- Home

- »

- Next Generation Technologies

- »

-

Digital Security Control Market Size Report, 2025-2030GVR Report cover

![Digital Security Control Market (2025 - 2033)Report]()

Digital Security Control Market (2025 - 2033)

Size, Share & Trends Analysis Report By Hardware (Smart Card, Sim Card), By Technology, By Application (User Authentication, Network Monitoring), By End-use (Healthcare, Commercial), By Region, And Segment Forecasts

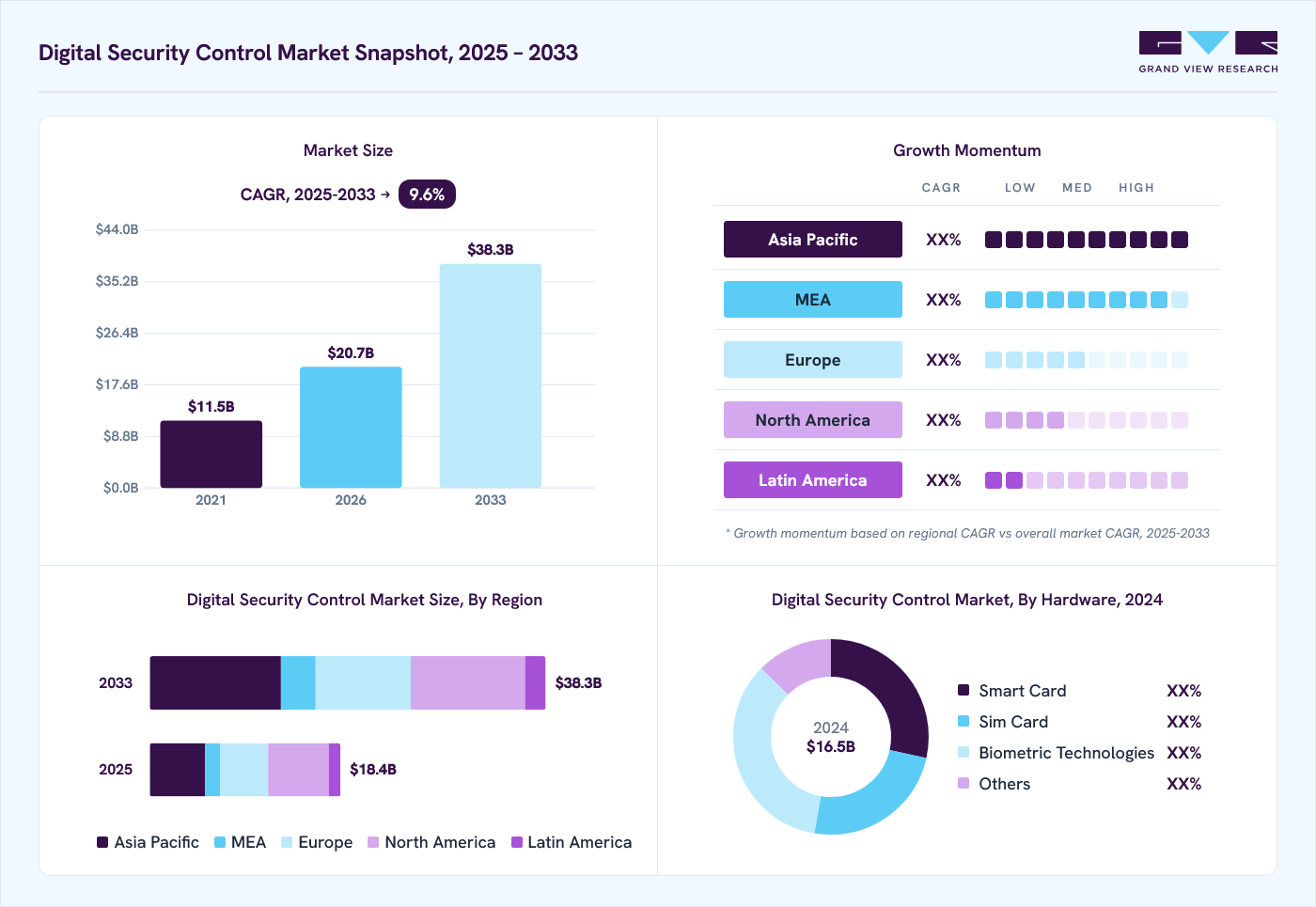

Market Size, 2024

$16.5BMarket Estimate, 2026

$20.7BMarket Forecast, 2033

$38.3BCAGR, 2025–2033

9.6%Digital Security Control Market Summary

The global digital security control market size was valued at USD 16.5 billion in 2024 and is projected to grow from USD 20.7 billion in 2026 to USD 38.3 billion by 2030, at a CAGR of 9.6% from 2025 to 2030. North America dominated the market, accounting for a revenue share of 32.2% in 2024. The digital security control market is growing due to the rising adoption of biometric authentication.

