- Home

- »

- Next Generation Technologies

- »

-

Edge Computing Market Size & Share Report, 2026-2033GVR Report cover

![Edge Computing Market (2026 - 2033)Report]()

Edge Computing Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Hardware, Software, Services), By Application (Video Analytics, Connected Cars, Smart Cities), By Organization Size, By Industry Vertical, By Region, And Segment Forecasts

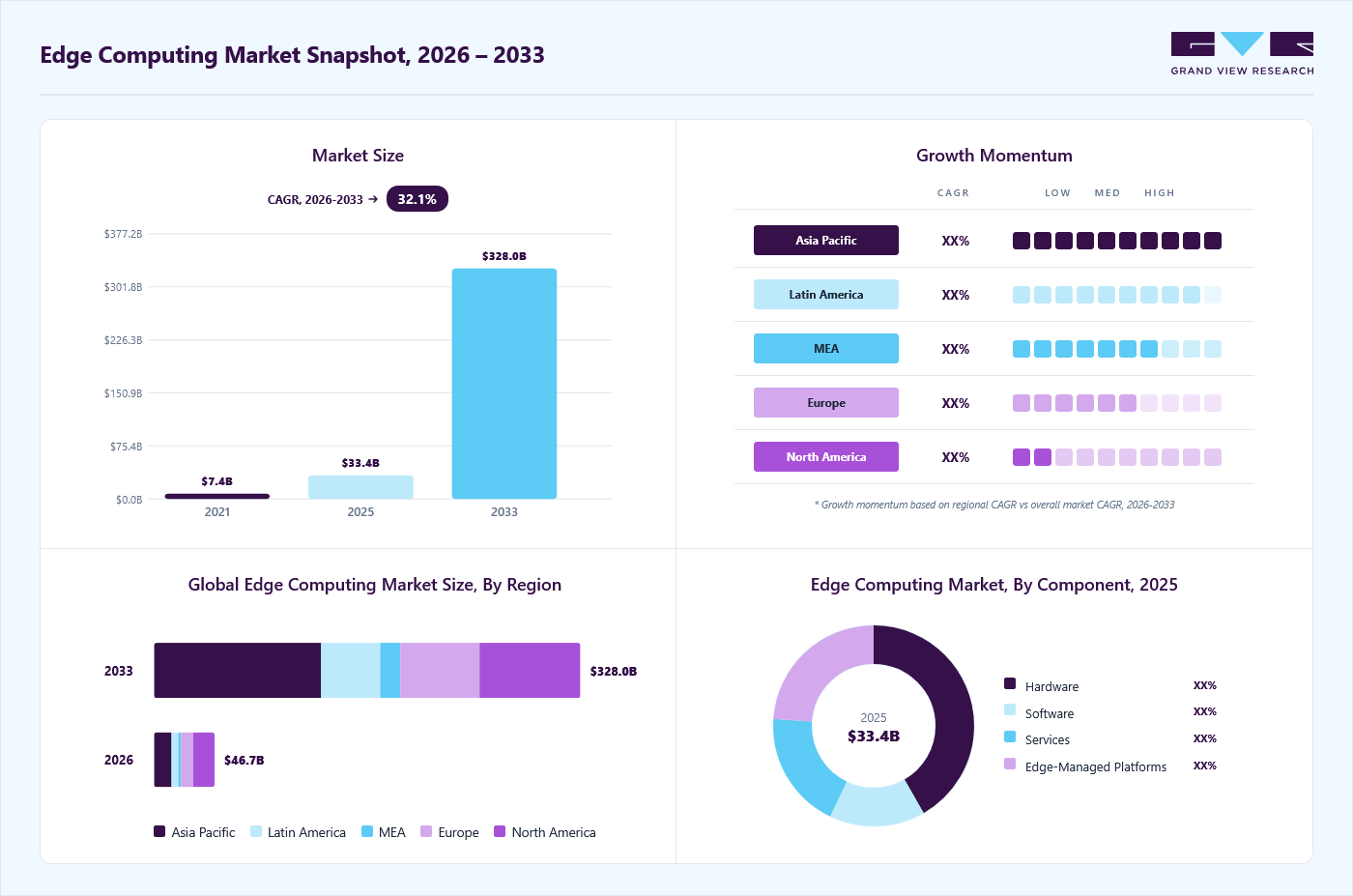

Market Size, 2025

$33.4BMarket Estimate, 2026

$46.7BMarket Forecast, 2033

$328.0BCAGR, 2026–2033

32.1%Edge Computing Market Summary

The global edge computing market size was valued at USD 33.4 billion in 2025 and is projected to grow from USD 46.7 billion in 2026 to USD 328.0 billion by 2033, growing at a CAGR of 32.1% from 2026 to 2033. North America dominated the global market, accounting for the largest revenue share of 36.7% in 2025. Edge computing adds a layer of complexity to organizations by enabling a diverse set of stakeholders to maintain IT infrastructures, networking, software development, traffic distribution, and service management.

