- Home

- »

- IT Services & Applications

- »

-

Data Encryption Market Size And Share Report, 2026-2033GVR Report cover

![Data Encryption Market (2026 - 2033)Report]()

Data Encryption Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Solutions, Services), By Deployment (On-Premises, Cloud), By Type, By Organization Size, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$15.2BMarket Estimate, 2026

$16.9BMarket Forecast, 2033

$37.2BCAGR, 2026–2033

11.9%Data Encryption Market Summary

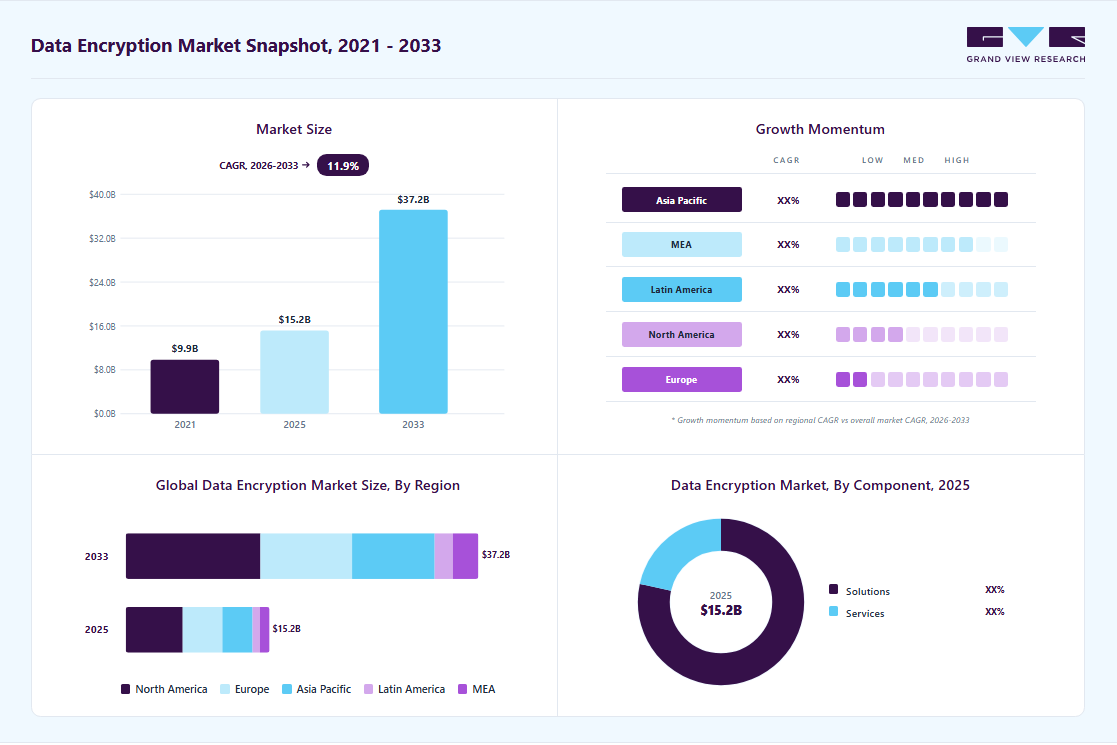

The global data encryption market size was valued at USD 15.2 billion in 2025 and is projected to grow from USD 16.9 billion in 2026 to USD 37.2 billion by 2033, at a CAGR of 11.9% from 2026 to 2033. The market in North America dominated with a revenue share of 39.6% in 2025. The global market is witnessing strong, sustained growth, driven by the rapid expansion of digital ecosystems, rising cyberattacks, and tightening data protection regulations worldwide.

Key Market Trends & Insights

- By component: Solutions segment held the largest market share of 78.4% in 2025.

- By deployment: Cloud segment held the largest market share in 2025.

- By type: Symmetric encryption segment held the largest market share in 2025.

