- Home

- »

- Advanced Interior Materials

- »

-

Circular Construction Market Size, Industry Report, 2033GVR Report cover

![Circular Construction Market Size, Share & Trends Report]()

Circular Construction Market (2026 - 2033) Size, Share & Trends Analysis Report By Material Type (Recycled Aggregates, Recycled Metals, Reclaimed Wood, Recycled Plastics), By End Use (Residential, Non-residential), By Region, And Segment Forecasts

Market Size, 2025

$167.6BMarket Estimate, 2026

$185.4BMarket Forecast, 2033

$375.2BCAGR, 2026–2033

10.6%Circular Construction Market Summary

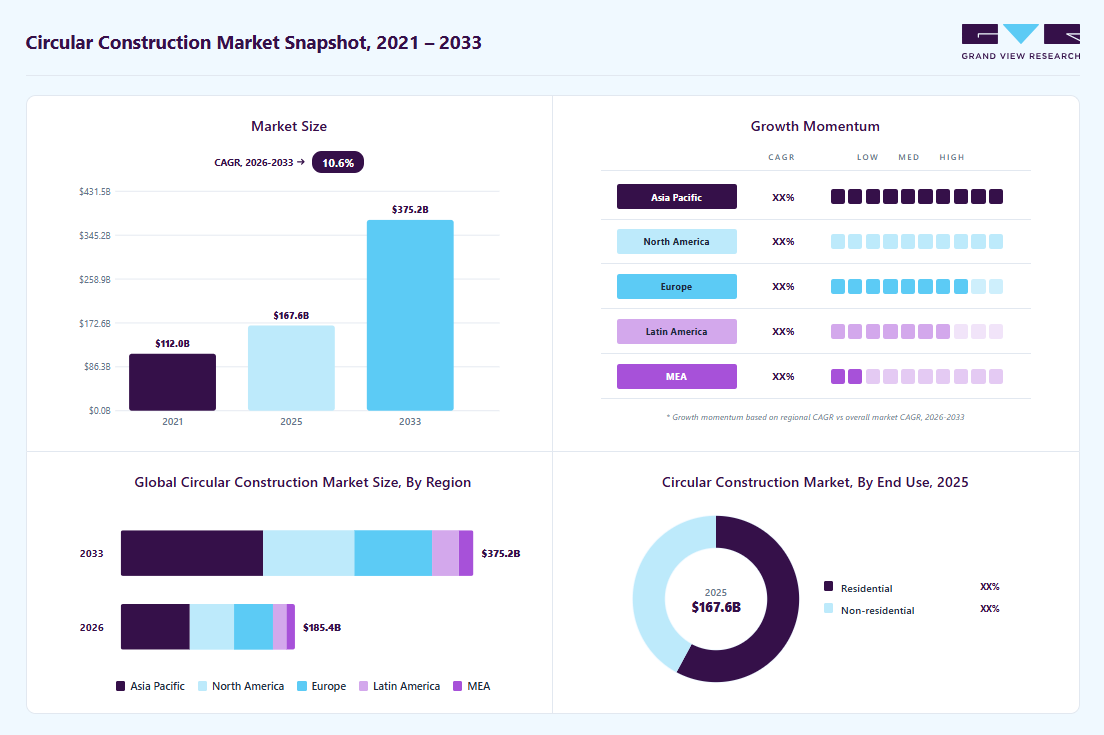

The global circular construction market size was estimated at USD 167.60 billion in 2025 and is projected to reach USD 375.24 billion by 2033, growing at a CAGR of 10.6% from 2026 to 2033. The demand for circular construction is increasing due to rising environmental concerns and the need to reduce construction waste.

Key Market Trends & Insights

- Asia Pacific dominated the circular construction market with the largest revenue share of 39.4% in 2025.

- By material type, the recycled plastics segment is expected to grow at the fastest CAGR of 11.4% over the forecast period.

- By end use, the non-residential segment is expected to grow at the fastest CAGR of 11.0% over the forecast period.

