- Home

- »

- Advanced Interior Materials

- »

-

Composites Market Size And Share Report, 2026-2033GVR Report cover

![Composites Market (2026 - 2033)Report]()

Composites Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Carbon Fiber, Glass Fiber), By Application (Automotive & Transportation, Electrical & Electronics, Wind Energy), By Manufacturing Process, By Region, And Segment Forecasts

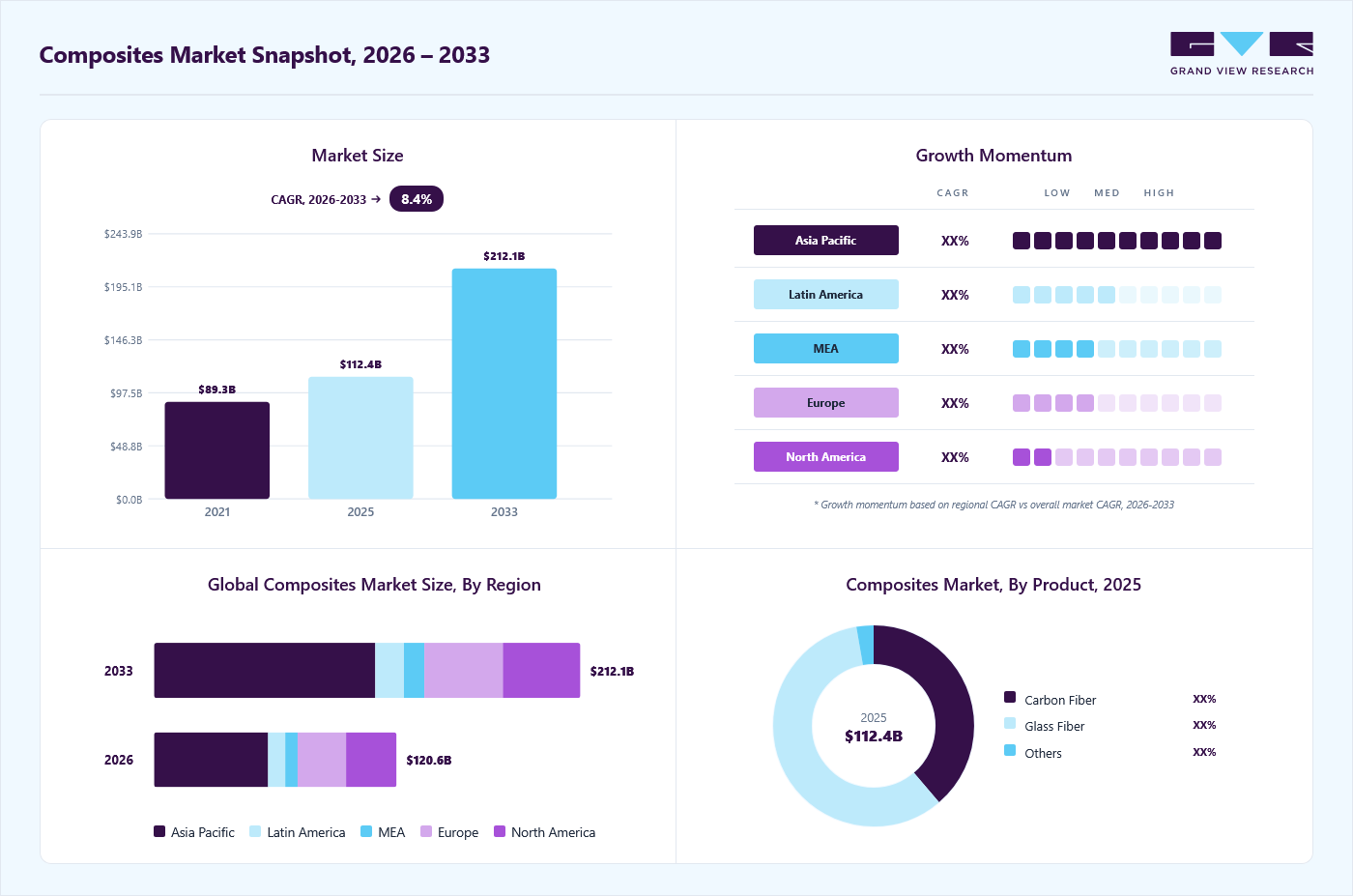

Market Size, 2025

$112.4BMarket Estimate, 2026

$120.6BMarket Forecast, 2033

$212.1BCAGR, 2026–2033

8.4%Composites Market Summary

The global composites market size was valued at USD 112.4 billion in 2025 and is projected to grow from USD 120.6 billion in 2026 to USD 212.1 billion by 2033, at a CAGR of 8.4% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 46.6% in 2025. The demand for composites is increasing steadily due to their superior strength-to-weight ratio, corrosion resistance, and durability compared to traditional materials such as steel and aluminum.

Key Market Trends & Insights

- By product: The carbon fiber segment is expected to grow at the fastest CAGR of 9.3% over the forecast period.

- By manufacturing process: The layup segment is expected to grow at the fastest CAGR of 10.1% over the forecast period.

- By application: The wind energy segment is expected to grow at the fastest CAGR of 10.1% over the forecast period.

Regional Highlights

- Largest regional market: Asia Pacific (46.6% revenue share, 2025)

- The composites industry in the China held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 112.4 Billion

- Estimated market size in 2026: USD 120.6 Billion

- Projected market size by 2033: USD 212.1 Billion

- CAGR (2026-2033): 8.4%

Industries such as aerospace, automotive, wind energy, and construction are increasingly adopting composites to improve performance and reduce overall system weight. Rising fuel-efficiency norms and emission-reduction targets are accelerating the replacement of metal components with composite materials. In infrastructure and construction, composites are being used to enhance longevity and reduce maintenance costs. The growing focus on renewable energy, especially wind turbines, further supports market growth.")

Key drivers include the growing need for lightweight materials in transportation to improve fuel efficiency and meet environmental regulations. Rapid expansion of the aerospace and defense sector is a major contributor, as composites offer high fatigue resistance and structural integrity. The automotive industry is adopting composites to reduce vehicle weight and enhance electric vehicle range. Growth in wind