- Home

- »

- Medical Devices

- »

-

Dental Implants Market Size & Share Report, 2026-2033GVR Report cover

![Dental Implants Market (2026 - 2033)Report]()

Dental Implants Market (2026 - 2033)

Size, Share & Trends Analysis Report By Surface Treatment Type, By Material, By Design, By Connection Type, By Implant Structure, By Price Tier, By Age Group, By Distribution Channel, By End-use, By Region, And Segment Forecasts

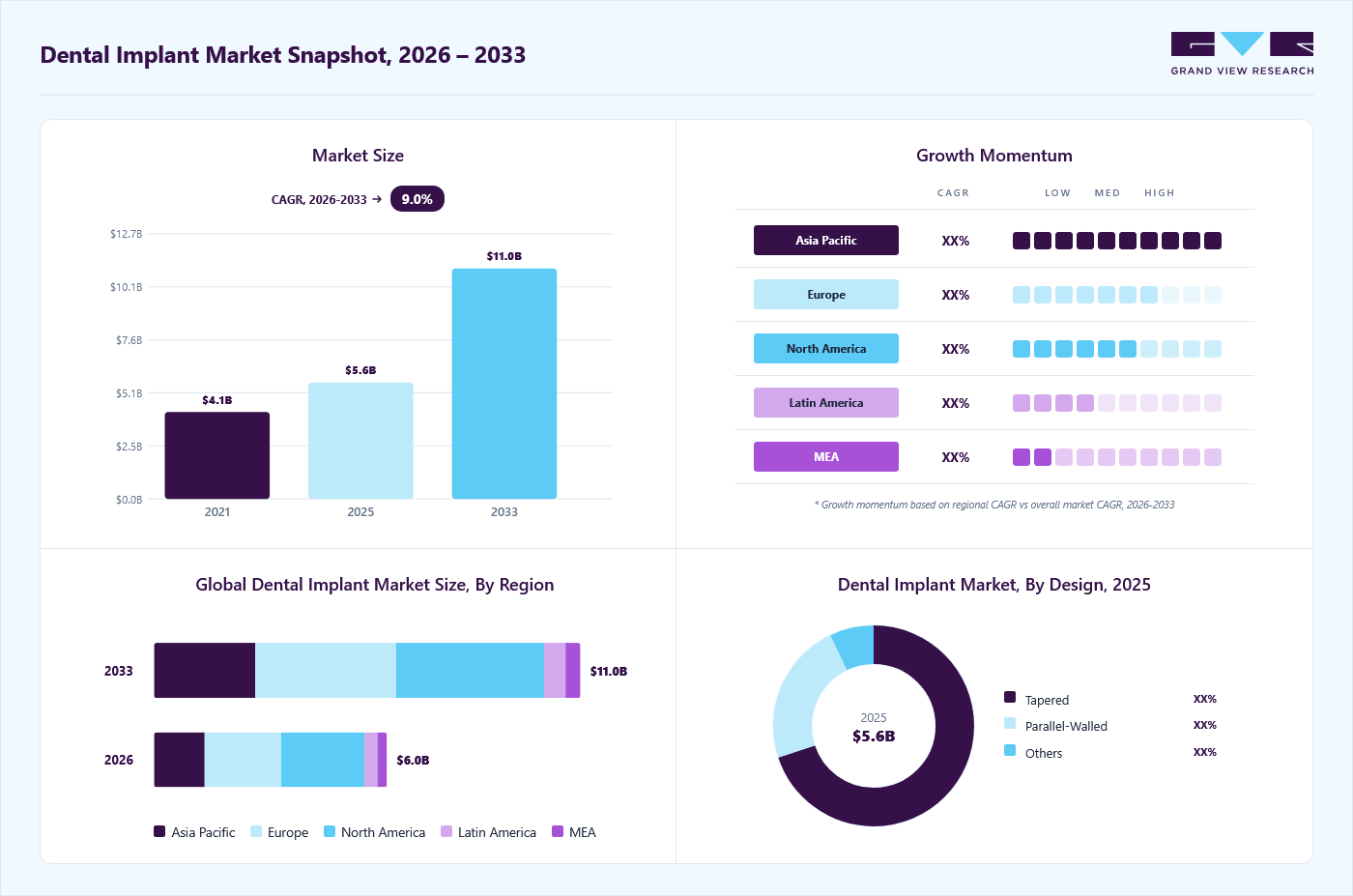

Market Size, 2025

$5.6BMarket Estimate, 2026

$6.0BMarket Forecast, 2033

$11.0BCAGR, 2026–2033

9.0%Dental Implants Market Summary

The global dental implants market size was valued at USD 5.6 billion in 2025 and is projected to reach from USD 6.0 billion in 2026 to USD 11.0 billion by 2033, growing at a CAGR of 9.0% from 2026 to 2033. North America held the largest revenue share of 36.1% in 2025. The market is driven by increasing demand for precise and advanced implant solutions, rising prevalence of tooth loss and oral disorders, and continuous innovations in implant materials and surface technologies.

Key Market Trends & Insights

- By surface treatment type: SLA AND SLActive segment accounted for the largest market revenue share of 37.8% in 2025.

- By material: Titanium segment led the dental implants market, accounting for the largest revenue share of 91.0% in 2025..

- By design: Tapered design held the largest revenue share of 69.8% in 2025.

- By connection type: Conical (Morse taper) connection held the largest revenue share of 46.1% in 2025.

- By implant structure: Two-piece segment held the largest revenue share of 90.9% in 2025.

- By price tier: Premium implants segment held the largest revenue share of 46.1% in 2025.

- By age group: Adult segment held the largest revenue share of 54.6% in 2025.

- By distribution channel: Direct sales segment held the largest revenue share of 61.2% in 2025.

- By end use: Dental clinics (including independent clinics and DSO-affiliated clinics) held the largest revenue share of 82.3% in 2025.