Market Size & Forecast

- 2025 Market Size: USD 167.60 Billion

- 2033 Projected Market Size: USD 375.24 Billion

- CAGR (2026-2033): 10.6%

- Asia Pacific: Largest Market in 2025

The construction sector is among the largest contributors to global carbon emissions and landfill waste. Governments and private developers are focusing on reducing material consumption and promoting reuse and recycling practices. Growing urbanization is putting pressure on natural resources, encouraging sustainable building methods. Companies are also adopting circular models to reduce long-term operational and material costs. Increasing awareness among investors and end users about green buildings is further accelerating adoption. As sustainability becomes a priority, circular construction practices are gaining mainstream acceptance.Key drivers include stricter environmental regulations and green building certifications such as LEED and BREEAM. The rising cost of raw materials is pushing developers to adopt recycled and reclaimed materials. Corporate ESG goals and net-zero commitments are prompting construction companies to redesign processes to improve resource efficiency. Technological advancements in material recovery, prefabrication, and modular construction are supporting circular practices. Demand for energy-efficient, low-carbon buildings in the residential and commercial sectors is also driving growth. Growing infrastructure investments in emerging economies are integrating sustainable frameworks from the planning stage. Additionally, digital tools like BIM are enabling better lifecycle management of materials.

")

Innovations such as modular construction and prefabrication are minimizing on-site waste and improving material efficiency. The use of recycled concrete aggregates, reclaimed steel, and bio-based materials is increasing. Design for disassembly (DfD) is becoming a key trend, allowing buildings to be dismantled and reused. Digital material passports are being developed to track materials throughout their lifecycle. 3D printing using recycled materials is emerging as a cost-effective and sustainable technique. Adoption of smart waste management systems on construction sites is also rising.

Market Concentration & Characteristics

The circular construction market is moderately fragmented with the presence of large construction firms, material manufacturers, recycling companies, and technology providers. Major global players are integrating circular strategies into their operations, while several regional players specialize in recycled materials and waste management solutions. Large firms have an advantage due to access to capital, technology, and established supply chains. However, innovation-driven startups are gaining traction by offering sustainable materials and digital platforms. Partnerships between contractors, material suppliers, and recycling firms are becoming common. Mergers and collaborations are helping companies expand their sustainable portfolios. The competitive landscape is evolving as sustainability becomes a core strategy.

Traditional linear construction methods remain the primary substitute for circular construction. Conventional building materials such as virgin cement, steel, and plastics are still widely used due to lower initial costs and established supply chains. Lack of awareness and higher upfront investment requirements can slow adoption of circular alternatives. In some developing regions, limited recycling infrastructure restricts implementation. However, increasing carbon taxes and regulatory pressure are reducing the attractiveness of traditional methods. Over time, cost advantages of resource efficiency and waste reduction are expected to lower the substitution threat. The long-term economic and environmental benefits support steady growth of circular construction practices.

Material Type Insights

The recycled aggregates segment held the highest revenue market share of 30.9% in 2025, primarily due to its wide application in road construction, foundations, and concrete production. Recycled concrete, asphalt, and demolition waste are extensively reused as cost-effective alternatives to virgin aggregates. Strong regulatory push toward construction and demolition (C&D) waste recycling has further supported segment growth. Infrastructure development projects globally prefer recycled aggregates to reduce environmental impact and material costs. Their easy availability and established supply chains make them the most commercially viable circular material category.

The recycled plastics segment is expected to grow at the fastest CAGR of 11.4% over the forecast period, due to increasing innovation in sustainable building materials. Recycled plastics are being used in insulation, piping, roofing membranes, and composite construction materials. Growing pressure to reduce plastic waste and landfill accumulation is encouraging its integration into building systems. Technological advancements are improving durability and structural performance of recycled plastic-based products. Additionally, rising green building certifications and eco-conscious developers are accelerating demand in this segment.