energy installations is driving demand for fiber-reinforced composites used in turbine blades. Advancements in manufacturing technologies, such as automated fiber placement, are improving production efficiency. Rising urbanization and infrastructure development also increase composite usage in bridges and structural applications. Cost optimization in high-volume manufacturing further supports adoption.

The market is witnessing innovations in thermoplastic composites due to their recyclability and faster processing times. Development of bio-based and natural fiber composites is gaining attention for sustainability-focused applications. Automation and digital manufacturing technologies are improving consistency and reducing production costs. Hybrid composites combining multiple fiber types are increasingly used to optimize performance and cost. Additive manufacturing of composite components is emerging as a viable approach for complex, customized parts. Smart composites with embedded sensors are being adopted in aerospace and defense applications. These trends are reshaping product development and expanding application areas.

Market Concentration & Characteristics

The composites market is moderately fragmented, with the presence of large multinational players and numerous regional manufacturers. Leading companies focus on continuous innovation, strategic partnerships, and capacity expansion to maintain competitiveness. High entry barriers exist in advanced composites due to the capital-intensive nature of manufacturing and the technical expertise required. However, local players continue to compete in glass fiber and construction-grade composites. Mergers and acquisitions are common to enhance product portfolios and geographic presence. Supplier integration and long-term contracts with aerospace and automotive OEMs strengthen market positioning. Overall, competition remains intense across product segments.

The threat of substitutes is moderate in the industry, primarily from lightweight metals such as aluminum alloys, magnesium, and advanced steel. These materials offer cost advantages and established manufacturing ecosystems. However, composites outperform their substitutes in terms of corrosion resistance, fatigue strength, and design flexibility. Material substitution depends heavily on cost sensitivity and performance requirements of the application. Recycling challenges and higher initial costs can hinder the adoption of composites in certain industries. Continuous material innovation is reducing this substitution risk over time. As sustainability improves, composites are expected to maintain a competitive edge.

