- Home

- »

- Next Generation Technologies

- »

-

Digital Workplace Market Size & Trends Report, 2026-2033GVR Report cover

![Digital Workplace Market (2026 - 2033)Report]()

Digital Workplace Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Solutions, Services), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By End-use (BFSI, Retail & Consumer Goods), By Region, And Segment Forecasts

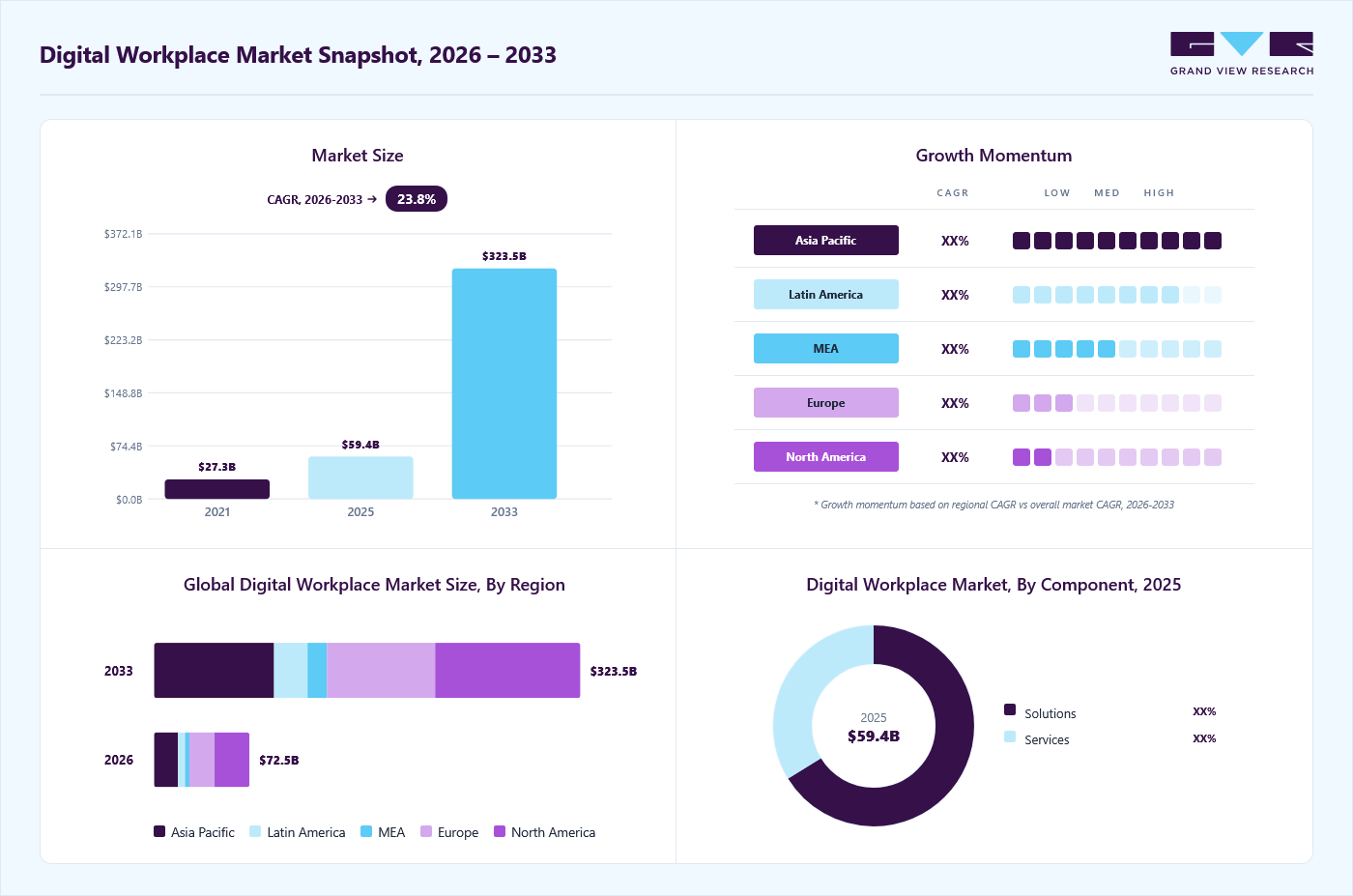

Market Size, 2025

$59.4BMarket Estimate, 2026

$72.5BMarket Forecast, 2033

$323.5BCAGR, 2026–2033

23.8%Digital Workplace Market Summary

The global digital workplace market size was valued at USD 59.4 billion in 2025 and is projected to grow from USD 72.5 billion in 2026 to USD 323.5 billion by 2033, at a CAGR of 23.8% from 2026 to 2033. North America dominated the market with the largest revenue share of 36.9% in 2025. The current market growth can be attributed to the increased digitalization, increasing demand for desktop-as-a-service, the increasing adoption of remote and hybrid work models.

Key Market Trends & Insights

- By component: Solutions segment accounted for the largest revenue share of over 66.2% in 2025.

- By organization size: Large enterprises segment accounted for the largest revenue share of 58.9% in 2025.

- By end-use: IT & telecommunication segment accounted for the largest revenue share of 21.9% in 2025.

Regional Highlights

- Largest regional market: North America (36.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The digital workplace market in the U.S. held the largest share in the North America region in 2025.

Market Size & Forecast

- Market size in 2025: USD 59.4 Billion

- Estimated market size in 2026: USD 72.5 Billion

- Projected market size by 2033: USD 323.5 Billion

- CAGR (2026-2033): 23.8%

The COVID-19 pandemic accelerated the shift toward flexible work environments, prompting companies to invest in digital workplace solutions that support seamless collaboration and communication, regardless of physical location. This trend continues as organizations recognize the long-term benefits of flexibility in their workforce.")

Moreover, the digital workplace market is experiencing a growing demand for employee experience platforms as organizations increasingly prioritize employee engagement and retention. These platforms, which often include unified communication tools, self-service portals, and personalized interfaces, are designed to enhance the overall user experience by simplifying workflows and reducing employee frustration. By improving accessibility to tools and information, these solutions not only boost employee satisfaction but also play a crucial role in talent management strategies, helping companies foster a more productive and motivated workforce. As businesses recognize the link between a positive employee experience and long-term retention, the adoption of such platforms is becoming essential for maintaining a competitive edge.

