- Home

- »

- Next Generation Technologies

- »

-

Data Center Construction Market Size Report, 2026-2033GVR Report cover

![Data Center Construction Market (2026 - 2033)Report]()

Data Center Construction Market (2026 - 2033)

Size, Share & Trends Analysis Report By Infrastructure (IT Infrastructure, PD And Cooling Infrastructure, Miscellaneous Infrastructure), By Tier, By End Use (IT & Telecom, BFSI), By Region, And Segment Forecasts

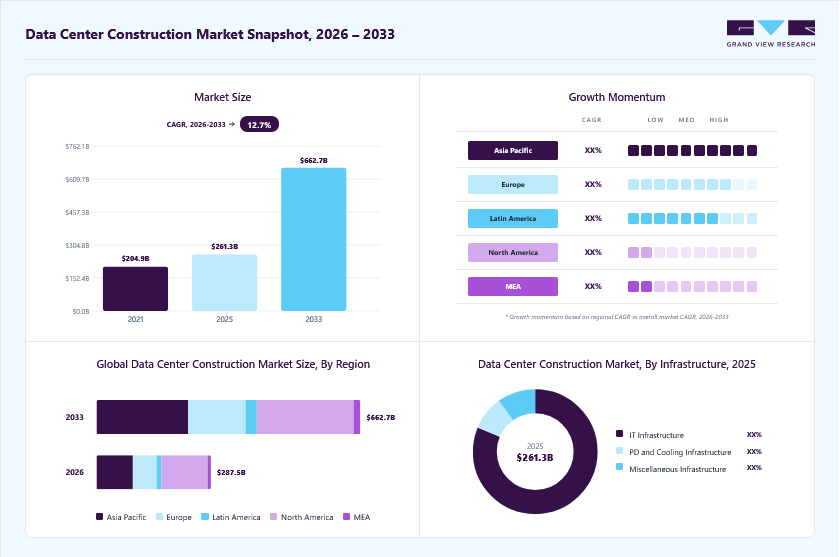

Market Size, 2025

$261.3BMarket Estimate, 2026

$287.5BMarket Forecast, 2033

$662.7BCAGR, 2026–2033

12.7%Data Center Construction Market Summary

The global data center construction market size was valued at USD 261.3 billion in 2025 and is projected to grow from USD 287.5 billion in 2026 to USD 662.7 billion by 2033, at a CAGR of 12.7% from 2026 to 2033. The market in North America dominated with a revenue share of 40.9% in 2025. Organizations across industries are increasingly adopting hybrid and multi-cloud environments to enhance scalability, resilience, and operational efficiency.

Key Market Trends & Insights

- By infrastructure: IT infrastructure segment dominated the market and accounted for a revenue share of 81.2% in 2025.

- By type: Tier 3 segment dominated the market and accounted for the largest revenue share in 2025.

- By end-use: IT & telecom segment dominated the market and accounted for the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (40.9% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 261.3 Billion

- Estimated market size in 2026: USD 287.5 Billion

- Projected market size by 2033: USD 662.7 Billion

- CAGR (2026-2033): 12.7%

This shift requires new hyperscale and edge facilities that can support high workloads, real-time analytics, and low-latency applications. The exponential increase in data generated from streaming platforms, social media, connected devices, and enterprise applications is driving the need for expanded data center capacity. Moreover, the rise of artificial intelligence (AI), machine learning (ML), and generative AI models is significantly increasing compute requirements, particularly for GPU-powered facilities. These workloads necessitate high-performance computing (HPC) infrastructure, specialized chipsets, and enhanced power and cooling capabilities, thereby stimulating new construction and retrofitting of existing facilities.")

The global rollout of 5G networks is accelerating the deployment of edge data centers closer to end users. Industries such as autonomous vehicles, smart cities, telemedicine, and industrial automation require ultra-low latency and real-time processing, which traditional centralized data centers cannot efficiently provide. This shift toward distributed computing architectures is fueling investments in smaller, modular, and geographically dispersed data centers.

Major cloud service providers, including Amazon Web Services (AWS), Microsoft Azure, Google Cloud, and Meta, are aggressively expanding their global footprint through large-scale data center campuses. In parallel, colocation providers are investing heavily in new facilities to cater to enterprises that prefer outsourced infrastructure. This dual expansion by hyperscalers and colocation firms is a structural driver of sustained construction activity in the sector. For instance, in June 2025, Amazon announced plans to invest about USD 13 billion (AUD 20 billion) from 2025 to 2029 to expand, operate and maintain its data center infrastructure across Australia, marking a global technology investment and aiming to support surging demand for cloud computing and artificial intelligence (AI) services, accelerate AI adoption and help modernize organizations of all sizes while also investing in renewable energy projects like three new solar farms to power the expanded facilities.

Infrastructure Insights

The IT infrastructure segment dominated the market and accounted for a revenue share of 81.2% in 2025, driven by the modernization of hardware stacks and the shift toward software-defined, automated, and highly resilient architectures that can support increasingly complex enterprise workloads. Organizations are replacing legacy equipment with high-density servers, advanced storage systems, and next-generation networking components to improve performance, energy efficiency, and total cost of ownership. The adoption of virtualization, containerization, and infrastructure-as-code is also pushing developers to design facilities that can accommodate flexible, scalable, and modular IT environments rather than static deployments.

