- Home

- »

- Next Generation Technologies

- »

-

Compliance Software Market Size, Share Report, 2026-2033GVR Report cover

![Compliance Software Market (2026 - 2033)Report]()

Compliance Software Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Software, Services), By Application, By Deployment (Cloud, On-premise), By Enterprise Size, By End-use (IT & Telecom, Government), By Region, And Segment Forecasts

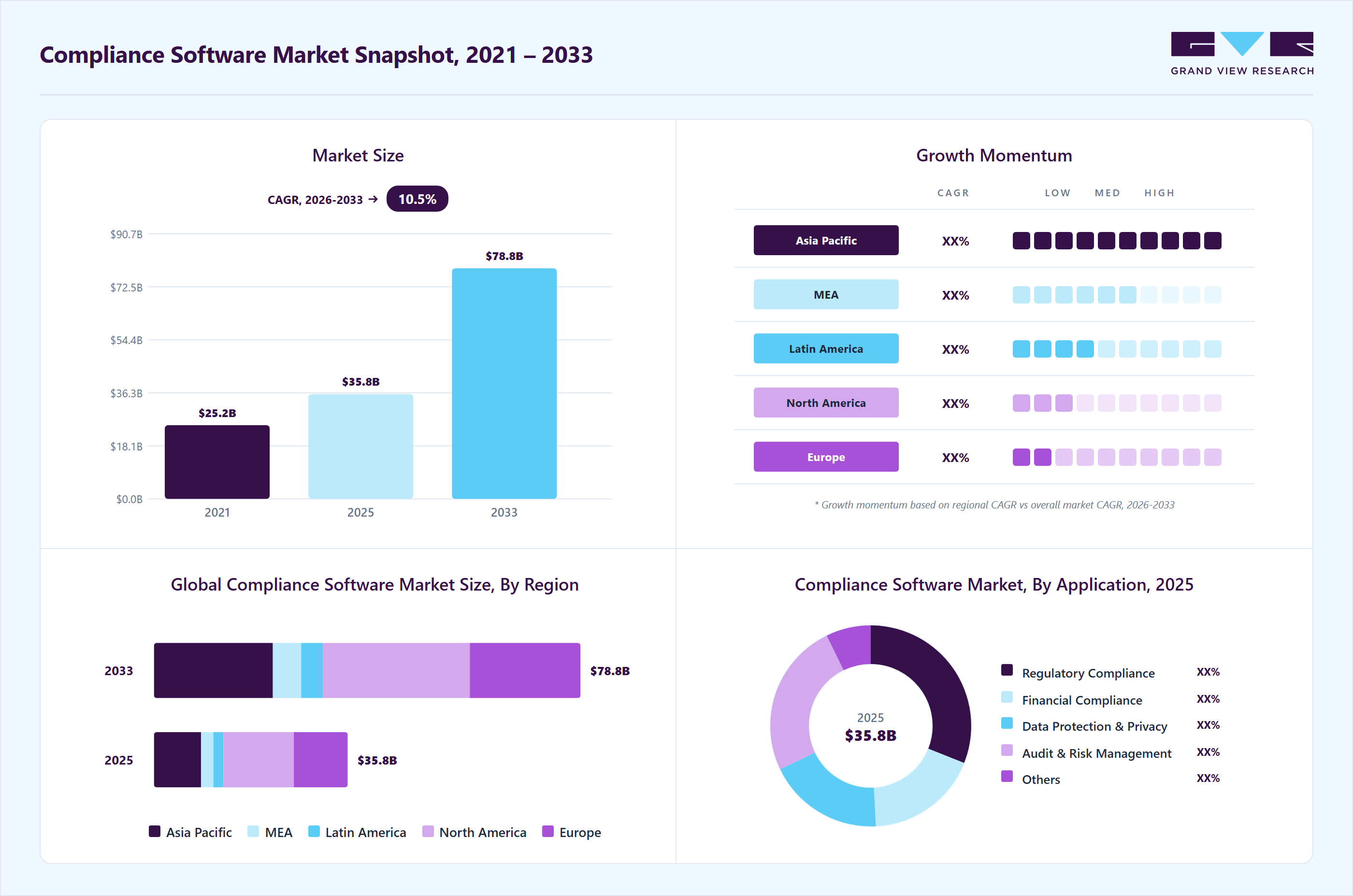

Market Size, 2025

$35.8BMarket Estimate, 2026

$39.3BMarket Forecast, 2033

$78.9BCAGR, 2026–2033

10.5%Compliance Software Market Summary

The global compliance software market size was valued at USD 35.8 billion in 2025 and is projected to grow from USD 39.3 billion in 2026 to USD 78.9 billion by 2033, at a CAGR of 10.5% from 2026 to 2033. The North America held the largest share of 36.3% of the global market in 2025. Increasing regulatory complexity across sectors is driving organizations to adopt compliance software for automation and scalability.

