- Home

- »

- Medical Devices

- »

-

Compression Therapy Market Size, Share Report, 2026-2033GVR Report cover

![Compression Therapy Market (2026 - 2033)Report]()

Compression Therapy Market (2026 - 2033)

Size, Share & Trends Analysis Report By Technology (Static Compression Therapy, Dynamic Compression Therapy), By End-use (Hospitals, Specialty Clinics), By Distribution Channel, By Region, And Segment Forecasts

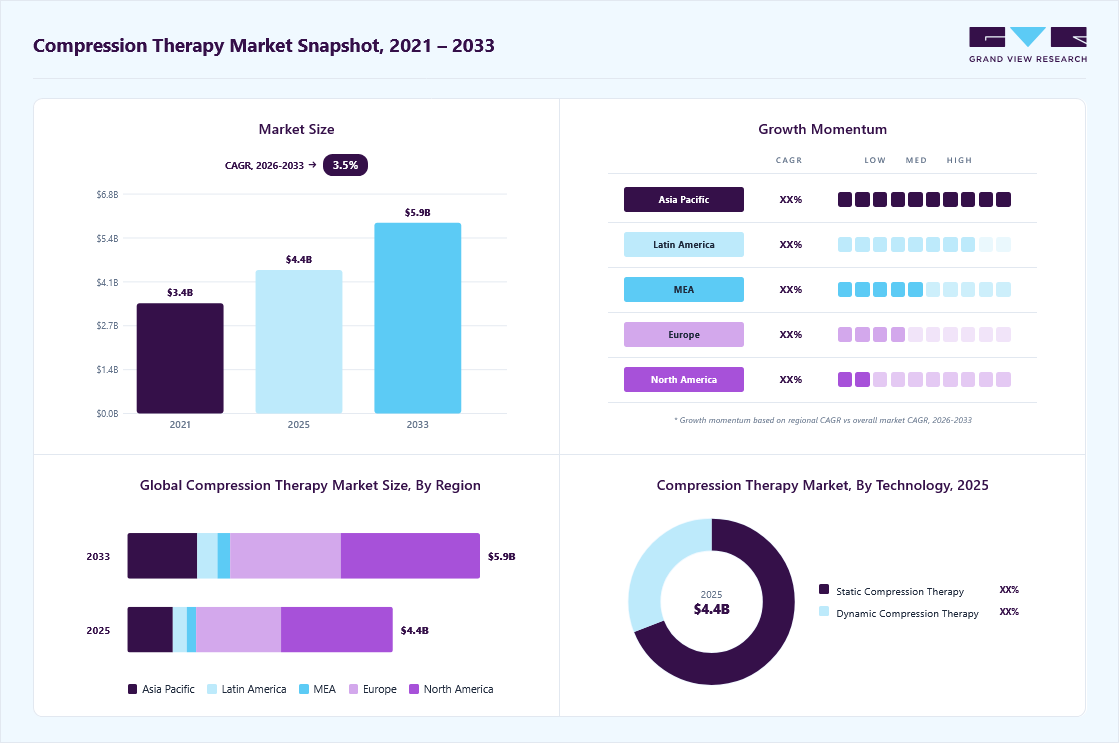

Market Size, 2025

$4.4BMarket Estimate, 2026

$4.6BMarket Forecast, 2033

$5.9BCAGR, 2026–2033

3.5%Compression Therapy Market Summary

The global compression therapy market size was valued at USD 4.4 billion in 2025 and is projected to grow from USD 4.6 billion in 2026 to reach USD 5.9 billion by 2033, growing at a CAGR of 3.5% from 2026 to 2033. North America held the largest global revenue share of 42.1% in 2025. The compression therapy industry’s growth is driven by the rising prevalence of venous and lymphatic disorders, including deep vein thrombosis (DVT), varicose veins, lymphedema, and chronic venous insufficiency.

Key Market Trends & Insights

- By technology: Static compression therapy held the largest revenue share in 2025.

- By distribution channel: Institutional sales held the largest revenue share in 2025.

- By end use: Hospitals held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (42.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (fastest CAGR, 2026-2033)

- By country: The U.S. held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 4.4 Billion

- Estimated market size in 2026: USD 4.6 Billion

- Projected market size by 2033: USD 5.9 Billion

- CAGR (2026-2033): 3.5%

Compression therapy, which applies controlled pressure to improve blood circulation and reduce swelling, has become an essential solution for both prevention and treatment of these conditions. Growth is further fueled by the increasing burden of chronic diseases such as obesity, diabetes, and cardiovascular conditions, along with a rapidly aging global population that is more susceptible to circulatory disorders. In addition, the rising number of surgical procedures and sports-related injuries is boosting demand for compression therapy in post-operative care and rehabilitation.

The rising prevalence of deep vein thrombosis is significantly driving the compression therapy market growth, as the condition requires effective prevention and management strategies to reduce complications. DVT, which involves the formation of blood clots in deep veins primarily in the legs, is becoming more common due to factors such as sedentary lifestyles, increasing obesity rates, an aging population, and a higher number of surgical procedures. Compression therapy, including stockings and pneumatic devices, is widely recommended to improve blood circulation, prevent clot formation, and reduce the risk of post-thrombotic complications.

