- Home

- »

- Next Generation Technologies

- »

-

Deep Space Exploration Market Size Report, 2025-2033GVR Report cover

![Deep Space Exploration Market (2025 - 2033)Report]()

Deep Space Exploration Market (2025 - 2033)

Size, Share & Trends Analysis Report By Application (Transportation, Mars Exploration), By Mission Type (Manned, Unmanned), By Subsystem, By End Use, By Region, And Segment Forecasts

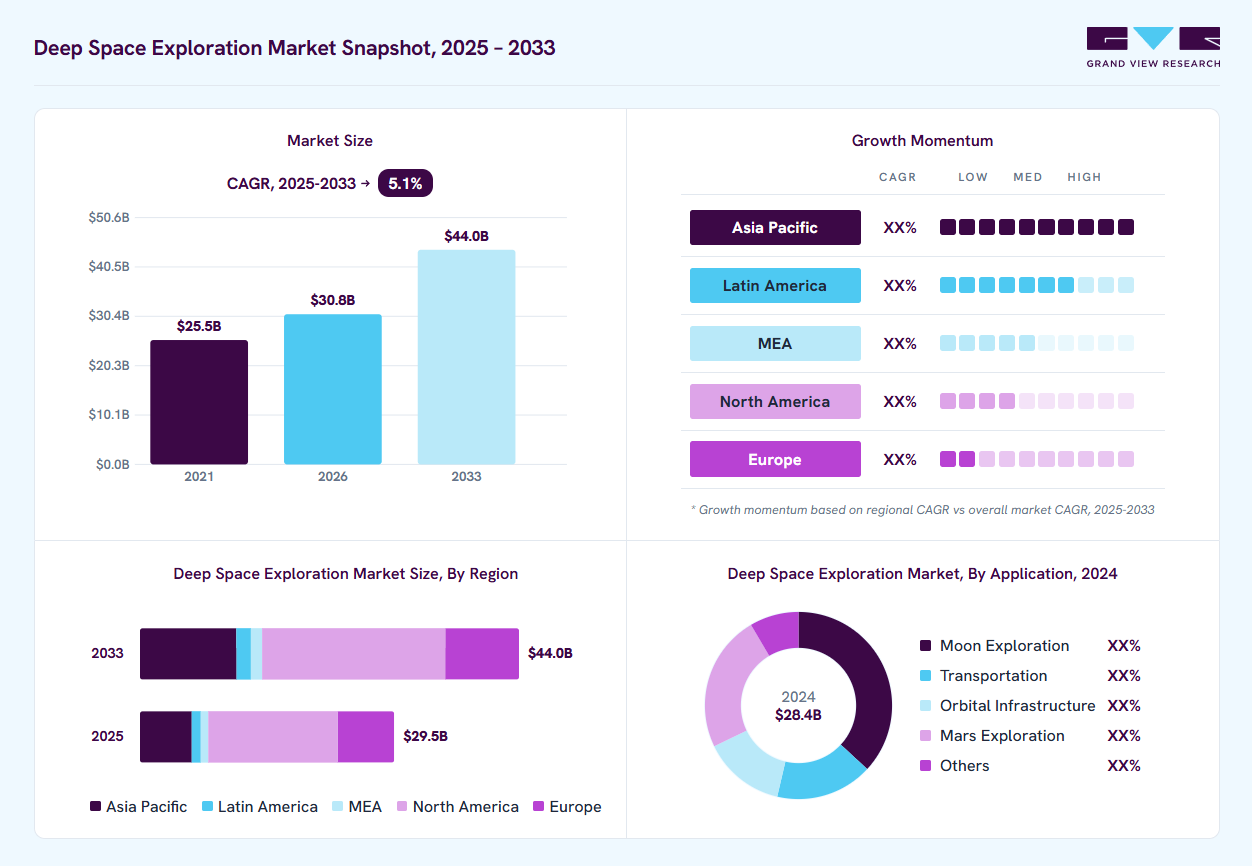

Market Size, 2024

$28.4BMarket Estimate, 2026

$30.8BMarket Forecast, 2033

$44.0BCAGR, 2025–2033

5.1%Deep Space Exploration Market Summary

The global deep space exploration market size was valued at USD 28.4 billion in 2024 and is projected to grow from USD 30.8 billion in 2026 to USD 44.0 billion by 2033, at a CAGR of 5.1% from 2025 to 2033. North America dominated the market, accounting for a revenue share of 51.0% in 2024. The market growth is primarily driven by increasing investments from government space agencies and private aerospace companies, rising interest in interplanetary missions, deep space communication technologies, growing demand for scientific research beyond Earth's orbit, and the development of reusable launch systems.