Key Market Trends & Insights

- By component: Hardware segment accounted for the largest revenue share of 41.8% in 2025.

- By application: Industrial internet of things (IIoT) segment held the largest revenue share of 22.7% in 2025.

- By organization size: Large enterprise segment accounted for a major revenue share of 67.5% the market in 2025.

- By industry vertical: Manufacturing segment led the market, accounting for the largest revenue share of 20.1% in 2025.

Regional Highlights

- Largest regional market: North America (36.7% revenue share, 2025)

- By country: The edge computing market in the U.S. held the largest share in the North America region in 2025.

Market Size & Forecast

- Market Size in 2025: USD 33.4 Billion

- Estimated Market Size in 2026: USD 46.7 Billion

- Projected Market Size by 2033: USD 328.0 Billion

- CAGR (2026-2033): 32.1%

The increasing demand for faster data processing, reduced latency, and real-time insights is significantly accelerating the adoption of edge computing across industries. The global market is largely driven by integrating software, advanced hardware solutions, and next-gen networking architecture to support a wide array of business use cases. While deployment and operating models are still evolving, this space presents substantial growth opportunities for emerging players and innovators. As enterprises prioritize decentralized computing to enhance responsiveness and efficiency, edge computing is rapidly becoming a foundational element of modern digital infrastructure.A notable market trend is the increasing demand for real-time data processing across diverse industries such as manufacturing and healthcare. Enterprises seek to reduce latency and bandwidth usage. Edge computing offers a decentralized architecture that processes data closer to the source. This allows for faster decision-making, improved data security, and optimized network traffic. The surge in Industrial Internet of Things (IIoT) is reinforcing the importance of the edge computing industry.

")

In addition, the expansion of 5G networks globally is further accelerating the adoption of the edge computing industry. 5G’s ultra-low latency and high throughput capabilities enhance edge infrastructure by supporting various applications such as autonomous vehicles, smart cities, and remote surgeries. Telecommunications providers are integrating Multi-Access Edge Computing (MEC) into their networks to deliver enhanced services with greater responsiveness. This shift is creating new opportunities for the edge computing industry.

Furthermore, the rise of artificial intelligence (AI) and machine learning (ML) at the edge transforms how data is analyzed and utilized. Businesses can derive immediate insights by enabling AI inference at the edge without relying solely on centralized cloud systems. This is especially valuable in mission-critical sectors like defense, retail, and energy, where rapid analytics and decision-making are essential. Integrating AI/ML into edge systems also reduces dependency on cloud connectivity, enhances privacy, and improves operational efficiency.

Leading companies in the edge computing sector are investing heavily in R&D to support innovations and maintain a competitive edge. Strategic partnerships, mergers, and acquisitions are being pursued to strengthen portfolios and enhance market reach. Regulatory developments around data sovereignty and cross-border data flows drive demand for localized edge computing infrastructures, further boosting market growth.

Market Dynamics

The edge computing market is expanding rapidly, driven by increasing demand for real-time data processing, ultra-low-latency applications, and the efficient handling of massive data generated by IoT devices, connected systems, and AI-enabled workloads across industries. Furthermore, the rapid expansion of IoT ecosystems, 5G network deployments, and AI-enabled edge analytics is accelerating the shift toward decentralized computing architectures that reduce dependency on centralized cloud infrastructure and enhance operational efficiency across industries.

The edge computing market is being driven by the increasing need to process and analyze data closer to the source, reducing latency and enabling real-time decision-making across industries such as manufacturing, healthcare, retail, automotive, telecommunications, and energy. Organizations are deploying edge computing infrastructure to support applications such as autonomous vehicles, industrial automation, remote monitoring, video analytics, and augmented reality, all of which require immediate data processing and minimal response times.

