- Home

- »

- Communications Infrastructure

- »

-

Data Center Colocation Market Size & Share Report, 2033GVR Report cover

![Data Center Colocation Market (2026 - 2033)Report]()

Data Center Colocation Market (2026 - 2033)

Size, Share & Trends Analysis Report By Colocation Type (Retail, Wholesale), By Enterprise Size, By Tier Level (Tier 1, Tier 2), By End Use (BFSI, Retail), By Region, And Segment Forecasts

Market Size, 2025

$91.1BMarket Estimate, 2026

$99.2BMarket Forecast, 2033

$184.4BCAGR, 2026–2033

9.3%Data Center Colocation Market Summary

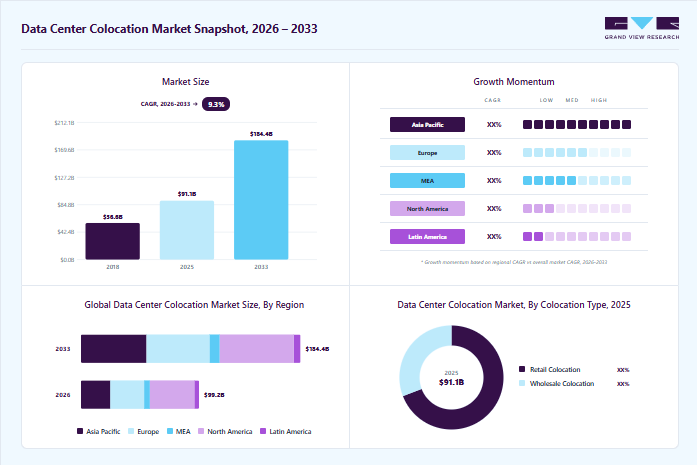

The global data center colocation market size was estimated at USD 91.1 billion in 2025 and is projected to grow from USD 99.2 billion in 2026 to USD 184.4 billion by 2033, growing at a CAGR of 9.3% from 2026 to 2033. North America dominated the market with the largest revenue share of 38.4% in 2025. Data centers play a crucial role in modern corporate operations by managing business applications and supporting IT infrastructure.

Key Market Trends & Insights

- By colocation type, the retail colocation segment led the market with the largest revenue share of 69.2% in 2025.

- By tier level, the Tier 3 segment led the market with the largest revenue share of 58.8% in 2025.

- By enterprise size, the large enterprise segment led the market with the largest revenue share of 58.3% in 2025.

- By end use, the IT & telecom segment led the market with the largest revenue share of 29.7% in 2025.

Regional Highlights

- Largest regional market: North America (38.4% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 91.1 Billion

- Estimated market size in 2026: USD 99.2 Billion

- Projected market size by 2033: USD 184.4 Billion

- CAGR (2026-2033): 9.3%

As companies increasingly rely on data, the demand for robust IT solutions has grown, leading to greater adoption of cloud services. Colocation data centers provide businesses with the flexibility to scale IT resources efficiently. Additionally, the high costs associated with building and maintaining in-house data centers, especially for organizations with fluctuating data needs, have been a significant factor driving market growth.The rise of technologies such as cloud computing, autonomous vehicles, IoT, and advanced robotics has driven demand for faster data processing and higher bandwidth. These technologies require low latency and high-speed network connectivity, making colocation data centers an ideal solution. By strategically locating facilities closer to end users, colocation providers enhance storage and networking capabilities. In the data center colocation industry, the expansion of 5G technology is expected to further boost colocation deployments, particularly in remote areas.

Additionally, the growing adoption of cloud data centers, driven by cost efficiency, is accelerating market growth. SMEs are increasingly turning to cloud solutions to reduce IT expenses, eliminate the need for dedicated IT staff, and benefit from scalable, low-cost infrastructure. To strengthen their market position, major industry players are engaging in strategic initiatives such as partnerships, acquisitions, and mergers.