- By organization size: Large enterprises segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (39.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 15.2 Billion

- Estimated market size in 2026: USD 16.9 Billion

- Projected market size by 2033: USD 37.2 Billion

- CAGR (2026-2033): 11.9%

Key players across industries are prioritizing encryption as a foundational layer of cybersecurity to secure sensitive data across storage, transmission, and cloud environments. Also, the shift toward cloud computing, remote work, and hybrid IT infrastructure has significantly increased the need for scalable, integrated encryption solutions.")

A key trend shaping the market is the accelerated adoption of cloud-based encryption solutions, particularly within public and hybrid cloud environments. Enterprises are increasingly relying on built-in encryption capabilities offered by hyperscalers, such as key management services and platform-native encryption tools. This transition is reducing dependence on traditional on-premises encryption deployments while driving higher demand for API-driven, automated, and policy-based encryption mechanisms that align with cloud-native architectures.

Another major trend is the rising importance of regulatory compliance and data privacy frameworks. Regulations such as GDPR, HIPAA, and sector-specific mandates in BFSI and healthcare are compelling organizations to implement robust encryption strategies. At the same time, increasing awareness around data sovereignty is pushing enterprises and governments to ensure that sensitive data remains protected regardless of geographic location or infrastructure type.

The market is also shifting toward integrating advanced encryption into broader data security ecosystems, including data discovery, classification, and security posture management. Encryption is no longer viewed as a standalone tool but as part of an integrated data protection strategy. Emerging technologies such as quantum-resistant encryption, zero-trust architectures, and AI-driven security analytics are further enhancing encryption capabilities and shaping next-generation solutions.

Regionally, North America continues to dominate the market due to early technology adoption and strong cybersecurity infrastructure, while Asia Pacific is emerging as the fastest-growing region driven by rapid digital transformation and cloud adoption. Consequently, the data encryption industry is evolving from traditional point solutions to embedded, intelligent, and cloud-native security frameworks, making encryption a critical enabler of enterprise digital trust and resilience.

Market Dynamics

One of the major drivers of the data encryption industry is the growing need to protect sensitive enterprise data across cloud, hybrid, and AI-driven environments. Organizations are increasingly facing cybersecurity threats, ransomware attacks, data breaches, and stricter regulatory requirements related to data privacy and compliance. As businesses continue to adopt cloud computing, artificial intelligence, and digital transformation strategies, the demand for advanced encryption technologies, centralized key management, and secure data processing solutions is rising significantly across industries such as BFSI, healthcare, government, and telecommunications.

For instance, in October 2025, NTT DATA partnered with Fortanix to launch a Cryptography-as-a-Service solution focused on securing AI, multicloud, and hybrid environments while preparing enterprises for post-quantum cybersecurity risks. The solution provides confidential computing, unified encryption management, and quantum-safe security capabilities for regulated industries. This development highlights how enterprises are increasingly investing in advanced encryption technologies to strengthen data security, ensure compliance, and prepare for future cyber threats, thereby supporting the market growth.

One of the key constraints in the data encryption industry is the performance slowdown caused by encryption processes in high-volume, real-time data environments. Advanced encryption methods can increase processing overhead, resulting in higher latency, slower application performance, and reduced system efficiency, particularly in industries that handle large-scale transactional or real-time workloads, such as BFSI, healthcare, telecommunications, and e-commerce. Organizations managing AI workloads, cloud applications, and big data analytics often face concerns regarding processing speed and user experience when implementing full-scale encryption across networks, databases, and storage systems.

The issue becomes more significant in multi-cloud and edge computing environments where encrypted data must be continuously processed, transferred, and accessed in real time. As a result, some enterprises limit encryption deployment to selected workloads or sensitive datasets rather than implementing it enterprise-wide, hindering broader adoption of advanced data encryption solutions.

Market Concentration & Characteristics

The data encryption industry is experiencing strong growth driven by the increasing need to secure sensitive enterprise data across cloud, hybrid, and AI-driven environments. Rising cybersecurity threats, accelerating digital transformation initiatives, and expanding regulatory requirements for data privacy are driving organizations to adopt advanced encryption solutions. The market is moderately fragmented, with the presence of several global cybersecurity companies, cloud service providers, and specialized encryption vendors competing across software, hardware, and cloud-based encryption offerings. At the same time, strategic partnerships, product innovations, and acquisitions are gradually increasing market consolidation.

