- Home

- »

- Network Security

- »

-

Cybersecurity Services Market Size Report, 2026-2033GVR Report cover

![Cybersecurity Services Market (2026 - 2033)Report]()

Cybersecurity Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Services (Professional Services, Managed Services), By End Use (BFSI, Healthcare, Defense & Government, Retail, Energy, Manufacturing, Others), By Region, And Segment Forecasts

Market Size, 2025

$53.6BMarket Estimate, 2026

$61.3BMarket Forecast, 2033

$161.0BCAGR, 2026–2033

14.8%Cybersecurity Services Market Summary

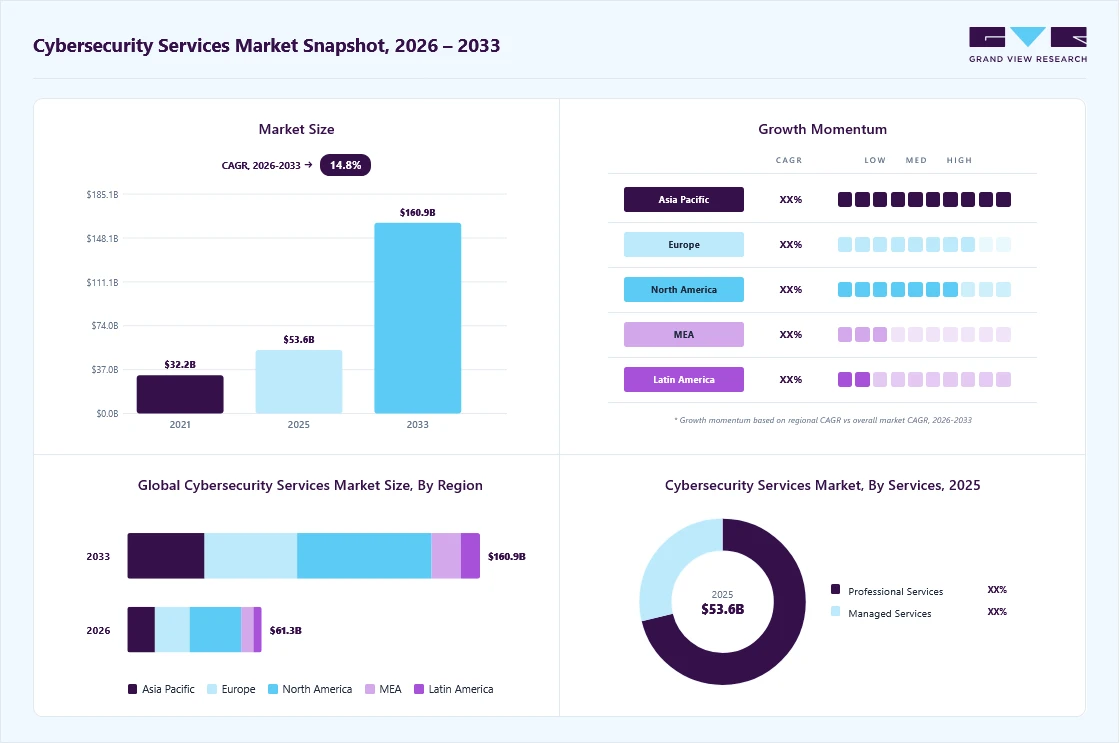

The global cybersecurity services market size was valued at USD 53.6 billion in 2025 and is projected to grow from USD 61.3 billion in 2026 to USD 161.0 billion by 2033, at a CAGR of 14.8% from 2026 to 2033. The market in North America dominated with a revenue share of 38.4% in 2025. Advances in Artificial Intelligence (AI), the Internet of Things (IoT), and Machine Learning (ML) have led to increased adoption of web and mobile applications, creating a more complex IT infrastructure that is increasingly vulnerable to cyberattacks.

Key Market Trends & Insights

- By services: Professional services segment held the largest market share of 71.1% in 2025.

- By end use: Defense and government segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (38.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 53.6 Billion

- Estimated market size in 2026: USD 61.3 Billion

- Projected market size by 2033: USD 161.0 Billion

- CAGR (2026-2033): 14.8%

To address potential security challenges, organizations are outsourcing security services to detect bugs and analyze the security landscape while efficiently responding to cyberattacks. The need to fix bugs in web applications and mobile apps and mitigate data loss risks associated with cybercrimes is expected to fuel the adoption of cybersecurity services over the forecast period.")