Rapid technological advancements in cloud computing, artificial intelligence (AI), and machine learning (ML) are transforming digital workplace tools, making them more efficient and capable. Innovations such as AI-powered virtual assistants and automation of routine tasks are boosting productivity and streamlining operations, significantly reducing operational costs. Additionally, cloud-based solutions offer seamless scalability, allowing businesses to easily adapt as their needs evolve. These cutting-edge technologies enhance flexibility and accessibility, making digital workplace solutions increasingly attractive for organizations of all sizes, fostering faster adoption and improved performance across industries.

The increasing focus on cybersecurity in remote work environments is fueling the demand for secure digital workplace solutions. As the number of endpoints and data access points grows, organizations are placing a higher priority on safeguarding sensitive data. This includes implementing robust security measures such as identity and access management, advanced encryption technologies, and secure collaboration tools. These solutions not only protect critical information from cyber threats but also ensure compliance with evolving regulations. As remote and hybrid work models become more prevalent, investing in comprehensive cybersecurity solutions is essential for maintaining operational continuity and trust.

Market Dynamics

The digital workplace market is experiencing rapid growth as organizations increasingly adopt cloud-based collaboration platforms, remote work technologies, employee experience solutions, and unified communication tools to enhance workforce productivity and operational agility. Digital workplace solutions enable employees to securely access applications, data, communication channels, and business processes from any location and device, supporting hybrid and distributed work models. The growing focus on employee engagement, business continuity, digital transformation, and workplace modernization is accelerating investments in digital workplace platforms that integrate collaboration, workflow automation, virtual desktops, knowledge management, and AI-powered productivity tools.