The market is characterized by high technological innovation, particularly in quantum-safe encryption, confidential computing, AI-driven security, and centralized key management. Regulatory frameworks, including GDPR, HIPAA, PCI-DSS, and regional data protection laws, play a major role in influencing enterprise investments in encryption technologies. Merger and acquisition activity is also increasing as companies aim to strengthen their cybersecurity portfolios and expand cloud security capabilities. In addition, demand remains highly concentrated among industries handling critical and sensitive data, including BFSI, healthcare, government, telecommunications, and large enterprises, while substitution risk remains moderate due to the growing preference for integrated cloud-native security solutions.

Component Insights

The solutions segment led the market with the largest revenue share of 78.4% in 2025 and is projected to grow at the fastest CAGR during the forecast period, primarily due to the widespread enterprise preference for integrated encryption platforms such as key management systems (KMS), hardware security modules (HSMs), and cloud-native encryption tools that provide end-to-end data protection across storage, applications, and networks. This dominance is further driven by rapid cloud adoption and the need for scalable, automated encryption solutions that reduce operational complexity while ensuring compliance with global data protection regulations.

In addition, organizations are increasingly shifting toward platform-based security architectures where encryption is embedded directly into cloud services and enterprise applications rather than deployed as standalone tools. For instance, in March 2026, Netlib Security announced the Encryptionizer Winter 2026 release, along with an upgraded Enterprise Key Management (EKM) system that enhances automated encryption workflows, centralized key control, and cloud-native integration capabilities to support enterprise-scale data protection demands. Such advancements highlight the growing demand for solution-centric encryption ecosystems, reinforcing the dominance of the solutions segment, which continues to expand as enterprises prioritize unified, scalable, and compliance-ready encryption frameworks.

The services segment is expected to grow at a significant CAGR from 2026 to 2033, driven by the increasing complexity of encryption deployments across hybrid and multi-cloud environments and the rising need for specialized expertise in managing cryptographic infrastructure. As enterprises scale their digital operations, they are finding it challenging to manage key lifecycle processes, compliance requirements, and the integration of encryption across diverse IT systems, driving a greater reliance on external service providers. Moreover, the shortage of skilled cybersecurity professionals is further accelerating the shift toward outsourced encryption support models, including consulting, deployment, managed security, and maintenance services.

Another key factor is the growing adoption of advanced encryption frameworks that require continuous configuration, monitoring, and updates to remain compliant with evolving global data protection regulations. Organizations are increasingly prioritizing operational efficiency and risk reduction, leading them to adopt managed encryption services rather than building in-house capabilities. Furthermore, the expansion of cloud-native architectures and zero-trust security models is reinforcing demand for services that can seamlessly integrate encryption across distributed environments. Overall, the services segment is gaining momentum as enterprises seek scalable, cost-effective, and expertise-driven solutions to manage encryption complexity, making it the fastest-growing component of the global market over the forecast period.

Deployment Insights

The cloud segment accounted for the largest market revenue share in 2025 and is projected to grow at the fastest CAGR during the forecast period, due to the rapid migration of enterprise workloads to cloud environments, where organizations increasingly require scalable, automated, and seamlessly integrated encryption solutions to protect data across distributed and dynamic infrastructures. Enterprises prioritize cloud-based encryption because it simplifies deployment, reduces infrastructure overhead, and enables consistent protection across storage, applications, and network layers within hybrid and multi-cloud ecosystems.

In addition, rising regulatory pressures and growing concerns around data sovereignty are compelling organizations to adopt advanced cloud encryption capabilities, including centralized key management and policy-driven security controls, to ensure compliance and mitigate data breach risks across jurisdictions. A key development reinforcing this trend is the growing focus on customer-controlled encryption models that enhance data ownership and transparency into security on cloud platforms. For instance, in March 2026, Zilliz introduced Customer-Managed Encryption Keys (CMEK) on Zilliz Cloud, enabling enterprises to retain full control over encryption keys while securing sensitive AI and vector data workloads in cloud environments. Subsequently, the dominance of the cloud segment is driven by its scalability, regulatory alignment, and continuous innovation in cloud-native encryption capabilities, making it the preferred deployment model for modern data security strategies.