Regional Highlights

- Largest regional market: North America (36.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (fastest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 5.6 Billion

- Estimated market size in 2026: USD 6.0 Billion

- Projected market size by 2033: USD 11.0 Billion

- CAGR (2026-2033): 9.0%

Growing awareness of oral health, expanding dental tourism, and advancements in surgical techniques enhance treatment outcomes and patient satisfaction, fueling market growth. In addition, digital implant planning and guided surgery systems improve procedural accuracy, reduce treatment time, and increase overall efficiency. The growing prevalence of oral disorders, including tooth loss, tooth decay, and tooth extraction, is anticipated to propel the demand for dental implants. The data published by the WHO in March 2025 reports that approximately 7% of adults aged 20 and above, and around 23% of those aged 60 and above, experience complete tooth loss, underscoring the need for implants. The increasing burden of oral diseases, including cavities, tooth loss, and gum disease, is expected to raise the demand for dental implants significantly.")

Furthermore, the burden of tooth loss is significant in the older population, underscoring the growing demand for dental implants among these patients. In addition, supportive policies contribute to the increased adoption of dental implants. For instance, a study published by the National Library of Medicine in September 2024 found that expanding dental care coverage for older adults in Korea led to a 13.5% increase in partial denture use and a 60.5% increase in dental implant use among individuals aged 65 and older. Therefore, these factors, along with the rising prevalence of dental disorders in this demographic, are expected to drive market growth.

")

The introduction of innovative dental implant technologies continues to play a pivotal role in driving the growth of the dental implant industry. Industry players are actively launching advanced implant systems to improve clinical outcomes and procedural efficiency.

For instance, in April 2025, ZimVie Inc. launched its Immediate Molar Implant System in the U.S. market. This new system features specially engineered instrumentation to streamline site preparation following molar extraction, enabling a more controlled and predictable surgical procedure. It also includes optimized wide-diameter implants that provide a better fit within the molar socket, offering superior primary stability. Notably, the system incorporates ZimVie's proprietary DAE coronal surface technology, which may potentially reduce the risk of peri-implantitis by up to 20%. Moreover, unlike traditional treatment protocols that typically require a healing period of several months after molar extraction before implant placement, this system enables immediate placement and restoration, cutting treatment time by nearly half. The result is a simplified, efficient, and more predictable clinical workflow.

“The launch of our Immediate Molar Dental Implant System marks a significant milestone in our commitment to advancing dental technology. We have expanded the offering of our implant systems to address the unique challenges of molar tooth restoration and provide patients with shorter and more cost-effective treatment while delivering a more predictable, lasting outcome,” said ZimVie CEO Vafa Jamali.

The rising burden of dental disorders in emerging economies such as China, India, and Brazil is creating substantial growth opportunities for the dental implants industry. According to data published by The Hindu in March 2025, nearly 60% of India's population is affected by dental caries, and approximately 85% suffer from gum disease. In China, data from the National Library of Medicine in March 2025 reveals that in 2021, the country accounted for 14.10% of global incident cases, 16.25% of prevalent cases, and 18.93% of YLDs (Years Lived with Disability) related to oral disorders. Similarly, Brazil is facing a significant economic impact, with the data published by the European Federation of Periodontology in March 2024 reporting that direct treatment costs for dental caries reached USD 36.23 billion among individuals aged 12-65. Some major causes of tooth loss include gum disease, cavities, and dental trauma, among others. Thus, the substantial population with risk factors for tooth loss is anticipated to drive the demand for implants among emerging markets.

Market Dynamics

Dental implants are gaining strong traction across the global dental industry as they play a critical role in replacing missing teeth and restoring oral function, aesthetics, and overall quality of life. Dental implant systems, including implant fixtures, abutments, and prosthetic components, provide a permanent and reliable solution for single-tooth, multiple-tooth, and full-arch restorations. Compared with conventional bridges and removable dentures, dental implants offer several advantages, including superior stability, long-term durability, preservation of jawbone structure through osseointegration, improved chewing efficiency, enhanced speech, and a more natural appearance. These clinical and functional benefits have made dental implants the preferred treatment option for tooth replacement among both patients and dental professionals.

Increasing cases of tooth loss caused by dental caries, periodontal disease, trauma, and aging are creating a greater need for permanent tooth replacement solutions. Poor oral hygiene, unhealthy dietary habits, tobacco use, and an aging population have contributed to the growing prevalence of oral diseases worldwide. As more patients seek durable, functional alternatives to removable dentures and bridges, the demand for dental implants continues to grow. Dental implants provide long-term stability, preserve jawbone structure, and improve chewing ability and aesthetics, making them a preferred restorative option.

Implant treatment involves multiple components, including implant fixtures, prosthetic crowns, diagnostic imaging, surgical procedures, and follow-up care, making it considerably more expensive than conventional tooth replacement methods. Additional procedures such as bone grafting or sinus lift surgery further increase treatment costs for patients with insufficient bone density. In many countries, dental implants are only partially covered or not covered by public and private health insurance, resulting in high out-of-pocket expenses. This limits treatment adoption, particularly in developing economies and among middle- and low-income populations.

Manufacturers and research institutions are conducting clinical studies to evaluate new implant materials, surface treatments, biomaterials, immediate loading protocols, and digital implant workflows aimed at improving osseointegration, long-term stability, and treatment success rates. Positive clinical evidence strengthens regulatory approvals, increases clinician confidence, and encourages the adoption of advanced implant systems in routine practice. Clinical trials also support the introduction of zirconia implants, short implants, patient-specific implant designs, and minimally invasive surgical techniques that address a wider range of patient needs.

Market Concentration & Characteristics

The market growth stage is moderate, and the pace of growth is accelerating. The dental implants industry is characterized by significant growth owing to the rising demand for restorative dentistry procedures, growing developments of innovative products, and increasing clinical trials.

The degree of innovation in the dental implant market is notably high, driven by rapid advancements in digital dentistry, biomaterials, and precision manufacturing technologies. Companies integrate computer-aided design and manufacturing (CAD/CAM), 3D printing, and AI-powered treatment planning to enhance implant accuracy and customization. Innovations in surface modification and nanotechnology are enhancing osseointegration and improving healing outcomes, while smart implants equipped with sensors are emerging to monitor implant stability and bone health in real-time. In August 2025, Dentsply Sirona launched its digital Product Selection Guide on its U.S. e-commerce platform. The new tool simplifies implant selection by providing clinicians with personalized product recommendations and a streamlined, user-friendly purchasing journey.