Key Market Trends & Insights

- By application: Regulatory compliance segment held the largest share of 31.1% in 2025.

- By component: Software segment accounted for the revenue share of 74.5% in 2025.

- By deployment: Cloud segment accounted for the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (36.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033).

- By country: The U.S. led the North America market in 2025.

Market Size & Forecast

- Market size in 2025: USD 35.8 Billion

- Estimated market size in 2026: USD 39.3 Billion

- Projected market size by 2033: USD 78.9 Billion

- CAGR (2026-2033): 10.5%

New and evolving laws such as GDPR, CSRD, DORA, and financial reporting regulations demand continuous monitoring, documentation, and reporting. Manual compliance processes are no longer sufficient to manage this volume and pace of change, prompting enterprises to invest in digital tools that ensure real-time oversight, reduce risk, and maintain adherence across jurisdictions.The compliance software market is witnessing significant transformation as businesses adapt to the complexities of modern regulatory landscapes. Technological advancements, especially in artificial intelligence (AI) and machine learning (ML), are reshaping how organizations manage compliance. These technologies enable the automation of repetitive tasks, real-time tracking of compliance activities, and predictive analytics to identify potential risks before they escalate. With increasing data privacy laws, financial reporting standards, and ESG mandates, companies are turning to AI-driven platforms to enhance transparency and responsiveness.

")

Automated compliance systems reduce manual intervention, minimize errors, and improve audit readiness across industries. Furthermore, the integration of AI supports continuous monitoring across multiple jurisdictions, ensuring faster adaptation to evolving regulations. As a result, organizations can streamline compliance operations, lower operational costs, and foster trust with regulators and stakeholders. This convergence of regulation and innovation is setting a new standard for intelligent, proactive compliance management worldwide.

The rapid adoption of cloud and Software-as-a-Service (SaaS) models is reshaping the compliance software market by providing greater scalability, flexibility, and cost efficiency. Cloud-based delivery significantly lowers upfront infrastructure costs, making compliance solutions accessible to organizations of all sizes. It also accelerates implementation timelines, enabling distributed and remote teams to access compliance tools seamlessly from any location. The SaaS model ensures automatic updates and easier integration with other enterprise systems, keeping organizations aligned with evolving regulations. As businesses increasingly operate across borders, cloud-based compliance software provides centralized visibility, real-time monitoring, and improved collaboration, making it the preferred and dominant delivery model for new buyers.

Market Dynamics

The increasing complexity of global regulatory frameworks and the growing emphasis on enterprise risk management are significant factors driving the growth of the compliance software market. Organizations across industries such as banking, healthcare, manufacturing, retail, energy, and telecommunications are facing rapidly evolving regulations related to data privacy, cybersecurity, anti-money laundering (AML), environmental, social, and governance (ESG), workplace safety, and financial reporting. As regulatory obligations expand across multiple jurisdictions, enterprises are increasingly adopting automated compliance software solutions to streamline regulatory monitoring, reduce manual workloads, improve audit readiness, and minimize the risk of financial penalties and reputational damage. Traditional spreadsheet-based and manual compliance processes are becoming inefficient and difficult to scale, thereby accelerating the adoption of integrated compliance management platforms.

In addition, several major enterprise software providers and RegTech companies are expanding investments in artificial intelligence (AI), machine learning, predictive analytics, and cloud-based compliance automation platforms to improve regulatory intelligence and operational efficiency. For instance, in December 2025, IBM expanded its AI-powered governance and compliance capabilities within its enterprise risk management portfolio to help organizations automate regulatory reporting, strengthen policy management, and enhance real-time compliance monitoring across hybrid cloud environments. Such developments highlight the increasing industry focus on intelligent automation, continuous compliance management, and digital governance transformation, thereby supporting the growth of the compliance software market.

