- Home

- »

- Biotechnology

- »

-

Continuous Bioprocessing Market Size, Industry Report 2030GVR Report cover

![Continuous Bioprocessing Market Size, Share & Trends Report]()

Continuous Bioprocessing Market (2025 - 2030) Size, Share & Trends Analysis Report By Product (Instruments, Consumables & Reagents), By Application (Monoclonal Antibodies, Vaccines), By End Use, By Region, And Segment Forecasts

Market Size, 2024

$349.3MMarket Estimate, 2026

$387.9MMarket Forecast, 2030

$911.4MCAGR, 2025–2030

18.6%Continuous Bioprocessing Market Summary

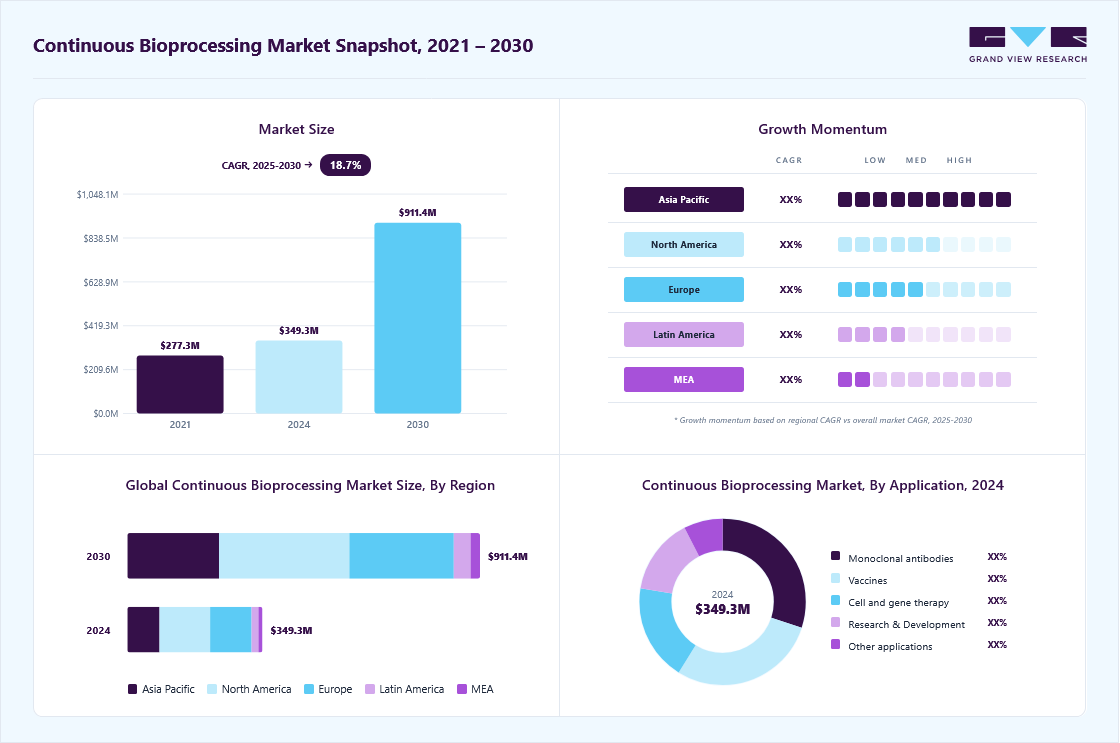

The global continuous bioprocessing market size was estimated at USD 349.3 million in 2024 and is projected to reach USD 911.4 million by 2030, growing at a CAGR of 18.63% from 2025 to 2030. The industry is driven by the growing demand for cost-efficient and scalable biopharmaceutical production, particularly for monoclonal antibodies, vaccines, and cell & gene therapies.

Key Market Trends & Insights

- In terms of region, North America was the largest revenue generating market in 2024.

- Country-wise, India is expected to register the highest CAGR from 2025 to 2030.

- In terms of segment, consumables and reagents accounted for a revenue of USD 214.6 million in 2024.

- Consumables and Reagents is the most lucrative product segment registering the fastest growth during the forecast period.

Market Size & Forecast

- 2024 Market Size: USD 349.3 Million

- 2030 Projected Market Size: USD 911.4 Million

- CAGR (2025-2030): 18.63%

- North America: Largest market in 2024

Process intensification, enabled by automation, real-time monitoring, and single-use technologies, is enhancing productivity and reducing operational costs. Regulatory agencies, including the FDA and EMA, are encouraging the adoption of continuous manufacturing due to its improved process control and product consistency.