Product Insights

The glass fiber segment held the largest revenue market share of 58.5% in 2025, primarily due to its cost efficiency and versatility across a wide range of end-use industries. Glass fiber composites offer good mechanical strength, chemical resistance, and electrical insulation properties, making them suitable for construction, automotive, marine, pipes, tanks, and electrical applications. Their relatively low raw material and processing costs support large-scale production and widespread adoption. The established global supply chain for glass fibers ensures consistent availability and stable pricing. In addition, growing infrastructure development and increasing use of glass fiber in wind turbine blades further strengthen the segment’s dominant revenue position.

The carbon fiber segment is expected to grow at a significant CAGR of 9.3% over the forecast period, due to rising demand for high-performance and lightweight materials. Carbon fiber composites provide exceptional strength, stiffness, and fatigue resistance, which is driving their adoption in aerospace, defense, and high-end automotive applications. The shift toward electric vehicles is a key growth driver, as manufacturers seek lightweight solutions to extend driving range. Technological advancements in precursor materials and manufacturing processes are gradually reducing production costs. Expanding applications in wind energy, pressure vessels, and industrial equipment further support rapid market growth.

Manufacturing Process Insights

The layup segment held the largest revenue market share of 36.7% in 2025, owing to its simplicity, design flexibility, and cost-effective production. Hand layup and spray layup processes are widely used for manufacturing large and complex composite structures. These methods are particularly suitable for marine, construction, and transportation applications with moderate production volumes. Low tooling investment and ease of customization make layup processes attractive for small and mid-sized manufacturers. The ability to produce thick and high-strength components also contributes to sustained demand. Despite slower production speeds, the broad applicability of layup techniques supports strong revenue generation.

The compression molding segment is expected to grow at a significant CAGR of 8.3% over the forecast period, due to its ability to support high-volume, automated composite production. The process offers improved dimensional accuracy, reduced cycle times, and lower material wastage compared to traditional methods. Compression molding is increasingly used in automotive and industrial applications that require consistent quality and scalability. The growing adoption of thermoplastic composites aligns well with compression molding technology. Enhanced surface finish and structural performance further increase its attractiveness. As manufacturers prioritize efficiency and cost reduction, the adoption of compression molding continues to rise.

Application Insights

The automotive & transportation segment held the largest revenue market share of 21.0% in 2025, driven by strict emission norms and the need for lightweight vehicle components. Composites are increasingly used in exterior panels, chassis components, and interior structures to reduce the overall weight of vehicles. Rising electric vehicle production has amplified demand for advanced composites to improve battery efficiency and driving range. Mass transit systems, railways, and commercial vehicles also contribute to strong demand. OEMs are investing in composite-intensive vehicle designs to meet performance and sustainability goals. These factors collectively sustain the segment’s leading market share.

The wind energy segment is expected to grow at a significant CAGR of 10.1% over the forecast period, supported by accelerating global investments in renewable energy. Composites are essential in wind turbine blade manufacturing due to their high strength, fatigue resistance, and lightweight characteristics. Increasing turbine sizes require advanced composite materials to maintain structural integrity and efficiency. Government incentives and renewable energy targets are driving the growth of wind power installations worldwide. Technological advancements in blade design, including longer and more aerodynamic blades, are increasing the consumption of composites per turbine. As wind capacity expansion continues, demand for composites in this segment is set to grow rapidly.

Regional Insights

The composites industry in the Asia Pacific dominated the global market and accounted for the largest revenue share of 46.6% in 2025, due to rapid industrialization and large-scale manufacturing activities. Strong growth in the automotive, construction, and wind energy sectors supports high demand. China, Japan, South Korea, and India are major contributors to regional consumption. Cost-effective labor and the availability of raw materials attract global composite manufacturers. Government investments in infrastructure and renewable energy further strengthen regional growth. Aerospace manufacturing expansion in the region also contributes to market dominance. The region is expected to maintain its leading position over the forecast period.