The on-premises segment is expected to grow at a significant CAGR from 2026 to 2033, due to the continued reliance of highly regulated industries on in-house data control and security infrastructure, where organizations prioritize direct ownership of encryption systems to ensure maximum data sovereignty and compliance with strict regulatory frameworks. Enterprises in sectors such as BFSI, government, and defense prefer on-premises encryption solutions as they offer greater control over sensitive data, reduced exposure to external cloud risks, and the ability to enforce customized security policies within closed IT environments.

In addition, concerns around data privacy, geopolitical restrictions, and data residency requirements are further sustaining demand for on-premises deployments, particularly in regions with stringent cybersecurity regulations. Moreover, many large enterprises continue to operate legacy IT systems and hybrid infrastructures, where on-premises encryption remains deeply embedded, and it is difficult to fully migrate to the cloud in the short term. In conclusion, despite the rapid shift toward cloud adoption, the on-premises segment is expected to maintain steady growth as organizations balance modernization with security control and regulatory compliance requirements.

Type Insights

The symmetric encryption segment accounted for the largest market share in 2025, driven by its high processing efficiency, lower computational complexity, and ability to securely encrypt large volumes of data with minimal latency, making it ideal for enterprise-scale workloads such as databases, storage systems, and cloud environments. It is also widely adopted as the default encryption method across operating systems, enterprise applications, and cloud platforms due to its strong performance and ease of integration into existing IT infrastructures. In addition, its widespread use in securing data at rest and in transit across regulated industries such as BFSI, healthcare, and government further strengthens its dominant position in the market.

Another key factor reinforcing its dominance is the increasing focus on high-performance, scalable encryption solutions that can support growing data volumes without compromising system efficiency. For instance, in December 2023, Fortinet partnered with Arqit and BT to launch a quantum-safe VPN solution, highlighting the continued importance of robust symmetric encryption mechanisms in ensuring secure, high-speed data transmission across enterprise networks. Overall, the dominance of symmetric encryption is driven by its optimal balance of security, performance, and scalability, making it the most widely deployed encryption type in the global market.

The asymmetric encryption segment is projected to witness at the fastest CAGR during the forecast period due to the increasing adoption of secure key exchange mechanisms and digital identity verification systems that are essential for enabling secure communications in cloud-first and zero-trust security environments. It is gaining strong traction as organizations expand their use of public key infrastructure (PKI), digital signatures, and certificate-based authentication to ensure secure data exchange across distributed networks. In addition, the rapid growth of e-commerce, online banking, and API-driven ecosystems is accelerating demand for asymmetric encryption, as it plays a critical role in establishing trust and securing communications over untrusted networks.

Moreover, the rising need for enhanced cybersecurity resilience against evolving threats, where asymmetric encryption provides stronger authentication and non-repudiation capabilities compared to traditional methods. The increasing integration of asymmetric encryption into blockchain technologies, secure messaging platforms, and cloud-native security frameworks is further supporting its adoption. Thus, the strong alignment of asymmetric encryption with modern digital trust requirements, combined with its expanding role in authentication-heavy and cloud-based environments, is driving its position as the fastest-growing encryption type in the global market over the forecast period.

Organization Size Insights

The large enterprises segment accounted for the largest market revenue share in 2025, driven by the high volume of sensitive data generated across complex and distributed IT environments, which necessitates robust encryption frameworks to ensure data confidentiality, integrity, and regulatory compliance. These organizations have the financial capability and operational maturity to deploy advanced encryption solutions, including enterprise-grade key management systems, hardware security modules, and end-to-end encryption platforms, across cloud, on-premises, and hybrid infrastructures. In addition, stringent global data protection regulations and rising cyber threats targeting large-scale enterprises are compelling them to adopt comprehensive encryption strategies as a core component of their cybersecurity posture.