End Use Insights

The residential segment held the highest revenue market share of 57.9% in 2025, driven by high housing demand and sustainable home development initiatives. Increasing consumer awareness of energy-efficient and eco-friendly homes has boosted adoption of recycled and low-carbon materials. Modular housing, prefabrication, and design-for-disassembly concepts are being widely implemented in residential construction. Government incentives for green housing and net-zero homes further support this segment. Rapid urbanization in emerging economies also contributes to sustained residential demand.

The non-residential segment is expected to grow at the fastest CAGR of 11.0% over the forecast period, due to increasing sustainability commitments in commercial, industrial, and institutional infrastructure. Corporates are aligning new office buildings, retail spaces, and industrial facilities with ESG and carbon neutrality targets. Large-scale infrastructure projects are incorporating circular procurement strategies and material reuse practices. Green certifications such as LEED and BREEAM are becoming standard in commercial developments. As regulatory compliance and investor pressure increase, non-residential construction is expected to accelerate adoption of circular models.

Regional Insights

Asia Pacific dominated the global circular construction market, accounting for the largest revenue share of 39.4% in 2025, due to rapid urbanization and infrastructure expansion. Countries like China, India, and Japan are incorporating green building standards in urban planning. Growing awareness of waste management challenges is encouraging material recycling initiatives. Governments are promoting sustainable infrastructure through smart city programs. Rising investment in commercial and residential real estate is supporting demand. Increasing raw material prices in the region are also pushing adoption of recycled alternatives. The region is expected to maintain strong growth due to large-scale infrastructure projects.

China Circular Construction Market Trends

China is focusing on circular economy reforms to reduce construction waste and carbon emissions. The government promotes prefabricated buildings and recycled material usage. Urban redevelopment projects are integrating sustainable construction practices. Strong regulatory monitoring of construction waste disposal is encouraging recycling industries. Technological innovation in modular and industrialized construction is expanding. State-backed investments in green infrastructure further support growth. China remains a key revenue contributor in the region.

North America Circular Construction Market Trends

North America is driven by strict environmental regulations and growing ESG commitments from corporations. The U.S. and Canada emphasize sustainable urban development and green certifications. High awareness among consumers about sustainable housing is supporting market adoption. Advanced recycling infrastructure enables better material recovery. Renovation and retrofitting of old buildings create opportunities for circular material use. Private sector investment in sustainable construction startups is increasing. The region shows steady growth supported by regulatory enforcement.

The U.S. circular construction market is growing due to strong green building standards and net-zero targets. Federal and state policies promote energy-efficient and low-carbon construction. Circular material innovations such as recycled concrete and reclaimed wood are gaining popularity. Commercial real estate developers are adopting sustainable models to attract investors. Growth in modular housing is contributing to waste reduction. Increasing demolition waste recycling rates are strengthening the ecosystem. The U.S. remains a leading innovator in circular construction practices.

Europe Circular Construction Market Trends

Europe is a leader in circular construction due to strict sustainability mandates. The EU Circular Economy Action Plan strongly influences the building sector. High recycling targets for construction and demolition waste are driving adoption. Countries like Germany, Netherlands, and France are emphasizing lifecycle carbon assessment. Green public procurement policies are encouraging sustainable projects. Innovation in bio-based and low-carbon materials is expanding rapidly. Europe continues to set global benchmarks in circular building frameworks.

The Germany circular construction industry focuses on energy-efficient buildings and sustainable infrastructure development. Strict waste management policies support high recycling rates. The country promotes timber construction and recyclable building materials. Advanced engineering expertise enables innovation in modular and prefabricated designs. Strong government incentives for green buildings drive demand. Industrial players are integrating digital lifecycle tracking tools. Germany remains a key European contributor to circular construction advancements.

Latin America Circular Construction Market Trends

Latin America is gradually adopting circular practices due to increasing environmental awareness. Brazil and Mexico are promoting sustainable urban housing projects. Limited recycling infrastructure remains a challenge in some areas. However, rising foreign investment in infrastructure is encouraging green standards. Governments are introducing policies to manage construction waste more efficiently. Demand for cost-effective recycled materials is increasing. The region offers long-term growth potential with improving regulations.