Rising awareness among Small and Medium-sized Enterprises (SMEs) and advancements in Artificial Intelligence (AI)-powered threat detection are helping address the shortage of skilled cybersecurity professionals and reducing the high costs of comprehensive solutions. The adoption of managed security services, which offer scalable, cost-effective solutions, has increased significantly, particularly among organizations with limited resources. The surge in Internet of Things (IoT) devices and the expansion of 5G networks are creating more vulnerabilities, driving the need for advanced, adaptable security solutions. Companies are increasingly adopting zero-trust security models, which continuously verify access to systems and data. At the same time, AI and Machine Learning (ML) are transforming the field by enabling faster threat detection, predictive analytics, and real-time responses to cyberattacks.

The proliferation of smartphones and the continued rollout of high-speed internet networks have driven the adoption of mobile banking and health-monitoring, shopping, and socializing apps. Mobile banking induces flexibility in banking practices by allowing users to transact irrespective of their location. Customers can also shop using e-commerce apps and make payments using their smartphones. As the number of smartphone users continues to increase, the preference for banking, shopping, making payments, and socializing via mobile apps is also growing. However, all these applications have also emerged as potential targets for hackers, thereby prompting companies to opt for cybersecurity services to identify loopholes in the applications, plug the loopholes, and subsequently save users from potential losses.

The number of cyberattacks worldwide shows no signs of abating. At the same time, cyberattacks are becoming more sophisticated, and the losses they cause are also increasing. While new networks are being rolled out and existing ones are being expanded, they are increasingly vulnerable to cyber threats. As a result, businesses are actively seeking advanced cybersecurity solutions to safeguard data and maintain operational integrity. This is driving the need to continuously monitor the networks, critical infrastructure, and digital assets of both small and large enterprises and hunt for potential threats. In November 2024, HCLTech launched DataTrustShield in collaboration with Intel, providing advanced cloud and data security for enterprises. Leveraging Intel TDX and Trust Authority, the solution ensures secure data sharing, scalability, and compliance. This strengthens the cybersecurity services market by protecting sensitive information and enhancing trust in cloud operations.

Services Insights

The professional services segment accounted for the largest market share of 71.1% in 2025, which can be attributed to the increasing demand for specialized expertise in areas such as risk assessments, penetration testing, and vulnerability management. The rapid adoption of new technologies such as cloud computing and IoT is driving the need for customized security solutions, prompting businesses to seek expert guidance. The need for regulatory compliance and stricter data protection laws in the cybersecurity services industry also increases demand for services such as audits and privacy assessments. In addition, the shortage of skilled cybersecurity professionals is leading organizations to rely on external providers for ongoing security monitoring, incident response, and managed services. These services help businesses maintain strong security while focusing on their core operations.

The managed services segment is expected to register a CAGR of around 15.3% from 2026 to 2033. This growth can be attributed to the increasing complexity of cyber threats, the shortage of skilled cybersecurity professionals, and the growing adoption of cloud computing and remote work. In addition, businesses seek to enhance their security posture without the burden of managing everything in-house, driving the demand for Managed Security Service Providers (MSSPs). Furthermore, MSSPs offer access to expert teams, advanced security tools, and scalable solutions that can adapt to evolving threats and compliance requirements, further fueling the growth of managed services in the coming years.

End Use Insights

The defense and government segment dominated the cybersecurity services market in 2025. This segment’s vulnerability stems from its handling of sensitive data, such as national security information and military strategies, which are frequent targets of cybercriminals. As a result, companies are introducing advanced partner programs to help organizations enhance security capabilities and address evolving threats. With governments confronting escalating threats to their data stored both on-premises and in the cloud, the demand for sophisticated security systems capable of countering these attacks is also surging. In February 2024, DirectDefense launched a new partner program enabling IT and managed service providers to offer managed security, OT, and professional services. The program expands revenue opportunities and strengthens client relationships. Recognized on CRN’s MSP 500 and with two executives named Channel Chiefs, this initiative reinforces its role in the industry.

The BFSI segment is projected to be the fastest-growing in the cybersecurity services market primarily due to its high exposure to cyber threats, rapid digital transformation, and stringent regulatory requirements. Financial institutions handle highly sensitive data and large volumes of transactions, making them prime targets for cyberattacks such as fraud, phishing, and ransomware, which drives continuous investment in advanced security solutions. At the same time, the widespread adoption of digital banking, mobile payments, cloud platforms, and fintech integrations has significantly expanded the attack surface, increasing the need for robust cybersecurity frameworks. Additionally, strict compliance mandates and data protection regulations compel BFSI organizations to continuously upgrade their security infrastructure, while the growing sophistication of cyber threats further accelerates demand for managed security services, threat intelligence, and real-time monitoring, collectively driving the segment’s strong growth.