")

The industry forecast indicates significant growth, driven by increasing adoption of advanced biomanufacturing technologies, rising demand for biologics, and ongoing investments in automation and process optimization. Furthermore, continuous bioprocessing enables higher productivity, reduced costs, and better product consistency, making it a preferred choice for pharmaceutical and biotech companies. Additionally, the growing prevalence of chronic diseases such as cancer, autoimmune disorders, and infectious diseases has intensified the need for faster and more cost-effective biologic drug production, further accelerating market growth.

Another major driver is the technological advancements in bioprocessing equipment and automation. The integration of real-time process monitoring, single-use bioreactors, perfusion systems, and advanced analytics has significantly improved the feasibility of continuous bioprocessing. Companies are investing in digital biomanufacturing solutions, artificial intelligence, and machine learning to optimize process control, ensuring higher yields and product quality. Moreover, regulatory agencies, including the FDA and EMA, are encouraging the adoption of continuous bioprocessing by providing guidelines and support for implementation, reducing barriers for companies looking to transition from batch to continuous operations.

The shift toward cost-efficient and sustainable manufacturing practices is also propelling the continuous bioprocessing market. Traditional batch processing generates significant waste and requires large production facilities, leading to high capital and operational expenses. Continuous bioprocessing minimizes resource consumption, reduces waste, and enhances overall process efficiency, making it an attractive option for companies seeking sustainable manufacturing solutions. Additionally, the biopharmaceutical industry's growing focus on decentralized manufacturing and flexible production capabilities, especially in response to global healthcare demands and pandemic preparedness, has further driven the adoption of continuous bioprocessing technologies.

Growing Demand for Biologics & Biosimilars

The growing demand for biologics and biosimilars is a major driver of the continuous bioprocessing market, as pharmaceutical and biotechnology companies seek higher efficiency, cost-effectiveness, and scalability in production. With rising global demand for monoclonal antibodies (mAbs), gene therapies, and recombinant proteins, companies are increasingly shifting from traditional batch processing to continuous bioprocessing to improve yields, reduce production time, and ensure consistent product quality. For instance, Boehringer Ingelheim has integrated continuous bioprocessing in its large-scale biologics manufacturing to enhance efficiency, while Samsung Biologics has expanded its single-use and perfusion-based bioprocessing capabilities to support biosimilar production. Similarly, Amgen has leveraged continuous manufacturing for next-gen biologics, aiming to reduce costs and enhance process control. As more companies invest in intensified bioprocessing strategies, the adoption of continuous bioprocessing is expected to accelerate, particularly in the biosimilar and novel biologics segments.

Technological Advancements in Bioprocessing Systems

Technological advancements and single-use systems are key drivers of the continuous bioprocessing market, enabling greater flexibility, reduced contamination risks, and cost savings. Innovations in perfusion bioreactors, real-time Process Analytical Technology (PAT), and automated control systems are making continuous processing more efficient and scalable. Merck KGaA has developed Mobius single-use bioreactors to support continuous perfusion processes, reducing downtime and improving operational efficiency. Cytiva (formerly GE Healthcare) has expanded its FlexFactory platform, integrating single-use filtration, chromatography, and bioreactors for seamless continuous biomanufacturing. Additionally, Thermo Fisher Scientific has invested in single-use systems for intensified upstream and downstream processing, allowing faster batch turnover and lower capital investment. As companies increasingly adopt disposable, modular, and automated solutions, the continuous bioprocessing industry is set to expand, particularly in biologics and biosimilars manufacturing.

For instance, in January 2024, Merck announced that its Life Science business sector has signed a non-binding Memorandum of Understanding (MoU) with Mycenax Biotech to explore potential collaboration in delivering innovative, high-capacity bioprocessing solutions to Taiwan and international markets. The agreement focuses on integrating Merck’s BioContinuum Platform across the entire bioprocessing spectrum for Mycenax’s customers, with plans to incorporate automation and digitalization into production workflows. This partnership aims to drive process intensification, support the transition to BioProcessing 4.0, and advance continuous bioprocessing technologies.