Regulations play a critical role in shaping the dental implant industry, ensuring patient safety, product efficacy, and quality compliance. Stringent standards set by authorities such as the U.S. FDA, European MDR, and other regional regulatory bodies have increased the need for robust clinical evidence and post-market surveillance. While this raises entry barriers for smaller players, it also enhances product reliability and market transparency. The focus on traceability, biocompatibility, and digital workflow integration under evolving frameworks encourages manufacturers to invest in R&D and quality assurance, ultimately driving innovation and patient trust.

The market has seen significant mergers and acquisitions (M&A) in recent years, driven by the need for portfolio expansion, technological integration, and market consolidation. Leading companies have actively acquired innovative startups and regional manufacturers to strengthen their global presence and digital capabilities. These strategic moves enable access to new technologies, such as 3D printing, AI-based planning systems, and regenerative biomaterials, while broadening the geographic reach. In February 2025, Medtronic acquired key nanosurface technology assets from Nanovis, a leader in biologic fixation solutions for spine, orthopedic, and dental implants. The acquisition also included intellectual property rights related to Sites Medical's OsteoSync titanium pads.

Analyst Perspective

The dental implants market is driven by the increasing prevalence of tooth loss, rising demand for permanent tooth replacement solutions, and growing awareness of the functional and aesthetic benefits of dental implants. Market growth is further supported by the expanding geriatric population, increasing incidence of periodontal diseases and dental trauma, and the rising adoption of implant-supported restorative procedures.

Continuous advancements in implant materials, surface technologies, digital treatment planning, guided implant surgery, and CAD/CAM-based prosthetics are improving clinical outcomes and treatment efficiency. The most successful companies will be those that offer a comprehensive portfolio of dental implants, prosthetic components, and digital implant solutions while focusing on product quality and clinician support. As dental clinics adopt digital workflows, intraoral scanners, 3D imaging, and computer-guided implant placement, market leadership will depend on continuous innovation, strong clinical evidence, strategic partnerships with dental professionals, and strong global manufacturing and distribution capabilities.

Rising Dental Tourism Driven by Affordable Implant Pricing

Dental tourism is creating a significant opportunity for the dental implants market by making implant treatments more affordable and accessible to a larger patient population. The high cost of dental implant procedures in developed countries encourages many patients to seek treatment in countries that offer comparable quality of care at substantially lower prices. For instance, the average cost of a single dental implant ranges from USD 3,500-6,000 in the U.S., USD 2,600-5,300 in the UK, and USD 2,000-4,000 in Germany and Australia, whereas countries such as Turkey (USD 800-1,500), Mexico (USD 700-1,400), and Thailand (USD 900-1,600) provide the same procedures at a much lower cost. This affordability enables patients who may otherwise postpone or avoid treatment to opt for dental implants.

In addition, this pricing gap has also encouraged segmentation of the dental implants industry into Premium Implants, Mid-Range Implants, and Value/Economy Implants, catering to different patient budgets and clinical requirements. Premium Implants are typically associated with advanced materials, leading brands, and complex restorative cases, while Mid-Range Implants balance cost and quality for standard procedures. Value/Economy Implants are used in cost-sensitive markets, including dental tourism destinations, where affordability is a primary decision factor.

Consumer Dynamics

Consumer dynamics in the dental implants market are evolving as awareness of implant therapy continues to rise and patients seek durable, functional, and aesthetically pleasing tooth-replacement solutions. In June 2025 survey of dental patients found that 72% were aware of dental implants, while 66% held a positive perception of implant treatment, indicating growing consumer acceptance. However, only 48% correctly identified implants as artificial tooth roots, suggesting that patient education remains an important factor influencing treatment decisions. Affordability remains the primary barrier to adoption, particularly in developing economies where out-of-pocket healthcare spending is high. Consumer willingness to undergo implant treatment is influenced by income level, educational background, perceived treatment quality, expected longevity, and aesthetic outcomes rather than price alone. Further, patients are relying more on online reviews, dentist credentials, and digital consultations before selecting a provider, making transparency, trust, and clinical reputation important drivers of purchasing behavior.

Consumer dynamics and purchase behavior in the dental implants market (2025)

Consumer Behavior Metric

Findings (2025)

Business Impact

Consumers aware of dental implants

72% of surveyed patients had heard of dental implants

Higher awareness supports future market growth and treatment adoption.

Knowledge of implant function

48% correctly identified implants as artificial tooth roots

Indicates opportunities for patient education and market expansion.

Consumer perception

66% of respondents had a positive opinion of dental implants

Positive perception increases the chances of treatment acceptance.

Major barrier to implant adoption

Treatment cost remains the leading barrier

Affordability continues to influence purchasing decisions.

Purchase decision factors

Income, education, treatment quality, and aesthetics are the primary factors

Consumers prioritize long-term value and clinical outcomes

Source: National Library of Medicine, Springer Nature

Surface Treatment Type Insights

The SLA AND SLActive segment accounted for the largest market revenue share of 37.8% in 2025, driven by their superior surface technology that enhances osseointegration and accelerates healing time. These advanced surface treatments enhance bone-to-implant contact, stability, and long-term success rates, making them the preferred choice among clinicians for both immediate and delayed loading procedures. Their strong clinical track record and proven reliability have positioned SLA and SLActive implants as the gold standard in modern implant dentistry.

The nano-textured surfaces segment is expected to register the fastest CAGR over the forecast period, driven by its ability to significantly enhance osseointegration, cellular response, and long-term implant stability. Nano-textured implants feature surface modifications at the nanometer scale that mimic the natural structure of bone tissue, promoting superior osteoblast adhesion, proliferation, and differentiation. This results in faster healing and stronger bone-to-implant integration than conventional surface treatments. In addition, advancements in nanotechnology and surface engineering have enabled manufacturers to develop implants with improved biocompatibility, antibacterial properties, and mechanical strength, thereby reducing the risk of peri-implantitis and implant failure. The growing clinical preference for implants that ensure early loading and high success rates, combined with increasing R&D investment in next-generation surface modification techniques, is expected to drive the rapid growth of the nano-textured surfaces segment over the forecast years.