Middle East & Africa Circular Construction Market Trends

The Middle East is integrating circular principles into large-scale infrastructure and smart city projects. Countries like UAE and Saudi Arabia promote sustainable urban development under national visions. Green building certifications are gaining importance in commercial projects. Africa is witnessing a gradual adoption due to infrastructure modernization. Waste management reforms are being introduced in select economies. Rising construction activities in the region create opportunities for recycled materials. Although adoption is still developing, long-term sustainability goals are supporting growth.

Key Circular Construction Company Insights

Some of the key players operating in the market include LafargeHolcim, KAJIMA CORPORATION

-

Holcim is a global leader in circular construction, focusing on low-carbon cement, recycled aggregates, and reuse of construction and demolition waste. Its circular material solutions support resource efficiency and reduced embodied carbon in building projects.

-

Kajima Corporation integrates circular construction practices through waste reduction, concrete recycling, and sustainable infrastructure development. The company emphasizes lifecycle efficiency and smart construction technologies to support the circular economy.

BAM and SEKISUI HOUSE, LTD. are some of the emerging market participants in the circular construction market.

-

Royal BAM Group applies circular economy principles across infrastructure and real estate projects, promoting material reuse and low-carbon construction. The company actively supports sustainable urban development in Europe.

-

Sekisui House advances circular construction in the residential sector through modular housing, material take-back programs, and energy-efficient building systems. Its focus on durability and resource recycling strengthens circular housing models.

Key Circular Construction Companies:

The following key companies have been profiled for this study on the circular construction market.

- LafargeHolcim

- Lendlease Corporation

- BAM

- KAJIMA CORPORATION

- CapitaLand

- Samsung C&T Corporation

- SEKISUI HOUSE, LTD.

- BESIX

- Skanska

- WSP Global

Recent Developments

-

In September 2025, Lendlease began construction on The Riverie residential towers in Brooklyn, New York, the largest geothermal residential project in the city, aimed at cutting annual carbon emissions from heating/cooling by ~53% vs conventional systems.

-

In September 2024, BAM started industrial & circular production of its modular wooden home concept “Flow,” aimed at sustainable, prefab, and rapid-build housing.

Circular Construction Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 185.36 billion

Revenue forecast in 2033

USD 375.24 billion

Growth rate

CAGR of 10.6% from 2026 to 2033

Base year for estimation

2025

Actual estimates/Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material Type, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Spain; China; Japan; India; South Korea

Key companies profiled

LafargeHolcim; Lendlease Corporation; BAM; KAJIMA CORPORATION; CapitaLand; Samsung C&T Corporation; SEKISUI HOUSE, LTD.; BESIX; Skanska; WSP Global

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Circular Construction Market Report Segmentation

This report forecasts revenue growth at regional & country levels and provides an analysis on the industry trends in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global circular construction market on the basis of material type, end use, and region:

-

Material Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Recycled Aggregates

-

Recycled Metals

-

Reclaimed Wood

-

Recycled Plastics

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Residential

-

Non-residential

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

-

Latin America

-

Middle East & Africa

-

Frequently Asked Questions About This Report

Some of the key players operating in the circular construction market include LafargeHolcim; Lendlease Corporation; BAM; KAJIMA CORPORATION; CapitaLand; Samsung C&T Corporation; SEKISUI HOUSE, LTD.; BESIX; Skanska; WSP Global

Key factors driving the circular construction market include rising sustainability goals, stricter waste management regulations, cost advantages of recycled materials, and growing adoption of green building practices.

The global circular construction market size was estimated at USD 167.60 billion in 2025 and is expected to reach USD 185.36 billion in 2026.

The global circular construction market is expected to grow at a compound annual growth rate of 10.6% from 2026 to 2033 to reach USD 375.24 billion by 2033.

The recycled aggregates segment held the highest revenue market share of 30.9% in 2025, primarily due to their wide-scale use in road construction, foundations, and structural concrete.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.