Market Concentration & Characteristics

Innovations in the industry are driven by the adoption of automation, real-time monitoring, AI-driven process optimization, and single-use technologies. Companies are focusing on hybrid bioprocessing systems, continuous chromatography, and perfusion-based bioreactors to improve process efficiency, reduce production costs, and enhance product yields. Sartorius and Thermo Fisher are investing heavily in digital bioprocessing solutions to enable predictive analytics and smarter manufacturing workflows. Additionally, advances in cell culture media, biosensors, and process intensification strategies are further transforming the market, enabling faster and more scalable biologics production.

Strategic partnerships and collaborations are central to the industry's growth, as biopharmaceutical companies, CDMOs, and equipment manufacturers work together to drive continuous bioprocessing adoption. Companies like Merck KGaA and Cytiva frequently collaborate with biotech firms and academic institutions to develop cutting-edge solutions. Additionally, alliances between tech firms and biomanufacturers, such as Danaher’s partnerships in AI-powered process control, are improving real-time monitoring and automation. Mergers and acquisitions, such as Thermo Fisher’s acquisition of Brammer Bio, further indicate an industry-wide trend of consolidation to strengthen capabilities in continuous manufacturing.

Regulatory frameworks significantly influence the adoption of continuous bioprocessing, with agencies like the FDA, EMA, and ICH setting stringent guidelines for process validation, quality assurance, and Good Manufacturing Practices (GMP). While regulatory bodies encourage continuous manufacturing due to its efficiency, consistency, and scalability, challenges remain in harmonizing standards across regions. The FDA’s Emerging Technology Program (ETP) and initiatives by the European Medicines Agency (EMA) are fostering regulatory support for innovation, making it easier for companies to transition from batch to continuous processing. However, compliance with evolving analytical and process control requirements adds complexity for new entrants.

Companies are expanding their product portfolios by introducing next-generation continuous bioreactors, perfusion systems, single-use solutions, and process analytical technologies (PATs) to enhance efficiency and scalability. Thermo Fisher and Sartorius have launched integrated hybrid systems that allow seamless transition between batch and continuous processing. Additionally, product expansions are focusing on customized solutions for monoclonal antibodies, gene therapy, and biosimilar production. The increasing demand for scalable, modular, and automated solutions is also driving companies to innovate across upstream and downstream processing stages.

North America and Europe currently dominate the market due to advanced biopharmaceutical infrastructure, early regulatory approvals, and strong investment in bioprocessing R&D. However, companies are aggressively expanding in Asia-Pacific and Latin America, driven by the growing biosimilar industry, increasing demand for affordable biologics, and government initiatives supporting biopharma manufacturing. China and India, in particular, are witnessing rapid growth, with domestic firms adopting continuous processing technologies to enhance bioproduction capabilities. Companies like Cytiva and Merck KGaA are establishing manufacturing and research centers in emerging markets to cater to the increasing demand for continuous bioprocessing solutions.

Product Insights

Based on products, the consumables & reagents segment dominated the market with the largest revenue share in 2024. The increasing adoption of single-use technologies (SUTs), advancements in cell culture media, and the need for high-purity reagents to support uninterrupted bioproduction. The shift from traditional batch processing to continuous bioprocessing has led to a growing demand for single-use bioreactors, perfusion media, chromatography resins, filters, and biosensors, which enhance process efficiency and reduce contamination risks.

The instruments segment is expected to grow at a significant CAGR from 2025 to 2030. the increasing demand for automated, scalable, and high-efficiency bioprocessing solutions to enhance biologics production. The shift toward perfusion-based bioreactors, continuous chromatography systems, and real-time monitoring tools is fueling innovation, allowing manufacturers to achieve higher yields, reduced process variability, and improved cost efficiency.

Application Insights

The monoclonal antibodies segment dominated the market, with the largest revenue share of 29.98% in 2024. The increasing global demand for biological therapies, particularly for treating cancer, autoimmune diseases, and infectious diseases. Continuous bioprocessing enhances process efficiency, scalability, and cost-effectiveness, making it ideal for high-volume mAb production. Companies like Sartorius, Cytiva, and Thermo Fisher Scientific are investing in perfusion bioreactors, continuous chromatography, and real-time monitoring systems to optimize yield and maintain consistent product quality. Additionally, the shift towards biosimilars and regulatory support for process intensification further fuel adoption, as manufacturers seek to reduce production costs while maintaining high product purity and potency.