Key Market Trends & Insights

- The deep space exploration market in the U.S. led the North America market and held the largest revenue share in 2024.

- By application, the moon exploration segment led the market and held the largest revenue share of over 36.0% in 2024.

- By subsystem, the propulsion system segment led the market and held the largest revenue share of over 40.0% in 2024.

- By mission type, the unmanned mission segment dominates the market and holds the largest revenue share of over 74.0% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 28.4 Billion

- 2033 Projected Market Size: USD 44.0 Billion

- CAGR (2025-2033): 5.1%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market.

The increasing demand for scientific discovery, space resource utilization, and long-duration interplanetary missions primarily drives market growth. The growing involvement of private aerospace companies and international collaborations accelerates mission planning and execution. Government investments and long-term strategic initiatives foster innovation and funding for advanced exploration technologies. Rising interest in planetary defense, asteroid mining, and extraterrestrial habitation is further propelling the expansion of the deep space exploration industry.")

The rising interest in interplanetary missions and space colonization is significantly fueling the growth of the deep space exploration industry. Government agencies like NASA, ESA, CNSA, and private companies such as SpaceX and Blue Origin are investing heavily in long-duration missions. These initiatives drive demand for advanced propulsion systems, space habitats, and autonomous navigation technologies. This surge in mission planning and execution is expanding the commercial viability of deep space ventures and accelerating innovation across the industry.

In addition, the increasing emphasis on international collaboration and public-private partnerships is becoming a major market growth driver. Collaborative R&D efforts enable shared access to critical technologies, reduce development costs, and boost the pace of mission deployment. This cooperative approach strengthens global capabilities and supports the sustainable expansion of the deep space economy.

Furthermore, advancements in AI, robotics, and autonomous systems are revolutionizing deep space exploration capabilities. These technologies are integrated into planetary rovers, space probes, and unmanned missions to enhance real-time decision-making, terrain mapping, and sample collection. Automation reduces reliance on human intervention, allowing extended missions in harsh and remote environments. AI and robotics continue to evolve, streamlining complex tasks and driving greater efficiency in mission planning and execution, accelerating market growth.

Moreover, growing investments in space infrastructure and on-orbit servicing technologies are enhancing the long-term potential of the deep space exploration industry. Innovations such as reusable launch vehicles, in-space manufacturing, and orbital refueling systems are laying the foundation for sustainable operations beyond Earth orbit. These advancements reduce mission costs and open new commercial opportunities, including asteroid mining, lunar tourism, and deep space logistics. As the infrastructure matures, it is expected to catalyze a new era of exploration and economic development in space, fueling market growth.

Mission Type Insights

The unmanned mission segment accounted for the largest market share in 2024, driven by the increasing demand for cost-effective, risk-free, and technologically advanced exploration capabilities. As space agencies and private players focus on exploring distant celestial bodies like Mars, asteroids, and outer planets, unmanned missions offer a practical solution without endangering human life. Advances in autonomous navigation, AI-driven data analysis, and high-performance robotics are enabling longer, more complex missions with greater scientific yield. These advantages, lower mission costs and faster deployment timelines, propel unmanned missions' dominance in the deep space exploration industry.

The manned mission segment is expected to witness the highest CAGR from 2025 to 2033, driven by increasing investments in human-led missions to the Moon, Mars, and beyond. Governments and space agencies prioritize crewed exploration to establish long-term human presence, conduct complex scientific research, and demonstrate geopolitical leadership in space. Developing advanced life support systems, radiation shielding, and deep space habitats further supports this growth. International collaborations and rising private sector involvement in astronaut-led missions are accelerating the momentum of manned deep space programs.

End Use Insights

The government space Agencies segment accounted for the largest market share in 2024, owing to increasing investments in deep space missions aimed at lunar exploration, Mars colonization, and asteroid mining. National agencies such as NASA, ESA, CNSA, and ISRO drive the demand for advanced propulsion systems, long-duration life support, and autonomous navigation technologies to support ambitious interplanetary missions. These agencies collaborate with international partners and private companies to expand scientific capabilities and geopolitical influence in space. The focus on strategic, long-term exploration goals and the development of next-generation spacecraft continues to position government space agencies as the primary market end-users.