TheChinadominated the Asia Pacific composites Market with a revenue share of 50.1% in 2025. Chinaindustry is the largest in the Asia Pacific, driven by wind energy, construction, and transportation sectors. Massive investments in renewable energy projects boost demand for fiber-reinforced composites. The automotive industry is increasingly using composites to meet fuel-efficiency standards. Government support for advanced material manufacturing accelerates domestic production capabilities. Expansion of aerospace manufacturing further strengthens demand. Local manufacturers are improving quality and scale to compete globally. Sustainability-focused composite innovation is also gaining traction.

Europe Composites Market Trends

The composites industry in Europe is a significant market due to strong automotive and aerospace manufacturing bases. Emission reduction regulations encourage the adoption of lightweight composites. Wind energy projects across the region drive demand for glass and carbon fiber composites. Automotive OEMs increasingly integrate composites into structural components. Focus on recyclable and bio-based composites aligns with sustainability goals. Advanced research institutions support material innovation. Europe maintains steady growth while leading in technology.

The Germany composites industry leads the regional landscape due to its strong automotive and engineering sectors. High-performance composites are widely used in premium and electric vehicles. Aerospace component manufacturing supports demand for carbon fiber. Industrial automation enhances composite production efficiency. Sustainability and recycling initiatives influence material selection. R&D investments foster advanced composite applications. Germany remains a key innovation hub in the market.

North America Composites Market Trends

The composites industry in North America is a technologically advanced market with strong demand from the aerospace, defense, and automotive industries. The presence of major aircraft manufacturers drives high adoption of carbon fiber composites. Wind energy installations continue to support demand for composite blades. Investments in lightweight materials for electric vehicles further enhance market growth. Advanced R&D capabilities strengthen innovation in high-performance composites. Government defense spending supports consistent demand. Recycling and sustainability initiatives are influencing product development.

U.S. Composites Market Trends

The U.S. composites industry is driven by aerospace, defense, and renewable energy applications. Strong demand for carbon fiber composites is supported by aircraft modernization programs. Automotive manufacturers use composites to reduce vehicle weight and improve efficiency. The expansion of wind energy increases demand for large composite structures. Advanced manufacturing technologies improve production efficiency. High R&D spending supports innovation and material advancements. The U.S. remains a key exporter of advanced composite solutions.

Central & South America Composites Market Trends

The composites industry in Central & South America is an emerging market driven by construction, wind energy, and transportation. Brazil leads regional demand due to renewable energy projects and infrastructure development. Cost-effective glass fiber composites dominate the market. Growing automotive production supports gradual composite adoption. Industrial expansion improves the regional demand outlook. Limited high-end manufacturing slightly restricts advanced composite growth. The region offers long-term growth potential.

Middle East & Africa Composites Market Trends

The composites industry in the Middle East & Africa is growing due to infrastructure development and renewable energy investments. Wind and solar projects increase demand for structural composites. Construction and oil & gas applications drive usage of corrosion-resistant materials. Government diversification initiatives support industrial development. Aerospace maintenance and defense spending contribute to demand. Adoption remains higher for glass fiber composites due to cost considerations. The region is expected to witness steady growth over time.

Key Composites Company Insights

Some of the key players operating in the market include Compagnie de Saint-Gobain S.A. and PPG Industries, Inc., among others.

-

Compagnie de Saint-Gobain S.A. is a global leader in construction materials and high-performance solutions, with strong expertise in advanced composites and engineered materials. The company serves a diverse range of end-use industries, including construction, automotive, industrial manufacturing, and energy. Its composites portfolio focuses on lightweight, durable, and sustainable material solutions. Saint-Gobain emphasizes innovation, energy efficiency, and decarbonization across its product offerings.

-

PPG Industries, Inc. is a major supplier of paints, coatings, and specialty materials, with a growing presence in composite resins and protective solutions. The company supports composite applications across aerospace, automotive, marine, and industrial sectors. PPG focuses on enhancing material performance, corrosion resistance, and durability. Continuous product innovation and strong customer relationships underpin its position in the composites value chain.

DuPont and SGL Group are some of the emerging market participants in the composites market.

-

DuPont is a global science and innovation leader offering advanced materials used extensively in high-performance composite applications. The company provides engineered polymers, fibers, and resins that enhance strength, thermal resistance, and durability. DuPont’s materials are widely used in aerospace, automotive, electronics, and industrial markets. Strong R&D capabilities and sustainability-driven innovation define its market presence.