The widespread adoption of hybrid and remote work models is a key driver of the digital workplace market. Organizations across industries are increasingly investing in cloud collaboration platforms, unified communications, virtual desktop infrastructure (VDI), enterprise mobility solutions, and employee experience technologies to support a geographically dispersed workforce. The need to improve productivity, enable seamless collaboration, ensure secure access to corporate resources, and enhance employee engagement is driving enterprises toward comprehensive digital workplace ecosystems. Furthermore, the integration of artificial intelligence (AI), workflow automation, and intelligent assistants into workplace platforms is helping organizations streamline operations, reduce administrative workloads, and improve decision-making, further fueling market growth.

For instance, in April 2026, Microsoft introduced new Microsoft 365 Copilot capabilities, including AI-powered workflow automation, enhanced collaboration tools, advanced data analysis features in Excel, and productivity improvements across Teams, Outlook, and PowerPoint. The announcement reflects the growing demand for AI-enabled digital workplace solutions that enhance employee productivity and support hybrid work environments. Such developments demonstrate how increasing demand for digital collaboration and intelligent workplace solutions continues to accelerate investments in digital workplace technologies, strengthening the market's growth outlook.

Cybersecurity risks and integration challenges remain significant restraints for the digital workplace market. As organizations deploy multiple cloud applications, collaboration tools, remote access solutions, and connected devices, the attack surface expands, increasing exposure to data breaches, ransomware attacks, identity theft, and insider threats. Ensuring secure access management, regulatory compliance, and data protection across distributed work environments requires substantial investment in cybersecurity infrastructure and governance frameworks.

Additionally, many enterprises operate legacy systems that may not seamlessly integrate with modern digital workplace platforms. The complexity of integrating diverse applications, migrating workloads, managing user adoption, and maintaining interoperability across different technology environments can increase implementation costs and deployment timelines. These challenges may slow adoption, particularly among organizations with limited IT resources or highly regulated operational environments.

The increasing adoption of artificial intelligence, workplace analytics, and intelligent automation is creating substantial opportunities for the digital workplace market. Organizations are leveraging AI-powered virtual assistants, intelligent search, automated workflows, predictive analytics, and personalized employee experience platforms to improve productivity, collaboration, and workforce satisfaction. AI-driven solutions can automate repetitive tasks, provide contextual recommendations, enhance knowledge discovery, and optimize workplace operations, enabling employees to focus on higher-value activities.

Furthermore, the growing demand for digital employee experience (DEX) platforms, low-code workflow automation tools, and integrated collaboration ecosystems is encouraging vendors to develop more advanced workplace solutions. As enterprises continue prioritizing workforce modernization, employee well-being, and operational efficiency, investments in AI-enabled digital workplace platforms are expected to create significant long-term growth opportunities for technology providers and service vendors.

Analyst Perspective

The digital workplace market sits at the intersection of several transformative growth drivers, including the widespread adoption of hybrid work models, accelerating digital transformation initiatives, increasing cloud migration, and growing demand for employee productivity and collaboration solutions. As organizations seek to enhance workforce agility, employee engagement, and business continuity, digital workplace platforms have become critical for enabling seamless communication, knowledge sharing, workflow automation, and secure remote access. The market also benefits from the rapid integration of artificial intelligence (AI), employee experience technologies, enterprise mobility solutions, and unified communications platforms. The central competitive advantage, however, will belong to providers that can seamlessly integrate AI-powered productivity tools, collaboration platforms, workflow automation, cybersecurity capabilities, and personalized employee experiences into a unified digital workplace ecosystem that supports evolving workforce needs and organizational objectives.