Another key driver is the growing shift toward cloud transformation and digital modernization initiatives, which require scalable, integrated encryption capabilities to secure multi-environment workloads and sensitive enterprise data. For instance, in February 2023, EnterpriseDB introduced Transparent Data Encryption (TDE) for PostgreSQL, strengthening enterprise database security and compliance by enabling seamless encryption of data at rest without application-level changes. In conclusion, the dominance of large enterprises in the global market is supported by their higher security requirements, regulatory obligations, and continuous investment in advanced encryption technologies to protect mission-critical data assets.

The small & medium-sized enterprises (SMEs) segment is expected to grow at the fastest CAGR from 2026 to 2033, primarily driven by the rapid adoption of digital payment systems, cloud-based business operations, and increasing reliance on online platforms for customer engagement and transactions. As SMEs expand their digital footprint, they are handling growing volumes of sensitive financial and customer data, accelerating the need for affordable, scalable encryption solutions to ensure data protection, regulatory compliance, and customer trust. In addition, the availability of cloud-based encryption services and security-as-a-service models is enabling SMEs to adopt advanced data protection capabilities without heavy infrastructure investments or dedicated cybersecurity teams. Further, the rising awareness of cybersecurity threats and the operational impact of data breaches on small businesses, which are increasingly becoming targets for cyberattacks due to relatively weaker security postures. This is pushing SMEs to prioritize encryption as a foundational security layer to safeguard business continuity and brand reputation.

Furthermore, the ongoing digital transformation of SMEs across emerging and developed markets is reinforcing the need for secure digital ecosystems, including encrypted payment systems, secure communications, and protected cloud storage environments. For instance, in June 2025, a Mastercard survey highlighted that digital payments are becoming essential for the growth and survival of SMEs in Latin America, with businesses increasingly relying on secure digital transaction ecosystems to improve efficiency and competitiveness. Overall, the combination of digital adoption, cybersecurity risk exposure, and improved access to cost-effective encryption solutions is driving strong growth in the SME segment of the global market.

End Use Insights

The BFSI segment accounted for the largest market revenue share in 2025, due to the extremely high volume of sensitive financial data it handles, including customer identities, transaction records, payment credentials, and banking operations that require strong encryption to ensure confidentiality, integrity, and regulatory compliance. Financial institutions operate under stringent global regulations, such as PCI-DSS, GDPR, and Basel guidelines, that mandate robust encryption across digital banking platforms, core banking systems, and payment infrastructure. In addition, the rapid digitization of financial services, including mobile banking, online transactions, and fintech-driven ecosystems, has significantly increased the need for end-to-end encryption across cloud and hybrid environments.

In addition, the rising sophistication of cyberattacks targeting the financial sector is making encryption a critical layer of defense against data breaches, fraud, and unauthorized access to sensitive systems. Furthermore, BFSI organizations are increasingly investing in advanced, customized encryption solutions to ensure greater control, data sovereignty, and security across global operations. For instance, in October 2022, Saxo Bank partnered with Baffle to deploy a global customized data encryption solution, enhancing its ability to secure sensitive financial data while maintaining compliance and operational control. Overall, the BFSI segment continues to dominate the global market due to its high security requirements, regulatory pressure, and continuous adoption of advanced encryption technologies to protect critical financial ecosystems.

The retail & e-commerce segment is expected to grow at the fastest CAGR during the forecast period, driven by the rapid expansion of online shopping platforms, digital payment ecosystems, and the increasing volume of sensitive customer data processed across web and mobile applications. As retailers continue to shift toward omnichannel and digital-first business models, the need to secure payment information, personal customer data, and transactional records has significantly increased, driving strong adoption of encryption technologies.

In addition, the rising incidence of cyber fraud, payment breaches, and identity theft in e-commerce platforms is compelling organizations to implement robust encryption mechanisms to ensure secure transactions and maintain customer trust. The widespread adoption of cloud-based retail infrastructure and third-party payment gateways is further amplifying the demand for end-to-end encryption across distributed systems. Moreover, increasing regulatory focus on data privacy and consumer protection laws is pushing retailers to strengthen their data security frameworks. Overall, the combination of rapid digitalization, growing cyber risks, and increasing reliance on secure digital payment ecosystems is driving strong growth in encryption adoption within the retail & e-commerce segment over the forecast period.