The rapidproliferation of Internet of Things (IoT) devices, 5G networks, and artificial intelligence at the edge is further accelerating market growth. Billions of connected sensors and devices generate vast volumes of data that must be processed locally to ensure efficiency and reliability. Telecommunications providers and cloud companies are expanding edge infrastructure to support next-generation applications such as smart factories, connected healthcare systems, and smart cities. In addition, enterprises are increasingly adopting edge computing to enhance data security, improve operational resilience, and ensure business continuity in distributed environments. Overall, rising investments in digital transformation, industrial automation, and real-time analytics are significantly driving the global edge computing market.

Despite strong growth potential, the edge computing market faces several challenges, including infrastructure costs, security, and operational complexity. Deploying edge computing solutions requires substantial investment in hardware, networking equipment, software platforms, and security systems. Organizations must also establish distributed infrastructure across multiple locations, which can increase implementation and maintenance costs, particularly for small and medium-sized enterprises with limited IT budgets.

Another significant restraint is the complexity of managing and securing geographically dispersed edge environments. Edge nodes often operate in remote or uncontrolled settings, making them more vulnerable to cyberattacks, physical tampering, and system failures. Integrating edge infrastructure with existing cloud and on-premises systems can also be technically challenging, requiring advanced orchestration and interoperability capabilities. In addition, the limited availability of skilled professionals in distributed computing, cybersecurity, and IoT systems can slow deployment and adoption. Concerns regarding data governance, regulatory compliance, and standardization further constrain the pace of market expansion.

The rapid deployment of 5G networks, edge artificial intelligence, and industry-focused solutions is creating substantial opportunities in the edge computing market. 5G technology enables ultra-low latency and high-bandwidth connectivity, making it possible to support advanced edge applications such as autonomous transportation, immersive gaming, remote surgery, and intelligent surveillance. Edge AI is also opening new opportunities by enabling devices to process and analyze data locally, delivering faster insights and reducing reliance on cloud connectivity. Industry-specific adoption presents another major growth avenue, with manufacturing, healthcare, retail, and energy sectors increasingly leveraging edge computing to optimize operations and improve responsiveness.

Furthermore, major technology providers such as Amazon Web Services, Microsoft, Google Cloud, IBM, and Cisco Systems are expanding edge computing platforms and services. In contrast, semiconductor leaders such as NVIDIA, Intel, and Advanced Micro Devices continue to introduce powerful processors optimized for edge workloads. These advancements are expected to unlock significant long-term opportunities for the global edge computing market.

Market Concentration & Characteristics

The edge computing market is moderately fragmented, with competition characterized by the presence of global cloud service providers, telecommunications companies, hardware manufacturers, software vendors, and specialized edge computing startups. The market is characterized by a high degree of innovation, driven by AI, 5G, real-time analytics, and distributed computing technologies. M&A activity is medium to high, as technology providers and telecom operators acquire capabilities to strengthen their edge portfolios. The impact of regulations is medium, with data privacy, cybersecurity, and data sovereignty requirements influencing deployments.

Furthermore, the threat from product substitutes is medium, as centralized cloud computing can address some workloads but cannot fully replicate edge computing’s low-latency benefits. End-user concentration is low to medium, with demand spread across manufacturing, healthcare, telecom, retail, transportation, energy, and other industries.

Analyst Perspective

The edge computing market is evolving into a critical pillar of modern digital infrastructure, supported by rising demand for real-time analytics, low-latency processing, and decentralized data architectures across industries. Growth is being shaped by the convergence of IoT expansion, 5G network rollout, and increasing adoption of AI-driven workloads at the network edge, enabling faster decision-making and reduced dependency on centralized cloud systems.

Component Insights

Based on component, the hardware segment accounted for the largest revenue share of 41.8% in 2025. The demand for hardware is gaining steam in the managed services industry and is predicted to account for the most significant market share over the forecast timeline. As the number of IoT and IIoT devices grows quickly, the volume of data created by these devices is also increasing. Therefore, to deal with the volume of data created, enterprises are adopting edge computing gear to lessen the load on the cloud and data centers.

The software segment is projected to have the highest CAGR of over 37% from 2025 to 2033. The increasing demand for scalable, low-latency software frameworks primarily drives this surge. Integrating AI and machine learning models into edge software allows for localized intelligence and automated decision-making. The rise of containerization and edge native orchestration tools, such as Kubernetes at the edge, further supports this momentum by enhancing flexibility. Enterprises prioritizing real-time insights and localized computing capabilities, the software segment is expected to maintain its strong growth trajectory throughout the forecast period.