Regional Insights

The North America cybersecurity services industry is expected to grow at a significant CAGR over the forecast period 2026 to 2033, driven by increasing cyber threats, stringent regulatory requirements, and the widespread adoption of advanced technologies such as cloud computing and IoT. Organizations are rapidly embracing zero-trust security models to mitigate risks associated with expanding attack surfaces. The region's strong IT infrastructure and the presence of major cybersecurity vendors foster innovation, while AI and ML are being increasingly integrated into security solutions for real-time threat detection.

U.S. Cybersecurity Services Market Trends

The cybersecurity services industry in the U.S. dominated the industry in 2025, which can be attributed to rising cyber threats, rapid technology adoption, and stringent regulations such as the California Consumer Privacy Act (CCPA). High-profile attacks on critical infrastructure and enterprises have pushed organizations to adopt advanced security solutions, including AI-powered threat detection and zero-trust architecture. The expansion of cloud computing, IoT, and remote work has further increased the need for robust cybersecurity measures. Government initiatives, such as the Biden Administration’s Executive Order on Improving the Nation’s Cybersecurity, have boosted investments in infrastructure modernization and enhancing public-private collaborations. The shortage of skilled cybersecurity professionals has led businesses to rely on MSSPs for expertise and scalable solutions. These factors collectively position the U.S. as a key leader in the global cybersecurity services industry.

Asia Pacific Cybersecurity Services Market Trends

The cybersecurity services industry in the Asia Pacific accounted for a significant share of 34.2% in 2025. This growth is driven by the increasing digitalization of businesses, rising cyberattacks, and government initiatives to strengthen cybersecurity frameworks. The region’s growing reliance on cloud services and IoT has created an urgent need for advanced security solutions. Key industries such as BFSI, healthcare, and manufacturing are driving market demand as they adopt digital technologies while addressing regulatory requirements. The region’s diverse economies and varying levels of cybersecurity maturity present both challenges and opportunities for service providers.

The China cybersecurity services industry has been growing significantly during the forecast period, which can be attributed to the rapid digitalization and stringent domestic regulations such as the Cybersecurity Law of the People’s Republic of China and the Data Security Law. These laws enforce strict guidelines for protecting critical infrastructure, industrial systems, and personal data, compelling businesses to invest in advanced cybersecurity measures. The rise in cyberattacks targeting key sectors such as manufacturing, finance, and government services has heightened the urgency for both managed and professional security services tailored to China’s specific needs.

The cybersecurity services industry in India is growing significantly, driven by increasing digitalization and the adoption of cloud technologies. Rising cyber threats targeting businesses and government organizations are boosting demand for advanced security solutions. The market benefits from government initiatives promoting data protection and IT infrastructure security. Growing awareness among enterprises about compliance and risk management is further supporting expansion. In addition, investments in AI-based threat detection and managed security services are strengthening the overall cybersecurity ecosystem in the country.

The Japan cybersecurity services industry is expected to grow significantly at a CAGR from 2026 to 2033, driven by increasing digital transformation and adoption of cloud and IoT technologies. Rising cyber threats targeting enterprises and critical infrastructure are boosting demand for advanced security solutions. The market benefits from government regulations and initiatives focused on data protection. Growing investments in AI-based threat detection and managed security services are further supporting expansion.

Europe Cybersecurity Services Market Trends

The cybersecurity services industry in Europe is anticipated to register considerable growth from 2026 to 2033, due to rising awareness of cyber threats, stringent data protection regulations, and rapid digital transformation across industries. The GDPR compliance has been a significant driver, pushing organizations to adopt stricter security measures to avoid penalties. The region is also seeing an increase in the adoption of managed security services while businesses address the shortage of cybersecurity professionals.

The UK cybersecurity services industry is growing significantly during the forecast period, driven by rising digital adoption and increasing cyber threats targeting businesses and public sector organizations. Strong government initiatives and regulations supporting data protection are boosting demand. Enterprises are investing in advanced security solutions, including managed services and AI-based threat detection. Growing awareness of compliance and risk management is further fueling market growth.