Key Market Trends & Insights

- The digital security control market in the U.S. is expected to grow significantly over the forecast period.

- By hardware, biometric technologies led the market and held the largest revenue share of 34.6% in 2024.

- By technology, the two-factor authentication segment held the dominant position in the market and accounted for the largest revenue share of 58.4% in 2024.

- By application, the user authentication segment held the dominant position in the market and accounted for the largest revenue share of 34.3% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 16.5 Billion

- 2033 Projected Market Size: USD 38.3 Billion

- CAGR (2025-2033): 9.6%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Technologies such as fingerprint, facial, and iris recognition are being widely implemented across access control systems. This shift is driven by the need for stronger, more seamless authentication, boosting demand across sectors.The digital security market is experiencing growth through the integration of advanced technologies. Companies are increasingly adopting AI and IT services to improve security capabilities. This includes enhanced identity verification and secure transaction processing. Advanced solutions are also being used to protect sensitive data more effectively. Such developments are contributing to the overall expansion of the market. As threats become more complex, organizations are prioritizing smarter, more adaptive security frameworks. For instance, in June 2024, Entrust Corporation, a U.S.-based software company, collaborated with Wipro to enhance its digital security offerings. Through this strategic collaboration, Wipro is providing AI and IT services to support Entrust’s expansion in identity, payment, and data protection solutions.

")

The adoption of integrated biometric authentication solutions supports the growth of the digital security control market. These technologies improve identity verification accuracy and reduce the chances of unauthorized access. Combining modalities such as fingerprint, facial, and voice recognition enhances overall system reliability. This builds greater trust in digital platforms used in sectors such as banking, healthcare, and corporate services.

Traditional security methods are being replaced as organizations seek more robust authentication frameworks. Increased focus on secure access is accelerating investments in advanced biometric systems. In January 2025, Fingerprint Cards AB, a Swedish biometrics company, collaborated with jNet Secure to develop a turnkey biometric System-in-Package (SiP) module for secure digital authentication. This collaboration targets sectors such as enterprise access, financial services, and government ID by offering a password-less, cryptography-based solution that simplifies integration and accelerates adoption.

The accelerated digitalization of both public and private sector operations continues to push the boundaries of connectivity, automation, and data exchange. As more core functions transition to cloud-based environments and digital platforms, the exposure to cyber threats grows significantly. The need for advanced digital security controls is therefore intensifying, prompting organizations to invest in comprehensive security architectures.

These controls help mitigate risks tied to unauthorized access, data breaches, and malicious cyber activities, especially in remote work scenarios. Governments are also implementing stricter regulations around data privacy and security, further driving adoption of sophisticated cloud and endpoint security tools. This evolving regulatory and threat landscape reinforces the importance of scalable, real-time, and AI-driven security solutions capable of safeguarding modern digital ecosystems.

Hardware Insights

The biometric technologies segment dominated the market with a revenue share of 34.6% in 2024. This segment is experiencing rapid growth in the digital security control market due to its unmatched ability to provide secure and convenient access control solutions. Biometrics, such as fingerprint, facial recognition, iris scanning, and voice recognition, offer highly reliable methods of verifying individual identities, significantly enhancing security measures compared to traditional password-based systems.

As cyber threats evolve and traditional authentication methods prove increasingly vulnerable to hacking and fraud, organizations across various sectors, including finance, healthcare, and government, are turning to biometric technologies to strengthen their defenses. Moreover, the growing adoption of mobile devices and IoT (Internet of Things) has further fueled demand for biometric solutions that can seamlessly integrate with these technologies, offering users a frictionless and secure experience.

The smart cards segment is projected to grow significantly over the forecast period. Smart cards, equipped with embedded microprocessors and memory chips, offer robust security features such as encryption and biometric authentication, making them ideal for securing access to physical and digital assets. They are widely adopted across various industries, including banking, healthcare, government, and transportation, for applications such as payment cards, identification cards, and access control.