")

Customers can leverage Digital Exchange to deploy IT infrastructure on demand, creating a foundation for modernizing operations in an increasingly digital landscape. The rise of 5G, AR, VR, and AI has significantly increased the demand for higher bandwidth to facilitate seamless data sharing between businesses. Additionally, the growing adoption of autonomous vehicles and advanced robotics has driven the need for low-latency solutions, further boosting the demand for colocation services. By allowing cloud service providers to establish data centers closer to end users, colocation ensures faster data transfers and higher bandwidth.

With the shift toward edge computing and cloud migration, businesses require high-capacity networks for seamless data processing. While colocation has some limitations, such as shared facilities and limited control over location and upgrades, its advantages, including enhanced connectivity, improved network security, redundant power supply, scalability, and cost efficiency, far outweigh the drawbacks. These benefits continue to attract businesses, accelerating the growth of the data center colocation market.

Market Dynamics

Data center colocation services are gaining significant traction as enterprises increasingly seek scalable, secure, and cost-efficient infrastructure solutions without the capital burden of building and maintaining their own data centers. Colocation facilities provide businesses with access to advanced power, cooling, connectivity, physical security, and disaster recovery capabilities while enabling rapid deployment of IT infrastructure. The growing adoption of cloud computing, artificial intelligence (AI), big data analytics, Internet of Things (IoT), and digital transformation initiatives across industries is driving demand for carrier-neutral and hyperscale colocation facilities.

The accelerating adoption of cloud computing, artificial intelligence (AI), big data analytics, and digital transformation initiatives is a major driver of the data center colocation market. Enterprises across industries are increasingly outsourcing infrastructure requirements to colocation providers to gain access to scalable power, cooling, connectivity, and security capabilities without incurring the high capital costs associated with building proprietary data centers. The growing use of hybrid cloud architectures, AI model training, high-performance computing (HPC), and data-intensive applications is further increasing demand for carrier-neutral and hyperscale colocation facilities. As organizations continue modernizing their IT environments and expanding digital services, colocation providers are becoming critical partners in supporting flexible and scalable infrastructure deployment.

For instance, in May 2026, Digi Power X announced a long-term colocation agreement with Cerebras Systems to develop a purpose-built 40 MW AI data center campus in Alabama, U.S. The 10-year agreement was designed to support large-scale AI computing workloads requiring substantial power capacity and advanced infrastructure. The announcement highlights how rising demand for AI-driven cloud services and high-density computing environments is accelerating investments in colocation facilities, reinforcing the market's growth trajectory.

High energy consumption and rising operational expenses remain significant restraints for the data center colocation market. Modern data centers require substantial investments in power distribution systems, backup generators, cooling technologies, network infrastructure, and security systems to maintain uninterrupted operations. Increasing electricity prices and growing concerns regarding energy efficiency have further elevated operating costs for colocation providers.

Moreover, stringent environmental regulations and sustainability requirements are compelling operators to invest in renewable energy procurement, carbon reduction initiatives, and advanced cooling solutions, increasing capital expenditure. In regions with limited power availability or aging grid infrastructure, obtaining sufficient power capacity for new facilities can be challenging, potentially delaying expansion projects and constraining market growth.

The rapid growth of artificial intelligence, edge computing, and hyperscale data center deployments is creating substantial opportunities for the data center colocation market. AI training and inference workloads require high-density computing environments with significant power and cooling capabilities, encouraging enterprises and cloud providers to partner with colocation operators that can support advanced infrastructure requirements.

Additionally, the increasing deployment of edge computing infrastructure to support real-time applications such as autonomous vehicles, industrial automation, smart cities, 5G networks, and IoT ecosystems is driving demand for geographically distributed colocation facilities. Hyperscale cloud providers are also expanding their global footprints through strategic colocation partnerships to accelerate market entry and reduce deployment timelines. These trends, combined with growing investments in renewable-powered and AI-ready data centers, are expected to create significant long-term growth opportunities for colocation service providers.