The compliance software market faces significant challenges, including high implementation costs, complex system integration requirements, and operational difficulties associated with enterprise-wide compliance transformation initiatives. Deploying advanced compliance management platforms often requires substantial investment in software licensing, cloud infrastructure, cybersecurity frameworks, employee training, regulatory customization, and integration with existing enterprise resource planning (ERP), customer relationship management (CRM), and data management systems. For many small- and medium-sized enterprises (SMEs), the high upfront costs associated with implementing comprehensive compliance software solutions may limit adoption.

In addition, integrating compliance software into existing enterprise environments can be technically complex, particularly for organizations operating across multiple regions with varying regulatory requirements and legacy IT infrastructures. Concerns related to data privacy, interoperability challenges, regulatory updates, system customization, and user adoption further increase deployment complexity. Organizations must also address challenges related to maintaining real-time regulatory accuracy, managing cross-border compliance obligations, integrating third-party risk management frameworks, and ensuring continuous monitoring in rapidly evolving digital business environments.

Market Concentration & Characteristics

The compliance software market is moderately concentrated, with the presence of large enterprise software providers, governance, risk, and compliance (GRC) platform vendors, cybersecurity companies, and specialized regulatory technology (RegTech) providers alongside emerging AI-driven compliance automation startups. Leading companies maintain strong market positions through comprehensive compliance management platforms, broad regulatory content libraries, strategic partnerships with enterprises and regulatory bodies, cloud-based deployment capabilities, and advanced analytics and automation technologies. These players offer integrated solutions including policy and document management, audit management, risk assessment tools, regulatory reporting, third-party risk management, incident management, ESG compliance tracking, data privacy compliance, and real-time monitoring dashboards, creating competitive advantages through operational efficiency, regulatory accuracy, automation, scalability, and improved governance visibility. High barriers to entry arise from the need for deep regulatory expertise, continuous updates to evolving compliance frameworks, significant investment in secure, scalable software infrastructure, integration with enterprise systems, and stringent data security and privacy requirements across highly regulated industries.

In terms of market characteristics, the industry is highly technology-driven, with rapid innovation in artificial intelligence (AI), machine learning, robotic process automation (RPA), predictive analytics, and cloud-native compliance management platforms. Increasing regulatory complexity across industries such as banking, healthcare, manufacturing, energy, and telecommunications is a major demand driver. Organizations are facing increasing pressure to comply with evolving global regulations on data privacy, cybersecurity, anti-money laundering (AML), environmental, social, and governance (ESG), workplace safety, and financial reporting. Moreover, the market is characterized by strong emphasis on real-time compliance monitoring, automated risk mitigation, digital audit trails, workflow automation, and centralized governance frameworks. Enterprises increasingly prioritize scalable and intelligent compliance software solutions to reduce manual workloads, minimize regulatory penalties, improve operational transparency, strengthen enterprise risk management, and support digital transformation initiatives across complex business environments.

Component Insights

The software segment dominated the market and accounted for the revenue share of 74.5% in 2025. Organizations are increasingly turning to compliance software to enhance efficiency, accuracy, and transparency in their operations. These solutions help streamline critical processes such as policy management, audit reporting, and risk assessment while minimizing manual effort and the likelihood of human error. As global regulatory environments become more complex driven by frameworks such as GDPR, SOX, and ESG disclosure mandates businesses need adaptable, scalable platforms that can manage evolving compliance requirements across jurisdictions. Configurable compliance software enables real-time monitoring, automated reporting, and centralized data management, allowing organizations to maintain regulatory readiness, mitigate compliance risks, and foster accountability across departments while ensuring adherence to multiple international standards.

The services segment is anticipated to grow at the highest CAGR of 11.5% during the forecast period. The services segment in the compliance software market is expanding as organizations increasingly seek specialized expertise to manage complex and evolving regulatory requirements. Businesses depend on consulting, integration, and managed services to ensure smooth deployment, customization, and optimization of compliance solutions tailored to their operational needs. These services help bridge skill gaps, enhance regulatory alignment, and reduce implementation risks. As compliance frameworks become more dynamic, continuous support for updates, training, and system maintenance is essential. In addition, the growing adoption of cloud-based platforms and AI-driven compliance tools requires expert assistance for migration, configuration, and security assurance driving sustained demand for professional and managed compliance services.