With increasing digitalization and cybersecurity threats, organizations are increasingly turning to smart cards to enhance security measures and protect sensitive information. The convenience, reliability, and scalability of smart card technology contribute to its continued growth in the digital security control market, addressing the evolving security needs of both enterprises and consumers alike.

Technology Insights

The two-factor authentication segment accounted for the largest revenue share in 2024. This segment’s growth is primarily due to its effectiveness in enhancing security beyond traditional password-based systems. Two-factor authentication improves security by requiring users to confirm their identity using two separate factors: usually, information they remember (such as a password) and something they have (like a mobile device or hardware token). This approach significantly reduces the risk of unauthorized access, data breaches, and identity theft, which are increasingly common in today's digital landscape. As businesses and individuals alike prioritize stronger security measures to protect sensitive information and comply with regulatory requirements, the demand for Two-Factor Authentication has surged.

The three-factor authentication segment is predicted to experience significant growth in the forecast period. This technology is experiencing growth in the digital security control market due to its heightened level of security and resilience against sophisticated cyber threats. Unlike traditional authentication methods that rely on just a username and password, Three-Factor Authentication adds a layer of verification, typically involving something the user knows, something they have, and something they are (biometric factors like fingerprint or facial recognition). This triple-layered approach significantly enhances security by requiring multiple proofs of identity, thereby reducing the risk of unauthorized access and data breaches. As businesses and organizations face increasingly sophisticated cyberattacks and regulatory pressures to strengthen data protection measures, Three-Factor Authentication offers a robust solution to mitigate these risks.

Application Insights

The user authentication segment accounted for the largest revenue share in 2024, due to its fundamental role in safeguarding sensitive data and resources from unauthorized access. As organizations across industries shift towards digital transformation and cloud-based services, the need for reliable and secure methods of verifying user identities has become paramount.

User authentication technologies, including password-based systems, biometric verification (such as fingerprint or facial recognition), and multi-factor authentication (MFA), offer varying levels of security to protect against identity theft, cyber-attacks, and data breaches. The segment's dominance is further driven by regulatory compliance requirements, such as GDPR in Europe and CCPA in California, which mandate robust authentication measures to protect personal and confidential information.

The network monitoring segment is projected to grow significantly over the forecast period. As businesses expand their digital footprint and embrace technologies such as cloud computing, IoT (Internet of Things), and remote work, the attack surface for cyber threats expands exponentially. Network Monitoring solutions continuously monitor network traffic, detect anomalies, and identify potential security breaches in real-time.

This proactive approach enables organizations to swiftly respond to security incidents, mitigate risks, and minimize the impact of cyber-attacks on their operations and data. Moreover, regulatory requirements such as GDPR, HIPAA, and others mandate stringent data protection measures, including robust network monitoring capabilities, to ensure compliance and protect sensitive information. As the threat landscape evolves with more sophisticated and persistent cyber threats, the demand for advanced Network Monitoring solutions continues to grow, making it an essential component of comprehensive digital security strategies across industries.

End-use Insights

The finance and banking segment accounted for the largest revenue share in 2024. This segment is growing in the digital security control market primarily due to the sector's heightened vulnerability to cyber threats and the critical importance of protecting financial transactions and sensitive customer data. As financial institutions increasingly digitize their services and adopt cloud-based solutions to enhance operational efficiency and customer experience, they simultaneously face escalating risks from cybercriminals targeting financial data and assets.

Moreover, the rapid adoption of mobile banking and online payment platforms has expanded the attack surface, necessitating stronger defenses against phishing, malware, and other sophisticated cyber-attacks. The Finance and Banking segment's growth in the digital security control market is thus driven by the imperative to safeguard financial transactions, maintain regulatory compliance, and uphold trust and credibility among customers in an increasingly interconnected digital economy.

The commercial segment is projected to grow significantly over the forecast period. Businesses across various industries, including retail, manufacturing, hospitality, and services, are increasingly digitizing their operations and utilizing technology to streamline processes and enhance customer engagement. This digital transformation exposes them to a wider range of cyber threats, including data breaches, ransomware attacks, and phishing scams. As a result, there is a heightened awareness among commercial enterprises about the importance of securing sensitive data, customer information, and intellectual property.

