- Home

- »

- Next Generation Technologies

- »

-

Distributed Fiber Optic Sensor Market Size Report 2026-2033GVR Report cover

![Distributed Fiber Optic Sensor Market (2026 - 2033)Report]()

Distributed Fiber Optic Sensor Market (2026 - 2033)

Size, Share & Trend Analysis Report By Function (Acoustic/Vibration Sensing, Temperature Sensing), By Technology (Rayleigh Effect, Brillouin Scattering, Raman Effect), By Application, By Vertical, By Region, And Segment Forecasts

Market Size, 2025

$1.6BMarket Estimate, 2026

$1.8BMarket Forecast, 2033

$3.9BCAGR, 2026–2033

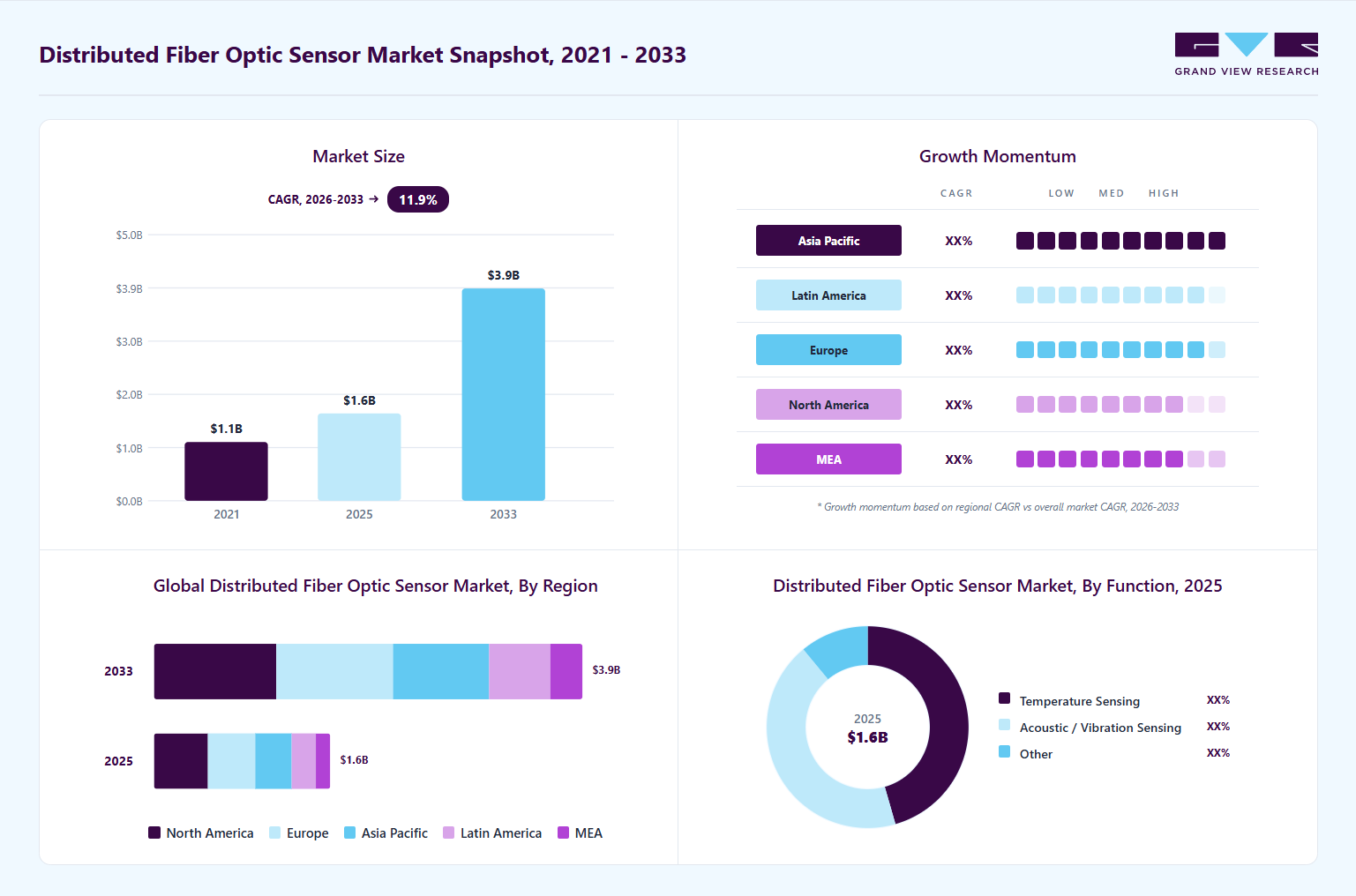

11.9%Distributed Fiber Optic Sensor Market Summary

The global distributed fiber optic sensor market size was valued at USD 1.6 billion in 2025 and is projected to grow from USD 1.8 billion in 2026 to USD 3.9 billion by 2033, at a CAGR of 11.9% from 2026 to 2033. The North America held the largest share of over 30.0% of the global market in 2025. The growing adoption of real-time monitoring across critical infrastructure, rising integration of AI and advanced analytics in DFOS platforms, increasing deployment in harsh and remote terrains, expanding use cases in smart cities and environmental monitoring, and accelerating demand for customized installation and maintenance services.

Key Market Trends & Insights

- By function: Temperature sensing segment held the largest market share of over 45.0% in 2025.

- By technology: Raman effect segment accounted for the largest revenue share of 34.0% in 2025.

- By application: Rail infrastructure monitoring segment accounted for the largest revenue share in 2025.

- By vertical: Oil and gas segment accounted for the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (over 30% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

Market Size & Forecast

- Market size in 2025: USD 1.6 Billion

- Estimated market size in 2026: USD 1.8 Billion

- Projected market size by 2033: USD 3.9 Billion

- CAGR (2026-2033): 11.9%

The distributed fiber optic sensor market represents a rapidly evolving segment of sensing technology, driven by rising demand for advanced, real-time monitoring solutions across multiple industries. These systems leverage optical fibers to measure temperature, strain, and acoustic variations over long distances, enabling continuous data collection with high precision. Key sectors including oil and gas, power and utilities, and civil engineering increasingly depend on these sensors to strengthen operational safety, improve asset performance, and reduce downtime. For instance, in September 2024, SLB entered a joint venture with Patterson-UTI and ADNOC Drilling Company PJSC to establish Turnwell Industries LLC OPC, aimed at advancing smart drilling design, AI-driven production capabilities, and completions engineering to accelerate the UAE’s unconventional oil and gas development. As infrastructure networks grow more complex and geographically distributed, the demand for reliable, high-accuracy fiber optic sensing solutions continues to intensify.")