Application Insights

The regulatory compliance segment dominated the market and accounted for the largest revenue share of 31.1% in 2025. The regulatory compliance segment is expanding quickly as organizations face increasingly complex global regulations and higher penalties for non-compliance. Stricter laws and standards such as GDPR, SOX, HIPAA, and other industry-specific regulations require businesses to adopt automated tools for monitoring, documenting, and enforcing compliance efficiently. As businesses expand globally, cross-border operations introduce additional regulatory complexity, making centralized compliance platforms essential for consistent monitoring and reporting across multiple jurisdictions. Moreover, digital transformation initiatives drive the need for scalable, real-time systems that can integrate with existing enterprise processes. By leveraging such platforms, organizations can enhance transparency, mitigate compliance risks, and maintain timely adherence to regulatory obligations while supporting growth and operational agility.

The audit & risk management segment is expected to grow at a significant CAGR during the forecast period. The Audit & Risk Management segment is expanding as organizations face heightened regulatory scrutiny and stricter corporate governance standards. Increasing operational complexity and exposure to financial, operational, and cyber risks drive the need for automated solutions. Compliance software enables businesses to streamline risk assessments, conduct internal audits, and perform continuous monitoring, reducing reliance on manual processes and minimizing human error. By providing real-time insights, predictive analytics, and centralized dashboards, these tools help organizations identify, evaluate, and mitigate risks proactively, ensuring regulatory adherence, operational efficiency, and enhanced decision-making across all business functions.

Deployment Insights

The cloud segment dominated the market and accounted for the largest revenue share in 2025. The cloud segment of the compliance software market is growing rapidly as organizations increasingly adopt cloud-based solutions for their scalability, flexibility, and cost-effectiveness. Cloud deployment eliminates the need for extensive on-premises infrastructure, reducing upfront investment and maintenance costs while providing seamless access to compliance tools from any location. This is particularly beneficial for distributed teams and organizations with remote operations, ensuring consistent monitoring and management of compliance activities across multiple sites. In addition, cloud-based platforms support faster implementation, automatic updates, and easier integration with other enterprise systems. Real-time reporting, centralized dashboards, and enhanced collaboration further drive the adoption of cloud compliance solutions across industries.

The on-premise segment is expected to grow at a significant CAGR during the forecast period. Many organizations in highly regulated sectors such as banking, healthcare, and government favor on-premises compliance software to ensure strict adherence to data privacy, residency, and security requirements. These solutions provide organizations with direct control over sensitive information and infrastructure, reducing dependence on external vendors. On-premises deployment also enables seamless integration with existing enterprise systems, legacy applications, and internal workflows, allowing customized configurations tailored to specific operational needs. By maintaining complete oversight of their compliance environment, organizations can ensure regulatory adherence, enhance data security, and support complex, industry-specific compliance processes more effectively.

Enterprise Size Insights

The large enterprises segment dominated the market and accounted for the largest revenue share in 2025. The large enterprises segment in the compliance software market is expanding rapidly as organizations face increasingly complex operations and stringent global regulatory requirements. Operating across multiple geographies, business units, and regulatory jurisdictions, large organizations require centralized and scalable compliance management systems to ensure consistent monitoring, reporting, and adherence. Compliance software enables automation of audits, risk assessments, and policy enforcement, reducing human error and improving operational efficiency. Furthermore, digital transformation initiatives, including AI and analytics integration, allow real-time risk identification and predictive insights. These capabilities help large enterprises manage financial, operational, and reputational risks effectively, maintain stakeholder trust, and ensure ongoing regulatory compliance across their global operations.

The SMEs segment is expected to grow at a significant CAGR during the forecast period. The SMEs segment in the compliance software market is expanding as small and medium-sized enterprises face growing regulatory requirements but often lack dedicated compliance teams. Cloud-based and modular SaaS solutions offer cost-effective, easy-to-deploy tools that automate policy management, reporting, and risk monitoring, making compliance more accessible. These solutions reduce upfront investment, simplify implementation, and scale with business growth. In addition, increasing awareness of data privacy, financial regulations, and industry standards drives adoption. By leveraging these tools, SMEs can maintain regulatory adherence, improve operational efficiency, and enhance credibility with clients and partners.