Component Insights

Based on component, the solutions segment led the market with the largest revenue share of 66.2% in 2025, driven by the demand for unified communication and collaboration platforms. Solutions such as Microsoft Teams, Zoom, and Slack integrate messaging, video conferencing, file sharing, and task management into a single platform, streamlining internal and external communications. As businesses continue adopting hybrid and remote work models, the need for efficient, scalable, and secure communication tools has surged, driving investments in these solutions.

The services segment is expected to grow at a CAGR of 24.0% over the forecast period owing to the increasing demand for managed services. As businesses adopt digital workplace solutions, many lack the in-house expertise to manage the complexities of deployment, integration, and ongoing support. Managed service providers (MSPs) offer end-to-end solutions, including monitoring, maintenance, and upgrades of digital workplace platforms. By outsourcing these tasks to experts, organizations can focus on core business activities while ensuring that their digital workplace infrastructure remains secure and up-to-date.

Organization Size Insights

Based on organization size, the large enterprises segment led the market with the largest revenue share of 58.9% in 2025, owing to the increasing focus on enhancing operational efficiency across globally distributed teams. Large organizations often operate in multiple regions, making it essential to have a unified digital workplace solution that allows seamless communication and collaboration across various departments and time zones. By adopting comprehensive digital workplace platforms, large enterprises can improve coordination, reduce communication barriers, and streamline workflows, which is crucial for maintaining competitiveness in the global market.

The SMEs segment is expected to grow at a significant CAGR over the forecast period due to the increasing need for cost-effective and scalable solutions. SMEs often operate with limited IT budgets, making cloud-based digital workplace tools highly appealing due to their affordability and flexibility. These solutions enable businesses to adopt advanced technology without the high upfront costs associated with traditional IT infrastructure, allowing them to scale their operations as they grow.

End-use Insights

Based on end-use, the IT & telecommunication segment led the market with the largest revenue share of 21.9% in 2025, due to the increasing demand for secure and scalable communication infrastructure. With the growing reliance on digital communication channels, IT and telecommunication companies are focusing on secure digital workplace solutions that provide robust data protection and privacy. As these industries handle large volumes of sensitive customer data, the need for secure collaboration tools, encrypted communication, and identity management systems is critical. This heightened focus on cybersecurity is pushing the adoption of advanced digital workplace platforms.

The manufacturing segment is expected to grow at a significant CAGR over the forecast period. The integration of Internet of Things (IoT) technologies within the manufacturing sector also plays a critical role in driving digital workplace adoption. IoT devices can collect vast amounts of data from machinery and equipment, providing insights that can enhance performance and maintenance schedules. By integrating IoT data with digital workplace solutions, manufacturers can create a connected ecosystem that improves collaboration between departments, enhances predictive maintenance capabilities, and ultimately leads to reduced downtime and increased operational efficiency.

Regional Insights

North America dominated the digital workplace market with the largest revenue share of 36.9% in 2025. The trend toward sustainability and corporate social responsibility is influencing the regional market growth. Organizations are increasingly looking for digital solutions that support eco-friendly practices, such as reducing paper usage through digital document management systems and minimizing carbon footprints by enabling remote work. As companies seek to align their operations with sustainability goals, the demand for digital workplace tools that facilitate these initiatives is expected to rise, further driving market growth in the region.

U.S. Digital Workplace Market Trends

The digital workplace market in the U.S. held the largest share in the North America region in 2025. The rapid advancement of technology, particularly in artificial intelligence (AI), machine learning (ML), and automation, is propelling growth in the U.S. market. These technologies enable organizations to streamline workflows, reduce manual tasks, and improve decision-making processes. For instance, AI-powered tools can automate routine administrative tasks, freeing up employees to focus on higher-value activities. As businesses increasingly leverage these innovations to enhance operational efficiency and productivity, the demand for digital workplace solutions that incorporate cutting-edge technologies is expected to rise.