Design Insights

The tapered design segment led the dental implants industry, accounting for the largest revenue share of 69.8% in 2025, capturing the most significant share owing to its superior primary stability and versatility in various bone conditions. Tapered implants closely mimic the natural shape of a tooth root, allowing for better adaptation in narrow ridges and extraction sockets, which enhances placement precision and load distribution. Their design facilitates immediate implantation and loading, reducing treatment time and improving patient outcomes. In addition, the growing adoption of minimally invasive and digitally guided implant procedures has further bolstered clinicians' preference for tapered implants.

The parallel-walled segment is expected to grow at the fastest CAGR over the forecast period, driven by its predictable load distribution, ease of placement, and suitability for dense bone structures. Parallel-walled implants offer a larger surface area for bone contact, promoting excellent osseointegration and long-term stability, particularly in cases that require multiple implants or complex restorations. Their uniform shape enables greater surgical flexibility and consistency in achieving optimal insertion torque, thereby reducing the risk of micro-movements and implant failure. The increasing adoption of computer-guided and digitally planned implant procedures has also enhanced the precision and efficiency of parallel-walled implant placement. As clinicians seek reliable, stable, and versatile implant options, the parallel-walled segment is poised for rapid growth.

Connection Type Insights

The conical (morse taper) connection segment led the dental implants market with the largest revenue share of 46.1% in 2025, driven by its superior mechanical stability, excellent sealing ability, and reduced micro-movement between implant components, which helps minimize the risk of bacterial infiltration and peri-implant complications. In addition, this connection type is widely preferred in modern implant dentistry due to its strong long-term clinical performance and improved stress distribution, which enhances implant durability and success rates. Within this segment, the CM 11.5° (Classic Morse Taper) is valued for its established clinical reliability and long-term use in conventional implant systems, while the CM 16° (Modern/Grand Morse) is gaining preference for its enhanced prosthetic flexibility, improved digital workflow compatibility, and better adaptability in contemporary implant designs.

The External Hex (HE) connection type segment is expected to grow at a significant CAGR over the forecast period. This growth can be attributed to its cost-effectiveness, long-standing clinical familiarity, and widespread adoption in conventional implant systems across global dental practices. In addition, External Hex implants are relatively simpler in design and easier to manufacture and restore, making them a preferred choice in price-sensitive markets and for routine implant procedures. Their compatibility with a wide range of prosthetic components and established clinical protocols further supports their continued usage in general dentistry and training institutions.

Implant Structure Insights

The two-piece implants segment led the dental implants industry, accounting for the largest revenue share of 90.9% in 2025, driven by their superior clinical flexibility and widespread adoption in complex dental restoration procedures. Two-piece implant systems allow independent placement of the implant fixture and abutment, enabling better customization of prosthetic components, improved angulation correction, and enhanced aesthetic outcomes, particularly in anterior restorations. In addition, their strong osseointegration performance and suitability for delayed loading protocols make them the preferred choice among dental professionals for long-term treatment success.

The one-piece implants segment is expected to grow at the fastest CAGR over the forecast period, driven by their cost-effectiveness, simplified surgical procedure, and reduced treatment time compared to multi-component implant systems. These implants are preferred in cases requiring single-stage placement, as they eliminate the need for abutment connections, thereby reducing overall procedural complexity and chair time. In addition, their growing adoption in small dental clinics and price-sensitive markets is supported by improved clinical outcomes in selected indications and advancements in implant design that enhance stability.

Price Tier Insights

The premium implants segment led the market with the largest revenue share of 46.1% in 2025, driven by the strong preference for advanced implant systems that offer higher success rates, improved biocompatibility, and superior long-term clinical outcomes compared to standard or value-based alternatives. Premium implants are widely adopted in complex restorative procedures due to their enhanced design precision, surface treatments, and compatibility with digital workflows, which improve osseointegration and overall treatment predictability. In March 2025, Dentsply Sirona announced the U.S. launch of the MIS LYNX all-in-one premium dental implant developed by MIS Implants Technologies. The system was positioned as a cost-effective yet high-performance solution for a wide range of clinical applications, including immediate placement in extraction sockets. These advancements are expected to further reinforce the dominance of premium implants by increasing clinical confidence, treatment success rates, and adoption in complex dental procedures.

The value/economy implants segment is expected to grow at the fastest CAGR over the forecast period, driven by the increasing demand for cost-effective dental restoration solutions, particularly in price-sensitive emerging markets where affordability plays a key role in treatment decisions. These implants strike a balance between acceptable clinical performance and lower overall treatment costs, making them attractive to a wider patient base. In addition, rising out-of-pocket dental costs and limited insurance coverage for advanced dental procedures are encouraging patients to opt for more economical implant options rather than premium systems. The expansion of low-cost dental service providers and the growing adoption of standardized, mass-produced implant components are further supporting segment growth.

Age Group Insights

The adult segment led the dental implants market, accounting for the largest revenue share of 54.6% in 2025, driven by the higher prevalence of tooth loss among middle-aged and older adults. Factors such as periodontal disease, dental caries, trauma, and age-related edentulism significantly increase implant demand in this group. In addition, growing awareness of oral aesthetics and the functional benefits of dental implants is encouraging adults to opt for permanent tooth replacement solutions over removable dentures. Improved affordability, wider insurance coverage in developed markets, and the expansion of outpatient and minimally invasive implant procedures have further supported adoption.

The geriatric segment is expected to grow at the fastest CAGR over the forecast period, driven by the rising global aging population and the increasing prevalence of tooth loss, edentulism, and age-related oral health disorders. Older adults are more likely to require tooth replacement due to long-term dental decay, periodontal diseases, and reduced bone density. For instance, in October 2025, according to the World Health Organization (WHO), around 1 in 6 people globally will be aged 60 years or older by 2030, significantly expanding the target patient base for dental implant procedures. In addition, improved healthcare access and higher adoption of advanced dental care among elderly populations are further supporting market growth.