End-use Insights

The BFSI segment dominated the market and accounted for the largest revenue share in 2025. The BFSI segment in the compliance software market is expanding rapidly as financial institutions face stringent regulatory requirements and growing exposure to financial fraud and operational risks. Banks, insurance companies, and other financial services organizations must comply with standards such as Basel III, SOX, AML/KYC, GDPR, and various regional regulations, creating a strong demand for automated compliance solutions. Compliance software enables these organizations to streamline audits, enforce policies, monitor transactions, and detect anomalies in real time. By ensuring regulatory adherence, mitigating risks, and providing transparent reporting, these tools help BFSI companies minimize penalties, protect their reputation, and maintain stakeholder trust while supporting secure and efficient financial operations.

The healthcare segment is expected to grow at a significant CAGR during the forecast period. The healthcare segment in the compliance software market is expanding as providers face strict regulations on patient data protection, privacy, and operational standards, including HIPAA, HITECH, etc. Compliance software helps automate policy enforcement, audit trails, reporting, and risk management, reducing errors and ensuring adherence. The growing adoption of digital health records, telemedicine, and connected medical devices further increases the need for centralized, real-time monitoring and compliance oversight. These solutions enable healthcare organizations to protect sensitive patient information, maintain regulatory compliance, improve operational efficiency, and mitigate legal and financial risks.

Regional Insights

North America dominated the global market with the largest revenue share of 36.3% in 2025. North American organizations lead in adopting cloud-based, AI-driven, and analytics-enabled compliance tools to enhance efficiency, enable real-time monitoring, and strengthen risk management. The region’s rapid digital transformation, rising cybersecurity threats, and complex multi-location operations increase the demand for centralized compliance platforms. These solutions help businesses maintain regulatory adherence, streamline reporting, and proactively identify risks, driving strong growth in the compliance software market across North America.

U.S. Compliance Software Market Trends

The compliance software market in the U.S. is expected to grow significantly at a CAGR of 9.5% from 2026 to 2033. The U.S. drives the compliance software market due to strict regulatory frameworks, strong enforcement, and high digital adoption. Large enterprises, financial institutions, and healthcare providers increasingly rely on automated solutions to manage compliance efficiently. Rising cybersecurity threats and ongoing digital transformation initiatives further accelerate adoption. Compliance software enables real-time monitoring, risk management, and audit readiness, helping U.S. organizations maintain regulatory adherence, reduce operational risks, and streamline reporting across diverse industries.

Europe Compliance Software Market Trends

The compliance software market in Europe is anticipated to register considerable growth from 2026 to 2033. Europe’s compliance software market is growing rapidly due to strict regulatory frameworks, stronger enforcement, and heightened awareness of data privacy and governance. Regulations such as GDPR, MiFID II, PSD2, ISO standards, and emerging ESG reporting requirements compel organizations to adopt automated compliance solutions. These tools help businesses ensure regulatory adherence, manage risks efficiently, and maintain transparency across operations.

The UK compliance software market is expected to grow rapidly in the coming years. The UK region is experiencing growth in the compliance software market due to stringent regulatory requirements, increasing focus on data protection, and strong enforcement of financial and corporate governance laws.

The Germany compliance software market held a substantial market share in 2025. Germany’s compliance software market is growing due to strict regulations, strong enforcement, and heightened awareness of data protection and corporate governance. Regulations such as GDPR, BaFin guidelines, MiFID II, and emerging ESG reporting requirements drive organizations to adopt automated compliance solutions, ensuring regulatory adherence, risk management, and operational transparency across industries.

Asia Pacific Compliance Software Market Trends

Asia Pacific compliance software held a significant share in the global market in 2025. In The Asia Pacific region, governments and regulatory bodies in countries such as China, Japan, India, and Australia are enforcing stricter compliance requirements, including data protection, financial reporting, and ESG regulations. This drives organizations to adopt cloud-based, AI-enabled, and analytics-driven compliance platforms that automate monitoring, reporting, and risk management. These solutions help businesses ensure regulatory adherence, improve operational efficiency, manage risks proactively, and maintain transparency across industries such as banking, healthcare, and manufacturing.