Europe Digital Workplace Market Trends

The digital workplace market in Europe is growing with a significant CAGR from 2025 to 2030, driven by the growing emphasis on digital transformation across industries. European companies are prioritizing the adoption of innovative technologies to improve operational efficiency and competitiveness. This shift is fueling investments in digital workplace solutions that enhance collaboration, automate processes, and enable data-driven decision-making. As organizations strive to remain competitive in the global market, they are increasingly turning to digital tools that facilitate innovation and agility, further propelling the growth of the Digital Workplace Market in Europe.

The UK digital workplace market is expected to grow rapidly in the coming years. The growing focus on data security and compliance is influencing the UK digital workplace market. With the increasing amount of sensitive data being shared and accessed remotely, organizations are prioritizing cybersecurity measures to protect their information assets.

The digital workplace market in Germany held a substantial market share in 2024. The rise of the gig economy is influencing the digital workplace landscape in Germany. More organizations are engaging freelancers and contractors to meet fluctuating demands, necessitating digital solutions that can accommodate diverse workforces. Companies are adopting platforms that allow for effective onboarding, communication, and project management for both permanent employees and gig workers.

Asia Pacific Digital Workplace Market Trends

Asia Pacific is growing significantly at a CAGR of 25.8% from 2026 to 2033, driven by the rapid urbanization and increasing penetration of internet connectivity. As more people move to urban areas, the demand for digital solutions that support remote work and collaboration is rising. Governments and businesses are investing heavily in improving internet infrastructure, leading to higher accessibility and adoption of digital workplace tools. This trend is particularly pronounced in developing countries, where enhanced connectivity is facilitating the growth of a digital economy and empowering organizations to leverage remote working capabilities.

The digital workplace market in Japan is expected to grow rapidly in the coming years, driven by the aging workforce, which is prompting manufacturers and service industries to seek solutions that can help mitigate the impact of labor shortages. Digital workplace tools that facilitate knowledge transfer, enhance remote collaboration, and support automation are becoming essential. By implementing these solutions, organizations can maintain productivity while addressing the challenges of a shrinking workforce.

The China digital workplace market held a substantial market share in 2024, driven by the government’s strong push for digital transformation across various industries. The Chinese government has been actively promoting initiatives such as Made in China 2025 and Internet Plus, which aim to modernize manufacturing and integrate digital technologies into traditional sectors. These initiatives encourage companies to adopt digital workplace solutions that enhance productivity and innovation, resulting in a more efficient economy. This governmental support is creating a favorable environment for the growth of digital workplace technologies.

Key Digital Workplace Company Insights

Some of the key companies in the digital workplace market include Accenture, IBM, Cognizant, Wipro, and HCL Technologies Limited. Organizations are focusing on increasing customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies

-

In October 2024, Atos announced the launch of its advanced Experience Operations Center (XOC) in collaboration with Nexthink. This innovative offering aims to improve digital workplace operations by enhancing end user experience through real-time, AI-driven efficiencies that boost workplace productivity. Building on an eight-year partnership, which positioned Atos as one of Nexthink’s first managed services partners, this new initiative focuses on creating employee-centric workplaces that foster innovative and sustainable business value for organizations.

-

In February 2024, HCL Technologies Limited launched FlexSpace 5G, an advanced digital workplace experience-as-a-service aimed at enhancing efficiency and security for global businesses. Utilizing Verizon’s secure network and HCLTech’s premium hardware partnerships, this solution facilitates a smooth transition to a digital workplace for all employees, whether at their desks, remote, or on the go. FlexSpace 5G offers unique benefits, including end-to-end device lifecycle management, enhanced mobility in hybrid work settings beyond standard Wi-Fi, and faster, more reliable connectivity for sectors such as financial services, healthcare, and media. It also addresses data security concerns for remote workers, creating a safer work environment.

Key Digital Workplace Companies:

The following key companies have been profiled for this study on the digital workplace market.