Application Insights

Based on application, the industrial internet of things (IIoT) segment led the market, accounting for the largest revenue share of 22.7% in 2025. This dominant position is primarily attributed to the rising adoption of edge computing across manufacturing and logistics industries, where real-time data processing and low-latency communication are mission-critical. IIoT applications require localized computing to ensure immediate insights from sensors, machines, and equipment, enabling predictive maintenance and enhanced efficiency. Industries aim to modernize legacy systems and adopt smart factory frameworks, and edge computing continues to serve as a foundational technology for scalable, resilient, and intelligent IIoT deployments.

The AR/VR segment is expected to experience the fastest growth from 2025 to 2033. The rising need for ultra-low latency and real-time data processing in immersive applications drives this growth. AR/VR technologies demand rapid computational response to deliver seamless user experiences. Deploying edge infrastructure closer to end users minimizes latency, enhances data security, and reduces bandwidth consumption, critical factors for high-performance AR/VR use cases. The proliferation of 5G networks, along with increasing investments in metaverse platforms and industrial AR solutions, is accelerating the adoption of edge computing in this segment.

Industry Vertical Insights

Based on industry vertical, the manufacturing segment led the market, accounting for the largest revenue share of 20.1% in 2025. Edge computing enables real-time data processing on the factory floor, enhancing predictive maintenance, quality control, and machine automation. The growing adoption of Industry 4.0 practices drives manufacturers to deploy edge devices for low-latency operations and decentralized decision-making. Industrial automation systems integrated with edge computing reduce operational downtimes and optimize resource allocation. Edge-powered robotics and AI-driven inspection systems are improving production accuracy and efficiency. These advancements significantly contribute to the dominance of the manufacturing segment in the edge computing industry.

The healthcare segment is projected to have the highest growth rate from 2025 to 2033. The healthcare industry has become modern and digital; clinics and hospitals increasingly implement digital health strategies with varying degrees of success and maturity. Hospitals and clinics are adopting edge computing solutions across main use cases, including patient record management, continuous patient monitoring, remote patient care, and intervention to assist these strategies.

Organization Size Insights

Based on organization size, the large enterprises segment led the market, accounting for the largest revenue share of 67.5% in 2025. This dominance is primarily driven by the ability of edge computing to support high-volume, latency-sensitive applications critical to large organizations. Large enterprises increasingly deploy edge infrastructure to process massive datasets generated from IoT devices and smart systems locally, reducing dependency on centralized cloud environments. The scalability and customization offered by edge solutions allow these organizations to enhance operational efficiency and improve customer experience. Digital transformation accelerates the demand for robust, low-latency edge architectures, which continues to grow, reinforcing the large enterprise segment’s leadership in the market.

The small & medium enterprise segment is projected to have the highest growth rate from 2025 to 2033. This surge is driven by the increasing digital transformation initiatives across SMEs aiming to improve agility and enhance customer experience. Edge computing enables these organizations to process data locally and reduces dependency on centralized cloud infrastructure. The affordability and scalability of edge solutions have made them increasingly accessible to SMEs, empowering them to adopt technologies like IoT, AI, and real-time analytics without massive IT overhead. SMEs continue to modernize their operations; the edge computing industry is becoming a vital enabler of innovation.

Regional Insights

North America dominated the edge computing market, accounting for the largest revenue share of 36.7% in 2025. The convergence of IIoT with edge computing is forming favorable conditions for manufacturers in the U.S. to move toward connected factories. Several startups have also evolved to deliver platforms for developing edge-enabled solutions that are anticipated to boost market growth. The edge computing program has allowed developers to build, test, and analyze the efficacy of edge-enabled applications in a low-latency environment, supporting the continued demand for the edge computing industry.

U.S. Edge Computing Market Trends

The edge computing market in the U.S. held the largest share in the North America region in 2025, driven by a robust digital infrastructure and rapid adoption of next-generation technologies. Federal initiatives like the National Strategy to Secure 5G and investments in smart city projects are accelerating edge deployments nationwide. U.S.-based cloud and tech giants are investing heavily in distributed edge nodes, micro data centers, and AI-enabled edge platforms to support applications requiring real-time analytics and high data throughput. Strong government support, ongoing innovation, and a thriving startup ecosystem, the U.S. remains at the forefront of edge computing advancements globally.