Distribution Channel Insights

The direct sales segment led the dental implants industry with the largest revenue share of 61.2% in 2025, driven by the dominance of manufacturer-to-clinic distribution models in the dental implants market, where implants are highly specialized, technique-sensitive products that require close technical coordination between suppliers and clinicians. This channel is preferred because it enables real-time product customization support, clinical training, and immediate troubleshooting during implant procedures, which are critical for treatment success.

The digital procurement platforms segment is expected to grow at a significant CAGR over the forecast period, driven by the increasing adoption of e-commerce-like purchasing models in the dental industry, which enable clinics and hospitals to efficiently compare, source, and order dental implant products through centralized online systems. These platforms improve procurement transparency, reduce purchasing time, and allow dental professionals to access a wider range of implant systems, components, and pricing options through a single interface. For instance, platforms such as Henry Schein One and Benco Dental Supply Company. They are widely used in healthcare supply chains to streamline ordering, improve inventory visibility, and reduce procurement costs across hospitals and clinics.

End Use Insights

The dental clinics (including independent clinics and DSO-affiliated clinics) segment led the market with the largest revenue share of 82.3% in 2025, driven by the rapid expansion of organized dental clinic networks, particularly through large-scale multi-location rollouts by established dental chains, which significantly enhance access to dental implant services across urban and semi-urban regions. For instance, in February 2026, Clove Dental launched 48 clinics in a single day, marking its 15-year milestone and expanding its network to 715 centers across 26 cities. The expansion was described as the largest single-day rollout in India’s organized dental sector. The company strengthened its nationwide presence with this rapid growth push. This expansion is expected to further enhance access to implant care and sustain the dominance of dental clinics in the market.

The hospitals segment is expected to grow at a significant CAGR over the forecast period, driven by the rising establishment of dedicated dental and maxillofacial departments within multi-specialty hospitals, which enhance access to advanced surgical care and complex implant procedures. For instance, in January 2026, NewEra Hospitals launched a Dental Care Department at its Vashi facility in Navi Mumbai, strengthening regional oral healthcare delivery by upgrading its infrastructure and offering services ranging from routine dental check-ups to advanced oral and maxillofacial procedures. This expansion is expected to strengthen hospital-based dental care infrastructure and support the steady growth of the hospitals segment.

“With the launch of its advanced dental care department, NewEra Hospitals has strengthened its commitment to delivering quality healthcare. This initiative is expected to greatly benefit residents of Navi Mumbai by making modern dental and oral healthcare more accessible, timely, and patient-centric,” - Dr Mataprasad B Gupta, Vice President & CEO.

Material Insights

The titanium segment led the dental implants market, accounting for the largest revenue share of 91.0% in 2025, due to its exceptional biocompatibility, mechanical strength, and corrosion resistance. Dental professionals widely prefer titanium implants as they offer excellent osseointegration, ensuring long-term stability and durability within the jawbone. Their proven clinical success, extensive research support, and cost-effectiveness compared to newer materials have further strengthened their market position. Moreover, the development of titanium alloys and surface-treated variants has enhanced their performance, promoting faster healing and reduced implant failure rates. These advantages continue to make titanium the material of choice for most dental implant procedures worldwide.

The zirconia segment is expected to grow at the fastest CAGR over the forecast period, driven by rising demand for metal-free, highly aesthetic, and biocompatible alternatives to traditional titanium implants. Zirconia implants offer a superior tooth-colored appearance, making them ideal for patients with thin gingival tissue or high esthetic expectations. In addition, their excellent corrosion resistance, low plaque accumulation, and non-allergenic properties make them suitable for individuals with metal sensitivities. Advances in material processing and surface modification technologies have significantly improved zirconia’s mechanical strength and osseointegration capabilities, addressing earlier concerns about brittleness. The growing shift toward minimally invasive and aesthetically pleasing dental restorations, combined with increasing clinical validation of zirconia’s long-term performance, is expected to drive rapid expansion of the segment.

Regional Insights

North America dominated the dental implants market with the largest revenue share of 36.1% in 2025, driven by the strong presence of leading manufacturers, advanced healthcare infrastructure, and high adoption of digital dentistry technologies. The region benefits from a large pool of trained dental professionals, the widespread use of CAD/CAM systems, 3D printing, and guided implant surgery, as well as increasing patient awareness of aesthetic and restorative dental procedures. Favorable reimbursement policies, rising dental expenditure, and high prevalence of oral diseases and tooth loss further support market growth. Furthermore, continuous product innovations by key players such as Dentsply Sirona, Zimmer Biomet, and Straumann contribute to technological leadership in the region. North America remains the global hub for research, product development, and adoption of advanced dental implant solutions.

U.S. Dental Implants Market Trends

The U.S. dental implants industry is growing, primarily driven by the rising incidence of oral cavity and oropharyngeal cancers, resulting in tooth loss, jawbone deterioration, and oral tissue damage. Patients undergoing cancer treatments such as surgery or radiation frequently require oral rehabilitation to restore function and aesthetics, creating a strong demand for advanced dental implant solutions. Modern implants, supported by digital imaging, guided surgery, and bone regeneration techniques, have enabled precise, long-term restorative outcomes for post-cancer patients. In addition, growing awareness about quality-of-life improvement and expanding insurance coverage for reconstructive dental procedures further support market growth. As the prevalence of head and neck cancers continues to rise, the demand for durable, biocompatible, and aesthetic dental implant systems in the U.S. is expected to increase significantly.

According to the CDC, 2024 Oral Health Surveillance Report

-

Ages 2-5: 11% had untreated decay; higher in Mexican American (18.5%) and high-poverty (18%) groups. Avg: 1.8 decayed, 2.6 filled teeth.

-

Ages 6-8: 18% had untreated decay; prevalence was higher in high- (24.6%) and middle-poverty (24.8%) vs. low-poverty (11.6%). Avg: 0.9 decayed, 3.2 filled teeth.

-

Ages 6-9: 50% had cavities; 17% untreated decay. High-poverty (26.3%) and middle-poverty (23.4%) > low-poverty (10%). Mexican American (70.3%) > White (43.4%).