Regional Insights

North America dominated the global data encryption market with the largest revenue share of 39.6% in 2025, primarily driven by large-scale deployment of encryption across cloud-first architectures by hyperscalers and enterprise SaaS providers, along with early enterprise migration toward post-quantum cryptography pilots in regulated sectors. The region also saw accelerated adoption of field-level and tokenization-based encryption in BFSI institutions, driven by tightening compliance requirements such as PCI DSS 4.0 and evolving FFIEC guidelines in the U.S. In addition, widespread integration of hardware security modules (HSMs) across government and defense networks, coupled with healthcare providers expanding encryption for EHR systems under HIPAA modernization initiatives, further strengthened regional dominance.

U.S. Data Encryption Market Trends

The data encryption market in the U.S. accounted for the largest market revenue share in North America in 2025, driven by large-scale migration toward post-quantum cryptography (PQC) readiness programs led by financial institutions and federal agencies, alongside increasing deployment of encryption key management services integrated with multi-cloud and hybrid cloud environments. The expansion of zero-trust architecture implementations across critical infrastructure sectors, such as energy grids and defense networks, is further accelerating demand for end-to-end encryption solutions. In addition, the rising adoption of privacy-enhancing technologies in digital payment ecosystems and the growing enterprise use of confidential computing to secure data-in-use workloads are strengthening long-term market expansion.

Asia Pacific Data Encryption Market Trends

The data encryption market in the Asia Pacific is expected to grow at the fastest CAGR during the forecast period, driven by the rapid expansion of digital payment ecosystems and mobile-first financial services, particularly across India, China, and Southeast Asia. Increasing enforcement of data localization mandates such as China’s Cybersecurity Law and India’s Digital Personal Data Protection framework is accelerating enterprise investment in encryption for data-at-rest and data-in-transit. The region is also witnessing strong adoption of encryption within 5G-enabled IoT deployments and connected manufacturing ecosystems, especially in automotive and industrial automation sectors. In addition, the rising deployment of sovereign cloud infrastructure and the integration of large-scale encryption across fintech platforms and super-app ecosystems are further fueling high-growth momentum.

The China data encryption market held a significant share in the Asia Pacific in 2025, driven by large-scale enterprise adoption of encryption aligned with stringent data sovereignty requirements under the Cybersecurity Law and Data Security Law, which mandate localized storage and controlled encryption of critical information. Rapid expansion of encryption deployment across state-owned enterprises in banking, telecom, and energy sectors further strengthened market penetration, particularly for protecting cross-border data flows and critical infrastructure systems. In addition, the accelerated integration of encryption into cloud platforms operated by domestic hyperscalers and the increasing use of cryptographic controls in AI training datasets and industrial IoT networks contributed to sustained demand across the country.

The data encryption market in Japan is witnessing strong expansion, driven by accelerated adoption of quantum-safe and post-quantum cryptography solutions across financial institutions and government agencies, particularly in response to rising cyber espionage risks targeting critical infrastructure. The increasing deployment of cloud-based encryption integrated with hybrid IT environments in enterprises is further strengthening demand, especially in the banking, telecom, and healthcare sectors, which handle sensitive personal and transactional data. In addition, the growing adoption of hardware security modules (HSMs) for secure key management and the rising use of encryption in IoT-enabled industrial systems and smart manufacturing ecosystems are contributing to sustained market growth.

The India data encryption market is experiencing strong growth due to rapid expansion of digital payment ecosystems such as UPI-driven transactions, which are increasing the need for end-to-end encryption across fintech platforms and banking infrastructure. Strengthening regulatory enforcement under the Digital Personal Data Protection Act is also compelling enterprises to adopt encryption for the storage and processing of personal and sensitive data. In addition, large-scale enterprise cloud migrations and government-backed digital initiatives are accelerating demand for encryption integrated with identity-centric security and key management solutions. The growing adoption of encryption in telecom networks supporting the 5G rollout and increasing cybersecurity investments across the BFSI and IT services sectors are further reinforcing market expansion.