The miscellaneous infrastructure segment is anticipated to grow at the fastest CAGR during the forecast period owing to the increasing emphasis on operational reliability, site resiliency, and compliance-driven facility upgrades that extend beyond core IT systems. Developers are investing more in auxiliary components such as security systems, access controls, fire suppression, advanced monitoring, structural enhancements, and site utilities to ensure uninterrupted operations and regulatory adherence

Tier Insights

The tier 3 segment dominated the market and accounted for the largest revenue share in 2025, driven by the enterprises and mid-sized organizations prioritizing a balanced model between reliability, cost efficiency, and operational flexibility. Tier 3 facilities, with their concurrently maintainable design, allow maintenance and upgrades without shutting down operations, making them particularly attractive for industries such as BFSI, healthcare, government, and managed service providers that require high availability but do not need the extreme redundancy and expense of Tier 4.

The tier 4 segment is expected to grow at a significant CAGR during the forecast period, driven by rising demand for mission-critical reliability, zero downtime, and fault-tolerant operations among industries where service interruption carries severe financial, regulatory, or safety consequences. Financial services, healthcare, government, and large-scale digital enterprises are increasingly prioritizing facilities with fully redundant power, cooling, and network paths to ensure continuous operations even during system failures or external disruptions.

End Use Insights

The IT & telecom segment dominated the market and accounted for the largest revenue share in 2025, driven by the rapid modernization of carrier networks and enterprise connectivity infrastructure as operator’s transition from legacy architectures to cloud-native, open, and software-defined networks. Telecom providers are expanding core and metro data facilities to support rising bandwidth consumption from streaming, OTT services, enterprise VPNs, and private networks, while also strengthening redundancy and reliability to meet stringent service-level agreements (SLAs).

The BFSI segment is expected to grow at a significant CAGR over the forecast period, driven by the rising need for secure, compliant, and highly resilient digital financial infrastructure to support real-time transactions, risk analytics, and regulatory reporting. Banks, insurance firms, and fintech players are increasingly investing in mission-critical facilities with built-in redundancy, disaster recovery capabilities, and advanced cybersecurity controls to minimize downtime and protect sensitive financial data. The growing adoption of digital banking, open banking frameworks, instant payment systems, and fraud detection platforms is further intensifying demand for reliable backend computing environments with stringent uptime and latency requirements.

Regional Insights

North America data center construction market dominated globally with the largest revenue share of 40.9% in 2025, driven by large-scale enterprise modernization and the concentration of global technology ecosystems, which require continuously upgraded computing facilities. A strong presence of cloud-native companies, digital platforms, and advanced research institutions is sustaining demand for high-performance data infrastructure, particularly in secondary and tertiary cities where land and power costs are comparatively lower.

U.S. Data Center Construction Industry Trends

The data center construction market in the U.S. is expected to grow significantly at a CAGR of 11.0% from 2026 to 2033, due to massive private capital inflows into hyperscale campuses and purpose-built facilities aligned with advanced chip manufacturing clusters.

Europe Data Center Construction Industry Trends

The data center construction market in Europe is anticipated to register considerable growth from 2026 to 2033 due to a strategic shift toward regional digital autonomy and secure domestic infrastructure. Governments and enterprises are prioritizing locally controlled digital ecosystems, encouraging investment in Pan-European data center corridors that connect multiple countries.

The UK data center construction industry is expected to grow rapidly in the coming years, owing to the rising demand from public sector digitization, digital services, and content delivery networks is reinforcing investment in both new builds and brownfield upgrades.

The Germany data center construction industry held a substantial market share in 2025 due to strong industrial base and the digitalization of manufacturing, automotive, and engineering sectors. Cities such as Frankfurt are expanding as critical European interconnection hubs, attracting international operators.

Asia Pacific Data Center Construction Industry Trends

Asia Pacific data center construction market held a significant share in the global market in 2025, due to the rapid urban digitization, rising internet penetration, and the emergence of regional digital economies across Southeast Asia, India, and Oceania. The need to support fast-growing e-services, government digital platforms, and regional cloud hubs is prompting investment in both large-scale and modular facilities.

The Japan data center construction industry is expected to grow rapidly in the coming years, driven by enterprise digital resilience and disaster preparedness, given the country’s exposure to natural risks. Corporations are prioritizing highly reliable, earthquake-resistant facilities with advanced power backup systems.

The China data center construction industry held a substantial market share in 2025, due to state-led digital infrastructure initiatives and the development of national computing hubs in designated zones.