Distributed fiber optic sensors based perimeter security systems are emerging as a preferred solution for airports, borders, utilities, and critical facilities that require continuous threat detection. Technology’s ability to differentiate between footsteps, vehicles, digging, cutting, and climbing activities is driving rapid adoption. Organizations are shifting from legacy point sensors to fiber-based systems to improve accuracy and reduce false alarms. Rising global security concerns and infrastructure vulnerability are further intensifying interest in acoustic-based fiber detection. This accelerating demand positions DFOS as a cornerstone technology for next-generation perimeter security networks.

Telecom operators and energy companies are rapidly adopting DFOS to monitor thousands of kilometers of submarine fiber cables for temperature shifts, vibration anomalies, and external threats. Distributed sensing enables early detection of anchor drags, seismic activity, and cable stress, reducing the risk of lengthy outages and costly repairs. Increasing global dependence on data transport and offshore energy infrastructure is accelerating investment in long-range DFOS deployments. Operators view fiber-based monitoring as a strategic capability for protecting mission-critical communication routes. This growing adoption trend is driving significant innovation in long-distance optical interrogation technologies.

Market Dynamics

Increasing investments in smart grid modernization projects are driving the adoption of distributed fiber optic sensing technologies throughout global energy infrastructure. Utility providers are deploying advanced sensing systems to enhance grid reliability, improve fault detection, and enable real-time monitoring of transmission and distribution networks. Distributed fiber-optic sensors facilitate continuous monitoring of temperature, strain, and acoustic conditions, which allows operators to optimize grid performance and minimize operational disruptions. Governments and energy companies are accelerating investments in intelligent power infrastructure to address rising electricity demand and the integration of renewable energy sources. This shift toward a digitally connected and resilient grid is generating substantial growth opportunities for distributed fiber-optic sensor manufacturers and solution providers.

