platforms offer an extensive range of products, from stationery to clothing and electronics, enabling parents to fulfill their shopping needs quickly and efficiently without the stress of crowded stores. Through e-commerce websites and mobile applications, consumers can easily compare prices, read product reviews, and access user-generated content that helps inform their decision-making. Moreover, online retailers often implement attractive promotional strategies, such as discounts, bundle offers, and special deals, specifically geared toward the back to school season, incentivizing buyers to complete their purchases before the school year begins.

Regional Insights

The back to school industry in North America captured a revenue share of over 21.23% of the global market in 2024. In the U.S. and Canada, the trend of sustainable schooling is emerging, as parents increasingly seek eco-friendly supplies, from recycled notebooks to ethically manufactured apparel. This shift reflects a growing awareness of environmental issues among consumers, influencing purchasing decisions to favor companies that uphold sustainable practices. Regions such as California and New York are at the forefront of promoting green products, as consumers in these areas tend to prioritize sustainability. Retailers are adapting their strategies by stocking innovative products that align with this focus, while also utilizing digital marketing campaigns on social media to effectively reach eco-conscious shoppers.

U.S. Back To School Market Trends

The U.S. back to school industry is expected to grow at a CAGR of 3.8% from 2025 to 2033. The market is experiencing robust growth, fueled by a shift towards increased online shopping as families seek convenience in their purchasing decisions. Major retailers are investing in their e-commerce capabilities and collaborating with third-party delivery platforms to meet the demand for same-day or next-day delivery. Furthermore, the integration of technology in shopping experiences, such as personalized recommendations based on past purchases, has also contributed to the growth of this trend. According to recent studies, over 70% of parents in the U.S. express a preference for online shopping, citing time constraints and safety as significant factors in their decision-making.

Europe Back To School Market Trends

The back to school industry in Europe is expected to grow at a CAGR of 4.2% from 2025 to 2033. The market in the region demonstrates diversity driven by various cultural and economic factors within different countries. Western European nations, such as Germany and France, are showcasing a trend towards premium educational supplies and technology, which is anticipated to enhance learning experiences. Moreover, Eastern European markets are more price-sensitive, with consumers seeking affordable options that fit their increasingly tight budgets.

The Germany back to school industry is experiencing a transformation driven by a mix of traditional values and modern consumer habits. Parents typically visit local stores to purchase essential supplies such as stationery, backpacks, and lunchboxes for their children as school starts in late summer. However, there is a noticeable rise in the popularity of on-demand delivery services, powered by the increasing demand for convenience and faster purchasing options. Many German retailers are enhancing their e-commerce platforms, offering express delivery options and free shipping on larger orders to attract tech-savvy families who prefer online ordering.

The back to school industry in the UK is characterized by a blend of traditional shopping with a rising preference for online purchases. Parents are increasingly looking for convenience and efficiency when purchasing school supplies, clothing, and accessories for their children. As a result, retailers are responding by enhancing their online shopping platforms and leveraging on-demand delivery services. Moreover, consumers in the country are prioritizing eco-friendly products and brands that promote ethical manufacturing practices.

Asia Pacific Back To School Market Trends

The back to school industry in the Asia Pacific dominated the market with a share of 36.88% in 2024 and is expected to witness a CAGR of 5.3% from 2025 to 2033. The region is seeing a robust revival in the market, driven primarily by the resumption of in-person classes after pandemic-driven disruptions. This trend is reflected in a renewed demand for traditional school supplies, including backpacks, stationery, and uniforms. Urban centers in countries such as China, India, and Japan are witnessing higher spending on educational technology, with parents keen on providing their children with devices that facilitate learning and engagement. Moreover, countries such as South Korea and Singapore are leading this trend, with parents prioritizing quality educational tools to give their children a competitive edge.

The China back to school industry reflects a rapidly changing landscape heavily influenced by digitalization and consumer technology. Families are increasingly utilizing e-commerce platforms for shopping, with an emphasis on speed and efficiency. On-demand delivery services have become a staple for many parents, enabling them to quickly purchase school supplies, clothing, and electronics. Moreover, major online platforms, like Alibaba.com, Taobao, and JD.com, have reported significant increases in sales during the back to school period, responding with promotions and specially curated product categories designed to meet consumer needs.

The back to school industry in India is entering a new phase characterized by rapid shifts in consumer behavior and lifestyle changes, especially spurred by the pandemic's aftereffects. Traditionally, Indian families would stock up on school supplies during the peak back to school season, often visiting local stores and street markets. However, with the rise of the digital economy, there has been a significant increase in online shopping, with e-commerce giants like Amazon and Flipkart quickly adapting to the demand for on-demand delivery services. As technology becomes increasingly integrated into daily life, parents are turning to online shopping not just for convenience but also for access to a broader range of products at competitive prices.