Analyst Perspective

The data center colocation market sits at the intersection of several powerful structural growth drivers, including accelerating cloud adoption, the proliferation of artificial intelligence (AI) workloads, expanding digital transformation initiatives, and rising enterprise demand for scalable and resilient IT infrastructure. As organizations increasingly prioritize operational agility and cost efficiency, colocation has emerged as a strategic alternative to building and maintaining proprietary data centers. The market also benefits from long-term demand generated by hyperscale cloud providers, edge computing deployments, 5G network expansion, and growing data sovereignty requirements. The central competitive advantage, however, will belong to providers that can seamlessly integrate high-density AI-ready infrastructure, renewable energy sourcing, robust interconnection ecosystems, and geographically diversified facilities into a unified platform.

Colocation Type Insights

Based on colocation type, the retail colocation segment led the market with the largest revenue share of 69.2% in 2025. Retail colocation allows businesses to lease smaller spaces within a data center, making it an ideal solution for managing smaller data volumes with minimal infrastructure requirements. This cost-effective model has driven strong adoption among SMEs, enabling them to access secure and scalable IT infrastructure without the high expenses of building their own data centers. The low-budget requirement further enhances its appeal, making retail colocation a preferred choice for SMEs seeking affordable, reliable, and flexible data solutions.

The wholesale colocation segment is expected to grow at a significant CAGR of 18.6% over the forecast period. Leading cloud service providers are increasingly adopting colocation to cater to large enterprises, which require extensive data storage and high-performance infrastructure. With a broad customer base generating massive data volumes, large enterprises demand spacious, scalable, and secure facilities to house their servers. This shift has been a key driver for the growth of the wholesale colocation segment, as enterprises seek cost-effective, high-capacity solutions to support their expanding digital operations, ultimately fueling overall market growth.

Tier Level Insights

Based on tier level, the Tier 3 segment led the market with the largest revenue share of 58.8% in 2025, driven by enterprises, cloud service providers (CSPs), financial institutions, and technology firms that require high reliability, scalability, and redundancy. Tier 3 facilities offer a significant uptime guarantee of 99.982% (~1.6 hours of downtime annually) and include N+1 redundancy for power and cooling, making them a preferred choice for mission-critical workloads, hybrid cloud deployments, and digital transformation initiatives.

The tier 4 segment is expected to grow at a significant CAGR over the forecast period. The rise of hyper scale cloud providers, artificial intelligence (AI), and high-performance computing (HPC) is fueling demand for Tier 4 colocation facilities. AI-driven workloads, deep learning models, and data-intensive applications require high-density computing power, precision cooling, and uninterrupted operations, all of which Tier 4 colocation centers are designed to support.

Enterprise Size Insights

Based on enterprise size, the large enterprise segment led the market with the largest revenue share of 58.3% in 2025. Ensuring uninterrupted business operations is a top priority for large enterprises, especially those handling mission-critical applications such as financial transactions, cloud-based SaaS platforms, and government operations. Colocation data centers provide redundant power, backup generators, disaster recovery solutions, and geographically distributed infrastructure, ensuring 99.999% uptime and minimal downtime risks. This is particularly beneficial for enterprises that require real-time replication, failover strategies, and instant data recovery solutions.

The SMEs segment is expected to grow at a significant CAGR over the forecast period. The rapid growth of software-as-a-service (SaaS) startups, fintech companies, and digital-first SMEs is driving demand for secure, high-performance colocation services. These businesses require scalable IT environments to support continuous software development, cloud-native applications, and real-time financial transactions. Colocation provides enterprise-grade infrastructure that enables startups and tech-driven SMEs to accelerate innovation while ensuring data security and reliability.

End Use Insights

Based on end use, the IT & telecom segment led the market with the largest revenue share of 29.7% in 2025. The global 5G deployment is a key driver for colocation data centers, as telecom operators require low-latency infrastructure to support ultra-fast network speeds. According to GSMA, 5G networks are expected to cover over 60% of the global population by 2027, increasing the need for edge data centers to process data closer to end users. Colocation facilities offer high-speed fiber connectivity, carrier-neutral ecosystems, and edge computing capabilities, allowing telecom providers to reduce network congestion, improve mobile broadband performance, and support applications like IoT, smart cities, and autonomous vehicles.