The Japan compliance software market is expected to grow rapidly in the coming years. In Japan, increasing acceptance of cloud-based (SaaS) solutions is lowering barriers for compliance software adoption. Cloud platforms offer scalable, cost-effective, and easily deployable tools, enabling enterprises to automate compliance processes, improve real-time monitoring, and manage regulatory requirements efficiently without heavy upfront infrastructure investments.

The China compliance software market held a substantial market share in 2025. China’s CSL and DSL regulations mandate that critical data be stored locally, compelling multinational corporations to establish separate IT and compliance infrastructures for their operations in the country. This drives demand for localized compliance software that ensures regulatory adherence, secure data management, and efficient monitoring within China’s legal framework.

Key Compliance Software Company Insights

Key players operating in the compliance software industry are Fenergo, Ltd., Actico GmbH, ComplyAdvantage Ltd., Strike Graph, RegEd, Inc., VComply, Inc., MetricStream, Inc., SAP SE, NAVEX Global, Inc., Prophix Software Inc, and Cflow Technologies Pvt Ltd. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In October 2025, Strike Graph launched a free, guided Cybersecurity Maturity Model Certification (CMMC) Self-Assessment and Compliance Toolkit to assist U.S. Department of Defense (DoD) contractors in preparing for the upcoming Defense Federal Acquisition Regulation Supplement (DFARS) Final Rule, effective November 10, 2025. This toolkit provides contractors with the necessary resources to achieve and maintain compliance, ensuring they can continue to participate in DoD contracts.

-

In March 2025, Keensight Capital agreed to acquire a majority stake in ACTICO Group, a leading provider of digital solutions for regulatory compliance and risk management in the financial services industry. This partnership aims to accelerate ACTICO's international growth and expand its product offerings, leveraging Keensight's expertise in scaling software companies.

-

In September 2024, Oracle Corporation launched its “Financial Crime and Compliance Management Monitor Cloud Service”, aimed at banks and fintechs, enabling them to gain a unified, centralized view of compliance and risk efforts. Through advanced dashboards with interactive visuals, customizable reports and drill-downs, the service helps institutions detect potential financial crime risks faster and meet AML/ regulatory reporting requirements more effectively.

Key Compliance Software Companies:

The following key companies have been profiled for this study on the compliance software market.

- Fenergo, Ltd.

- Actico GmbH

- ComplyAdvantage Ltd.

- Strike Graph

- RegEd, Inc.

- VComply, Inc.

- MetricStream, Inc.

- SAP SE

- NAVEX Global, Inc.

- Prophix Software Inc

- Cflow Technologies Pvt Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: SAP SE; MetricStream, Inc.; NAVEX Global, Inc.; Fenergo, Ltd.

- Expanding AI-powered governance, risk, and compliance (GRC) platforms with integrated regulatory intelligence and automation capabilities.

- Investing in cloud-native compliance management, predictive analytics, cybersecurity governance, and ESG reporting solutions.

- Strengthening partnerships with cloud providers, cybersecurity firms, financial institutions, and enterprise software vendors to enhance integrated compliance ecosystems.

- Strong global enterprise presence and extensive customer base across regulated industries.

- Broad end-to-end portfolios covering policy management, audit management, AML, ESG compliance, third-party risk management, and regulatory reporting solutions.

- Strong regulatory expertise, advanced analytics capabilities, and large-scale deployment experience supporting enterprise digital governance transformation.

- High implementation, customization, and subscription costs may limit adoption among SMEs and mid-sized enterprises.

- Legacy enterprise architectures and complex integration requirements may increase deployment timelines and operational complexity.

- Large organizational structures may reduce agility in addressing niche compliance requirements and rapidly evolving regional regulations.

Emerging Players: Strike Graph; Cflow Technologies Pvt Ltd.; VComply, Inc.; Actico GmbH

- Focusing on AI-driven compliance automation, low-code workflow management, and real-time regulatory monitoring platforms.

- Developing cloud-based compliance solutions optimized for SMEs, fintech companies, and digitally transforming enterprises.

- Expanding scalable compliance management offerings supporting cybersecurity governance, ESG compliance, and third-party risk management.

- Faster innovation cycles and greater flexibility in deploying customized compliance automation solutions.

- Strong specialization in workflow automation, regulatory intelligence, and user-friendly SaaS-based compliance platforms.

- Easier adaptability to emerging regulatory frameworks, digital governance trends, and cloud-native enterprise environments.

