- Home

- »

- Healthcare IT

- »

-

Clinical Data Analytics Solutions Market Report, 2026-2033GVR Report cover

![Clinical Data Analytics Solutions Market (2026 - 2033)Report]()

Clinical Data Analytics Solutions Market (2026 - 2033)

Size, Share & Trends Analysis Report By Deployment (Cloud-Based, On-premise), By Application (Clinical Decision Support, Clinical Trials, Regulatory Compliance), By Region, And Segment Forecasts

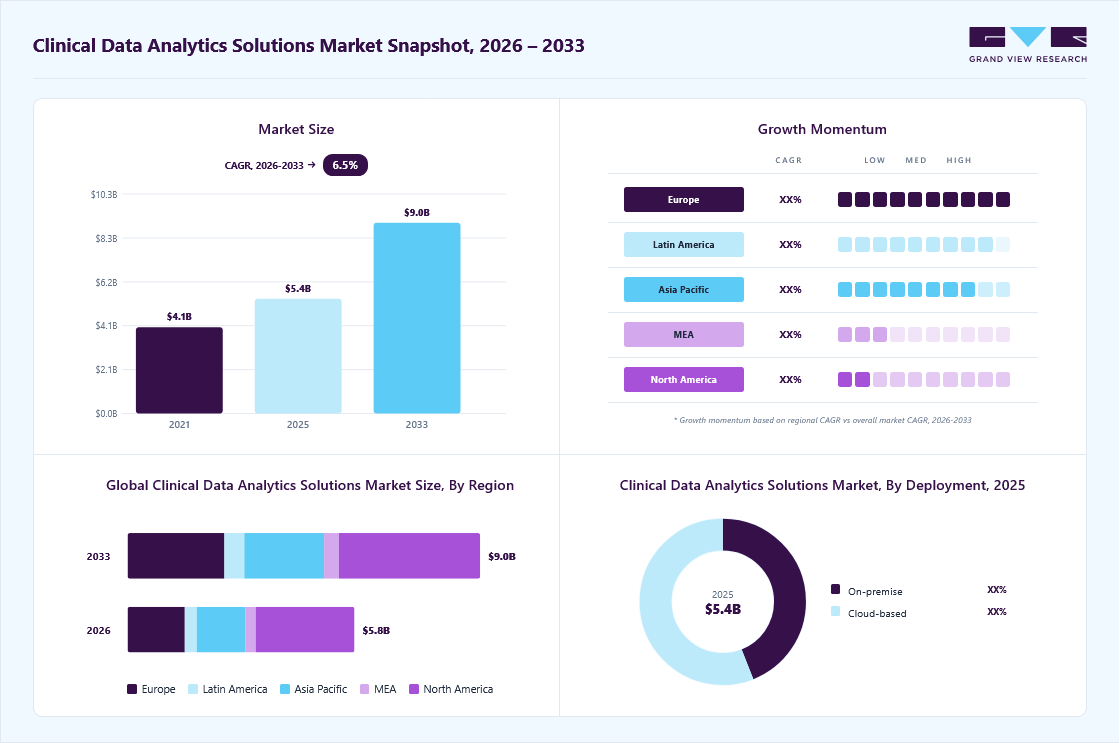

Market Size, 2025

$5.4BMarket Estimate, 2026

$5.8BMarket Forecast, 2033

$9.0BCAGR, 2026–2033

6.5%Clinical Data Analytics Solutions Market Summary

The global clinical data analytics solutions market size was valued at USD 5.4 billion in 2025 and is projected to grow from USD 5.8 billion in 2026 to USD 9.0 billion by 2033, at a CAGR of 6.5% from 2026 to 2033. The market in North America dominated with a revenue share of 42.6% in 2025. This growth is driven by rapid advancements in artificial intelligence (AI) and machine learning, which enhance diagnostic accuracy by identifying patterns in large datasets such as electronic health records (EHRs) and medical imaging, enabling improved prediction of patient outcomes and disease risks.