-

Accenture

-

Atos

-

Cognizant

-

Fujitsu

-

HCL Technologies Limited

-

Hewlett Packard Enterprise Development LP

-

IBM

-

Infosys Limited

-

Mphasis

-

NTT DATA Group Corporation

-

Tata Consultancy Services Limited

-

Wipro

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Accenture, IBM, Tata Consultancy Services Limited, Infosys Limited, Wipro, Cognizant, HCL Technologies Limited)

- Expand digital workplace portfolios through AI-powered productivity tools, employee experience platforms, cloud collaboration solutions, and managed workplace services.

- Invest in strategic partnerships with major technology providers such as Microsoft, Google, ServiceNow, and VMware to enhance end-to-end workplace transformation capabilities.

- Extensive global delivery networks, strong enterprise customer relationships, and comprehensive consulting, implementation, and managed service capabilities.

- Broad service portfolios enable end-to-end digital workplace transformation across diverse industries and geographies.

- High operational complexity associated with managing large-scale global engagements.

- Longer implementation cycles and higher service costs can reduce flexibility when addressing the needs of smaller organizations and rapidly changing workplace requirements.

Emerging Players (Atos, Fujitsu, Hewlett Packard Enterprise Development LP)

- Focus on industry-specific workplace solutions, hybrid work enablement, cloud-based collaboration platforms, and employee experience enhancement services.

- Strengthen regional presence through strategic partnerships and targeted digital transformation initiatives.

- Greater agility in addressing evolving workplace trends and customer requirements.

- Strong expertise in selected industries and regional markets enables more customized and flexible digital workplace offerings.

- Smaller global market presence and customer reach compared to leading providers.

- Limited scale and investment capacity may constrain expansion of advanced AI-powered workplace platforms and large multinational deployments.

Digital Workplace Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 59.4 billion

Estimated Market Size in 2026

USD 72.5 billion

Projected Market Size by 2033

USD 323.5 billion

Growth rate

CAGR of 23.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share, competitive landscape, growth factors, and trends

Segments covered

Component, organization size, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; U.K.; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Atos; Cognizant; IBM; Wipro; Infosys Limited; Accenture; HCL Technologies Limited; Fujitsu; NTT DATA Group Corporation; Hewlett Packard Enterprise Development LP

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Digital Workplace Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global digital workplace market report based on component, organization, end-use, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Solutions

-

Services

-

-

Organization Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

Small and Medium-sized Enterprises (SMEs)

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

IT & Telecommunication

-

Retail & Consumer Goods

-

Healthcare & Pharmaceuticals

-

Manufacturing

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Component

Revenue capture definition

Solutions

Revenue is primarily generated through subscription-based licensing fees for digital workplace platforms, including collaboration tools, unified communications, virtual desktop infrastructure (VDI), employee experience platforms, enterprise mobility solutions, workflow automation, and workplace productivity software. Pricing is typically based on the number of users, features deployed, or usage volume.

Services

Revenue is generated through consulting, implementation, integration, customization, training, technical support, managed services, and ongoing maintenance associated with digital workplace deployments. Organizations engage service providers to optimize adoption, enhance user experience, and manage workplace transformation initiatives.

Segment - Organization Size

Revenue capture definition

Large Enterprises

Revenue is generated from enterprise-wide deployments of digital workplace solutions across multiple departments, business units, and geographic locations. Large organizations typically invest in advanced collaboration platforms, AI-powered productivity tools, security solutions, and managed services under multi-year subscription or service agreements.

SMEs

Revenue is derived from cloud-based and scalable digital workplace subscriptions tailored to small and medium-sized businesses. SMEs typically adopt cost-effective collaboration, communication, and productivity solutions with flexible pricing models that minimize upfront investment and support business growth.

Segment - End Use

Revenue capture definition

BFSI

Revenue is generated from digital workplace solutions that support secure collaboration, remote workforce management, document sharing, workflow automation, and regulatory compliance across banking, financial services, and insurance organizations.

IT & Telecommunication

Revenue is derived from the deployment of collaboration platforms, virtual workspaces, project management tools, and unified communications solutions that enable distributed teams, software development collaboration, and digital operations management.