The healthcare segment is expected to grow at a significant CAGR over the forecast period. The healthcare sector is witnessing a rapid digital transformation, driven by electronic health records (EHRs), telemedicine, AI-driven diagnostics, and medical IoT (IoMT). The growing volume of patient data, real-time monitoring applications, and regulatory compliance requirements has led to an increasing demand for high-performance, secure, and scalable IT infrastructure.

Regional Insights

North America dominated the data center colocation market with the largest revenue share of 38.4% in 2025, due to the expanding cloud computing industry, AI-driven workloads, and increasing enterprise digitalization. The region's strong presence of hyperscalers like AWS, Microsoft Azure, and Google Cloud drives demand for high-performance, interconnected colocation facilities. The rise of 5G, IoT deployments, and edge computing is also fueling colocation adoption, particularly in major hubs like Northern Virginia, Dallas, and Silicon Valley.

U.S. Data Center Colocation Market Trends

The data center colocation market in the U.S. held the largest share in the North America region in 2025. The U.S. is the largest market for data center colocation globally, driven by the booming digital economy, AI innovations, and increasing cloud adoption. Key industries like BFSI, healthcare, media, and e-commerce rely on colocation for secure, scalable IT infrastructure.

Europe Data Center Colocation Market Trends

The data center colocation industry in Europe is anticipated to register a considerable growth from 2026 to 2033. The Europe market is expanding due to the rise in cloud adoption, stringent data protection laws (GDPR), and enterprise IT modernization. Countries like Germany, the UK, and the Netherlands are key colocation hubs due to strong connectivity infrastructure and favorable business environments. The demand for AI-ready, high-density colocation facilities is rising as businesses leverage big data, IoT, and machine learning.

The UK data center colocation market is expected to grow rapidly in the coming years, driven by the hybrid cloud revolution, AI investments, and financial services sector requiring secure, high-performance colocation facilities. London remains a top colocation hub, offering direct connectivity to global cloud providers and major financial institutions. The rise of post-Brexit data sovereignty laws is also compelling businesses to keep data within the country, increasing demand for Tier 3 and Tier 4 colocation.

The data center colocation market in Germany held a substantial market share in 2025. The demand for edge computing and low-latency processing is increasing, especially in cities like Berlin and Munich, where industrial and automotive sectors are digitizing rapidly. The country’s commitment to energy-efficient data centers, with mandates for sustainable cooling and renewable energy integration, is also driving colocation providers to invest in green infrastructure.

Asia Pacific Data Center Colocation Market Trends

Asia Pacific data center colocation industry is growing significantly at a CAGR of 12.3% from 2026 to 2033. The market is experiencing rapid expansion due to the rise of digital economies, AI-driven enterprises, and cloud computing adoption. Major tech hubs like Singapore, Tokyo, and Sydney are attracting investments in hyperscale colocation facilities to support growing internet penetration and e-commerce demand. The proliferation of 5G networks and smart city projects is also fueling colocation adoption.

The Japan data center colocation market is expected to grow rapidly in the coming years, due to the rise of AI, IoT, and 5G-driven digital infrastructure. Tokyo and Osaka serve as key colocation hubs, supporting cloud computing, financial services, and gaming industries that require low-latency, high-redundancy data centers. The country’s strict data privacy laws (APPI) and growing cybersecurity threats are driving demand for secure, compliant colocation facilities.

The data center colocation market in China held a substantial market share in 2025, due to the rapid expansion of cloud computing, AI-powered enterprises, and strict data localization laws. Major cities like Beijing, Shanghai, and Shenzhen are witnessing high demand for hyperscale colocation facilities, driven by domestic tech giants like Alibaba Cloud, Tencent, and Huawei Cloud.The government’s cybersecurity and data residency policies require businesses to store data within the country, increasing colocation investments.