The increasing emphasis on energy efficiency, predictive maintenance, and operational safety is strengthening market demand for fiber-sensing technologies in smart grid applications. Distributed fiber-optic sensors enable utilities to detect equipment failures, overheating, and cable faults at an early stage, thereby reducing downtime and maintenance costs. The expansion of renewable energy projects, such as solar and wind farms, is also driving the deployment of advanced monitoring solutions across power networks. Furthermore, the adoption of automation and artificial intelligence-based grid management systems is accelerating the integration of real-time sensing technologies within modern utility infrastructure. As global investments in next-generation power grids continue to grow, the distributed fiber optic sensor market is projected to experience sustained long-term growth.

The increasing vulnerability to physical fiber damage and network disruptions is emerging as a significant restraint for the distributed fiber optic sensor market. Fiber optic cables deployed across pipelines, transportation corridors, offshore facilities, and industrial environments are highly exposed to external risks such as construction activities, harsh weather conditions, vibrations, and accidental mechanical impacts. Damage to fiber networks can disrupt real-time monitoring capabilities, resulting in data transmission failures and reduced operational reliability. In critical infrastructure applications, even minor network interruptions can negatively impact safety monitoring, predictive maintenance, and asset management operations. These challenges are increasing concerns among end users regarding the long-term durability and operational stability of distributed fiber optic sensing systems.

Network disruptions and fiber breakages also contribute to higher maintenance costs and operational complexities for system operators. Repairing damaged fiber infrastructure often requires specialized equipment, skilled technicians, and extended downtime, particularly in remote or underwater installations. The risk of signal loss and reduced sensing accuracy during network disruptions can further limit system performance in mission-critical applications. In addition, organizations operating large-scale sensing networks may face difficulties in ensuring uninterrupted connectivity and consistent monitoring efficiency across extensive infrastructure assets. As a result, the growing exposure to physical damage and network reliability challenges may restrain the large-scale adoption of distributed fiber optic sensor solutions across several industries.

The growing adoption of smart city infrastructure monitoring solutions is creating substantial growth opportunities for the distributed fiber optic sensor market. Governments and municipal authorities across the globe are increasingly investing in intelligent infrastructure systems to improve urban safety, operational efficiency, and public service management. Distributed fiber optic sensors are gaining strong traction in smart city projects due to their ability to provide real-time monitoring of bridges, tunnels, highways, rail networks, and utility infrastructure. These sensing technologies enable continuous detection of structural stress, temperature fluctuations, vibrations, and potential infrastructure failures, supporting proactive maintenance strategies. The rising focus on building resilient, connected, and data-driven urban environments is expected to accelerate the deployment of distributed fiber optic sensing systems in smart city initiatives.

The expansion of smart transportation systems and intelligent utility networks is further strengthening market opportunities for fiber optic sensing solution providers. Cities are increasingly integrating advanced monitoring technologies with IoT platforms, AI-based analytics, and centralized control systems to optimize infrastructure performance and reduce operational risks. Distributed fiber optic sensors also support enhanced public safety by enabling early detection of infrastructure damage, traffic disturbances, and security threats in densely populated urban areas. In addition, increasing investments in sustainable urban development and digital infrastructure modernization are encouraging the adoption of advanced sensing technologies across both developed and emerging economies. As smart city development continues to expand globally, the distributed fiber optic sensor market is expected to witness significant long-term growth opportunities.

Market Concentration & Characteristics

The distributed fiber optic sensor market has moderate concentration, with established energy technology firms, industrial automation providers, and specialized vendors competing in infrastructure monitoring, oil and gas, transportation, and utilities. Leading companies enhance their positions through advanced distributed acoustic sensing, distributed temperature sensing, and real-time monitoring, supported by strong partnerships and global distribution. Emerging and niche players focus on cost-effective, customized solutions for smart infrastructure and industrial monitoring. Growing adoption of smart grids, smart cities, predictive maintenance, and critical infrastructure monitoring is increasing competition and driving innovation. Companies are increasingly pursuing strategic collaborations, product development, and investments in AI-enabled analytics, cloud-based monitoring, and intelligent infrastructure to expand their market presence and operational capabilities.

Distributed fiber optic sensors compete with conventional electronic sensors, wireless monitoring, and legacy inspection systems that may offer lower initial costs. Large industrial operators with existing infrastructure may prefer traditional technologies and periodic inspections to advanced fiber-optic systems. High installation costs, deployment complexity, and maintenance challenges can also limit adoption among cost-sensitive and small-scale operators. However, distributed fiber-optic sensing offers significant advantages, including continuous, real-time monitoring, long-distance coverage, high accuracy, and improved safety for critical infrastructure. The increasing focus on predictive maintenance, infrastructure resilience, energy efficiency, and automation is expected to sustain long-term demand for these advanced solutions worldwide.