- Limited global enterprise penetration and smaller partner ecosystems compared to established GRC vendors.

- Dependence on channel partnerships, cloud marketplaces, and external integrations for broader market expansion.

- Lower brand visibility and limited resources for supporting highly complex multinational compliance deployments.

Compliance Software Market Report Scope

Report Attribute

Details

Market size in 2025

USD 35.8 billion

Estimated market size in 2026

USD 39.26 billion

Projected market size by 2033

USD 78.85 billion

Growth rate

CAGR of 10.5% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report scope

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, application, deployment, enterprise size, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Fenergo, Ltd.; Actico GmbH; ComplyAdvantage Ltd.; Strike Graph; RegEd, Inc.; VComply, Inc.; MetricStream, Inc.; SAP SE; NAVEX Global, Inc.; Prophix Software Inc; Cflow Technologies Pvt Ltd.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Compliance Software Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global compliance software market report based on component, application, deployment, enterprise size, end-use, and region:

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Software

-

Services

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Regulatory Compliance

-

Financial Compliance

-

Data Protection & Privacy

-

Audit & Risk Management

-

Others

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud

-

On-Premise

-

-

Enterprise Size Outlook (Revenue, USD Million, 2021 - 2033)

-

Large Enterprises

-

Small and Medium Enterprises (SMEs)

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Banking, Financial Services & Insurance (BFSI)

-

Healthcare

-

Manufacturing

-

Energy & Utilities

-

IT & Telecom

-

Government

-

Aerospace & Defense

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

AI-driven compliance automation and regulatory intelligence assessment

- Analysis of AI-powered compliance automation adoption trends across banking, healthcare, manufacturing, retail, government, and enterprise sectors.

- Evaluation of regulatory monitoring, automated risk assessment, fraud detection, policy management, and real-time compliance reporting capabilities across cloud and hybrid environments.

- Identified high-growth compliance automation use cases and digital governance investment trends.

- Supported expansion strategies targeting highly regulated industries and enterprise digital transformation initiatives.

- Highlighted evolving regulatory intelligence, cybersecurity, and operational risk management requirements across organizations.

Regional regulatory landscape and compliance modernization assessment

- Analysis of evolving regulatory environments across North America, Europe, Asia-Pacific, the Middle East, and Latin America.

- Evaluation of cross-border compliance requirements, localization mandates, and digital governance initiatives influencing software adoption.

- Identified region-specific regulatory growth opportunities and compliance investment hotspots.

- Supported international expansion and localization strategies.

- Highlighted regional differences in compliance maturity and digital transformation initiatives.

Low-code/no-code compliance workflow automation assessment

- Evaluation of low-code and no-code platforms enabling customizable compliance workflows, automated approvals, and policy management processes.

- Analysis of enterprise demand for flexible compliance configuration tools, reducing IT dependency.

- Identified opportunities in citizen-developer and workflow automation ecosystems.

- Supported product innovation strategies for configurable compliance management platforms.

- Highlighted increasing enterprise focus on operational agility and rapid compliance deployment.

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The regulatory compliance segment led with a 31.1% revenue share in 2025.

The software segment led with a 74.5% revenue share in 2025, while services is the fastest-growing component.

The cloud segment dominated the market and accounted for the largest revenue share in 2025.

Large enterprises segment led the market with the largest revenue share in 2025.

North America dominated the global market with the largest revenue share of 36.3% in 2025. North American organizations lead in adopting cloud-based, AI-driven, and analytics-enabled compliance tools to enhance efficiency, enable real-time monitoring, and strengthen risk management.

The global compliance software market size was valued at USD 35.8 billion in 2025 and is estimated at USD 39.3 billion for 2026.

The global compliance software market is expected to grow at a CAGR of 10.5% from 2026 to 2033, reaching USD 78.9 billion by 2033.

Key players include Fenergo, Ltd.; Actico GmbH; ComplyAdvantage Ltd.; Strike Graph; RegEd, Inc.; VComply, Inc.; MetricStream, Inc.; SAP SE; NAVEX Global, Inc.; Prophix Software Inc; Cflow Technologies Pvt Ltd.

Increasing regulatory complexity across sectors is driving organizations to adopt compliance software for automation and scalability. New and evolving laws such as GDPR, CSRD, DORA, and financial reporting regulations demand continuous monitoring, documentation, and reporting.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.