Key Data Center Colocation Company Insights

Key players operating in the data center colocation industry are Equinix, Inc., Digital Realty Trust, China Telecom Corporation Limited, NTT Ltd., CyrusOne, and Telehouse. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In September 2024, the US Department of Homeland Security (DHS) granted Equinix, Inc. a contract for colocation services for its Homeland Security Enterprise Network. The tender specifies the provision of "power, connectivity, and related operations and maintenance," with the services encompassing the "Homeland Security Enterprise Network (HSEN) COLO East and West Enterprise cloud access points."

-

In July 2024, Digital Realty Trust announced the acquisition of a colocation data center located in the Slough Trading Estate for USD 200 million. This acquisition expands the company's West London market presence and enhances its colocation capabilities in the City and Docklands areas.

Key Data Center Colocation Companies:

The following key companies have been profiled for this study on the data center colocation market.

-

China Telecom Corporation Limited

-

Cologix

-

Colt Technology Services Group Limited

-

CoreSite

-

CyrusOne

-

Centersquare

-

Digital Realty Trust

-

Equinix, Inc.

-

Flexential

-

Iron Mountain, Inc.

-

NTT Ltd. (NTT DATA)

-

QTS Realty Trust, LLC

-

Rackspace Technology

-

Telehouse (KDDI CORPORATION)

-

Zayo Group, L

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Equinix, Inc., Digital Realty Trust, NTT Ltd., CyrusOne, QTS Realty Trust, LLC, China Telecom Corporation Limited)

- Expand hyperscale and AI-ready data center capacity across key metropolitan and emerging markets.

- Invest in high-density power infrastructure, liquid cooling technologies, and renewable energy procurement.

- Extensive global footprint with strong brand recognition and long-term enterprise relationships.

- Large interconnected ecosystems offering access to multiple cloud providers, network carriers, and digital service platforms.

- High capital expenditure requirements for facility construction, power procurement, and infrastructure modernization.

- Longer deployment timelines due to the complexity of large-scale projects and regulatory approvals.

Emerging Players (CoreSite, Cologix, Flexential, Iron Mountain, Inc., Telehouse, Colt Technology Services Group Limited)

- Focus on regional expansion in high-growth markets with increasing cloud and edge computing demand.

- Differentiate through customized colocation, hybrid IT, and managed service offerings.

- Greater agility in responding to evolving customer requirements and emerging technology trends.

- Strong regional market knowledge and customer relationships.

- Smaller geographic footprints and lower capacity compared to market leaders.

- Limited financial resources for large-scale hyperscale and AI infrastructure investments.

Data Center Colocation Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 91.1 billion

Estimated market size in 2026

USD 99.2 billion

Projected market size by 2033

USD 184.4 billion

Growth rate

CAGR of 9.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share, competitive landscape, growth factors, and trends

Segments covered

Colocation type, tier level, enterprise size, end use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; U.K.; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

China Telecom Corporation Limited; Cologix; Colt Technology Services Group Limited; CoreSite; CyrusOne; Centersquare; Digital Realty Trust; Equinix, Inc.; Flexential; Iron Mountain, Inc.; NTT Ltd. (NTT DATA); QTS Realty Trust, LLC; Rackspace Technology; Telehouse (KDDI CORPORATION); Zayo Group, LLC.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Data Center Colocation Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the data center colocation market report based on colocation type, tier level, enterprise size, end use, and region:

-

Colocation Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Retail Colocation

-

Wholesale Colocation

-

-

Tier Level Outlook (Revenue, USD Billion, 2021 - 2033)

-

Tier 1

-

Tier 2

-

Tier 3

-

Tier 4

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

SMEs

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Retail

-

BFSI

-

IT & Telecom

-

Healthcare

-

Media & Entertainment

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Colocation Type

Revenue capture definition

Retail Colocation

Revenue is primarily generated through recurring monthly or annual rental fees charged for racks, cabinets, cages, power consumption, cross-connects, and managed services. Customers typically include enterprises, SMEs, cloud-native companies, and network providers seeking flexible infrastructure without large upfront capital investments.