Function Insights

The temperature sensing segment led the market and accounted for over 45% of the global revenue in 2025, owing to rising industry demand for continuous thermal monitoring across critical assets such as pipelines, power cables, and industrial systems. The ability of distributed fiber optic technology to deliver real-time, high-resolution temperature profiles is driving rapid adoption, as operators prioritize early detection of overheating, leaks, and equipment stress. Strong performance in harsh and electrically challenging environments positions temperature sensing as a foundational tool for safety and operational reliability. Ongoing advancements in interrogation speed and measurement accuracy are accelerating deployment across energy, utilities, and large infrastructure projects. Growing investment in predictive maintenance strategies further strengthens the segment’s momentum and solidifies its leadership in the global DFOS market.

The acoustic and vibration sensing segment is predicted to foresee significant growth in the forecast period, driven by increasing industry demand for real-time detection of disturbances, structural stress, and potential intrusions across critical assets. Distributed acoustic sensing delivers continuous, high-resolution monitoring along the entire fiber length, enabling rapid identification of events such as leaks, third-party interference, equipment faults, or ground movement. Its ability to operate reliably in harsh environments is accelerating adoption across oil and gas, rail networks, perimeter security, and geotechnical applications. Advances in signal processing and interrogation methods are enhancing accuracy and expanding the range of deployable use cases. Heightened focus on safety, operational continuity, and proactive risk mitigation continues to propel the momentum of acoustic and vibration-based DFOS solutions worldwide.

Technology Insights

The Raman effect segment accounted for the largest market revenue share in 2025, driven by the technique’s ability to deliver distributed temperature measurements through analysis of inelastic light scattering along the fiber. Its high sensitivity to thermal variations supports applications in fire detection, environmental monitoring, and industrial process control. Raman sensors perform well in electrically noisy or hazardous environments, offering non-intrusive and reliable measurement capabilities. Recent advances in interrogation technology have improved measurement speed and spatial resolution, strengthening their operational value. These enhancements are broadening application areas and improving safety across critical infrastructure.

The Rayleigh effect segment is expected to record significant growth during the forecast period, supported by its use of naturally occurring backscattering within the fiber to measure strain and temperature with very high spatial resolution. This technique is widely applied in structural health monitoring, pipeline surveillance, and geotechnical assessment due to its ability to detect localized changes with precision. Rayleigh-based sensors generate continuous data along the entire fiber, enabling detailed mapping of physical parameters for early issue detection. Advances in interrogation methods have improved signal clarity and reduced noise levels, strengthening overall accuracy. The passive nature of the method removes the need for external light sources, simplifying installation and long-term maintenance.

Application Insights

The rail infrastructure monitoring segment accounted for the largest market revenue share in 2025, supported by the growing need for continuous assessment of track conditions, structural integrity, and environmental factors that influence rail operations. Distributed fiber optic sensors detect strain, vibration, and temperature changes, enabling early identification of track deformation, wear, or external disturbances that could compromise safety. For instance, in June 2025, Sensonic GmbH partnered with the Chicago Transit Authority to deploy a DAS pilot program designed to automatically detect intrusions and fallen objects along the rail right-of-way. The initiative uses fiber optic cables for continuous real-time monitoring, strengthening hazard detection and improving overall transit system reliability. These capabilities enhance maintenance planning, reduce the likelihood of accidents, and support more efficient rail network operations.

The urban monitoring segment is expected to record strong growth as cities increasingly adopt distributed fiber optic sensing to assess infrastructure health, environmental conditions, and public safety. Embedded sensors in roads, bridges, and buildings deliver continuous data on stress, vibration, and temperature, enabling proactive maintenance and early hazard identification. This non-intrusive technology can be incorporated into existing urban assets with minimal disruption, supporting long-term infrastructure resilience and lowering emergency repair costs. Real-time insights also improve resource allocation and strengthen emergency response capabilities for municipal authorities. For instance, in February 2025, the City Changer project in Croatia deployed a DAS system along a 17-kilometer fiber route between Gruda and Vitaljina, demonstrating how fiber-based sensing can detect seismic activity, traffic patterns, landslides, and other critical urban events.