The commercial segment is expected to witness a significant CAGR from 2025 to 2033. This growth is driven by increasing private sector investments in lunar missions, asteroid mining, and satellite deployment beyond Earth’s orbit. Emerging space companies are capitalizing on cost reductions in launch services, reusable rockets, and miniaturized spacecraft technologies to develop profitable deep space ventures. Strategic partnerships with national space agencies and advancements in in-space propulsion and autonomous navigation systems enable commercial players to pursue long-duration missions, fueling rapid market expansion.

Application Insights

The moon exploration segment dominated the market with a market share of over 36% in 2024, driven by renewed global interest in lunar missions for scientific, commercial, and strategic purposes. Government-led programs such as NASA’s Artemis and increasing private sector investments accelerate mission planning and infrastructure development around the Moon. The segment's leadership is further supported by advancements in propulsion systems, autonomous navigation, and lunar surface robotics, all crucial for sustained lunar presence. The Moon's potential as a staging point for deeper space missions reinforces its strategic importance in the exploration ecosystem.

Mars exploration is expected to witness the highest CAGR of over 7% from 2025 to 2033. This growth is primarily driven by rising government investments and international collaborations focused on crew and robotic missions to Mars. Advancements in propulsion systems, autonomous navigation, and life-support technologies are further enhancing mission feasibility. The increasing role of private space companies and strategic partnerships with space agencies is accelerating innovation, making Mars exploration a central focus of the next-generation deep space exploration industry.

Subsystem Insights

The propulsion system segment accounted for the largest market share in 2024, driven by the increasing number of deep space missions requiring advanced propulsion technologies for extended travel beyond low Earth orbit. Agencies and private companies invest in high-efficiency systems such as electric propulsion, nuclear thermal propulsion, and ion thrusters to reduce travel time and enhance mission capability. As deep space exploration targets more ambitious destinations like Mars and asteroids, the demand for reliable and scalable propulsion systems continues to surge. The growing emphasis on long-duration missions and interplanetary travel further propels the adoption of next-generation propulsion subsystems in the deep space exploration industry.

The command and control system segment is expected to witness the highest CAGR from 2025 to 2033. This growth is driven by the increasing complexity of interplanetary missions and the need for highly autonomous, real-time decision-making systems. Advancements in AI-powered navigation, fault detection, and spacecraft health monitoring enable deep space probes to operate with minimal ground intervention. The rising deployment of robotic missions to the Moon, Mars, and beyond fuels demand for robust and scalable command and control architectures, accelerating adoption across government and commercial space programs.

Regional Insights

The North America deep space exploration market accounted for the largest share of over 51% in 2024, driven by the strong presence of leading space agencies, robust government funding for space research, and early adoption of advanced aerospace technologies. The region benefits from a mature ecosystem of private space companies engaged in developing interplanetary missions and space infrastructure. Increasing investment in AI-powered autonomous systems, rapid advancements in launch vehicle technologies, and growing interest in lunar and Mars missions are accelerating the adoption of the deep space exploration industry across the region.

U.S. Deep Space Exploration Market Trends

The deep space exploration market in the U.S. dominated with the largest market share of over 85% in 2024, driven by the country’s strong presence of government space, a thriving private aerospace sector, and significant investment in next-generation space technologies. The increasing number of collaborative programs between NASA and private players accelerates mission timelines and fosters innovation. Integrating AI, robotics, and autonomous systems into mission planning and operations further boosts efficiency and expands the capabilities of unmanned missions, contributing to the country's rapid growth of the deep space exploration industry.

Europe Deep Space Exploration Market Trends

The deep space exploration market in Europe has a significant market share of over 22% in 2024. In Europe, the growth is driven by increased funding from the European Space Agency (ESA) and national governments for Moon and Mars missions, alongside strong participation in international collaborations like the Artemis program. Europe's focus on developing autonomous navigation systems, reusable launch vehicles, and in-space manufacturing further fuels innovation. The presence of advanced aerospace industries supports the development of next-generation deep space technologies, driving sustained market momentum.