The vaccine segment is expected to grow at the fastest CAGR from 2025 to 2030. The vaccines segment is witnessing strong growth in continuous bioprocessing due to the need for rapid, scalable, and cost-effective production, particularly after the COVID-19 pandemic. Continuous manufacturing allows for higher yields, shorter production cycles, and increased flexibility, which is crucial for mRNA, viral vector, and recombinant protein-based vaccines.

End Use Insights

The pharmaceutical and biotechnology companies segment dominated the market, with the largest revenue share of 48.43% in 2024.The increasing demand for efficient, high-yield, and cost-effective biologics production. With the rise of monoclonal antibodies, biosimilars, cell & gene therapies, and next-generation vaccines, biopharma firms are shifting from traditional batch processing to continuous manufacturing to enhance productivity and scalability. Companies like Thermo Fisher Scientific, Cytiva (Danaher), and Sartorius are providing automated perfusion bioreactors, continuous chromatography, and process analytical technology (PAT) to optimize real-time monitoring and control.

")

The CMOs & CROs segment is expected to witness the fastest CAGR during the forecast period. CMOs & CROs are rapidly adopting continuous bioprocessing technologies to meet the growing demand for outsourced biopharmaceutical development and production. As biopharma companies focus on cost reduction and faster time-to-market, CMOs are investing in single-use, modular, and automated continuous processing systems to improve efficiency and flexibility. Leading CMOs like Lonza, WuXi Biologics, and Samsung Biologics are expanding their continuous manufacturing capabilities to handle high-throughput production of biologics, biosimilars, and gene therapies. Additionally, CROs are leveraging advanced bioprocessing technologies for early-stage research, process development, and clinical-scale manufacturing, driving overall market growth in the continuous bioprocessing space.

The continuous bioprocessing industry is dominated by key players such as Danaher, Sartorius AG, Thermo Fisher Scientific Inc., and others. These companies drive market growth through innovations in continuous bioreactors, perfusion systems, chromatography solutions, and single-use technologies, catering to the rising demand for efficient biologics production. Danaher, Sartorius, and Thermo Fisher lead with integrated continuous bioprocessing solutions. Merck KGaA and Agilent provide consumables and analytical tools for process monitoring, enhancing scalability and efficiency. Strategic acquisitions, collaborations, and technological advancements continue to shape the competitive landscape, making continuous bioprocessing a key driver in biopharmaceutical manufacturing.

The heat map analysis evaluates five key companies including, Danaher, Sartorius AG, Thermo Fisher Scientific Inc., WuXi Biologics, and Merck KGaA, based on their product portfolio, strategic initiatives, and geographic presence in the continuous bioprocessing market.

Danaher, Thermo Fisher, and Merck KGaA exhibit strong capabilities across all three parameters, with consistently high scores. Their comprehensive product portfolios, global reach, and active strategic initiatives position them as leading players in continuous bioprocessing. Sartorius AG also scores highly, particularly in product portfolio and geographic presence, indicating its strong foothold in the market. WuXi Biologics stands out in strategic initiatives but has relatively lower scores in product portfolio compared to other global giants. This suggests that while the company is actively expanding in continuous bioprocessing, it may still be building a more diversified product offering.

Regional Insights

North America continuous bioprocessing market dominated the global industry with the largest revenue share of 37.46% in 2024. The market is driven by strong investments in biopharmaceutical R&D, advanced manufacturing infrastructure, and supportive regulatory policies. Leading players like Thermo Fisher Scientific, Cytiva (Danaher), and Sartorius are heavily investing in next-generation bioprocessing technologies to support the production of biologics, biosimilars, and cell & gene therapies. Additionally, government initiatives, such as funding from the Biomedical Advanced Research and Development Authority (BARDA) and the growing adoption of single-use technologies, are fueling market expansion.

U.S. Continuous Bioprocessing Market Trends

The continuous bioprocessing industry in the U.S. is growing due to the presence of leading biopharma companies, extensive R&D investments, and regulatory support from the FDA for continuous manufacturing. The demand for personalized medicine, mAbs, and gene therapies is driving biopharmaceutical firms to adopt high-efficiency bioprocessing solutions, including automated perfusion bioreactors and real-time monitoring systems. Companies like Amgen, Lonza, and WuXi Biologics are expanding their continuous manufacturing capabilities, further boosting market growth.