Vertical Insights

The oil and gas segment accounted for the largest market revenue share in 2025, driven by the need to monitor pipelines, wells, and processing facilities for temperature, strain, and acoustic signals that indicate leaks or structural concerns. Continuous distributed sensing improves safety by enabling early detection of operational anomalies and environmental risks. Technology also supports compliance with strict industry regulations and reduces unplanned downtime through predictive maintenance. Fiber optic sensors are highly suitable for complex oilfield environments due to their immunity to electromagnetic interference and strong performance in harsh conditions. For instance, in February 2025, ABB deployed its advanced temperature measurement technology for Equinor at the Johan Sverdrup oil field in the North Sea, enabling precise, real-time temperature monitoring across pipelines and production equipment to identify issues such as overheating or blockages.

The industrial segment is projected to grow significantly over the forecast period, supported by rising adoption of DFOS for equipment health monitoring, process control, and environmental measurement to improve safety and productivity. These sensors deliver continuous data on strain, temperature, and vibration, which strengthens predictive maintenance strategies and lowers downtime. Their resistance to harsh industrial settings and electromagnetic interference ensures dependable performance across manufacturing, chemical processing, and related sectors. Integration with industrial IoT platforms improves real-time analytics and operational decision-making. Enhanced monitoring capabilities improve asset utilization and reduce maintenance costs. The scalability and flexibility of sensor networks allow tailored configurations for diverse industrial operations, and advancements in sensing technologies and data integration continue to expand future use cases.

Regional Insights

North America DFOS market accounted for over 30% of the global share in 2025, supported by strong investments across oil and gas, telecommunications, and energy infrastructure. The region’s advanced technological landscape and continuous innovation are elevating the precision and functionality of fiber optic sensing solutions. Expanding applications in civil engineering, defense, and security further reinforce market momentum. Collectively, these factors position North America as a leading hub for real-time monitoring and safety-driven DFOS deployments.

U.S. Distributed Fiber Optic Sensor Market Trends

The U.S. DFOS market is propelled by growing activity in the oil and gas industry, where real-time pipeline monitoring and leak detection have become operational priorities. Advanced sensing technologies, such as OFDR and OTDR, are enhancing accuracy and broadening the range of DFOS applications. Government support, including funding initiatives from the Department of Energy and the Federal Communications Commission, continues to accelerate adoption. As a result, the U.S. maintains strong demand for next-generation fiber optic networks and monitoring solutions.

Europe Distributed Fiber Optic Sensor Market Trends

The Europe DFOS market is being driven by the region’s accelerating shift toward renewable energy and the need for continuous monitoring of wind farms, solar plants, and associated transmission assets. Growing regulatory emphasis on operational safety and environmental protection is encouraging industries to adopt high-precision sensing technologies for early fault detection and structural health monitoring. Advancements in distributed acoustic sensing and temperature monitoring are enabling utilities and transportation operators to improve efficiency, reduce downtime, and optimize asset life cycles. Collectively, these factors are reinforcing DFOS as a critical enabler of Europe’s energy transition and infrastructure resilience strategy.

Asia Pacific Distributed Fiber Optic Sensor Market Trends

The Asia Pacific DFOS market is expected to register the fastest CAGR over the forecast period due to rapid industrial expansion and large-scale infrastructure investments across China, India, and Southeast Asia. Increasing adoption of DFOS for structural health monitoring, seismic detection, and perimeter security is strengthening its use across transportation, utilities, and civil engineering projects. The region’s growing focus on smart infrastructure, supported by government initiatives and significant telecom upgrades including widespread 5G deployment, is further accelerating technology uptake. These developments collectively position Asia Pacific as a major engine of global DFOS market growth.

Key Distributed Fiber Optic Sensor Company Insights

Some key companies in the DFOS industry Schlumberger Limited, Halliburton, Omnisens SA, OFS Fitel, LLC

-

Schlumberger Limited is a provider of advanced technologies and services for the oil and gas industry, covering subsurface characterization, drilling, production, and processing. The company delivers a comprehensive portfolio spanning exploration initiatives to integrated pore-to-pipeline solutions designed to maximize hydrocarbon recovery and enhance reservoir performance. In addition, Schlumberger is expanding its offerings to support emerging sectors such as carbon capture and storage (CCS) and groundwater extraction, aligning its capabilities with the growing demand for sustainable resource management.