The UK deep space exploration market is expected to grow significantly in the coming years. The country benefits from strong government backing through initiatives by the UK Space Agency aimed at participation in the Mars mission. Investment in advanced satellite and propulsion technologies and partnerships with ESA and private aerospace firms is boosting research and development. The presence of world-class universities and innovation hubs fosters talent and drives technological advancements. Increasing focus on commercial space ventures and orbital infrastructure creates new growth opportunities across the country's deep space exploration industry.

The deep space exploration market in Germany is driven by the country’s robust aerospace engineering capabilities, strong government backing through institutions like DLR (German Aerospace Center), and active participation in European Space Agency (ESA) missions. Germany’s commitment to scientific research, space innovation, and sustainability leads to increased investment in propulsion systems, orbital infrastructure, and unmanned exploration technologies. Collaboration between academia, private firms, and international partners fosters technological advancements and reinforces Germany’s strategic role in future Moon and Mars missions.

Asia Pacific Deep Space Exploration Market Trends

The deep space exploration market in Asia Pacific is expected to grow at the highest CAGR of over 8% from 2025 to 2033, driven by increasing investments from interplanetary missions and satellite programs. The region’s growing technological capabilities boost mission readiness, including robotics, AI, and launch vehicle development advancements. Supportive government policies, rising public-private partnerships, and expanding regional space agencies are accelerating innovation. Establishing dedicated spaceports and R&D facilities strengthens the infrastructure for long-term deep space initiatives across Asia Pacific.

Japan deep space exploration market is gaining traction, driven by the country's advanced aerospace capabilities, strong government support, and collaborative efforts with global space agencies. Japan's space agency, JAXA, plays a key role in lunar and asteroid missions, including partnerships in the Artemis program and the successful Hayabusa missions. The nation’s expertise in robotics and miniaturized satellite technology also enhances mission efficiency and scientific output. With a focus on innovation and international collaboration, Japan continues to expand its presence in the deep space exploration industry.

The deep space exploration market in China is rapidly expanding. The country’s strong commitment to space leadership, demonstrated through major initiatives like the Chang’e lunar missions and the Tianwen Mars program, drives significant investments in deep space technologies. Robust government support through policies and funding, along with advancements in propulsion systems, robotics, and AI, is accelerating mission readiness. China's growing commercial space sector and strategic collaborations with international partners are enhancing innovation and boosting the overall growth of the deep space exploration industry.

Key Deep Space Exploration Company Insights

Some key players operating in the market include SpaceX and Lockheed Martin Corporation.

-

SpaceX is a leading force in the market, known for its ambitious Starship program designed for interplanetary travel to the Moon, Mars, and beyond. With successful contracts under NASA's Artemis program and continuous advancements in reusable launch technology, SpaceX is revolutionizing the economics and scale of deep space missions. Its vertically integrated approach, rapid development cycles, and proven launch capabilities position it as a central player in the future of human and robotic exploration.

-

Lockheed Martin Corporation is an aerospace and defense contractor with a major footprint in the deep space exploration industry. It is critical in developing NASA’s Orion spacecraft, designed for crewed missions beyond low Earth orbit. Lockheed Martin is also a key contributor to the Lunar Gateway program and Mars Sample Return mission architecture. Decades of expertise and collaborations with multiple space agencies are central to shaping next-generation deep space missions.

ASTROBOTIC TECHNOLOGY and ROCKET LAB are some of the emerging market participants.

-

ASTROBOTIC TECHNOLOGY is an emerging deep space exploration player specializing in lunar logistics and lander systems. The company’s Peregrine and Griffin landers are developed to deliver payloads to the Moon under NASA's CLPS (Commercial Lunar Payload Services) initiative. Focused on low-cost, reliable access to the lunar surface, Astrobotic enables scientific and commercial missions, positioning itself as a vital player in the commercial lunar economy.

-

ROCKET LAB is an emerging commercial space company gaining momentum in deep space exploration through its Photon spacecraft platform. Originally focused on small satellite launches, the company has expanded into interplanetary missions, including a planned mission to Venus. With its flexible launch services and deep space-ready spacecraft, Rocket Lab is carving out a niche in affordable, agile deep space missions for governments and private customers.

Key Deep Space Exploration Companies:

The following are the leading companies in the deep space exploration market. These companies collectively hold the largest market share and dictate industry trends.

- SpaceX

- BLUE ORIGIN

- NEC Space Technologies, Ltd.