Asia Pacific Continuous Bioprocessing Market Trends

The continuous bioprocessing industry in Asia Pacific is driven by rising biopharmaceutical investments, increasing biosimilar production, and expanding biomanufacturing hubs in countries like China, Japan, India, and South Korea. Governments are supporting local biologics production through favorable policies and funding initiatives, while global biopharma companies are partnering with regional CMOs and CROs to expand their presence. Continuous bioprocessing adoption is further accelerated by advancements in single-use bioreactors, continuous purification, and PAT technologies.

China continuous bioprocessing industry is expanding due to strong government support for biopharmaceutical innovation, local biotech startups, and increasing foreign investments. The "Made in China 2025" initiative promotes local biologics manufacturing, encouraging companies like WuXi Biologics and Innovent Biologics to adopt continuous manufacturing technologies. The demand for biosimilars, monoclonal antibodies, and cell & gene therapies is also driving bioprocessing innovations, supported by large-scale biomanufacturing facilities and regulatory advancements.

The continuous bioprocessing industry in Japan is driven by its aging population, rising demand for biologics, and strong regulatory framework that supports process intensification. Leading pharmaceutical companies like Takeda and Astellas are investing in continuous biomanufacturing technologies to improve efficiency and reduce costs. The Japanese government is promoting bioprocessing innovation through funding initiatives, while CMOs like CMIC Group are expanding their continuous manufacturing capabilities to serve both domestic and global markets.

Europe Continuous Bioprocessing Market Trends

The continuous bioprocessing market in Europe is driven by stringent regulatory requirements, strong investments in biotech R&D, and leading biopharma companies like Roche, Novartis, and Sanofi. The European Medicines Agency (EMA) supports continuous manufacturing initiatives, leading to increased adoption of single-use technologies, continuous chromatography, and real-time process monitoring. Additionally, the region's focus on biosimilars and personalized medicine is accelerating the adoption of continuous bioprocessing across biopharma companies and CMOs.

The UK continuous bioprocessing market is growing due to government funding for advanced biomanufacturing and strong partnerships between academia and industry. Organizations like the Cell and Gene Therapy Catapult are supporting the development of next-generation bioprocessing solutions, while major biopharma firms and CMOs are investing in continuous bioreactor systems and AI-driven process analytics. The demand for biosimilars, gene therapies, and COVID-19-related vaccines is further driving market expansion.

The bioprocessing industry in Germany leads the European market with strong biotech R&D investments, a highly skilled workforce, and key players like Merck KGaA and Sartorius pioneering continuous bioprocessing technologies. The country’s focus on biomanufacturing innovation, regulatory compliance, and process automation is driving demand for continuous chromatography, perfusion bioreactors, and PAT-enabled systems. Additionally, Germany's high biosimilar adoption rates and the presence of leading CMOs make it a crucial market for continuous bioprocessing growth.

Latin America Continuous Bioprocessing Market Trends

The continuous bioprocessing industry in Latin America is expanding due to growing biopharmaceutical production, increasing investments in biosimilars, and government support for local biomanufacturing. Countries like Brazil, Argentina, and Mexico are investing in advanced biologics production, while global companies are forming regional partnerships with local CMOs to establish continuous manufacturing capabilities. The demand for cost-effective biologics and vaccines is further propelling market growth in the region.

Brazil is a major player in Latin America’s biopharmaceutical market, with increasing government investments in biologic drug production and vaccine manufacturing. The Brazilian Health Regulatory Agency (ANVISA) is promoting advanced biomanufacturing technologies, encouraging local firms like Instituto Butantan and Fiocruz to adopt continuous bioprocessing solutions. The demand for biosimilars, vaccines, and monoclonal antibodies is driving market expansion, with global biopharma companies partnering with Brazilian CMOs to establish continuous biomanufacturing capabilities.

Key Continuous Bioprocessing Company Insights

Companies' key strategies for maintaining their market presence include mergers, acquisitions, and licensing deals for R&D activities. Moreover, companies are expanding their global presence, forming strategic partnerships, and investing in automation and AI-driven bioprocessing solutions to enhance efficiency and scalability in biologics manufacturing.

Key Continuous Bioprocessing Companies:

The following are the leading companies in the continuous bioprocessing market. These companies collectively hold the largest market share and dictate industry trends.

- Danaher

- Sartorius AG

- Thermo Fisher Scientific Inc.