Wholesale Colocation

As the largest type segment, revenue is primarily captured through tiered subscription models (free cycle-tracking with premium fertility/hormone insights) and, increasingly, through payer/insurer reimbursement partnerships that cover period and ovulation monitoring for reproductive planning.

Segment - Tier Level

Revenue capture definition

Tier 1

Revenue is generated from cost-sensitive customers requiring basic colocation services with limited redundancy and uptime guarantees. Income is primarily derived from rack space rentals and power provisioning for non-critical workloads, development environments, and smaller enterprise deployments where affordability outweighs availability requirements.

Tier 2

Revenue is captured through colocation contracts offering partial redundancy in power and cooling infrastructure. Customers include regional enterprises, managed service providers, and growing digital businesses seeking a balance between cost efficiency and operational reliability.

Tier 3

As the dominant tier segment, revenue is primarily earned through premium colocation contracts that provide concurrently maintainable infrastructure, high uptime guarantees, and enhanced security. Enterprise customers, cloud providers, financial institutions, and government agencies pay recurring fees for mission-critical workloads, interconnection services, and disaster recovery capabilities.

Tier 4

Revenue is generated through premium-priced contracts supporting fault-tolerant infrastructure with the highest levels of redundancy and availability. Customers include hyperscalers, financial trading firms, healthcare organizations, and government agencies operating mission-critical applications where downtime carries substantial operational or financial risk.

Segment - Enterprise Size

Revenue capture definition

Large Enterprises

Revenue is predominantly captured through large-scale, multi-year colocation agreements covering high-density deployments, dedicated suites, hybrid cloud integration, and disaster recovery environments. Additional revenue is generated from managed services, direct cloud connectivity, cybersecurity solutions, and customized infrastructure requirements supporting global operations.

SMEs

Revenue is generated through flexible retail colocation offerings that allow small and medium-sized businesses to access enterprise-grade infrastructure without significant capital expenditures. Subscription-based pricing models for rack space, connectivity, managed hosting, and cloud interconnection services are key contributors to revenue growth in this segment.

Segment - End Use

Revenue capture definition

Retail

Revenue is captured through colocation services supporting e-commerce platforms, omnichannel retail systems, payment processing infrastructure, inventory management applications, and customer analytics platforms. Demand increases during seasonal shopping peaks, driving additional spending on scalable capacity and disaster recovery solutions.

BFSI

Revenue is primarily generated through premium colocation contracts supporting mission-critical banking applications, digital payments, trading platforms, fraud detection systems, and regulatory compliance requirements. Financial institutions typically demand high-availability infrastructure, advanced security, and low-latency connectivity, resulting in higher average revenue per customer.

IT & Telecom

As the largest end-use segment, revenue is captured through large-scale deployments supporting cloud computing, managed services, telecommunications networks, content delivery, AI workloads, and edge computing infrastructure. Additional revenue streams arise from interconnection services, carrier-neutral ecosystems, and high-capacity network connectivity.

Healthcare

Revenue is generated through secure colocation environments supporting electronic health records (EHRs), telemedicine platforms, medical imaging storage, clinical applications, and healthcare analytics. Demand for regulatory compliance, data protection, and business continuity solutions contributes to premium service adoption within the segment.

Media & Entertainment

Revenue flows from hosting and distributing digital content, video streaming platforms, gaming infrastructure, broadcasting systems, and content delivery networks (CDNs). The growing consumption of high-definition and real-time digital content drives demand for scalable, low-latency colocation facilities and connectivity services.

Others

This segment captures revenue from government agencies, manufacturing companies, energy providers, educational institutions, logistics operators, and research organizations utilizing colocation facilities for secure data storage, business continuity, IoT deployments, industrial applications, and digital transformation initiatives. Revenue is generated through a combination of rack rentals, managed services, connectivity solutions, and customized infrastructure deployments.

Estimation Model

Colocation Demand layer

Addressable Market Layer

Adoption & Capacity Utilization Layer

Monetisation Layer

Who can benefit from colocation services?