Europe Edge Computing Market Trends

The edge computing market in Europe is expected to grow at a CAGR of over 31 % in 2024, owing to the proliferation of IoT, which has led to a significant surge in data. Various industries in the region, including IT & Telecom, healthcare, retail, transportation & logistics, energy & utilities, are creating lucrative opportunities for the market. The ongoing expansion of internet infrastructure across the region is expected to accelerate market growth further in the coming years.

The UK edge computing market growth is driven by the nation’s aggressive digital transformation initiatives and the proliferation of data-intensive technologies. The rapid rollout of 5G networks, particularly in urban centers, enables edge computing to support low-latency healthcare, manufacturing, and transportation applications. The involvement of tech giants and local startups and support from initiatives like the UK’s National AI Strategy mean the UK market is poised for sustained expansion.

The edge computing market in Germany is driven by the country’s strong industrial base and commitment to digital innovation. The country's emphasis on data sovereignty and compliance with GDPR also pushes enterprises to adopt localized edge solutions to ensure secure and regulated data processing. Increasing collaboration between German tech startups and global cloud providers fosters the development of scalable, low-latency edge platforms tailored to local enterprise needs. These factors position Germany as a key hub for the edge computing industry in Europe.

Asia Pacific Edge Computing Market Trends

The edge computing market in Asia Pacific has the highest CAGR of 39%, owing to the increasing focus on growing networking technology in the region. Technology trends, including IIoT, Industry 4.0, and the launch of 5G network services, along with bolstering the connected devices ecosystem, have generated a large amount of data, demanding a robust computational infrastructure. This is anticipated to present a lucrative opportunity for companies to expand their footprint across various developing nations.

China edge computing market is expected to grow in the coming years, driven by its national digitalization strategy and expansive 5G deployment. China's booming e-commerce, fintech, and online gaming sectors are generating massive volumes of data that require low-latency processing at the edge to maintain performance and user experience. Major Chinese tech firms are developing proprietary edge computing platforms integrated with AI, IoT, and cloud capabilities, further enhancing the ecosystem.

The edge computing market in India is experiencing robust growth, driven by rapid digitization, the rollout of 5G networks, and increasing demand for real-time data processing. The government’s Digital India initiative and smart city programs are accelerating the deployment of edge infrastructure, especially in tier-2 and tier-3 cities. India’s thriving startup ecosystem fosters innovation in edge AI and IoT applications, supported by cloud service providers offering scalable edge solutions tailored for small and medium enterprises. These factors are collectively propelling the edge computing industry.

Key Edge Computing Company Insights

Some key players operating in the market include Amazon Web Services, Inc., and Microsoft Corporation.

-

Amazon Web Services, Inc. (AWS) offers a comprehensive portfolio of edge computing solutions through AWS Wavelength, AWS Outposts, and AWS Greengrass. These services enable ultra-low latency applications by extending AWS infrastructure to telecom networks and local environments. AWS is widely adopted across sectors such as autonomous mobility, video streaming, and smart cities. With continuous hybrid and multi-access edge computing innovation, AWS remains a dominant force driving the global edge ecosystem.

-

Microsoft Corporation delivers robust edge computing capabilities through its Azure Stack Edge and Azure IoT platforms, allowing enterprises to process and analyze data close to the source. Microsoft's solutions support real-time decision-making, AI model deployment, and machine learning inference at the edge, especially for the manufacturing, healthcare, and logistics sectors. Microsoft invests in secure, scalable, and developer-friendly edge platforms in its hybrid cloud strategy.

Schneider Electric and Siemens are some of the emerging market participants.

-

Schneider Electric focuses on sustainable edge computing through its EcoStruxure Micro Data Centers and prefabricated edge solutions. Known for integrating power, cooling, and IT infrastructure into compact, remotely manageable systems, Schneider targets industries such as energy, utilities, and industrial automation. Its emphasis on green technologies and localized computing positions it as a leading emerging player in industrial and decentralized edge applications.

-

Siemens is expanding rapidly in the industrial edge market with its Industrial Edge platform, which enables real-time data processing and analytics on the factory floor. Siemens leverages its industrial automation and control systems strength to offer edge solutions that support predictive maintenance, quality assurance, and operational efficiency. The company’s integration of edge AI and IIoT (Industrial Internet of Things) places it at the forefront of Industry 4.0 adoption globally.

Key Edge Computing Companies:

The following are the leading companies in the edge computing market. These companies collectively hold the largest market share and dictate industry trends.

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Cisco Systems, Inc.

- Hewlett-Packard Enterprise Development

- Intel Corporation

- Huawei Technologies Co., Ltd.