Key Market Trends & Insights

- By deployment: Cloud-based segment held the largest market share of 56.1% in 2025.

- By application: Clinical trials segment held the largest market share of 34.9% in 2025.

Regional Highlights

- Largest regional market: North America (42.6% revenue share, 2025)

- Fastest-growing regional market: Europe (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 5.4 Billion

- Estimated market size in 2026: USD 5.8 Billion

- Projected market size by 2033: USD 9.0 Billion

- CAGR (2026-2033): 6.5%

The rising demand for personalized diagnostic tests and treatments has led to a significant increase in clinical trials, generating vast volumes of data that require advanced analytics solutions for effective interpretation. This trend is accelerating the adoption of clinical data analytics platforms. For instance, in August 2023, Lokavant introduced a study planning solution that enables contract research organizations and sponsors to optimize site selection and overall study performance. The growing focus on population health management further supports market expansion.")

Moreover, several initiatives by market players are strengthening the adoption of advanced analytics tools. For instance, in September 2024, Komodo Health expanded its MapLab platform with the launch of MapAI and MapExplorer, enhancing collaborative analytics and enabling simplified, no-code access to patient, provider, and payer insights through AI-driven capabilities.

Market Characteristics & Concentration:

The global clinical data analytics solutions industry is characterized by a high degree of innovation, with new technologies being developed and introduced at regular intervals. Key players are continuously investing in AI/ML technologies to address the growing demand for advanced analytics solutions. For instance, in November 2025, Penguin AI partnered with UPMC Enterprises to co-develop advanced AI models aimed at enhancing clinical data analytics and accelerating real-world healthcare insights. This reflects the increasing focus on innovation and strategic collaborations to strengthen analytics capabilities in the market.

Several market players such as UnitedHealth Group, SAS Institute, and IQVIA are actively involved in merger and acquisition activities to expand their geographic presence and strengthen analytics capabilities. Through M&A, these companies enhance their service portfolios and enter new markets. For instance, in August 2025, Optum acquired Holston Medical Group to expand its healthcare delivery and data capabilities, reflecting a broader strategy of vertical integration and analytics-driven care expansion.

Stringent regulations enhance data security, driving demand for compliant clinical data analytics solutions. Companies face challenges in ensuring adherence to privacy and transparency requirements. The compliance costs are expected to rise; however, the emphasis on regulatory alignment increases trust and innovation.

Deployment Insights

Based on deployment, the market is segmented into cloud-based and on-premise. The cloud-based segment dominated the market with a revenue market share of 56.1% in 2025 and is anticipated to exhibit the fastest growth over the forecast period. This growth is driven by the scalability offered by cloud platforms, enabling healthcare organizations to efficiently adjust their analytics infrastructure in line with evolving data requirements, particularly in an industry characterized by fluctuating data volumes. In addition, cloud-based solutions eliminate the need for significant upfront investments in hardware and maintenance, allowing organizations to adopt cost-efficient pay-as-you-go models.

Based on deployment, the on-premise segment is expected to grow significantly over the forecast period. This growth is driven by the increasing need for enhanced data security, privacy, and regulatory compliance among healthcare organizations. On-premise solutions provide greater control over sensitive patient data and system customization, making them suitable for institutions with strict data governance requirements. However, growth is relatively moderate compared to cloud-based solutions due to higher infrastructure and maintenance costs.

Application Insights

The clinical trials segment held the largest market share of 34.9% in 2025, driven by growing awareness of the benefits of clinical data analytics solutions in this domain. In addition, the increasing number of clinical trials fueled by the rising demand for technologically advanced and cost-effective medical treatments, continues to support segment growth. According to a report by the WHO published in February 2023, the total number of clinical trials increased from 51,451 in 2017 to 54,954 in 2022.