The American Cancer Society’s most recent estimates for oral cavity and oropharyngeal cancers in the U.S. are for 2025

-

About 59,660 new cases of oral cavity or oropharyngeal cancer

-

About 12,770 deaths from oral cavity or oropharyngeal cancer

Europe Dental Implants Market Trends

The dental implants industry in Europe is experiencing growth driven by the rising prevalence of tooth loss, growing awareness of oral rehabilitation, and advancements in digital dentistry. The region benefits from a strong base of practicing dentists and well-established clinical infrastructure, particularly in countries such as the UK, Germany, Italy, Spain, and France. The growing number of dental practitioners supported by expanding dental service organizations and group practices has significantly enhanced access to implant procedures across the region. In addition, increasing adoption of computer-guided surgery, CAD/CAM systems, and digital imaging has improved treatment precision and efficiency, further boosting implant demand. The rising preference for aesthetic restorations and the aging population continue to support market growth, making Europe one of the most technologically advanced and mature regions in the global dental implant landscape.

Dentists Practicing, 2022

Country

Dentists (number)

Dentists (per 100,000)

Denmark

4,205

71.8

Germany

71,297

85.1

Spain

28,833

60.4

France

45,989

67.6

Italy

52,559

89.1

Norway

4,792

87.8

Source: Eurostat

The UK dental implants market is primarily driven by the growing incidence of tooth extractions and dental caries. The high prevalence of dental decay, driven by poor oral hygiene, unhealthy dietary habits, and lifestyle factors, has increased the need for tooth-replacement solutions. As more patients undergo extractions due to untreated cavities or advanced periodontal diseases, the demand for long-term restorative options such as dental implants continues to rise. In addition, increasing awareness about implants' functional and aesthetic advantages over traditional dentures and bridges influences patient preference and clinical practice. The National Health Service (NHS) and private dental clinics are witnessing a rise in implant procedures, supported by advancements in digital dentistry, improved implant materials, and a growing population seeking permanent tooth replacement solutions.

As per the Office for Health Improvement & Disparities UK, in May 2023

-

42,180 total hospital episodes of tooth extractions were recorded for children and young people aged 0-19 years.

-

26,741 episodes (63%) had a primary diagnosis of dental caries (tooth decay).

-

There was an 83% increase in caries-related tooth extraction episodes compared to 2020-2021.

-

Highest rates: Yorkshire and the Humber - 378 per 100,000 population

-

Lowest rates: East Midlands - 71 per 100,000 population

-

England average: 205 per 100,000 population

The dental implants market in Germany is experiencing growth driven by the increasing prevalence of oral cancers and other health-related issues. A significant portion of the German population suffers from conditions such as periodontitis, tooth loss due to decay, and complications from oral cancer treatments that often result in the need for tooth replacement. The growing number of oral cancer cases, particularly among aging adults and smokers, has increased the demand for advanced restorative and reconstructive dental solutions. Dental implants are preferred for post-oncological rehabilitation, as they restore functionality and aesthetics, improving patients’ quality of life after surgery or radiation therapy. Moreover, Germany’s well-established dental infrastructure, high number of practicing dentists, and strong emphasis on preventive and restorative dental care support the adoption of implant therapies.

Asia Pacific Dental Implants Market Trends

The Asia Pacific dental implants industry is experiencing rapid growth, driven by rising oral health awareness, an expanding elderly population, and increasing disposable incomes across emerging economies, including China, India, and Thailand. The growing incidence of tooth loss, dental caries, and periodontal diseases is boosting the demand for long-term restorative solutions. In addition, the region’s improving healthcare infrastructure, the growing number of skilled dental professionals, and the surge in dental tourism, particularly in countries like India and South Korea, are making implant treatments more accessible and affordable. Adopting advanced technologies such as digital dentistry, CAD/CAM systems, and guided implant surgery further enhances clinical precision and treatment efficiency. Moreover, favorable government initiatives, the expansion of private dental chains, and the introduction of cost-effective implant materials, such as zirconia, are strengthening market growth.

The India dental implants market is witnessing growth, primarily driven by the increasing burden of oral health problems across the country. A large segment of the population continues to experience oral diseases such as dental caries, periodontal disease, tooth decay, and tooth loss conditions exacerbated by poor oral hygiene practices, high sugar intake, and widespread tobacco use. These issues have significantly increased the need for effective restorative dental solutions. Dental implants are the preferred treatment option due to their superior durability, functionality, and natural appearance compared to traditional dentures or bridges. In addition, growing awareness of oral health, rising disposable incomes, and improved access to advanced dental care, especially in urban centers, are accelerating market adoption. The rapid expansion of private dental clinics, greater availability of cost-effective implant systems, and the presence of both domestic and global dental manufacturers are further strengthening market growth.

Oral Health Burden in India (2022)

Oral Health Condition

Number of Cases in India

Percentage of Global Cases (%)

Caries of Permanent Teeth

366,858,183

18.1

Severe Periodontal Disease

221,084,427

20.3

Caries of Deciduous Teeth

98,199,025

18.9

Edentulism

34,905,533

9.9

Lip and Oral Cavity Cancer

327,648

23.4

Source: Global Oral Health Status Report (GOHSR)

The dental implants market in China is experiencing growth, driven by a rising oral health awareness, increasing disposable incomes, and expanding access to advanced dental care. A growing prevalence of oral diseases such as tooth decay, periodontal disorders, and tooth loss, particularly among the aging population, has significantly increased the demand for restorative dental procedures. Government initiatives promoting oral health, such as the “Healthy China 2030” plan, further enhance public awareness and encourage preventive dental care. Moreover, the expansion of dental clinics, the modernization of dental hospitals, and the increasing adoption of digital dentistry technologies such as CAD/CAM systems and 3D printing transform treatment practices and improve procedural outcomes. Domestic manufacturers are also playing a key role by offering affordable implant systems tailored to local market needs.

Middle East and Africa Dental Implants Market Trends

The Middle East & Africa dental implants industry is experiencing growth, driven by improvements in healthcare infrastructure, rising awareness of oral health, and increasing demand for advanced restorative dental solutions. The growing prevalence of tooth loss, periodontal diseases, and dental caries, combined with an increasing geriatric population, has significantly increased the adoption of dental implants across the region. Countries such as the UAE, Saudi Arabia, and South Africa are leading the market, supported by well-established dental care facilities, strong government healthcare initiatives, and a growing focus on aesthetic dentistry. In addition, the rise of dental tourism, particularly in the Gulf region, and the increasing disposable income among the middle class are fueling market expansion.