- Schneider Electric

- Siemens

- General Electric Company

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Siemens AG, Google Nest, and Schneider Electric SE)

- Strengthen edge computing capabilities through strategic partnerships, acquisitions, and industry-focused solution development.

- Invest in edge servers, AI accelerators, and high-speed networking to support real-time, low-latency data processing.

- Extensive global reach, established enterprise relationships, and broad portfolios

- The capability to provide scalable edge computing solutions across distributed and edge environments

- Reliance on legacy infrastructure and large organizational structures can slow adoption of next-generation edge computing solutions and reduce operational agility.

Emerging Players (Assa Abloy AB and Philips Lighting B.V.)

- Develop specialized, cost-effective edge computing solutions for niche applications, including edge AI, industrial automation, and sector-specific deployments.

- Emphasize agility, customization, and rapid innovation to address evolving requirements for low-latency processing and real-time analytics.

- Faster development cycles enable quick adoption of emerging edge computing technologies and evolving deployment models.

- Flexible and customer-focused approaches help differentiate solutions in niche segments such as edge AI, industrial IoT, and industry-specific edge deployments.

- Limited financial resources and a smaller market presence can constrain large-scale expansion and infrastructure deployment.

- Lower brand recognition and a narrower enterprise customer base may hinder market penetration and customer acquisition.

Recent Developments

-

In April 2025, Google LLC announced significant upgrades to its Distributed Cloud Edge platform, integrating advanced Google AI models and Anthos features to streamline edge-native application deployment and orchestration. This initiative targets telecom providers by enabling low-latency, high-performance edge computing environments that support next-generation services like 5G, IoT, and real-time analytics. By enhancing automation and interoperability across hybrid and multi-cloud environments, Google strengthens its position in the market and supports the growing demand for scalable, AI-powered infrastructure solutions.

-

In March 2025, Intel unveiled its next-generation Meteor Lake processors, purpose-built to power edge inference workloads and enable real-time analytics in embedded and industrial environments. These processors combine low power consumption with advanced AI acceleration, making them ideal for predictive maintenance, smart manufacturing, and intelligent transportation systems. Enhancing local data processing capabilities at the edge, Intel reinforces its commitment to supporting scalable, high-performance edge computing infrastructure and meeting the evolving needs of Industry 4.0 and IoT-driven enterprises worldwide.

-

In February 2025, Microsoft expanded its edge computing strategy to support utilities navigating grid modernization, electrification, and distributed energy integration. The initiative focuses on hybrid architectures that connect Supervisory Control and Data Acquisition (SCADA), Energy Management Systems (EMS), and Distributed Energy Resource Management Systems (DERMS) with Microsoft Cloud services. Microsoft reinforces its role in modernizing critical infrastructure across Europe and North America by delivering resilient and secure edge solutions tailored for the energy sector.

Edge Computing Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 33.4 billion

Estimated market size in 2026

USD 46.7 billion

Projected market size by 2033

USD 328.0 billion

Growth rate

CAGR of 32.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, organization size, application, industry vertical, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Germany; UK; Germany, France; Italy; Spain; Russia; Nordic Region; China; Japan; India; Australia; ASEAN, Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

Amazon Web Services, Inc.; Microsoft Corporation; Google LLC; Cisco Systems, Inc.; Hewlett-Packard Enterprise Development; Intel Corporation; Huawei Technologies Co., Ltd.; Schneider Electric; Siemens; General Electric Company

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Edge Computing Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest technological trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global edge computing market report based on component, application, industry vertical, organization size, and region:

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Hardware

-

Hardware by Type

-

Edge Nodes/Gateways (Servers)

-

Sensors/Routers

-

Others

-

-

Hardware by End-Point Devices

-

Cameras

-

Drones

-

HMD

-

Robots

-

Others

-

-

-

Software

-

Services

-

Edge-Managed Platform

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Industrial Internet of Things (IIoT)

-

Remote Monitoring

-

Content Delivery

-

Video Analytics

-

AR/VR

-

Connected Cars

-

Smart Grids

-

Critical Infrastructure Monitoring

-

Traffic Management

-

Assets Tracking

-

Security & Surveillance

-

Smart Cities

-

Others

-

-

Organization Size Outlook (Revenue, USD Million, 2021 - 2033)

-

Small & Medium Enterprise

-

Large Enterprise

-

-

Industry Vertical Outlook (Revenue, USD Million, 2021 - 2033)

-

Industrial

-

Energy & Utilities

-

Healthcare

-

Agriculture

-

Transportation & Logistics

-

Retail

-

Data Centers

-

Wearables

-

Government & Public Sector

-

Media & Entertainment

-

Manufacturing

-

Telecom & IT

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

-

Latin America

-

Brazil

-

Mexico

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Component

Revenue capture definition

Hardware

Revenue is generated from physical infrastructure used in edge computing, including edge servers, gateways, routers, switches, sensors, and edge data center equipment. Monetization is driven by hardware sales, installation services, and infrastructure deployment for distributed computing environments.