The cybersecurity services industry in Germany is expected to grow significantly at a CAGR from 2026 to 2033, driven by increasing digitalization across enterprises and the adoption of cloud and IoT technologies. Rising cyber threats targeting critical infrastructure and businesses are boosting demand. Government regulations and initiatives supporting data protection further propel growth. Investments in AI-based threat detection and managed security services are increasing. In addition, organizations are focusing on compliance, risk management, and the safeguarding of sensitive information, thereby strengthening the overall cybersecurity ecosystem.

Key Cybersecurity Services Company Insights

Some of the key companies operating in the market include Accenture, AT&T INC., and others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In July 2025, CyberRisk Alliance and Bleeping Computer partnered to deliver expert-led webinars for the cybersecurity community. The collaboration provides interactive, real-world guidance on threats, cloud security, ransomware, and identity management. By offering live education and insights, the initiative strengthens the cybersecurity services market and helps professionals stay ahead of evolving risks.

-

In December 2024, GoSecure partnered with SMART USA to strengthen cybersecurity for U.S. semiconductor research and manufacturing. The collaboration focuses on advanced threat monitoring, incident response, and secure operations, supported by CyManII and Idaho National Labs. This initiative enhances the cybersecurity services industry by safeguarding critical technology infrastructure and supporting innovation.

-

In October 2024, Thales and BCG partnered to strengthen cyber resilience for large enterprises, combining Thales’ advanced cybersecurity services with BCG’s strategic consulting. The collaboration offers crisis preparedness, tailored simulations, and dedicated management support, enhancing the cybersecurity services market by helping companies prevent, respond to, and recover from escalating digital threats.

Key Cybersecurity Services Companies:

The following key companies have been profiled for this study on the cybersecurity services market.

- Accenture

- AT&T INC.

- Atos SE

- Capgemini

- Cisco Systems, Inc

- CrowdStrike Holdings, Inc

- Deloitte

- DXC Technology Company

- IBM Corporation

- Rapid7

Cybersecurity Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 53.6 billion

Estimated Market size in 2025

USD 61.3 billion

Projected Market size by 2033

USD 161.0 billion

Growth rate

CAGR of 14.8% from 2026 to 2033

Actual data

2021 - 2024

Base year

2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Services, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East and Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; Kingdom of Saudi Arabia (KSA); UAE; South Africa

Key companies profiled

Accenture; AT&T INC.; Atos SE; Capgemini; Cisco Systems, Inc; CrowdStrike Holdings, Inc; Deloitte; DXC Technology Company; IBM Corporation; Rapid7

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cybersecurity Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and offers qualitative and quantitative analysis of the market trends for each of the segments and sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global cybersecurity services market report based on services, end use, and region:

-

Services Outlook (Revenue, USD Million, 2021 - 2033)

-

Professional Services

-

Integration

-

Support and Maintenance

-

Training, Consulting, and Advisory

-

Penetration Testing

-

Bug Bounty

-

Others

-

-

Managed Services

-

Managed Detection Response (MDR)

-

Managed Security Incident and Event Management (SIEM)

-

Compliance and Vulnerability Management

-

Others

-

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

BFSI

-

Retail

-

Healthcare

-

IT & Telecom

-

Defense and Government

-

Energy

-

Manufacturing

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global cybersecurity services market is expected to grow at a compound annual growth rate of 14.8% from 2026 to 2033 to reach USD 161.0 billion by 2033.

The professional services segment accounted for the largest market share in the cybersecurity services market in 2025, driven by the increasing demand for specialized expertise in areas such as risk assessments, penetration testing, and vulnerability management.

Some key players operating in the market include Accenture, AT&T INC., Atos SE, Capgemini, Cisco Systems, Inc, CrowdStrike Holdings, Inc, Deloitte, DXC Technology Company, IBM Corporation, Rapid7, and Others.

The global cybersecurity services market size was estimated at USD 53.6 billion in 2025 and is expected to reach USD 61.3 billion in 2026.

Factors such as rising awareness among SMEs and advancements in Artificial Intelligence (AI)-powered threat detection are helping address the shortage of skilled cybersecurity professionals and reducing the high costs of comprehensive solutions.

North America dominated with a 38.4% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The defense and government segment held the largest revenue share in 2025, while the BFSI segment is the fastest-growing.

About the Author(s)

Network Security Research Team

Technology · Network SecurityThis report was authored by the network security research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the network security segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.