Europe Data Encryption Market Trends

The data encryption market in Europe is anticipated to grow at a significant CAGR from 2026 to 2033,driven by the enforcement of stringent regulatory frameworks such as the GDPR and the EU Data Act, which mandate encryption for personal and industrial data across enterprises. The increasing adoption of sovereign cloud initiatives across countries such as Germany and France is further accelerating demand for localized encryption and key management solutions to ensure data residency compliance. In addition, rising investments in post-quantum cryptography pilots led by EU cybersecurity agencies and growing deployment of encryption in critical sectors such as automotive connected systems, financial services, and cross-border payment networks are strengthening regional growth momentum.

The UK data encryption market is witnessing strong growth due to increasing adoption of encryption in financial services ecosystems, particularly across London-based banking and fintech firms handling high-volume digital transactions and open banking APIs under PSD2 frameworks. The growing adoption of zero-trust architectures across government and defense networks is further driving demand for advanced key management and identity-based encryption controls. In addition, the growing deployment of cloud-native encryption solutions across enterprises migrating to hybrid cloud environments, along with heightened cybersecurity requirements in healthcare under NHS digital transformation programs, is reinforcing sustained market expansion.

The data encryption market in Germany held a significant market share in Europe in 2025, driven by strong enterprise-wide adoption of encryption solutions across its automotive and industrial manufacturing sectors, particularly for securing connected vehicle data, smart factory systems, and industrial IoT communications. Strict enforcement of GDPR compliance, combined with Germany’s national data protection regulations, is pushing organizations to implement advanced encryption for data at rest and in transit across cloud and on-premises environments. In addition, the increasing deployment of sovereign cloud infrastructure by German enterprises and the rising use of hardware security modules (HSMs) in banking and public-sector networks for secure key management are further strengthening market dominance.

Key Data Encryption Company Insights

Some of the key companies operating in the market include Amazon Web Services, Broadcom, Check Point Software Technologies, Cisco, among others.

Key Data Encryption Companies:

The following key companies have been profiled for this study on the data encryption market.

- Amazon Web Services

- Broadcom

- Check Point Software Technologies

- Cisco

- Dell Technologies

- Entrust

- Fortinet

- IBM

- Microsoft

- Oracle

- Palo Alto Networks

- Sophos

- Thales

- Trend Micro

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Microsoft; IBM; Thales; Cisco; Oracle

- Focus on integrated encryption platforms across cloud, endpoint, database, and hybrid IT environments.

- Strong investments in AI-driven security, quantum-safe cryptography, and compliance-focused encryption solutions.

- Strong global enterprise customer base with established brand trust and regulatory certifications.

- Broad cybersecurity ecosystems integrated with cloud, networking, identity, and data management platforms.

- Large product portfolios can create integration complexity and slower deployment cycles.

- Higher pricing and operational costs compared to specialized or niche encryption vendors.

Emerging Players: Trend Micro; Entrust; Sophos

- Expanding cloud-native encryption and zero-trust security capabilities through acquisitions and platform integration.

- Increasing focus on AI-powered threat detection, managed security services, and SME-focused encryption solutions.

- Faster innovation cycles and stronger focus on cloud workload, endpoint, and AI security environments.

- Competitive pricing and flexible deployment models for mid-sized enterprises and cloud-first organizations.

- Lower enterprise penetration compared to large legacy vendors in highly regulated industries.

- Dependence on partnerships and channel ecosystems for global market expansion.

Recent Development

-

In March 2026, Broadcom launched an end-to-end, Post-Quantum Cryptography (PQC)-safe in-flight network encryption solution using its Emulex SecureHBA technology. It enables organizations to encrypt data in motion across server-to-storage networks using quantum-resistant algorithms and hardware-based key management, ensuring protection against future quantum computing threats and “harvest now, decrypt later” attacks.