")

According to the Centers for Disease Control and Prevention (CDC) data from 2025, up to 900,000 people in the U.S. are affected by venous thromboembolism (VTE) each year, highlighting the significant burden of this condition on the healthcare system.

Conditions such as chronic venous insufficiency and venous ulcers impact many people worldwide, with factors such as aging populations, inactive lifestyles, and obesity playing a major role. Compression therapy for venous ulcers is highly effective; therefore, the rising prevalence of venous ulcers will drive market growth. Moreover, compression therapy for varicose veins is highly effective compared to other options. For instance, data from the Society for Vascular Surgery indicate that as many as 40 million Americans have varicose veins. Moreover, according to an article published by NCBI, around 150,000 new cases of chronic venous insufficiency are diagnosed each year, with approximately USD 500 million spent on the care of these patients.

Compression therapy works by applying controlled pressure to the affected limbs, helping ease symptoms, enhance blood flow, reduce swelling, and aid healing, while preventing complications. Thus, the growing awareness of compression therapy's effectiveness in managing chronic venous conditions is expected to drive market growth.

The growing number of orthopedic procedures is driving an increased need for compression therapy as part of postoperative care and rehabilitation protocols. Orthopedic surgeries, including joint replacements (such as knee or hip replacements), fracture repairs, ligament reconstructions, and arthroscopic surgeries, are becoming more common due to an aging population, sports-related injuries, and advancements in surgical techniques. For instance, according to data from the American College of Rheumatology, the number of knee and hip replacements performed annually in the U.S. is on the rise due to the aging population, with approximately 790,000 knee replacements and 544,000 hip replacements performed each year. According to data published by the Australian Orthopedic Association National Joint Replacement Registry (AOANJRR) in 2024, more than 2.1 million orthopedic procedures were performed in Australia.

After an orthopedic procedure, patients commonly experience swelling, inflammation, and reduced mobility in the operated limbs. Compression therapy plays a vital role in managing these postoperative symptoms and in providing recovery by improving blood circulation, reducing swelling, and supporting the surgical site.

The increasing cases of obesity have led to an increase in the adoption of compression therapy as a crucial device in managing health-related concerns. Obesity, characterized by excessive body fat accumulation, not only increases the risk of chronic disorders such as CVD, diabetes, & hypertension but also contributes to venous insufficiency and associated disorders. For instance, an article published in the International Journal of Medical Science and Clinical Invention suggests that obesity increases the risk of venous insufficiency and associated complications by more than sixfold. As per the World Obesity Federation, in 2024, more than one billion people worldwide were living with obesity, which is about one in eight people. This includes nearly 880 million adults, and 159 million children and adolescents aged 5-19. The World Obesity Federation’s 2025 Atlas, published on World Obesity Day (4 March), projects that the total number of adults living with obesity will increase by more than 115% between 2010 and 2030, from 524 million to 1.13 billion.

The table below indicates the Prevalence of Obesity in the U.S. based on Self-Reported Weight and Height by State and Territory, Behavioral Risk Factor Surveillance System BRFSS, 2024

State

Prevalence (%)

95% CI

District of Columbia

25.5

(23.5, 27.5)

Colorado

25

(24.0, 26.0)

Hawaii

27

(25.4, 28.6)

Massachusetts

27

(25.8, 28.2)

New Jersey

27.7

(26.3, 29.0)

Vermont

29

(27.5, 30.5)

California

29.1

(27.6, 30.5)

Florida

29.6

(28.1, 31.3)

New York

29.5

(28.8, 30.2)

New Hampshire

31.1

(29.3, 32.9)

Rhode Island

31.1

(29.3, 32.9)

Montana

31

(29.5, 32.4)

Utah

31

(29.9, 32.1)

Connecticut

32

(30.4, 33.6)

Washington

31.5

(30.7, 32.2)

Virginia

32.3

(30.7, 34.0)

Wyoming

32.5

(30.7, 34.3)

Virgin Islands

37.7

(30.7, 45.3)

Idaho

32.7

(30.8, 34.7)

Nevada

34.2

(31.3, 37.3)

Minnesota

32.3

(31.4, 33.3)

Arizona

33.3

(31.4, 35.3)

Maryland

32.7

(31.5, 33.8)

Alaska

34

(32.0, 36.0)

Pennsylvania

34.2

(32.0, 36.5)

Source: CDC

Obesity can worsen venous insufficiency by increasing venous pressure, especially in the lower limbs. The additional weight places strain on the venous system, hindering blood flow back to the heart and leading to venous congestion, swelling, and discomfort. Over time, this chronic venous insufficiency can progress to more serious conditions such as varicose veins, venous ulcers, and DVT. Thus, this factor is expected to surge demand for compression therapy, driving the growth of the compression therapy industry.

Market Dynamics

The increasing prevalence of chronic venous disorders, including chronic venous insufficiency (CVI), varicose veins, deep vein thrombosis (DVT), and venous leg ulcers, is a key driver of the compression therapy market. Factors such as sedentary lifestyles, obesity, aging populations, and prolonged periods of standing or sitting at work are significantly contributing to the growing global burden of these conditions. According to data published by the Society for Vascular Surgery in July 2025, chronic venous insufficiency affects up to 40% of Americans. Similarly, data from WebMD LLC published in July 2025 indicate that in the U.S., more than 11 million men and 22 million women aged 40-80 years suffer from varicose veins, while over 2 million individuals are affected by advanced CVI. Each year, more than 20,000 people are diagnosed with ulcers resulting from CVI.