Key Data Center Construction Company Insights

Key players operating in the data center construction industry are Acer Inc., Cisco Systems Inc., Inc., Dell Inc., IPXON Networks, Fujitsu, and HostDime Global Corp. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In December 2025, ABB announced an agreement to acquire IPEC, a UK-based technology firm specializing in intelligent monitoring solutions for critical electrical infrastructure, in a move aimed at strengthening ABB’s digital power management capabilities. The acquisition will integrate IPEC’s AI-driven, real-time analytics platform which continuously monitors high-voltage assets and predicts equipment failures into ABB’s portfolio to help data centers, healthcare providers, utilities, and industrial manufacturers reduce outage risks, improve reliability, and prevent potentially multi-million-dollar operational losses.

-

In April 2025, Fujitsu announced a joint initiative with Supermicro and Nidec aimed at reducing data center energy consumption through more efficient cooling technologies. Under the collaboration, Fujitsu aims to contribute its liquid-cooling monitoring and control software, Supermicro supplies high-performance GPU server platforms, and Nidec provides its advanced liquid-cooling systems to co-develop a new service designed to lower power usage effectiveness (PUE) and help operators run more sustainable, cost-efficient data centers.

-

In February 2025, Cisco Systems Inc. announced an expanded strategic collaboration with NVIDIA to deliver integrated AI infrastructure solutions for enterprise customers, as companies increasingly view artificial intelligence as a core growth driver while still grappling with the technical, operational, and security challenges of modern AI-ready data centers. The strengthened partnership aims to combine Cisco’s networking and data center technologies with NVIDIA’s AI computing platforms to enable high-performance, low-latency, and energy-efficient connectivity across on-premises data centers, cloud environments, and end users, giving organizations greater flexibility in deploying and scaling AI workloads.

Key Data Center Construction Companies:

The following key companies have been profiled for this study on the data center construction market.

- ABB

- Acer Inc.

- Ascenty

- Cisco Systems, Inc.

- Dell Inc.

- Equinix, Inc.

- Fujitsu

- Gensler

- Hewlett Packard Enterprise Development LP

- Hitachi, Ltd.

- HostDime Global Corp.

- Huawei Technologies Co., Ltd.

- IBM Corporation

- INSPUR Co., Ltd.

- IPXON Networks

- KIO

- Lenovo

- Oracle

- Schneider Electric

- Vertiv Group Corp.

Data Center Construction Market Report Scope

Report Attribute

Details

Market size in 2025

USD 261.3 billion

Estimated market size in 2026

USD 287.5 billion

Projected market size by 2033

USD 662.7 billion

Growth rate

CAGR of 12.7% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report enterprise size

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Infrastructure, tier, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

ABB; Acer Inc.; Ascenty; Cisco Systems, Inc.; Dell Inc.; Equinix, Inc.; Fujitsu; Gensler; Hewlett Packard Enterprise Development LP; Hitachi, Ltd.; HostDime Global Corp.; Huawei Technologies Co., Ltd.; IBM Corporation; INSPUR Co., Ltd.; IPXON Networks; KIO; Lenovo; Oracle; Schneider Electric; Vertiv Group Corp.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Data Center Construction Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the data center construction market report based on infrastructure, tier, end use, and region.

-

Infrastructure Outlook (Revenue, USD Billion, 2021 - 2033)

-

IT Infrastructure

-

Networking Equipment

-

Server

-

Storage

-

-

PD and Cooling Infrastructure

-

Power Distribution

-

Cooling

-

Air

-

Computer Room Air Conditioners (CRAC)

-

Computer Room Air Handlers (CRAH)

-

Rear Door Heat Exchangers

-

Others

-

-

Liquid

-

Direct-to-Chip Liquid Cooling

-

Immersion Cooling

-

Rear Door Heat Exchanger with Liquid

-

-

-

Others

-

-

Miscellaneous Infrastructure

-

-

Tier Outlook (Revenue, USD Billion, 2021 - 2033)

-

Tier 1

-

Tier 2

-

Tier 3

-

Tier 4

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

IT & Telecom

-

BFSI

-

Government & Defense

-

Healthcare

-

Energy

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

Some key players operating in the data center construction market include ABB, Acer Inc., Ascenty, Cisco Systems, Inc., Dell Inc., Equinix, Inc., Fujitsu, Gensler, Hewlett Packard Enterprise Development LP, Hitachi, Ltd., HostDime Global Corp., Huawei Technologies Co., Ltd., IBM, INSPUR Co., Ltd., IPXON Networks, KIO, Lenovo, Oracle, Schneider Electric, Vertiv Group Corp.

Key factors that are driving the data center construction market growth include the rapid expansion of cloud computing, the proliferation of big data, and the increased adoption of artificial intelligence (AI) and Internet of Things (IoT) devices. Enterprises are increasingly relying on cloud service providers (CSPs) and colocation data centers to manage large volumes of data, necessitating the construction of new, high-capacity facilities

North America dominated with a 40.9% revenue share in 2025.

Tier 3 held the largest revenue share in 2025.

Tray segment held the largest share in 2025.

The global data center construction market size was estimated at USD 261.3 billion in 2025 and is expected to reach USD 287.5 billion in 2026.

The global data center construction market is expected to grow at a compound annual growth rate of 12.7% from 2026 to 2033 to reach USD 662.7 billion by 2033.

The IT infrastructure segment dominated the market and accounted for the revenue share of 81.2% in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.