- WuXi Biologics

- Ginkgo Bioworks

- Merck KGaA

- GE Healthcare

- Repligen Corporation

- Asahi Kasei Bioprocess America, Inc.

Recent Development

-

In June 2024, PAK BioSolutions secured USD 12 million in funding from Arboretum Ventures, BroadOak Capital Partners, and other investors to support the expansion of its commercial operations and product development for its automated continuous manufacturing systems designed for biologics. The company's PAK Pilot System can process 50 to 500 liters of cell culture daily, catering to a significant portion of the biopharmaceutical production market by offering an efficient and scalable solution.

-

In August 2023, Sartorius partnered with Repligen Corporation to introduce the Integrated Bioreactor System. This system seamlessly integrates Repligen’s XCell ATF upstream intensification technology with Sartorius' Biostat STR bioreactor, streamlining intensified seed train and N perfusion implementation for biopharmaceutical manufacturers.

-

In July 2022, Cytiva expanded its operations by establishing a new chromatography resins manufacturing facility in Muskegon, Michigan, as part of its broader investment in expansion.

-

In February 2021, The United States Pharmacopeia (USP) and Plow Corp. have partnered to create a new laboratory focused on developing test methods and standards for continuous manufacturing. This facility emphasizes product development, technology transfer, and drug application filings, aiming to accelerate the adoption of continuous manufacturing among generic drug producers and pharmaceutical manufacturers.

Continuous Bioprocessing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 387.89 million

Revenue Forecast in 2030

USD 911.43 million

Growth Rate

CAGR of 18.63% from 2025 to 2030

Actual Data

2018 - 2024

Forecast period

2025 - 2030

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2030

Report Coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments Covered

Product, application, end use and region

Regional scope

North America, Europe, Asia Pacific, Latin America, and MEA

Country scope

U.S., Canada, Mexico, UK, Germany, France, Italy, Spain, Denmark, Sweden, Norway, China, Japan, India, Australia, South Korea, Thailand, Brazil, Argentina, Saudi Arabia, South Africa, UAE, Kuwait

Key companies profiled

Danaher; Sartorius AG; Thermo Fisher Scientific Inc.; WuXi Biologics; Ginkgo Bioworks; Merck KGaA; GE Healthcare; Repligen Corporation; Asahi Kasei Bioprocess America, Inc.

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Continuous Bioprocessing Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and analyzes the latest industry trends in each sub-segment from 2018 to 2030. For this study, Grand View Research has segmented the global continuous bioprocessing market report based on product, application, end use, and region:

-

Product Outlook (Revenue, USD Million, 2018 - 2030)

-

Instruments

-

Bioreactors

-

Filtration Systems

-

Chromatography Systems

-

Process Analytical Technologies

-

Others

-

-

Consumables & Reagents

-

Media & Buffers

-

Filters & Membranes

-

Resin

-

Tubing & Bags

-

Others

-

-

-

Application Outlook (Revenue, USD Million, 2018 - 2030)

-

Monoclonal antibodies

-

Vaccines

-

Cell and gene therapy

-

Research & Development

-

Other applications

-

-

End Use Outlook (Revenue, USD Million, 2018 - 2030)

-

Pharmaceutical and biotechnology companies

-

CMOs and CROs

-

Research and academic institutes

-

-

Regional Outlook (Revenue in USD Million, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global continuous bioprocessing market size was estimated at USD 349.29 million in 2024 and is expected to reach USD 387.89 million in 2025.

The global continuous bioprocessing market is expected to grow at a compound annual growth rate of 18.63% from 2025 to 2030 to reach USD 911.43 million by 2030.

North America dominated the market with the largest revenue share of 37.46% in 2024. The market is driven by strong investments in biopharmaceutical R&D, advanced manufacturing infrastructure, and supportive regulatory policies.

Some key players operating in the continuous bioprocessing market include Danaher, Sartorius AG, Thermo Fisher Scientific Inc., WuXi Biologics, Ginkgo Bioworks, Merck KGaA, GE Healthcare, Repligen Corporation, Asahi Kasei Bioprocess America, Inc.

The increasing demand for biopharmaceuticals, including monoclonal antibodies, cell and gene therapies, and vaccines, is a key driver of the continuous bioprocessing industry. Traditional batch processing methods are often inefficient, leading to high costs, long production cycles, and limited scalability.

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.