The growing availability of alternative treatment methods is restraining the adoption of traditional compression therapy products. Minimally invasive procedures such as endovenous laser therapy (EVLT), radiofrequency ablation (RFA), foam sclerotherapy, and vein stenting are preferred for the treatment of chronic venous disease due to faster recovery, long-term symptom relief, and improved patient convenience. In June 2025, the Society for Cardiovascular Angiography & Interventions published updated chronic venous disease guidelines highlighting ablation therapy, sclerotherapy, and venous interventions alongside conservative compression approaches, reflecting the growing clinical acceptance of alternative treatments. Furthermore, in December 2025, a study published on ResearchGate highlighted the growing adoption of minimally invasive procedures and novel pharmacological therapies for chronic venous insufficiency, which are improving patient outcomes and reducing dependence on conventional compression therapy as a standalone treatment approach.

Market Concentration & Characteristics

The compression therapy market’s growth stage is moderate, and the pace of growth is accelerating. Key characteristics include strong demand driven by the rising prevalence of chronic venous disorders and an aging population, along with increasing preference for non-invasive treatment options. In addition, the market is innovation-oriented, with continuous advancements in materials, product design, and digital integration aimed at improving patient comfort, compliance, and therapeutic outcomes. Strategic expansion into home care settings, coupled with growing awareness and reimbursement support in developed regions, further shapes the market's competitive and operational dynamics.

The market is characterized by strong, evolving innovation driven by the need to enhance clinical outcomes and improve patient experience. Advancements center on the development of smart compression systems that deliver adjustable, personalized pressure and integrate digital features, such as Bluetooth connectivity and mobile applications, for real-time monitoring and therapy tracking. Innovations in materials and product design, including lightweight, breathable, and ergonomically designed garments, are improving comfort and patient adherence, especially for long-term use. For instance, Hyperice launched Hyperice X 2 Knee and X 2 Shoulder devices, which feature integrated compression alongside heat and cold therapy. These devices provide multi-modal treatment in a single wearable system, improving circulation and accelerating recovery for musculoskeletal conditions. In addition, the introduction of portable and user-friendly pneumatic compression devices is supporting the shift toward home-based care, making treatment more accessible and convenient. While the fundamental concept of compression therapy remains consistent, ongoing technological advancements are significantly transforming product capabilities and market dynamics.

Compression therapy products are medical devices subject to strict regulatory standards. Regulatory bodies, such as the U.S. FDA in the U.S. or CE (Conformité Européene) marking in Europe, set guidelines and standards to ensure the safety, effectiveness, and quality of these devices. Innovation in compression therapy product design, materials, and features often requires regulatory approvals. Manufacturers must navigate the regulatory landscape to ensure new and improved products meet the required standards. For instance, in 2026, AIROS Medical, a medical technology manufacturer specializing in compression therapy systems for peripheral vascular disorders, announced the launch of its U.S. Food and Drug Administration (FDA)- cleared 510(k) ARTAIRA® arterial compression device. Regulatory bodies set quality and safety standards for medical equipment, including compression therapy. Compliance with these standards is essential for manufacturers to ensure patient safety during transportation. In addition, regulations may require manufacturers to adopt eco-friendly practices in the production and disposal of compression therapy products.

Mergers and acquisitions are driving the growth of the compression therapy industry by enabling companies to expand their technological capabilities, product offerings, and geographic presence. Through strategic acquisitions, companies gain access to advanced compression technologies and innovative product lines, which enhance their ability to meet evolving patient needs and improve treatment outcomes. These activities also strengthen distribution networks and allow faster entry into emerging markets, increasing overall market penetration. In addition, consolidation through mergers creates stronger entities with greater financial and research resources, accelerating product development and commercialization. As a result, rising M&A activity is contributing to increased competition, innovation, and overall market expansion.

In February 2026, Tactile Medical announced the acquisition of LymphaTech to expand the breadth and depth of its lymphedema solutions portfolio. The acquisition, valued at an upfront payment of USD 6.8 million with additional milestone-based considerations, strengthens Tactile Medical’s position in lymphatic disease management.

Regional Expansion

Product expansion in the global market involves introducing new products or enhancing existing ones to meet evolving patient needs, technological advancements, and market demands. Companies can introduce new product lines to target specific market segments. This might include developing compression garments for different anatomical areas, such as the arms, legs, and torso, as well as for specific conditions, such as lymphedema or venous insufficiency.

The compression therapy market exhibits elements of both fragmentation and consolidation, with the degree varying by product type, geographic region, and market segment. In certain segments of the market, particularly in regions with a wide range of manufacturers and suppliers, the market can be fragmented. This fragmentation may be due to the presence of numerous small- and medium-sized companies offering a range of compression therapy products, including compression garments, bandages, stockings, and devices. These companies often compete based on factors such as price, product differentiation, and distribution channels. Conversely, the market is characterized by consolidation, particularly in segments dominated by a few large companies with significant market share. These companies may have established brand recognition, extensive distribution networks, and diverse product portfolios encompassing a range of compression therapy solutions.