Moreover, the adoption of cloud computing, IoT devices, and mobile technologies in commercial environments expands the attack surface, necessitating robust cybersecurity measures to safeguard interconnected networks and endpoints. The imperative, therefore, drives the Commercial segment's growth in the digital security control market to mitigate cyber risks, ensure business continuity, and maintain trust and confidence among customers and stakeholders in an increasingly interconnected and digital business sector.

Regional Insights

The North America digital security control market held the dominant position with a revenue share of 32.2% in 2024. North America's dominance in the digital security control market is driven by its concentration of leading technology firms, driving continuous innovation in cybersecurity solutions. These companies utilize substantial resources for research and development, advancing technologies to combat evolving cyber threats effectively.

The region's stringent regulatory environment, including laws like GDPR and robust federal and state regulations in the U.S., compels organizations to invest in comprehensive security measures to protect data and ensure compliance. North America's strong economy and extensive adoption of digital technologies across diverse sectors amplify the demand for sophisticated cybersecurity solutions.

U.S. Digital Security Control Market Trends

The digital security control market in the U.S. is expected to grow significantly over the forecast period. The digital security control market in the U.S. is poised for substantial growth over the forecast period, driven by increasing cyber threats and widespread adoption of digital technologies across industries. Investments in advanced cybersecurity solutions, including AI-driven threat detection and cloud security services, are expected to escalate as organizations prioritize safeguarding sensitive data.

Europe Digital Security Control Market Trends

The Europe digital security control market is witnessing steady growth, driven by stringent data protection regulations such as the General Data Protection Regulation (GDPR). This regulatory framework has compelled organizations to bolster their cybersecurity measures to protect personal data and avoid hefty fines for non-compliance.

The digital security control market in the UK is experiencing significant growth, driven by rising cybersecurity threats and stringent regulatory requirements such as GDPR. Organizations are increasingly investing in advanced cybersecurity technologies to protect sensitive data and comply with regulatory mandates. The rapid adoption of digital technologies further amplifies the demand for robust security solutions across various sectors.

The digital security control market in Germany held a significant share of the European market. The country's security administration sectors, including automotive, manufacturing, and finance, have stringent security requirements to protect valuable intellectual property and sensitive data. German enterprises typically have a proactive approach toward adopting advanced digital security solutions, driven by the necessity to mitigate evolving cyber threats and maintain operational resilience.

Asia Pacific Digital Security Control Market Trends

The Asia Pacific digital security control market is anticipated to register the fastest CAGR over the forecast period. This growth is driven by increasing digitalization across sectors, rapid adoption of cloud computing and IoT technologies, and rising awareness of cybersecurity threats. As economies in the region continue to expand and innovate, there is a growing emphasis on enhancing digital security measures to protect critical infrastructure, personal data, and intellectual property. This growth is further bolstered by regulatory initiatives aimed at strengthening cybersecurity frameworks and encouraging investments in advanced security solutions to safeguard against emerging cyber risks.

China digital security control market is expected to grow significantly over the forecast period. The rapid digital transformation across various industries in China has heightened the need for robust cybersecurity measures to protect against cyber threats and data breaches. Government initiatives and regulations aimed at enhancing cybersecurity resilience and protecting sensitive information are fostering increased investments in advanced security technologies.

The digital security control market in India is expected to grow substantially over the forecast period. As businesses and organizations in India increasingly embrace digital technologies and cloud computing, there is a heightened demand for advanced security solutions to safeguard against evolving cyber risks and ensure data protection.

Middle East & Africa (MEA) Digital Security Control Market Trends

In the Middle East & Africa (MEA) digital security control market, the proliferation of mobile devices and internet connectivity is significantly expanding the attack surface, compelling organizations to prioritize cybersecurity measures. This heightened focus includes enhancing network monitoring capabilities, deploying secure cloud solutions, and educating stakeholders on cyber hygiene practices to mitigate the risks posed by increasingly sophisticated cyber threats.

Rapid urbanization and digital transformation further drive the adoption of advanced security technologies across sectors such as finance, healthcare, and energy in MEA. This includes substantial investments in AI-driven threat detection, encryption technologies, and multi-factor authentication solutions to enhance security posture and ensure compliance with evolving regulatory requirements.