Who can deploy workloads in colocation facilities?

Who actively leases colocation capacity?

How much revenue is generated?

Identify total enterprises, cloud providers, telecom operators, government agencies, and digital-native businesses globally to define the potential customer base for third-party data center infrastructure and colocation services.

Apply cloud adoption rates, digital transformation maturity, regulatory requirements, connectivity needs, and outsourcing preferences to determine the realistically serviceable and operationally reachable market.

Apply enterprise migration rates, hyperscale expansion activity, AI infrastructure demand, and workload deployment trends to convert reachable organizations into active colocation customers and capacity users.

Assess revenue generation potential by analyzing spending on rack space, power consumption, connectivity services, cross-connects, managed services, and long-term capacity contracts across the active customer base.

Output: Potential Customer Base

Output: Serviceable Addressable Market

Output: Active Customers & Capacity Users

Output: Revenue Opportunity

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Hyperscale, AI & Cloud Infrastructure Demand Analysis

Conducted a focused assessment of demand trends across hyperscale cloud providers, AI infrastructure operators, and enterprise digital transformation initiatives. Evaluated colocation requirements related to high-density computing, AI-ready facilities, cloud interconnection, edge deployments, power availability, and liquid cooling adoption across major global markets.

Helps stakeholders identify high-growth demand centers, prioritize capacity expansion, evaluate AI-driven infrastructure opportunities, and align investment strategies with rapidly evolving cloud and AI workload requirements.

Enterprise Colocation Adoption & Industry Vertical Assessment

Analyzed colocation adoption patterns across BFSI, IT & Telecom, Healthcare, Retail, Media & Entertainment, and government sectors. Assessed enterprise migration from on-premises infrastructure to colocation environments, including hybrid cloud deployment strategies, disaster recovery requirements, cybersecurity needs, and regulatory compliance considerations.

Provides insights into key revenue-generating customer segments, evolving infrastructure requirements, and industry-specific growth opportunities, enabling targeted sales, product development, and market expansion strategies.

Data Center Expansion, Sustainability & Market Opportunity Assessment

Evaluated opportunities related to hyperscale campus development, edge data center expansion, renewable energy integration, carbon-neutral operations, and emerging AI infrastructure investments. Assessed challenges associated with power procurement, land availability, regulatory approvals, sustainability mandates, and competitive positioning across regional markets.

Supports investment and expansion decisions by identifying underserved markets, assessing infrastructure readiness, benchmarking competitive landscapes, and uncovering long-term growth opportunities driven by AI, cloud computing, edge infrastructure, and sustainability initiatives.

Frequently Asked Questions About This Report

The global data center colocation market size was estimated at USD 91.1 billion in 2025 and is expected to reach USD 99.2 billion in 2026.

The global data center colocation market is expected to grow at a compound annual growth rate of 99.2 billion in 2026 to reach USD 184.4 billion by 2033.

North America dominated with 38.4% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The retail type segment led with a 69.2% revenue share in 2025, while the wholesale colocation segment is the fastest-growing segment.

The Tier 3 segment led with a 58.8% revenue share in 2025, while the Tier 4 segment is the fastest-growing segment.

The IT & telecom segment led with a 29.7% revenue share in 2025, while the healthcare segment is the fastest-growing.

Key players operating in the data center colocation market include China Telecom Corporation Limited; Cologix; Colt Technology Services Group Limited; CoreSite; CyrusOne; Centersquare; Digital Realty Trust; Equinix, Inc.; Flexential; Iron Mountain, Inc.; NTT Ltd. (NTT DATA); QTS Realty Trust, LLC; Rackspace Technology; Telehouse (KDDI CORPORATION); Zayo Group, LLC.

Key factors include accelerating the adoption of cloud computing, artificial intelligence (AI), big data analytics, and digital transformation initiatives

About the Author(s)

Communications Infrastructure Research Team

Technology · Communications InfrastructureThis report was authored by the communications infrastructure research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the communications infrastructure segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.