Key Dental Implants Company Insights

Industry players are focusing on expanding their product portfolio by launching innovative products. In addition, they are adopting advanced technologies and acquiring other players to strengthen their position in the market.

Key Dental Implants Companies

The following key companies have been profiled for this study of the dental implants market.

-

BioHorizons

-

Nobel Biocare (Envista)

-

ZimVie Inc.

-

Osstem Implant

-

Institut Straumann AG

-

Bicon, LLC

-

Leader Medica

-

Dentsply Sirona

-

Dentis

-

Dentium Co., Ltd.

-

T-Plus Implant Tech Co., Ltd.

-

Kyocera Medical Corp

-

Double Medical Technology Inc.

-

Bioconcept Dental Implants

-

Neoss Ltd.

-

Southern Implants

-

Glidewell

-

Keystone Dental Group

-

MEGA’GEN IMPLANT CO., LTD

-

OCO Biomedical

-

Park Dental Research

-

Zest Dental Solutions

-

Hiossen Implant

-

Implant Direct

-

Noris Medical

-

Nuventus AG

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Established Players (Institut Straumann AG, Nobel Biocare (Envista), Dentsply Sirona, ZimVie Inc., Osstem Implant)

- Invest heavily in R&D to develop advanced dental implant systems, implant surface technologies, digital treatment planning software, and CAD/CAM prosthetics.

- Expand global presence through strategic acquisitions, partnerships with dental clinics, DSOs, and universities.

- Strong global brand recognition, extensive clinical evidence, and well-established distribution networks.

- Broad product portfolios covering dental implants and guided implant surgery solutions provide a strong competitive position.

- High R&D investment, manufacturing costs, and stringent regulatory compliance increase operational expenses.

- Premium pricing of advanced implant systems limits adoption in price-sensitive markets.

Emerging Players (BioHorizons, Bicon, LLC, Dentis, Dentium Co., Ltd., Leader Medica)

- Focus on expanding cost-effective implant systems, localized manufacturing, and specialized implant solutions for regional markets.

- Strengthen distribution through partnerships with dental clinics, laboratories, and regional distributors.

- Competitive pricing, operational flexibility, and the ability to respond quickly to regional customer requirements.

- Strong presence in selected markets and specialized implant solutions help increase adoption among independent dental clinics and emerging healthcare markets.

- Limited global brand recognition and smaller international distribution networks compared to established manufacturers.

- Lower investment capacity for large-scale clinical research and global marketing initiatives.

Recent Developments

-

In June 2026, BioHorizons launched its Pro Zygoma Implant, expanding its remote anchorage portfolio for advanced full-arch dental procedures. The implant was designed for immediate placement in severely resorbed maxillae, aimed at improving clinical predictability, reducing chair time, and enabling graftless treatment workflows.

“This product launch allows us to offer more solutions to our customers, giving them a new, versatile option for providing life-changing treatment in dense zygomatic bone. And with Vulcan Custom Dental, we provide clinicians comprehensive support from treatment planning to restoration.”-Steve Boggan, president and CEO of BioHorizons

-

In July 2025, ZimVie Inc. announced a strategic distribution partnership with Osstem Implant Co., Ltd. (“Osstem Implant”), a prominent provider of high-quality dental implants and integrated dental technologies worldwide. This collaboration aims to strengthen ZimVie's global footprint by expanding into the rapidly growing Chinese implant market, which is estimated to exceed 10 million units sold annually, and to improve customer access to its innovative range of implant solutions.

-

In June 2025, INSTITUT STRAUMANN AG will invest USD 76 to 102 million on the Villeret site in Switzerland over the next five years. Villeret will continue to focus on the production of high-value-added products, including the newly launched iEXCEL high-performance implant system.

-

In March 2025, Dentsply Sirona announced its participation in the Academy of Osseointegration’s (AO) Annual Meeting 2025, scheduled for March 27-29 in Seattle, WA. At the event, the company showcased its newest innovation, the MIS LYNX implant, and hosted a Corporate Forum centered on the continued evolution of implant dentistry.

Dental Implants Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 5.6 billion

Estimated market size in 2026

USD 6.0 billion

Projected market size by 2033

USD 11.0 billion

Growth rate

CAGR of 9.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Surface treatment type, material, design, connection type, implant structure, price tier, distribution channel, end use, age group, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa (MEA)

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; South Korea; Australia; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

BioHorizons; Nobel Biocare (Envista); ZimVie Inc.; Osstem Implant; Institut Straumann AG; Bicon, LLC; Leader Medica; Dentsply Sirona; Dentis; Dentium Co., Ltd.; T-Plus Implant Tech Co. Ltd.; Kyocera Medical Corp; MEGA’GEN IMPLANT CO.,LTD, Double Medical Technology Inc.; Bioconcept Dental Implants; Neoss Ltd.; Southern Implants; Glidewell; Keystone Dental Group; OCO Biomedical; Park Dental Research; Zest Dental Solutions; Hiossen Implant; Implant Direct; Noris Medical; Nuventus AG

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Dental Implants Market Report Segmentation

This report forecasts revenue growth at the global, regional & country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global dental implants market report based on surface treatment type, material, design, connection type, implant structure, price tier, distribution channel, end use, age group, and region:

-

Surface Treatment Type Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

SLA and SLActive

-

Anodized Surfaces

-

Nano-Textured Surfaces

-

Others

-

-

Material Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Titanium

-

Commercially Pure Titanium (cpTi)

-

Titanium Alloy (Ti-6Al-4V)

-

Titanium-Zirconium Alloy (Ti-Zr)

-

-

Zirconia

-

Y-TZP Zirconia

-

Alumina-Toughened Zirconia (ATZ)

-

-

-

Design Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Tapered

-

Parallel-Walled

-

Others

-

-

Connection Type Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Conical (Morse Taper) Connection

-

CM 11.5° (Classic Morse Taper)

-

CM 16° (Modern/Grand Morse)