Software

Revenue is derived from edge computing software solutions that enable data processing, workload orchestration, virtualization, analytics, and AI execution at the network edge. Monetization includes licensing, subscriptions, and integration services with cloud and IoT platforms.

Services

Revenue is generated from consulting, system integration, deployment, maintenance, and managed services supporting edge computing adoption. Monetization includes ongoing support, optimization, and cybersecurity services.

Edge-Managed Platform

Revenue is captured from centralized platforms that manage distributed edge environments, including device orchestration, workload management, monitoring, and automation. Monetization is based on subscription models and enterprise platform licensing.

Segment - Application

Revenue capture definition

Industrial Internet of Things (IIoT)

Revenue is generated from edge-enabled industrial automation solutions that support real-time monitoring, predictive maintenance, and machine connectivity in manufacturing environments.

Remote Monitoring

Revenue is derived from systems enabling real-time monitoring of assets, infrastructure, and operations across distributed locations using edge-enabled sensors and analytics.

Content Delivery

Revenue is generated from edge-based content distribution networks that reduce latency and improve streaming performance for digital content and media platforms.

Video Analytics

Revenue is captured from edge computing solutions used for real-time video processing, surveillance, object detection, and behavioral analysis powered by AI.

AR/VR

Revenue is generated from low-latency edge processing solutions that support augmented and virtual reality applications requiring high-speed data rendering and interaction.

Connected Cars

Revenue is derived from edge-enabled automotive systems supporting real-time communication, autonomous driving, and vehicle-to-everything (V2X) connectivity.

Smart Grids

Revenue is generated from intelligent energy systems that use edge computing for real-time monitoring, load balancing, and grid optimization.

Critical Infrastructure Monitoring

Revenue is captured from edge-based monitoring solutions for essential infrastructure such as power plants, water systems, and transportation networks.

Traffic Management

Revenue is generated from smart transportation systems that use edge computing for real-time traffic optimization, congestion management, and signal control.

Assets Tracking

Revenue is derived from real-time tracking solutions for logistics and industrial assets using edge-enabled sensors and analytics platforms.

Security & Surveillance

Revenue is generated from edge-based security systems including smart cameras, intrusion detection, and real-time threat analytics.

Smart Cities

Revenue is captured from integrated urban infrastructure solutions using edge computing for public safety, utilities, mobility, and environmental monitoring.

Others

Revenue is generated from emerging and niche applications of edge computing across various sectors not covered in core categories.

Segment - Organization Size

Revenue capture definition

Small & Medium Enterprise (SME)

Revenue is generated from SMEs adopting scalable edge computing solutions to improve efficiency, reduce latency, and enable cost-effective digital transformation.

Large Enterprise

Revenue is derived from large enterprises deploying advanced edge infrastructure for mission-critical operations, global scalability, and high-performance analytics.

Segment - Industry Vertical

Revenue capture definition

Industrial

Revenue is generated from edge computing applications in industrial automation, robotics, and real-time production monitoring systems.

Energy & Utilities

Revenue is derived from smart grid management, energy optimization, and infrastructure monitoring solutions powered by edge computing.

Healthcare

Revenue is generated from real-time patient monitoring, diagnostics, and connected medical devices using edge-enabled systems.

Agriculture

Revenue is captured from precision farming solutions including IoT-based crop monitoring, irrigation control, and agricultural analytics.

Transportation & Logistics

Revenue is generated from fleet tracking, route optimization, and supply chain visibility enabled by edge computing platforms.

Retail

Revenue is derived from in-store analytics, customer behavior tracking, and inventory optimization systems using edge intelligence.

Data Centers

Revenue is generated from distributed edge data center infrastructure supporting low-latency computing and hybrid cloud environments.

Wearables

Revenue is captured from edge-enabled wearable devices used for health monitoring, fitness tracking, and real-time data processing.