The market is influenced by various factors, including advancements in healthcare infrastructure, the rising prevalence of chronic diseases, and technological innovations in compression therapy, such as improved designs that enhance patient comfort & compliance. Regional expansion scenarios in the market are driven by factors such as an aging population, the rising prevalence of chronic diseases, increased awareness of venous disorders, and the overall development of healthcare infrastructure.

Technology Insights

The static compression therapy segment led the compression therapy industry, accounting for the largest revenue share in 2025. Static compression therapy involves applying consistent pressure to affected areas to increase blood flow and reduce swelling. This method utilizes compression garments such as stockings, bandages, or wraps, known for their ease and effectiveness in treating conditions like varicose veins, Deep Vein Thrombosis (DVT), and lymphedema. The therapy is favored for its ease of use and convenience, making it a preferred choice for both patients and physicians. It offers effective pressure & pain relief, rapid functional recovery, and reduced swelling, which are crucial for treating various sports injuries & conditions. Static compression devices are versatile, suitable for various medical conditions, and offer various levels of compression. They are relatively more affordable than dynamic compression devices, making them a cost-effective option for patients and healthcare providers, especially in regions with limited healthcare budgets.

The dynamic compression therapy segment is expected to register the fastest growth during the forecast period. This therapy is gaining traction in the market, driven by several key factors and trends. This therapy involves applying pressure to the affected area, gradually adjusting it to promote blood flow and reduce swelling. The therapy products include dynamic compression pumps. Dynamic compression therapy offers a flexible approach, allowing pressure levels to be adjusted based on patient needs, unlike static compression therapy, which applies constant pressure. This flexibility makes it effective for treating various conditions, including postsurgical wounds and injury pains.

End-use Insights

The hospitals segment accounted for the largest revenue share of the compression therapy industry in 2025. Hospitals are preferred over other healthcare facilities due to their capability to provide comprehensive care to patients with complex medical needs. Hospitals have the necessary infrastructure, medical expertise, and resources to effectively manage & monitor patients' conditions, ensuring optimal treatment outcomes. In addition, they offer immediate access to advanced medical care in the event of complications or emergencies. Compression therapy products are widely used in hospitals for the treatment of various medical conditions, including venous disorders, lymphedema, and postsurgical recovery. The use of these products in hospitals has increased due to their proven efficacy in managing conditions, reducing complications, and improving patient outcomes.

The home healthcare segment is expected to grow at the fastest CAGR over the forecast period. Compression therapy at home healthcare is utilized for the management of conditions such as varicose veins, DVT, lymphedema, orthostatic hypotension, sports injuries, and leg ulcers. Home-based healthcare and patient self-management strategies have increased demand for user-friendly, wearable compression therapy devices. These devices are designed to be easy to use at home, allowing patients to manage their conditions without frequent visits to healthcare facilities. Integrating compression therapy consultations, fitting services, and patient education into telemedicine platforms further enhances access to care and supports remote patient monitoring initiatives.

Distribution Channel Insights

The institutional sales segment accounted for the largest revenue share of the compression therapy market in 2025. Institutional sales in the global market involve distributing products through channels such as hospitals, clinics, & nursing homes and offer several advantages over retail sales. These advantages include selling products in larger quantities, reduced marketing costs, and the potential to establish long-term business relationships with key institutional customers. The dominance of institutional sales in the market is driven by increasing demand for these products in healthcare settings. As the global population ages, there is a growing need for compression therapy solutions to treat conditions such as chronic venous insufficiency, lymphedema, and DVT. Institutional sales offer an effective and dependable way to deliver these products to healthcare providers who require them.

The retail sales segment is expected to grow at the fastest CAGR during the forecast period. Retail sales in the market encompass the distribution of products through channels such as pharmacies, medical supply stores, and online retailers. Retail sales offer greater accessibility to compression therapy products, providing a wide range of options and allowing consumers to compare & select the best products for their needs. In addition, retail sales offer convenience, enabling consumers to purchase products directly without a prescription or a visit to a healthcare provider. Hence, rising benefits associated with retail sales are anticipated to boost the segment growth.

Regional Insights

North America dominated the compression therapy market with a 42.1% revenue share in 2025, driven by technological advancements, the rising prevalence of chronic diseases, and government initiatives. The market's expansion is further bolstered by advancements in compression therapy technology, such as the development of innovative materials and improved designs that enhance patient comfort & compliance. The increasing prevalence of chronic diseases such as diabetes and obesity, which often lead to circulatory issues, significantly contributes to market growth. For instance, chronic venous insufficiency (CVI), a condition commonly associated with varicose veins, is highly prevalent. Approximately one in four U.S. adults has CVI. When spider veins are also considered, the prevalence of venous disorders rises to nearly eight in 10 adults.

U.S. Compression Therapy Market Trends

The U.S. compression therapy industry is growing, driven by the increasing prevalence of venous and lymphatic disorders such as Varicose Veins, deep vein thrombosis (DVT), and chronic venous insufficiency. The rising prevalence of varicose veins is a major driver, as they affect a significant portion of the adult population due to factors such as sedentary lifestyles, prolonged standing or sitting, obesity, and aging. For instance, more than 40 million people in the U.S. suffer from varicose veins. Almost 50% of patients with varicose veins have a family history of varicose veins. If both parents have varicose veins, your chances of developing the disease are close to 90%. These conditions lead to symptoms like leg pain, swelling, and visible vein enlargement, prompting patients to seek effective and non-invasive treatment options such as compression therapy. Increasing awareness and early diagnosis of varicose veins are further accelerating the adoption of compression stockings and bandages for both prevention and long-term management. Rising healthcare awareness, increasing preference for preventive care, and the integration of compression therapy in post-surgical recovery and rehabilitation are strengthening market growth.