Central & South America Back To School Market Trends

The back to school industry in Central and South America is characterized by a blend of traditional purchasing behaviors and the adaptation of digital commerce. As the economy gradually stabilizes, families are prioritizing essential school supplies while remaining cost-conscious. Countries like Brazil and Argentina have witnessed an uptick in demand for budget-friendly options as consumers navigate economic challenges. Local retailers are responding by offering bundled deals and promotions that emphasize value and accessibility, creating a competitive landscape as they vie for customers’ attention during the back to school season.

Middle East & Africa Back To School Market Trends

The back to school industry in the Middle East & Africa is poised for growth, driven by rising populations and a greater emphasis on education. Countries such as the UAE and Saudi Arabia are witnessing increasing investment in educational resources, alongside a culture that emphasizes high-quality education. Families are increasingly seeking premium products, including advanced learning materials and school supplies that meet global standards. The presence of international retailers in these markets provides parents with a wider selection of high-quality products, thereby enriching the local educational landscape.

Key Back To School Company Insights

The back to school industry has seen a dynamic shift as major players adapt to emerging consumer needs and changing educational landscapes. Manufacturers are increasingly focusing on innovative product launches to meet the changing needs of students and educators. With the rise of remote learning and hybrid classrooms, there is a growing demand for technology-infused supplies, such as smart notebooks, digital planners, and educational apps. In response, manufacturers are ramping up their research and development (R&D) investments, enabling them to create cutting-edge products that enhance learning experiences. By leveraging expertise and resources, these partnerships allow for the development of integrated solutions that not only cater to the immediate demands of back to school shopping but also anticipate future educational trends. In addition to product innovation, the back to school market has witnessed an increase in mergers and acquisitions as companies seek to consolidate their positions and expand their market reach.

Key Back To School Companies:

The following are the leading companies in the back to school market. These companies collectively hold the largest market share and dictate industry trends.

- The ODP Corporation

- Acco Brands Corporation

- Staples Inc.

- Apple Inc.

- HP Inc.

- Faber Castell AG

- Newell Brands Inc.

- ITC Ltd.

- Pelikan

- Mitsubishi Pencil Co. Ltd.

Recent Developments

-

In August 2024, Apparel Group's R&B brand introduced its Back to school Collection in the UAE, aiming to offer trendy and budget-friendly styles that appeal to both students and parents. The company’s strategy centered on utilizing social media marketing and collaborating with influencers to enhance brand awareness and connect with the younger audience.

-

In February 2024, Mitsubishi Pencil announced the acquisition of LAMY to expand its product lineup and strengthen its foothold in the premium stationery market, especially for back to school products. This acquisition will enhance Mitsubishi's competitive position, foster opportunities for collaboration between brands, and unlock new avenues for growth in both traditional and digital stationery markets.

Back To School Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 181.84 billion

Revenue forecast in 2033

USD 259.71 billion

Growth rate

CAGR of 4.6% from 2025 to 2033

Actual data

2021 - 2024

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; China; Japan; India; South Korea; Australia & New Zealand; Brazil; South Africa

Key companies profiled

The ODP Corporation; Acco Brands Corporation; Staples Inc.; Apple Inc.; HP Inc.; Faber Castell AG; Newell Brands Inc.; ITC Ltd.; Pelikan; Mitsubishi Pencil Co. Ltd.

Customization scope

Free Report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Back To School Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global back to school market report based on product, distribution channel, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Clothing & Accessories

-

Electronics

-

Stationery Supplies

-

-

Distribution Channel Outlook (Revenue, USD Million, 2021 - 2033)

-

Offline

-

Online

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

France

-

Germany

-

Spain

-

Italy

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia & New Zealand

-

South Korea

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa

-

South Africa

-

-

Frequently Asked Questions About This Report

The global back to school market size was estimated at USD 172.34 billion in 2024 and is expected to reach USD 181.84 billion in 2025.

The global back to school market is expected to grow at a compound annual growth rate of 4.6% from 2025 to 2033 to reach USD 259.70 billion by 2033.

The Asia Pacific dominated the back to school market with a share of 36.88% in 2024. This is attributable to the higher population in the region coupled with the increasing spending on school supplies.

Some key players operating in the back to school market include The ODP Corporation; Amazon.com, Inc.; Acco Brands Corporation; Staples Inc.; Apple Inc.; Faber Castell AG; Newell Brands Inc.; ITC Ltd.; Tommy Hilfiger B.V.; and Mitsubishi Pencil Co. Ltd.

Key factors that are driving the market growth include increasing enrollment of students in school, developments in retail sector of school supplies, and increasing expansion of educational institutes and organization.

About the Author(s)

Clothing, Footwear & Accessories Research Team

Consumer Goods · Clothing, Footwear & AccessoriesThis report was authored by the clothing, footwear & accessories research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clothing, footwear & accessories segment of the consumer goods industry. All findings are based on proprietary consumer goods databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.