Key Digital Security Control Company Insights

Some key companies in the digital security control industry include Cisco Systems, Inc., Digital Security Concepts, Fortinet, Inc., Hadrian Security, Linked Security NY, and others. Organizations are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Cisco Systems, Inc. enhances its digital security control through integrated network and endpoint security features. It focuses on protecting hybrid and multi-cloud environments with real-time threat detection. The SecureX platform provides centralized visibility and automates responses across tools. Cisco strengthens its Zero Trust framework to ensure secure access and identity control. It also improves analytics and threat response using AI-based techniques.

-

Microsoft develops digital security controls through Defender and Sentinel to cover endpoints, identities, and cloud environments. It embeds access control through multi-factor authentication and conditional policies. The company uses AI to detect advanced threats and streamline incident response. Microsoft integrates its security tools with Azure to create a unified defense environment. It also supports organizations with built-in compliance and risk management capabilities.

Key Digital Security Control Companies:

The following are the leading companies in the digital security control market. These companies collectively hold the largest market share and dictate industry trends.

- Cisco Systems, Inc.

- Digital Security Concepts

- Fortinet, Inc.

- Hadrian Security

- Linked Security NY

- McAfee, LLC

- Microsoft

- Orbit Security Systems

- Palo Alto Networks

- RSA Security LLC

Recent Developments

-

In May 2024, Palo Alto Networks launched PrismaSASE 3.0, a new software-defined security solution that expands Zero Trust protection to include devices. This update includes an industry-first natively integrated enterprise browser powered by AI for enhanced data security and up to five times faster application performance to address modern enterprise security and operational challenges.

-

In May 2024, Fortinet, Inc. signed a three-year sponsorship agreement with FC Barcelona, a professional football club based in Spain. This partnership aims to enhance digital security at the future Camp Nou stadium using Fortinet's Security Fabric platform.

-

In April 2024, Cisco Systems, Inc. introduced HyperShield, a new security product that utilizes AI to safeguard critical systems. It transforms various IT assets, including virtual machines and Kubernetes clusters in public clouds, into security enforcement points to prevent application exploits and curb hackers' lateral movement, enhancing cyberattack defenses.

Digital Security Control Market Report Scope

Report Attribute

Details

Market size in 2024

USD 16.5 billion

Estimated Market size in 2026

USD 20.7 billion

Projected Market size by 2030

USD 38.3 billion

Growth rate

CAGR of 9.6% from 2025 to 2033

Base year for estimation

2024

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million and CAGR from 2025 to 2033

Report coverage

Revenue forecast, company ranking, competitive sector, growth factors, and trends

Segment scope

Hardware, technology, application, end-use, region

Region scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; Australia; South Korea; Brazil; KSA; UAE; South Africa

Key companies profiled

Cisco Systems, Inc.; Digital Security Concepts; Fortinet, Inc.; Hadrian Security; Linked Security NY; McAfee, LLC; Microsoft, Orbit Security Systems; RSA Security LLC; Vertex Security Systems

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Digital Security Control Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global digital security control market report based on hardware, technology, application, end-use, and region:

-

Hardware Outlook (Revenue, USD Million, 2021 - 2033)

-

Smart Card

-

Sim Card

-

Biometric Technologies

-

Others

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Two-Factor Authentication

-

Three-Factor Authentication

-

Four-Factor Authentication

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Anti-Phishing

-

User Authentication

-

Network Monitoring

-

Security Administration

-

Web Technologies

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Mobile Security and Telecommunication

-

Finance and Banking

-

Healthcare

-

Commercial

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global digital security control market size was valued at USD 16.5 billion in 2024 and is estimated at USD 20.7 billion for 2026.

The global digital security control market is expected to grow at a CAGR of 9.6% from 2025 to 2030, reaching USD 38.3 billion by 2030.

North America dominated the digital security control market with a share of 32.2% in 2024. This is attributable to its advanced technological infrastructure, high cybersecurity awareness, and significant investments in research and development.

Some key players operating in the digital security control market include Cisco Systems, Inc., Digital Security Concepts, Fortinet, Inc., Hadrian Security, Linked Security NY, McAfee, LLC, Microsoft, Orbit Security Systems, Palo Alto Networks, and RSA Security LLC.

Key factors that are driving the market growth include rising cyber threats, stringent regulatory compliance, increased cloud adoption, ongoing digital transformation, and the expansion of remote work.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.