Europe Compression Therapy Market Trends

The compression therapy industry in Europe is expected to grow at a significant CAGR over the forecast period. This growth can be attributed to the rising geriatric population and growing advancements in the market. Moreover, the region's advanced healthcare infrastructure, coupled with a focus on minimally invasive medical interventions, fosters the adoption of compression therapy products.

The UK compression therapy market is expected to grow at a moderate CAGR over the forecast period.The aging population in the UK, prone to venous ulcers, foot ulcers, and edema, necessitates the use of compression therapy to prevent recurrence & manage symptoms. The high incidence of DVT, affecting 1 to 2 out of every 1,000 people annually, which increases with age, underscores the importance of compression therapy in DVT management. Compression therapy, including compression hosiery, bandaging, or other devices, plays a critical role in DVT management. According to data published by the National Library of Medicine in 2025, hospitalizations for VTE increased by 62.6% between 1998 and 2022, from 109.5 to 178.1 per 100,000 population. This was driven by a 202% increase in hospitalizations for PE (from 40.4 to 122.2 per 100,000 population).

The compression therapy market in France is expected to grow at the fastest CAGR over the forecast period, driven by the rising geriatric population and the increasing prevalence of CVDs in the region. The country’s aging population is contributing to a higher incidence of venous and lymphatic disorders such as varicose veins, lymphedema, and deep vein thrombosis, thereby increasing the demand for compression-based treatments. In 2024, a study published by the National Library of Medicine reported that the number of venous thromboembolism cases among adults in France reached 896,846 on 1 January 2023. VTE was the primary diagnosis during a hospital stay or in a medical unit for 62,055 patients hospitalized in 2022. The age-standardized rate of hospitalized patients was 23.0% higher among men than among women. In addition, rising cases of obesity and sedentary lifestyles are further driving the need for effective, non-invasive therapeutic solutions. France’s well-established healthcare system, which reimburses the cost of compression garments and devices, enhances patients' access to and adoption of these treatments.

Asia Pacific Compression Therapy Market Trends

The Asia Pacific compression therapy industry is expected to grow at the fastest CAGR over the forecast period. The market has been experiencing significant growth, driven by several key factors, including the increasing prevalence of chronic diseases, including venous disorders, lymphedema, and DVT, among the region's population. Moreover, the rising geriatric population, coupled with the growing awareness about the benefits of compression therapy in managing such conditions, has further fueled market expansion. Technological advancements, such as innovative compression garment designs & materials, have enhanced patient comfort and compliance, boosting market demand.

China's compression therapy market is experiencing growth, supported by a rapidly aging population and a rising burden of chronic diseases. The country has a large elderly demographic, which significantly increases the prevalence of conditions such as chronic venous insufficiency, lymphedema, and varicose veins, all of which require compression-based treatment. In addition, supportive government healthcare initiatives and ongoing improvements in healthcare infrastructure are playing a crucial role in strengthening the market, positioning China as a key growth region for compression therapy. For instance, a major factor supporting market expansion is the Healthy China 2030 strategy, introduced by the Chinese government to strengthen the national healthcare system and improve disease prevention, diagnosis, and treatment services. The policy focuses on improving healthcare access, expanding medical coverage, strengthening disease prevention programs, and promoting advanced medical technologies to enhance healthcare outcomes.

The India compression therapy market is growing, driven strongly by the rising prevalence of chronic diseases, particularly diabetes, which is significantly contributing to vascular complications. The increasing number of diabetic patients in the country is leading to a higher incidence of conditions such as poor blood circulation, diabetic foot ulcers, and chronic venous insufficiency, all of which require compression therapy as part of effective management and recovery. As per the International Diabetes Federation, India's diabetes cases in adults are 89,826,900 in 2024, and the prevalence of diabetes is 10.5%. As diabetes continues to rise due to sedentary lifestyles, unhealthy dietary habits, and urbanization, the demand for compression garments, stockings, and bandages is also increasing steadily. In addition, the growing burden of Deep Vein Thrombosis (DVT) is further supporting market expansion, as prolonged sitting, long travel, obesity, and rising surgical procedures increase the risk of clot formation. Improved awareness and early diagnosis are encouraging the use of compression therapy for both prevention and post-treatment care.

Latin America Compression Therapy Market Trends

The Latin America market is growing in the compression therapy sector, driven by the rising incidence of Deep Vein Thrombosis (DVT) across the region. Increasing cases of DVT are largely associated with sedentary lifestyles, higher obesity rates, prolonged immobility, and a growing number of surgeries and hospital admissions, all of which elevate the risk of blood clot formation. In addition, long-distance travel and limited early-stage diagnosis in certain areas are contributing to the expanding patient pool. According to a 2025 study by the National Library of Medicine, a total of 700,315 admissions for venous thromboembolism were documented in the Brazilian public health system between 2008 and 2022, representing 3.02 admissions per 10,000 inhabitants per year. The Southeast region accounted for more than half (54.5%) of the hospitalizations.