-

SGL Group is a leading manufacturer of carbon-based materials and solutions, specializing in carbon fibers and carbon fiber-reinforced composites. The company primarily serves aerospace, automotive, wind energy, and industrial markets. SGL Group focuses on lightweight construction and high-performance structural applications. Its advanced manufacturing capabilities and technical expertise support its strong position in the global composites market.

Key Composites Companies:

The following key companies have been profiled for this study on the composites market.

- Teijin Ltd.

- Owens Corning

- DuPont

- PPG Industries, Inc.

- Toray Industries, Inc.

- Huntsman Corporation LLC

- SGL Group

- Hexcel Corporation

- Compagnie de Saint-Gobain S.A.

- Weyerhaeuser Company

- Momentive Performance Materials, Inc.

- Cytec Industries (Solvay, S.A.)

- China Jushi Co., Ltd.

- Kineco Limited

- Veplas Group

Recent Developments

-

In September 2024, Teijin announced the expansion of its glass fiber prepreg production capacity at its Thailand facility to strengthen its market position.

Composites Market Report Scope

Report Attribute

Details

Market size in 2025

USD 112.4 billion

Estimated market size in 2026

USD 120.6 billion

Projected market size by 2033

USD 212.1 billion

Growth Rate

CAGR of 8.4% from 2026 to 2033

Base year for estimation

2025

Actual estimates/Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, manufacturing process, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East and Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; Italy; France; Spain; China; Japan; India; South Korea; Brazil; Argentina

Key companies profiled

Teijin Ltd.; Owens Corning; DuPont; PPG Industries, Inc.; Toray Industries, Inc.; Huntsman Corporation LLC; SGL Group; Hexcel Corporation; Compagnie de Saint-Gobain S.A.; Weyerhaeuser Company; Momentive Performance Materials, Inc.; Cytec Industries (Solvay, S.A.); China Jushi Co., Ltd.; Kineco Limited; Veplas Group

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Composites Market Report Segmentation

This report forecasts revenue growth at the global, regional & country levels and provides an analysis on the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global composites market report on the basis of product, application, manufacturing process, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Billion; 2021 - 2033)

-

Carbon Fiber

-

Glass Fiber

-

Others

-

-

Manufacturing Process Outlook (Volume, Kilotons; Revenue, USD Billion; 2021 - 2033)

-

Layup

-

Filament

-

Injection Molding

-

Pultrusion

-

Compression Molding

-

RTM

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Billion; 2021 - 2033)

-

Automotive & Transportation

-

Wind Energy

-

Electrical & Electronics

-

Construction & Infrastructure

-

Pipes & Tanks

-

Marine

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Billion; 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

Italy

-

UK

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Frequently Asked Questions About This Report

The global composites market size was estimated at USD 112.4 billion in 2025 and is expected to reach USD 120.6 billion in 2026.

The glass fiber segment held the highest revenue market share of 58.5% in 2025, primarily due to its cost efficiency and versatility across a wide range of end-use industries.

Some of the key players operating in the composites market include Teijin Ltd., Owens Corning, DuPont, PPG Industries, Inc., Toray Industries, Inc., Huntsman Corporation LLC, SGL Group, Hexcel Corporation, and Compagnie de Saint-Gobain S.A., Weyerhaeuser Company, Momentive Performance Materials, Inc., Cytec Industries (Solvay, S.A.), China Jushi Co., Ltd., Kineco Limited, Veplas Group

The rising demand for lightweight, high-strength materials across the automotive, aerospace, renewable energy, and construction industries to improve performance, fuel efficiency, and sustainability is the key factor driving the composites market.

Layup held the largest revenue share 36.7% in 2025.

Automotive & transportation held the largest share (over 21.0%) in 2025 and online retail is the fastest-growing market.

Asia Pacific dominated with a 46.6% revenue share in 2025.

The global composites market is expected to grow at a compound annual growth rate of 8.4% from 2026 to 2033 to reach USD 212.1 billion by 2033.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.