The clinical decision support segment is expected to grow at the fastest CAGR over the forecast period. This is driven by the rising adoption of clinical decision support systems for customizing recommendations and treatment plans to individual patient profiles. Clinical data analytics solutions play a key role in enhancing CDS by offering patient-specific insights to clinicians and facilitating tailored and effective treatments. Furthermore, these solutions integrate artificial intelligence (AI) and machine learning into CDS applications, enabling predictive insights for early diagnosis and treatment planning. These factors are expected to drive growth in this segment over the forecast period.

Regional Insights

North America Clinical Data Analytics Solutions Market Trends

North America clinical data analytics solutions industry dominated with a revenue share of 42.6% in 2025. This is owing to the region's well-established healthcare infrastructure and widespread integration of advanced technologies. A rising incidence of chronic diseases and an aging population are compelling healthcare institutions in the region to adopt analytics solutions. Furthermore, the presence of major industry players drives market growth.

U.S. Clinical Data Analytics Solutions Market Trends

The clinical data analytics solutions industry in the U.S. held the largest share in 2025. This is due to the country’s advanced healthcare infrastructure and early adoption of digital health technologies. The increasing prevalence of chronic diseases and rising demand for value-based care are accelerating the adoption of data-driven solutions. Healthcare providers are increasingly leveraging AI and machine learning to enhance clinical decision-making and improve patient outcomes. In addition, strong investments by key players such as Optum, IQVIA, and Oracle Corporation are further supporting market expansion. The growing focus on interoperability and real-time data integration is also contributing to the increasing demand for clinical analytics solutions across the U.S. healthcare ecosystem.

Europe Clinical Data Analytics Solutions Market Trends

Europe clinical data analytics solutions industry is anticipated to witness the fastest growth at a CAGR of 7.8% from 2026 to 2033. This growth is driven by interoperability initiatives, crucial in a region where healthcare systems are diverse and often fragmented. In addition, the healthcare sector in Europe is enthusiastically embracing AI and machine learning technologies, especially in fields such as radiology and pathology, to efficiently analyze extensive datasets. Governments are also investing in digital health infrastructure and incentivizing the uptake of clinical data analytics solutions, with the aim of enhancing healthcare access, cost reduction, and improved patient outcomes.

The clinical data analytics solutions industry in the UK is experiencing significant growth, driven by increasing adoption of digital health technologies and strong government support for data-driven healthcare. The country is focusing on integrating advanced analytics within the NHS to improve patient outcomes and operational efficiency. For instance, in 2025, the UK government announced an investment of up to USD 657.7 million (Euro 600million) to develop a national health data research service, aimed at accelerating clinical research and analytics capabilities.

Asia Pacific Clinical Data Analytics Solutions Market Trends

The Asia Pacific clinical data analytics solutions industry is expected to witness significant growth over the forecast period, driven by rapid digital transformation in healthcare systems across emerging economies such as China, India, and Japan. Increasing adoption of electronic health records (EHRs), telemedicine, and AI-powered analytics solutions is accelerating market expansion. Government initiatives promoting healthcare digitization and investments in health IT infrastructure are further supporting growth. In addition, the rising prevalence of chronic diseases and growing demand for data-driven decision-making are contributing to increased adoption of advanced analytics solutions in the region.

Key Clinical Data Analytics Solutions Company Insights

Key players in the clinical data analytics solutions industry include IQVIA, SAS Institute, Optum, and Oracle. IQVIA focuses on providing advanced analytics and real-world evidence solutions to support clinical research and drug development, while SAS Institute offers AI-driven analytics platforms to enhance clinical decision-making. Optum delivers integrated analytics solutions to improve healthcare efficiency and patient outcomes, and Oracle provides cloud-based platforms enabling scalable and interoperable data analytics. These companies are actively engaged in strategies such as mergers and acquisitions, geographic expansion, and new product launches to strengthen their market presence and enhance their solution offerings.

Key Clinical Data Analytics Solutions Companies:

The following key companies have been profiled for this study on the clinical data analytics solutions market.