As awareness of DVT and its complications improves, there is a greater emphasis on preventive care and post-treatment management, leading to higher adoption of compression therapy products such as stockings and bandages. Furthermore, the aging population in countries like Brazil and Argentina is accelerating demand, as elderly individuals are more vulnerable to venous disorders. The market is also supported by rising healthcare expenditure, improved healthcare infrastructure, and greater awareness among healthcare professionals and patients about effective treatment options.

Middle East and Africa Compression Therapy Market Trends

The Middle East and Africa compression therapy industry is expected to grow at a significant CAGR during the forecast period, driven by increasing investments in healthcare infrastructure and the rising prevalence of chronic diseases. Advancements in the healthcare system are expected to boost the development of the medical device industry in this region. Growing health insurance penetration, increasing privatization, and rising regional disease burden are factors expected to drive regional market growth.

The Saudi Arabia compression therapy market is expected to grow at the fastest CAGR over the forecast period. In Saudi Arabia, the prevalence of CVI is significantly high, with 45.6% of the adult population affected, especially in the Western region. This high prevalence, higher than in Western countries, is linked to lifestyle factors and risk factors such as age, family history, prolonged standing occupation, and use of hormonal therapy. This scenario presents a competitive market for CVI treatment products and services, emphasizing the need for innovative solutions & targeted interventions to address the prevalent risk factors.

Here are several key advancements in compression garments

-

Modern compression garments use breathable fabrics, moisture-wicking technology, and antimicrobial and hypoallergenic materials to improve comfort, reduce skin irritation, and prevent bacterial growth, while also reducing the risk of allergies and skin irritation

-

Advanced knitting techniques enable varying compression levels within a garment, enhancing blood circulation by being strongest at the extremities and decreasing towards the core

-

Advancements in body scanning and 3D printing technology enable personalized compression garments, providing optimal comfort and minimal waste, while 3D knitting technology enhances comfort and sustainability

-

Modern compression garments use embedded sensors to monitor physiological parameters, enabling real-time performance optimization and health monitoring. Integration with mobile apps allows users to track progress, adjust training or treatment, and share information

-

Compression garments offer fashionable options in various colors, patterns, and styles, and are designed for specific user groups like pregnant women, athletes, or patients recovering from specific surgeries

-

Modern compression garments are enhanced by durable fabrics and easy care routines, making them resistant to wear and tear, deformation, and loss of compression

A patient-centric approach to compression therapy: the use and adoption of a novel mobile application to support the clinical selection of medical compression hosiery

Compression therapy is widely recognized as an effective treatment option for the management of lower limb conditions; however, clinicians do not always apply it appropriately. A lack of knowledge and clinical uncertainty, combined with increased workload and less time with patients, might lead to inappropriate decisions about compression.

A research article published in wound.uk in November 2023 studied the use of the Hosiery Hunter app (Medi UK) and its role in clinical decision-making. The Hosiery Hunter app is a new mobile app that simplifies the selection of medical compression hosiery for patients with lower-limb conditions. According to qualitative data from a user feedback survey, the Hosiery Hunter app made it easier to choose the most suitable compression therapy, saved time, and provided swift, timely access to prescription codes.

Clinical Results and Studies

-

Tactile Medical has invested in several research studies that generate clinical and economic outcome data to support its product and demonstrate its effectiveness.To date, more than 25 studies on the safety and efficacy of the firm’s products have been completed, involving more than 2,100 subjects. A few of them studying the efficacy of the Flexitouch System are listed below:

-

Economic Impact of Tactile Medical’s Flexitouch System in Patients with Phlebolymphedema

-

Impact on Clinical Outcomes and Healthcare Costs with Use of Flexitouch System

-

Flexitouch System Impact on Limb Volume and Patient-Reported Outcome

-

Comparison of Flexitouch System with Simple Pneumatic Compression Devices

-

Study of Patient-Reported Satisfaction with Use of Flexitouch System

-

Flexitouch System Impact on Patient-Reported Improved Quality-of-Life

Shifts Towards E-commerce

Digitalization transforms the way the company markets and sells products, solutions, and services, and builds relationships with consumers, patients, and caregivers. Essity's focus on digital channels reflects a broader industry trend of investing in e-commerce to cater to evolving consumer needs and behaviors.

Essity has expanded its distribution channels from offline to digital in recent years. Digital interactions with customers and consumers help understand their needs and improve communication and engagement. For instance, Medtronic has its Connect E-Store, an e-commerce platform designed to streamline order management for healthcare professionals and organizations. This platform enhances convenience by enabling easy access to essential medical products, simplifying procurement processes, and reducing ordering time through its user-friendly interface and advanced digital features. By improving accessibility and efficiency in purchasing medical supplies, such digital platforms support faster adoption of products like compression therapy devices, thereby contributing to the market growth.