- Lockheed Martin Corporation.

- Northrop Grumman.

- Thales Alenia Space

- AIRBUS

- ROCKET LAB

- Sierra Nevada Corporation

- Boeing.

- ASTROBOTIC TECHNOLOGY

- Maxar Technologies

Recent Developments

-

In June 2025, ROCKET LAB successfully launched “Symphony in the Stars,” a small satellite mission to sun-synchronous orbit, demonstrating its expanding capabilities in orbital delivery. The company secured a NASA contract for its Photon spacecraft to support the Aspera ultraviolet astronomy mission in 2026. These developments highlight Rocket Lab’s growing role in the deep space exploration industry, offering reliable and cost-effective solutions for scientific payload deployment and interplanetary missions.

-

In May 2025, Northrop Grumman announced a USD 50 million investment in space startup Firefly Aerospace to accelerate the development of their jointly built medium lift launch vehicle, Eclipse. Designed for deep space missions, Eclipse combines technology from Northrop’s Antares and Firefly’s Alpha rockets. The vehicle will support a range of applications, including space station supply, scientific payload delivery, and national security missions. This strategic collaboration enhances market capabilities.

-

In May 2025, Lockheed Martin Corporation commenced integrating its Orion spacecraft for the Artemis II lunar mission, marking a major advancement in the deep space exploration industry. The Orion spacecraft is a critical component of NASA’s crewed mission architecture, designed to transport astronauts beyond low Earth orbit. This milestone highlights Lockheed Martin’s pivotal role in enabling sustainable human exploration of the Moon and future missions to Mars, reinforcing its leadership in next-generation deep space transportation systems.

Deep Space Exploration Market Report Scope

Report Attribute

Details

Market size in 2024

USD 28.4 billion

Estimated market size in 2026

USD 30.8 billion

Projected market size by 2033

USD 44.0 billion

Growth rate

CAGR of 5.1% from 2025 to 2033

Base year for estimation

2024

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report Product

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Application, subsystem, mission type, end use, region

Region scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Russia; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; UAE; South Africa

Key companies profiled

SpaceX; BLUE ORIGIN; NEC Space Technologies, Ltd.; Lockheed Martin Corporation; Northrop Grumman; Thales Alenia Space; AIRBUS; ROCKET LAB; Sierra Nevada Corporation; Boeing; ASTROBOTIC TECHNOLOGY; Maxar Technologies

Customization scope

Free report customization (equivalent to up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet you exact research needs. Explore purchase options

Global Deep Space Exploration Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest technological trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the deep space exploration market report based on application, subsystem, mission type, end use, and region:

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Moon Exploration

-

Transportation

-

Orbital Infrastructure

-

Mars Exploration

-

Others

-

-

Subsystem Outlook (Revenue, USD Million, 2021 - 2033)

-

Propulsion system

-

Command and control system

-

Navigation and guidance system

-

-

Mission Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Manned Mission

-

Unmanned Mission

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Government Space Agencies

-

Commercial

-

Military

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021- 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Russia

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The key players in the deep space exploration market are SpaceX, BLUE ORIGIN, NEC Space Technologies, Ltd. , Lockheed Martin Corporation., Northrop Grumman., Thales Alenia Space, AIRBUS, ROCKET LAB, Sierra Nevada Corporation, Boeing., ASTROBOTIC TECHNOLOGY, Maxar Technologies

Key drivers of deep space exploration market include by the increasing investments from government space agencies and private aerospace companies, rising interest in interplanetary missions, deep space communication technologies, growing demand for scientific research beyond Earth's orbit, and the development of reusable launch systems.

The global deep space exploration market size was valued at USD 28.4 billion in 2024 and is estimated at USD 30.8 billion for 2026.

The North America deep space exploration market accounted for the largest market share of over 51.0% in 2024, driven by the strong presence of leading space agencies, robust government funding for space research, and early adoption of advanced aerospace technologies. The region benefits from a mature ecosystem of private space companies which are actively engaged in interplanetary missions and space infrastructure development. Increasing investment in AI-powered autonomous systems, rapid advancements in launch vehicle technologies, and growing interest in lunar and Mars missions are accelerating the adoption of the deep space exploration industry across the region.

The global deep space exploration market is expected to grow at a CAGR of 5.1% from 2025 to 2033, reaching USD 44.0 billion by 2033.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.