-

In July 2025, Fortinet introduced quantum-safe security capabilities in FortiOS that integrate post-quantum cryptography (PQC) and quantum key distribution (QKD) to protect enterprise encryption from future quantum-computing attacks. This strengthens data encryption by enabling organizations to transition to quantum-resistant algorithms and hybrid key-exchange mechanisms, reducing the risks posed by “harvest-now, decrypt-later” attacks.

Data Encryption Market Report Scope

Report Attribute

Details

Market size in 2025

USD 15.2 billion

Estimated market size in 2026

USD 16.9 billion

Projected market size by 2033

USD 37.2 billion

Growth rate

CAGR of 11.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, deployment, type, organization size, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Amazon Web Services; Broadcom; Check Point Software Technologies; Cisco; Dell Technologies; Entrust; Fortinet; Google; IBM; Microsoft; Oracle; Palo Alto Networks; Sophos; Thales; Trend Micro

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Data Encryption Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global data encryption market report based on component, deployment, data encryption, organization size, end use, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Solutions

-

Services

-

Professional Services

-

Managed Services

-

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-Premises

-

Cloud

-

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Symmetric Encryption

-

Asymmetric Encryption

-

-

Organization Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

Small & Medium-Sized Enterprises (SMEs)

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

IT & Telecommunications

-

Retail & E-commerce

-

Healthcare

-

Government & Defense

-

Manufacturing

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Country-specific analysis for the Germany data encryption market along with GDPR and BSI compliance coverage.

Added Germany-specific market sizing and forecast analysis.

Included detailed assessment of GDPR, BSI IT Security Act, and cloud encryption compliance requirements.

Added profiles of regional cybersecurity and encryption solution providers operating in Germany.

Helped the client evaluate regulatory-driven demand opportunities in Germany.

Supported localization strategy for encryption product positioning.

Improved understanding of competitive intensity from domestic vendors.

Region-specific report for the Middle East data encryption market with additional local players and cybersecurity regulations.

Expanded analysis for UAE and Saudi Arabia markets.

Included profiles of regional encryption and cybersecurity service providers.

Assisted the client in understanding regulatory adoption trends in the Middle East.

Helped benchmark regional competitors and partnership opportunities.

Additional analysis of the healthcare data encryption market in North America with HIPAA compliance trends and hospital-specific adoption insights.

Added healthcare industry segmentation covering hospitals, clinics, and healthcare cloud platforms.

Included analysis of HIPAA-driven encryption requirements and patient data security trends.

Provided country-level market outlook for the U.S. and Canada healthcare sectors.

Helped the client identify high-demand encryption applications in healthcare.

Supported product positioning aligned with healthcare compliance requirements.

Enabled better targeting of hospitals and healthcare IT service providers.

Frequently Asked Questions About This Report

Factors such as rising frequency of cyberattacks, ransomware incidents, and data breaches targeting sensitive information and increasing adoption of cloud computing, remote work, and digital transformation initiatives across industries play a key role in accelerating the data encryption market.

The solutions segment led with a 78.4% revenue share in 2025, while the services segment is the fastest-growing.

The cloud segment held the largest revenue share in 2025, while the cloud segment is the fastest-growing.

The symmetric encryption segment held the largest revenue share in 2025, while the asymmetric encryption segment is the fastest-growing.

Large enterprises segment held the largest share in 2025, while the small & medium-sized enterprises segment is the fastest-growing.

The global data encryption market size was valued at USD 15.2 billion in 2025 and is estimated at USD 16.9 billion for 2026.

The global data encryption market is expected to grow at a CAGR of 11.9% from 2026 to 2033, reaching USD 37.2 billion by 2033.

North America dominated with a 39.6% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include Amazon Web Services; Broadcom; Check Point Software Technologies; Cisco; Dell Technologies; Entrust; Fortinet; Google; IBM; Microsoft; Oracle; Palo Alto Networks; Sophos; Thales; Trend Micro

About the Author(s)

IT Services & Applications Research Team

Technology · IT Services & ApplicationsThis report was authored by the it services & applications research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the it services & applications segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.