Key Compression Therapy Company Insights

Cardinal Health; Julius Zorn GmbH; Hartmann AG; Medi GmbH & Co.; SIGVARIS; BSN Medical GmbH; ArjoHuntleigh; 3M Health Care; Spectrum Healthcare; Bio Compression Systems, Inc.; and Stryker are some of the major global players. The market has been witnessing notable trends that are impacting the activities of emerging players in the industry. These companies offer a wide range of compression garments, stockings, wraps, and devices for various medical conditions, including venous disorders, lymphedema, and wound healing. There is also a growing number of emerging players and startups entering the market, offering innovative solutions and disrupting traditional market dynamics. These companies often focus on niche segments or develop novel technologies to address unmet needs in wound care management and vascular health.

Moreover, advancements in compression therapy technologies have led to the development of innovative products and treatment modalities. Some notable advancements include smart compression technology, 3D printing, gradient compression systems, cold compression therapy, and hydrotherapy compression devices. In addition, companies in the global market are focusing on developing patient-centric solutions that prioritize comfort, convenience, and usability.

Key Compression Therapy Companies

The following key companies have been profiled for this study of the compression therapy market.

-

Essity Aktiebolag (publ).

-

Cardinal Health

-

Julius Zorn GmbH

-

Hartmann AG

-

Medi GmbH & Co.

-

SIGVARIS

-

ArjoHuntleigh

-

3M (Solventum)

-

Spectrum Healthcare

-

Bio Compression Systems, Inc.

-

Stryker

-

Gottfried Medical

-

Tactile Medical

-

URGO MEDICAL

-

Medline Industries, LP.

-

Smith+Nephew

-

Mölnlycke Health Care AB

-

L&R Group

-

AIROS Medical, Inc.

-

Lympha Press

-

L WELL MEDTECH SOLUTIONS SDN. BHD.

-

Ofa Bamberg GmbH

-

Zimmer Biomet

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Essity Aktiebolag (publ)

- Mature companies diversify and upgrade their product lines to meet a broader range of patient needs, such as introducing premium flat-knit custom garments, smart/connected hosiery, and advanced dynamic compression pumps.

- To grow beyond saturated home markets, mature firms pursue mergers, acquisitions, and partnerships to enter new regional markets or adjacent segments.

- Extensive Product Portfolio: Offering a broad range of compression products: flat-knit, circular-knit, multi-layer bandages, hosiery, and dynamic compression devices.

- Covering all therapy classes (Class 1-4) and custom-made options to meet diverse patient needs.

- Strong Brand Recognition & Clinical Credibility: A well-established reputation fosters trust among healthcare providers, patients, and distributors.

- Clinical validation of products supports adoption and compliance.

- Many mature players offer similar product features (e.g., compression levels, materials), making it challenging to differentiate purely on product attributes.

- Established supply chains and legacy manufacturing setups can result in higher fixed costs.

Emerging Players: AIROS Medical, Inc.

- Focus on advanced materials (breathable fabrics, lightweight fibers, antimicrobial properties) to improve patient comfort and adherence.

- Focus on specialized compression hosiery for chronic conditions like lymphedema or venous insufficiency, where patient-specific customization is valued.

- Innovation & Differentiation: Emerging players can quickly introduce advanced materials, smart compression devices, and patient-focused designs, offering solutions that combine medical efficacy with comfort and style.

- Targeting underserved segments like home healthcare, post-surgical recovery, or pediatric compression helps build strong brand loyalty and specialized market presence.

- Emerging players often struggle with low brand awareness compared to established incumbents, making it harder to gain trust from patients and healthcare providers.

- Emerging players may face limitations in funding, R&D, and production capacity, restricting large-scale expansion and innovation.

Recent Developments

-

In September 2025, AIROS Medical announced the expansion of its trunkal compression garment line to improve inclusivity for patients suffering from lymphedema. The newly introduced garments feature extended sizing options, enabling a broader range of patients with abdominal and pelvic swelling to access pneumatic compression therapy to manage edema and pain effectively.

-

In October 2025, WRS Group announced that it had entered into a definitive agreement with Avanos Medical to acquire many assets and rights associated with the Game Ready orthopedic rental business in the U.S. The acquisition, effective from December 2025, strengthens WRS Group’s portfolio of orthopedic pain management and recovery solutions.

-

In February 2025, Tactile Medical announced the expanded launch of its next-generation pneumatic compression platform, Nimbl, to include patients with lower extremity lymphedema across the U.S. This expansion builds on the product’s initial introduction in October 2024, which was primarily focused on treating upper extremity lymphedema.

-

In November 2024, Cardinal Health launched the Kendall SCD SmartFlow Compression System, an advanced medical device designed to enhance venous thromboembolism prevention in hospitalized patients. The system provides sequential compression therapy, which helps reduce the risk of deep vein thrombosis and pulmonary embolism.

-

In November 2024, Scottish scientists from the University of Edinburgh developed a low-cost, flexible device to prevent blood clots. This represents a significant advancement in post-surgical care, particularly for patients at risk of developing conditions like Deep Vein Thrombosis (DVT). The device, a polymer-based sensor, fits under bandages and compression stockings and uses a handheld reader to measure whether the bandage is applying the correct pressure to the body.

-

In October 2024, Tactile Medical launched the next-generation Nimbl Pneumatic Compression Platform, designed to enhance lymphedema management. This chronic condition results in swelling in the arms or legs due to a blockage in the lymphatic system. This innovative platform offers an advanced solution for patients with lymphedema, providing a more comfortable, effective, and improved form of treatment.