-

-

External Hex (HE)

-

Internal Hex (IH)

-

Other Specialized Interfaces (Tri-Channel, Internal Octagon, No Connection (One Piece), among others)

-

-

Implant Structure Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Two-piece

-

One-Piece

-

-

Price Tier Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Premium Implants

-

Mid-Range Implants

-

Value/Economy Implants

-

-

Age Group Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Adult

-

Geriatric

-

-

Distribution Channel Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Direct Sales

-

Distributors

-

Group Purchasing Organizations (GPOs)

-

Digital Procurement Platforms

-

-

End Use Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Dental Clinics (includes independent clinics and DSO-affiliated clinics)

-

Hospitals

-

Academic & Research Institutes

-

-

Regional Outlook (Revenue, USD Million/Billion, 2021–2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

Segment Definition

Segment - Material

Revenue capture definition

Titanium

Revenue generated from the sale of titanium dental implants, including commercially pure titanium and titanium alloy implant systems used for single-tooth, multiple-tooth, and full-arch restorations. This segment includes titanium implant fixtures due to their high biocompatibility, strength, durability, and proven osseointegration.

Zirconia

Revenue generated from the sale of zirconia dental implants, including one-piece and two-piece zirconia implant systems used for aesthetic and metal-free dental restorations. This segment covers zirconia implants that offer excellent aesthetics, biocompatibility, and corrosion resistance and are increasingly adopted by patients seeking metal-free treatment options.

Estimation Model

Layer Name

Key Question

Description

Bottom-Up

Bottom-Up Estimation

Revenue is estimated by aggregating the sales of dental implants across dental clinics, hospitals, implantology centers, dental service organizations (DSOs), and specialty dental practices at the country, regional, and global levels. The analysis considers the number of implant procedures performed for single-tooth replacement, multiple-tooth replacement, and full-arch restorations, along with the adoption of titanium and zirconia implant systems, and related prosthetic components.

Top-Down

Top-Down Approach

The overall dental devices and restorative dentistry market is assessed first, followed by estimating the share attributable to dental implants using secondary research and expert validation. Key market indicators such as the prevalence of tooth loss, aging population, incidence of periodontal disease, demand for cosmetic dentistry, dental tourism, implant procedure volumes, and patient access to advanced restorative care are analyzed to determine the contribution of the dental implants segment.

Supply-Side

Supply-Side Analysis

This approach evaluates the total production and sales of dental implants by implant manufacturers, abutment and prosthetic component suppliers, and dental laboratories worldwide. Key parameters include manufacturing capacity, production volumes, utilization of titanium and zirconia materials, average selling prices, product portfolios, distribution networks, regional sales performance, and adoption of digital implant planning, guided surgery, and CAD/CAM prosthetic workflows to estimate the overall market size.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Dental Implants Market Share, Pricing & Portfolio Benchmarking

Delivered a detailed competitive assessment of the global Dental Implants Market, benchmarking leading manufacturers based on implant system revenue, estimated procedure volumes, average selling prices (ASP), product portfolio breadth, and regional market share. The study evaluated premium, value, and economy implant systems, digital implant workflows, and customer reach across key geographic markets.

Enables stakeholders to compare market positioning, identify pricing strategies, evaluate portfolio competitiveness, and understand revenue opportunities across premium and value implant segments. The analysis supports strategic planning for product positioning, regional expansion, and competitive differentiation.

Innovation & Technology Assessment – Dental Implants Market

Conducted an in-depth analysis of technological advancements shaping the dental implants industry, including implant surface technologies, biomaterials, immediate loading solutions, digital treatment planning, guided implant surgery, CAD/CAM prosthetics, and 3D printing applications. The assessment reviewed innovation pipelines, patent activity, clinical developments, and company-specific R&D strategies across major implant manufacturers.

Provides insights into technology leadership, innovation intensity, product differentiation, and commercialization potential. The study helps clients identify emerging technologies, evaluate partnership and acquisition opportunities, and understand future competitive trends influencing long-term market growth.

Dental Implants Manufacturing, Supply Chain & Procurement Analysis

Performed a comprehensive assessment of dental implant manufacturing capabilities, titanium and zirconia raw material sourcing, precision machining, surface treatment technologies, sterilization processes, packaging, and global supply chain strategies. The study also evaluated manufacturing efficiency, quality control systems, production scalability, supplier networks, and cost optimization initiatives adopted by leading manufacturers.

Supports sourcing, procurement, and investment decisions by identifying resilient supply chain models, efficient manufacturing strategies, and cost optimization opportunities. The analysis enables stakeholders to assess operational risks, manufacturing scalability, margin sustainability, and long-term competitiveness in the global dental implants market.

Frequently Asked Questions About This Report

The global dental implants market size was valued at USD 5.6 billion in 2025 and is estimated at USD 6.0 billion for 2026.

The global dental implants market is expected to grow at a CAGR of 9.0% from 2026 to 2033, reaching USD 11.0 billion by 2033.

North America dominated the dental implants market with the largest revenue share of 36.1% in 2025. The aging population is prone to tooth loss and tooth decay due to various medications prescribed to them. Hence, the region is expected to influence the dental implant market to a large extent due to its high geriatric population demanding oral care services.

Key players include BioHorizons; Nobel Biocare (Envista); ZimVie Inc.; Osstem Implant; Institut Straumann AG; Bicon, LLC; Leader Medica; Dentsply Sirona; Dentis; Dentium Co., Ltd.; T-Plus Implant Tech Co. Ltd.; Kyocera Medical Corp; Double Medical Technology Inc.; Bioconcept Dental Implants; Neoss Ltd.; Southern Implants.

Increasing applications of dental implants in various therapeutic areas along with increasing demand for prosthetics are some of the key factors expected to boost the market growth.

Asia Pacific is the fastest-growing region over the forecast period.

SLA and SLActive segment held the largest share (over 37.0%) in 2025, while nano-textured surfaces is the fastest-growing type.

The tapered segment led with a 69.8% revenue share in 2025, while parallel-walled is the fastest-growing design.

The titanium segment led with a 91.0% revenue share in 2025, while zirconia is the fastest-growing material.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.