Retail & Consumer Goods

Revenue is generated through workplace platforms that facilitate communication between corporate offices, retail outlets, suppliers, and field employees while supporting workforce scheduling, training, and operational coordination.

Healthcare & Pharmaceuticals

Revenue is captured from digital workplace solutions that enable secure communication, telehealth collaboration, research coordination, document management, workforce productivity, and compliance with healthcare data regulations.

Manufacturing

Revenue is generated from workplace platforms that connect corporate, production, and field teams through digital collaboration, workflow automation, knowledge sharing, and operational communication tools across manufacturing environments.

Others

Revenue is derived from adoption across government, education, energy, transportation, professional services, and other sectors utilizing digital workplace technologies to improve employee productivity, collaboration, and business process efficiency.

Estimation Model

Digital Workplace Addressable Layer

Technology Access Layer

Adoption & Utilization Layer

Monetisation Layer

Who can benefit from agricultural drones?

Who can access and deploy digital workplace technologies?

Who actively uses digital workplace platforms?

How much revenue is generated?

Identify the total workforce across enterprises, SMEs, government agencies, and other organizations that can benefit from collaboration, communication, and productivity solutions.

Apply cloud readiness, internet connectivity, device availability, cybersecurity capabilities, and digital infrastructure maturity to determine the reachable market.

Apply digital workplace adoption rates, hybrid work trends, and enterprise digital transformation initiatives to convert reachable organizations into active users.

Assess revenue potential through spending on workplace software subscriptions, collaboration platforms, employee experience solutions, implementation services, managed services, and ongoing support contracts.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Hybrid Work & Collaboration Platform Adoption Trends

Conducted a focused analysis of enterprise adoption trends for hybrid work solutions, including collaboration platforms, unified communications, virtual meeting tools, digital workspaces, and employee engagement technologies across key industries and regions.

Helps stakeholders identify high-growth workplace technologies, evaluate workforce transformation trends, and assess opportunities arising from evolving hybrid and remote work models.

Managed Digital Workplace Services Opportunity Analysis

Evaluated demand for workplace consulting, managed collaboration services, workplace support services, and digital transformation outsourcing across enterprise customers.

Provides visibility into recurring revenue opportunities, service-led growth strategies, and customer outsourcing preferences.

Generative AI Use Case Assessment in Digital Workplaces

Evaluated publicly announced enterprise deployments of AI assistants, content generation tools, meeting intelligence, knowledge management, and workflow automation applications.

Helps identify commercially viable AI use cases and emerging innovation opportunities.

Frequently Asked Questions About This Report

The global digital workplace market was estimated at USD 59.4 billion in 2025 and is expected to reach USD 72.5 billion in 2026.

The global digital workplace market is expected to witness a compound annual growth rate of 23.8% from 2026 to 2033 to reach USD 323.5 billion by 2033.

The current growth of the digital workplace market can be attributed to the increased digitalization, increasing demand for desktop-as-a-service, the increasing adoption of remote and hybrid work models.

Asia Pacific is the fastest-growing region over the forecast period.

The solutions segment led with a 66.2% revenue share in 2025, while the services segment is the fastest-growing segment.

The large enterprises segment led with a 58.9% revenue share in 2025, while the SMEs segment is the fastest-growing segment.

The IT & telecommunications segment led with a 21.9% revenue share in 2025, while the manufacturing segment is the fastest-growing.

Key players operating in the digital workplace market include Atos; Cognizant; IBM; Wipro; Infosys Limited; Accenture; HCL Technologies Limited; Fujitsu; NTT DATA Group Corporation; Hewlett Packard Enterprise Development LP

The digital workplace market in North America accounted for 36.9% of the market share in 2025. The trend toward sustainability and corporate social responsibility is driving growth in the digital workplace market in North America. Organizations are increasingly seeking digital solutions that support eco-friendly practices, such as reducing paper use through digital document management systems and minimizing carbon footprints by enabling remote work.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.