Compression Therapy Market Report Scope

Report Attribute

Details

Market size in 2025

USD 4.4 billion

Estimated market size in 2026

USD 4.6 billion

Projected market size by 2033

USD 5.9 billion

Growth rate

CAGR of 3.5% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, trends, and volume analysis

Segments covered

Technology, end-use, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; UK; Germany; Italy; France; Spain; Denmark; Sweden; Norway; Japan; China; India; South Korea; Australia; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Essity Aktiebolag (publ); Cardinal Health; Julius Zorn GmbH; Hartmann AG; Medi GmbH & Co.; SIGVARIS; ArjoHuntleigh; 3M (Solventum); Spectrum Healthcare; Bio Compression Systems, Inc.; Stryker; Gottfried Medical; Tactile Medical; URGO MEDICAL; Medline Industries, LP.; Smith+Nephew; Mölnlycke Health Care AB; L&R Group; AIROS Medical, Inc.; Lympha Press; L WELL MEDTECH SOLUTIONS SDN. BHD.; Ofa Bamberg GmbH; Zimmer Biomet

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to the country & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Compression Therapy Market Report Segmentation

This report forecasts revenue growth at the global, regional & country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global compression therapy market report based on technology, end-use, distribution channel, and region:

-

Technology Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Static Compression Therapy

-

Compression Bandages

-

Indication & Pathology

-

Venous Leg Ulcers

-

Mixed Leg Ulcers

-

Post-operative Edema

-

Deep Vein Thrombosis (DVT)

-

Lymphedema - used in decongestive therapy

-

-

Compression Class

-

Class 1

-

Class 2

-

Class 3

-

Class 4

-

-

-

Compression Stockings & Hosiery

-

Medical-grade Stockings

-

Indications / Use Cases

-

Varicose Veins

-

Deep Vein Thrombosis (DVT) Prevention

-

Lymphedema

-

Chronic Venous Insufficiency

-

Post-surgical Recovery

-

Other Medical Conditions

-

-

Compression Class

-

Class 1

-

Class 2

-

Class 3

-

Class 4

-

-

-

Socks and Tights

-

Indications / Use Cases

-

Everyday Wear & Comfort

-

Travel & Long-haul Use

-

Sports & Athletic Recovery

-

Others

-

-

Compression Class

-

Class 1

-

Class 2

-

Class 3

-

Class 4

-

Class 5

-

-

-

Custom-fit Hosiery

-

Indications / Use Cases

-

Lymphedema

-

Chronic Venous Insufficiency

-

Post-surgical Recovery

-

Severe Varicose Veins

-

Other Therapeutic Uses

-

-

Compression Class

-

Class 1

-

Class 2

-

Class 3

-

Class 4

-

-

-

-

Compression Tape

-

Indication & Pathology

-

Sports Injuries

-

Post-operative Edema

-

Lymphedema

-

-

Compression Class

-

Class 1

-

Class 2

-

-

-

Adjustable Compression Wraps (Leg/Calf)

-

Indications & Pathology

-

Venous Leg Ulcers (VLU)

-

Lymphedema

-

Deep Vein Thrombosis (DVT)

-

Chronic Venous Insufficiency

-

Post-operative Edema

-

Pregnancy-related Edema

-

-

Compression Class

-

Class 1

-

Class 2

-

Class 3

-

Class 4

-

Class 5

-

Class 6

-

-

-

Dynamic Compression Therapy

-

Compression Pumps

-

Compression Sleeves

-

By Indication & Pathology

-

Lymphedema

-

Sports Recovery

-

Post-operative Edema

-

CVI Prevention

-

-

Compression Class

-

Class 1

-

Class 2

-

Class 3 and 4

-

-

-

-

End-use Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Hospitals

-

Specialty Clinics

-

Home Healthcare

-

Physician’s Office

-

Nursing Homes

-

Others

-

-

Distribution Channel Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Institutional Sales

-

Retail Sales

-

-

Regional Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global compression therapy market size was valued at USD 4.4 billion in 2025 and is estimated at USD 4.6 billion for 2026.

Key factors that are driving the market growth include the increasing prevalence of venous disorders, rising significance in the treatment of sports injuries and a significant increase in orthopedic surgeries across the world.

The global compression therapy market is expected to grow at a CAGR of 3.5% from 2026 to 2033, reaching USD 5.9 billion by 2033.

North America dominated the compression therapy market with the largest revenue share of 42.1% in 2025. This is attributable to favorable government reimbursement plans, the high incidence of chronic venous disorders, and the growing healthcare awareness level.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include Essity Aktiebolag (publ); Cardinal Health; Julius Zorn GmbH; Hartmann AG; Medi GmbH & Co.; SIGVARIS; ArjoHuntleigh; 3M; Spectrum Healthcare; Bio Compression Systems, Inc.; Stryker; Gottfried Medical; Tactile Medical.

The institutional sales segment held the largest revenue share (over 60.0%) in 2025, while retail sales is the fastest-growing channel.

The static compression therapy segment led the market with the largest revenue share of 69.0% in 2025, while dynamic compression therapy is the fastest-growing technology.

The hospitals segment led the market with the largest revenue share of 33.1% in 2025, while home healthcare is the fastest-growing segment.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.