-

OFS Fitel, LLC is a prominent manufacturer of optical fiber cables, connectivity systems, and integrated fiber-optic solutions supporting telecommunication and industrial applications. Its core competencies include the design and production of high-strength fiber cables engineered for diverse indoor, outdoor, and harsh-environment use cases. OFS Fitel serves a broad range of industries-including government, aerospace, medical, industrial networking, telecommunications, and defense-through a robust product portfolio comprising optical fibers, advanced connectivity solutions, fiber laser components, fusion splicing equipment, and professional engineering services.

Key Distributed Fiber Optic Sensor Companies:

The following key companies have been profiled for this study on the distributed fiber optic sensor market.

- Schlumberger Limited

- Halliburton

- Yokogawa Electric Corporation

- OFS Fitel, LLC

- Omnisens SA

- Brugg Kable AG

- AP Sensing GmbH

- Baker Hughes Company

- Silixa Ltd

- Luna Innovations Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Schlumberger Limited; Yokogawa Electric Corporation; OFS Fitel, LLC.

- Focus on expanding Major market participants are focusing on scalable sensing deployments across smart city and transportation projects.

- Increasing investments in R&D are supporting the development of advanced distributed acoustic and temperature sensing technologies.

- Companies with integrated hardware and analytics capabilities are gaining stronger competitive positioning.

- Growing demand for end-to-end infrastructure monitoring solutions is strengthening the market presence of established players.

- • Dependence on legacy infrastructure systems is limiting operational flexibility for several established companies.

- Increasing maintenance complexities in large-scale sensing deployments are creating operational constraints.

Emerging Players: Omnisens SA; AP Sensing GmbH, Silixa Ltd; Luna Innovations Inc.

- Emerging companies are focusing on cost-effective sensing solutions for niche industrial monitoring applications.

- Rapid product innovation is enabling smaller players to address evolving industrial monitoring demands.

- Faster speed-to-market is enabling quick adoption of new sensing and monitoring technologies.

- Strong focus on niche applications is enabling smaller companies to establish specialized market positions.

- Limited financial resources are restricting large-scale expansion and global deployment capabilities.

- Dependence on external partnerships for scaling operations may impact long-term profitability and growth.

Recent Developments

-

In May 2026, DarkPulse Inc. announced an exclusive license agreement with the U.S. Naval Air Warfare Center Weapons Division (NAWCWD) to commercialize advanced LADAR laser targeting and sensing technologies in the United States. The licensed technologies enhance high-resolution sensing, object detection, velocity measurement, and 3D spatial imaging capabilities, supporting advanced monitoring and surveillance applications. This development reflects the growing integration of distributed fiber optic sensing technologies with defense-grade laser and sensing systems for critical infrastructure and security applications. The agreement also strengthens the commercialization of next-generation sensing solutions across aerospace, defense, and industrial monitoring sectors.

-

In February 2026, AP Sensing collaborated with Ampacimon to develop advanced overhead transmission line monitoring and grid optimization solutions using Distributed Fiber Optic Sensing (DFOS) technologies. The partnership integrates Distributed Acoustic Sensing (DAS), Distributed Temperature Sensing (DTS), and Dynamic Line Rating (DLR) capabilities to provide real-time monitoring of power transmission infrastructure through optical ground wire (OPGW) networks. The solution enables utilities to enhance grid reliability, optimize transmission capacity, detect infrastructure disturbances, and improve operational efficiency without deploying additional physical sensors on conductors. This collaboration reflects the growing adoption of distributed fiber optic sensing technologies for intelligent grid modernization, predictive maintenance, and critical energy infrastructure management.

-

In November 2025, Knowit signed a three-year agreement with Equinor to further develop and operate Equinor’s Distributed Fiber Optic Sensing (DFOS) platform, expanding their strategic collaboration. DFOS technology provides real-time monitoring and analysis of pipelines, cables, and wells, delivering actionable insights to improve safety, resource utilization, and emissions reduction. Knowit will deliver software development, system integration, and technology advisory services to scale the DFOS platform and extend its use across Equinor’s portfolio. This partnership builds on previous projects, including Fibra, and strengthens Knowit’s position as a trusted technology partner in advanced sensor solutions for the energy sector.

-

In January 2025, OFS introduced DataSens Enhanced Optical Fiber, a distributed fiber optic sensing (DFOS) solution that delivers greater backscatter signal than conventional fibers. It extends sensing range, improves accuracy, and is fully compatible with standard fiber types. This technology enables precise monitoring of infrastructure, vibrations, and pipelines without requiring costly signal amplification.