- Optum, Inc. (UnitedHealth Group)

- Oracle

- SAS Institute

- IQVIA

- Health Catalyst

- eClinical Solutions LLC

- OSP

- BD

- Dassault Systèmes

- Cognizant

- Epic Systems

- MedeAnalytics

- Veradigm

- ICON plc

- IBM

- Arcadia

Recent Developments

-

In January 2026, Oracle introduced advanced cloud-based healthcare analytics solutions integrating AI capabilities and interoperability standards such as HL7 and FHIR. These innovations enable real-time data processing, seamless integration across systems, and scalable analytics, reinforcing the growing reliance on cloud platforms in clinical data analytics.

-

In December 2025, Medicus Pharma Ltd. announced a strategic engagement with Reliant AI to develop an AI powered clinical data analytics platform. This collaboration outlines a multi-phase framework aimed at enabling capital-efficient, AI-powered development of Teverelix, a next-gen GnRH antagonist. The therapy is being positioned as a potential first in place treatment for acute urinary retention (AURr) and high cardiovascular-risk prostate cancer, collectively representing an estimated market opportunity of approximately $6 billion.

-

In January 2023, IQVIA announced a collaboration with Alibaba Cloud. This collaboration is anticipated to strengthen IQVIA’s geographical presence in China by better serving its customers.

-

In November 2022, Hartford HealthCare and Google Cloud announced a long-term partnership to enhance data analytics, advance digital transformation, and improve access and care delivery.

Clinical Data Analytics Solutions Market Report Scope

Report Attribute

Details

Market size in 2025

USD 5.4 billion

Estimated market size in 2026

USD 5.8 billion

Projected market size by 2033

USD 9.0 billion

Growth rate

CAGR of 6.5% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion & CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors and trends

Segments covered

Deployment, application, region

Regional Scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country Scope

U.S.; Canada; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; Japan; China; India; Australia; Thailand; South Korea; Brazil; Mexico; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Optum, Inc. (UnitedHealth Group); Oracle Corporation; SAS Institute; IQVIA; Health Catalyst; eClinical Solutions LLC; OSP; BD; Dassault Systèmes; Cognizant; Epic Systems; MedeAnalytics; Veradigm; ICON plc; IBM; Arcadia

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Clinical Data Analytics Solutions Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels and provides an analysis of the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global clinical data analytics solutions market report based on deployment, application, and region:

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

On-premise

-

Cloud-based

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Clinical Decision Support

-

Clinical Trials

-

Regulatory Compliance

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Norway

-

Denmark

-

Sweden

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

Key factors driving the market growth include the increasing need for advanced technologies such as AI in healthcare organizations, the growing number of clinical trials, and the rising prevalence of chronic diseases. Moreover, increasing focus on population health management and personalized patient care is anticipated to drive the market over the forecast period.

Some of key players include Optum, Inc. (UnitedHealth Group); Oracle Corporation; SAS Institute; IQVIA; Health Catalyst; eClinical Solutions LLC; OSP; BD; Dassault Systèmes; Cognizant; Epic Systems; MedeAnalytics; Veradigm; ICON plc; IBM; Arcadia

The cloud-based segment led with a 56.1% revenue share in 2025 while on-premise segment is fastest growing market

The clinical trials segment led with a 34.9% revenue share in 2025 while clinical decision support is the fastest growing segemnt.

The global clinical data analytics solutions market size was valued at USD 5.4 billion in 2025 and is estimated at USD 5.8 billion for 2026.

The global clinical data analytics solutions market is expected to grow at a CAGR of 6.5% from 2026 to 2033, reaching USD 9.0 billion by 2033.

North America dominated with a 42.6% revenue share in 2025.

Europe is the fastest-growing region over the forecast period.

About the Author(s)

Healthcare IT Research Team

Healthcare · Healthcare ITThis report was authored by the healthcare it research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the healthcare it segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.