Government & Public Sector

Revenue is derived from smart governance, public safety systems, and infrastructure monitoring solutions powered by edge computing.

Media & Entertainment

Revenue is generated from low-latency streaming, gaming, and immersive content delivery using edge computing infrastructure.

Manufacturing

Revenue is captured from smart factory solutions, predictive maintenance, and industrial IoT deployments.

Telecom & IT

Revenue is derived from 5G-enabled edge infrastructure, network optimization, and cloud-edge integration services.

Others

Revenue is generated from emerging applications across finance, education, defense, and other niche sectors.

Estimation Model

Digital Infrastructure Layer

Automation Readiness Layer Solution Adoption Layer Monetisation Layer Where can edge computing be deployed??

Which organizations can deploy edge computing solutions? Which organizations adopt edge computing use cases? How much revenue is generated? Identify data-intensive sites that benefit from local processing, including manufacturing plants, warehouses, retail stores, hospitals, telecom sites, utilities, transportation hubs, smart buildings, and remote industrial assets. This layer defines the Total Addressable Market (TAM) based on the total deployment footprint.

Filter the addressable base using connectivity, IT maturity, cloud integration, cybersecurity readiness, and operational requirements. Organizations must have workloads that require low latency, real-time analytics, or local data processing. This defines the Serviceable Available Market (SAM). Apply industry-specific adoption rates across use cases such as industrial automation, AI inference, computer vision, predictive maintenance, smart retail, healthcare analytics, and telecom edge services. This identifies active deployments within the Serviceable Obtainable Market (SOM). Estimate annual spending per deployment across edge hardware, software, and services, including servers, gateways, edge platforms, cybersecurity, integration, and managed services. Multiply spending by active deployments to calculate total market revenue. Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Edge Computing Adoption & Digital Infrastructure Trends

Conducted a focused assessment of edge computing adoption across manufacturing, telecommunications, healthcare, retail, and smart city ecosystems, covering distributed computing architectures, real-time data processing needs, latency-sensitive applications, and integration with cloud and IoT environments.

Helps stakeholders identify high-growth edge deployment segments, evaluate infrastructure modernization needs, and assess opportunities driven by low-latency computing and real-time analytics demand.

Edge Computing Adoption & Digital Infrastructure Trends

Conducted a focused assessment of edge computing adoption across manufacturing, telecommunications, healthcare, retail, and smart city ecosystems, covering distributed computing architectures, real-time data processing needs, latency-sensitive applications, and integration with cloud and IoT environments.

Helps stakeholders identify high-growth edge deployment segments, evaluate infrastructure modernization needs, and assess opportunities driven by low-latency computing and real-time analytics demand.

Edge Computing Adoption & Digital Infrastructure Trends

Conducted a focused assessment of edge computing adoption across manufacturing, telecommunications, healthcare, retail, and smart city ecosystems, covering distributed computing architectures, real-time data processing needs, latency-sensitive applications, and integration with cloud and IoT environments.

Helps stakeholders identify high-growth edge deployment segments, evaluate infrastructure modernization needs, and assess opportunities driven by low-latency computing and real-time analytics demand.

Frequently Asked Questions About This Report

The global edge computing market size was estimated at USD 333.4 billion in 2025 and is expected to reach USD 46.7 billion by 2026.

The global edge computing market is expected to grow at a compound annual growth rate of 32.1% from 2026 to 2033, reaching USD 328.0 billion by 2033.

The manufacturing segment led the market with the largest revenue share of 20.1% in 2025, while the healthcare segment is the fastest-growing.

Key players operating in the edge computing market include Amazon Web Services, Inc.; Microsoft Corporation; Google LLC; Cisco Systems, Inc.; Hewlett-Packard Enterprise Development; Intel Corporation; Huawei Technologies Co., Ltd.; Schneider Electric; Siemens; General Electric Company

Key factors that are driving the market growth include the rising demand for low-latency processing and real-time decision-making in edge computing, the increasing adoption of IoT and connected devices across industries, and the growing need for decentralized data infrastructure to reduce cloud dependency.

The hardware segment accounted for the largest revenue share of 41.8% in 2025, while the software segment is the fastest-growing.

The Industrial Internet of Things (IIoT) segment dominated with a revenue share of 22.7% in 2025, while AR/VR is the fastest-growing area.

The large enterprise held the largest revenue share of 67.5% in 2025, while the small & medium enterprise is the fastest-growing model.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.