-

In January 2025, Baker Hughes introduced SureCONNECT FE, a downhole fiber-optic wet-mate system for real-time reservoir monitoring in HPHT conditions. The system connects lower and upper well completions, providing continuous fiber-optic and electronic data across the wellbore without intervention. It reduces rig time, maintenance costs, and operational risks while delivering insights to enhance production and well performance.

Distributed Fiber Optic Sensor Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.6 billion

Estimated market size in 2026

USD 1.8 billion

Projected market size by 2033

USD 3.9 billion

Growth rate

CAGR of 11.9% from 2026 to 2030

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Function, technology, application, vertical, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Schlumberger Limited; Halliburton; Yokogawa Electric Corporation; OFS Fitel, LLC; Omnisens SA; Brugg Kable AG; AP Sensing GmbH; Baker Hughes Company; Silixa Ltd; Luna Innovations Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Distributed Fiber Optic Sensor Report Segmentation

This report forecasts Revenue growth on global, regional, and country levels and provides an analysis of the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global distributed fiber optic sensor market report based on function, technology, application, vertical, and region.

-

Function Outlook (Revenue, USD Million, 2021 - 2033)

-

Acoustic/Vibration Sensing

-

Temperature Sensing

-

Other

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Rayleigh Effect

-

Brillouin Scattering

-

Raman Effect

-

Interferometric

-

Bragg Grating

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Geophysical Event Monitoring

-

Network Disturbance Monitoring

-

Rail Infrastructure Monitoring

-

Urban Monitoring

-

Subsea Infrastructure Monitoring

-

Others

-

-

Vertical Outlook (Revenue, USD Million, 2021 - 2033)

-

Oil and Gas

-

Power and Utility

-

Safety and Security

-

Industrial

-

Civil Engineering

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Objective

Custom Research Modules Delivered

Strategic Value / Business Impact

Market Entry & Expansion Assessment

Regional demand sizing and forecasting across oil & gas, utilities, transportation, and smart infrastructure sectors

Customer segmentation and industrial buying behavior analysis

Competitive landscape benchmarking for distributed fiber optic sensing technologies

Regulatory standards and distribution channel assessment

Identified high-growth infrastructure monitoring opportunities

Supported go-to-market and regional expansion strategies

Highlighted investment priorities and operational risks

Enabled data-driven market penetration planning

Product Positioning & Competitive Intelligence

Distributed acoustic sensing (DAS) and distributed temperature sensing (DTS) product benchmarking

Pricing and value proposition analysis

Competitor strategy and innovation evaluation

Brand perception and customer preference study

Improved product differentiation and positioning strategy

Supported pricing and portfolio optimization

Identified unmet industrial monitoring requirements

Enhanced competitive positioning across infrastructure applications

Technology & Innovation Assessment

Emerging fiber optic sensing technology trend analysis

Innovation pipeline and patent review

Smart grid and smart city deployment readiness assessment

Ecosystem and strategic partnership mapping

Identified future growth and innovation opportunities

Supported technology roadmap and commercialization planning

Evaluated adoption potential across industrial sectors

Strengthened strategic collaboration and partnership decisions

Frequently Asked Questions About This Report

The global distributed fiber optic sensor market size was valued at USD 1.6 billion in 2025 and is estimated at USD 1.8 billion for 2026.

The global distributed fiber optic sensor market is expected to grow at a CAGR of 11.9% from 2026 to 2033, reaching USD 3.9 billion by 2033.

Asia Pacific is the fastest-growing region over the forecast period.

Some key players operating in the distributed fiber optic sensor market include Schlumberger Limited; Halliburton; Yokogawa Electric Corporation; OFS Fitel, LLC; Omnisens SA; Brugg Kable AG; AP Sensing GmbH; Baker Hughes Company; Silixa Ltd; Luna Innovations Inc.

Key factors driving the DFOS market growth include the growing adoption of real-time monitoring across critical infrastructure, the rising integration of AI and advanced analytics into DFOS platforms, increasing deployment in harsh and remote terrain, and expanding use cases in smart cities & environmental monitoring.

The temperature sensing segment led with over 45.0% revenue share in 2025.

The Raman effect segment held the largest revenue share of 34% in 2025.

The rail infrastructure monitoring segment held the largest revenue share in 2025.

North America dominated the market with over 30.0% revenue share in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.