- Home

- »

- Communications Infrastructure

- »

-

Fiber Optics Market Size & Share Report, 2026-2033GVR Report cover

![Fiber Optics Market (2026 - 2033)Report]()

Fiber Optics Market (2026 - 2033)

Size, Share & Trend Analysis Report By Type (Single Mode, Multi-mode, Plastic Optical Fiber (POF)), By Application (Telecom, Oil & Gas, BFSI, Military & Aerospace, Medical, Railway, Others), By Region, And Segment Forecasts

Market Size, 2025

$10.8BMarket Estimate, 2026

$11.5BMarket Forecast, 2033

$18.0BCAGR, 2026–2033

6.6%Fiber Optics Market Summary

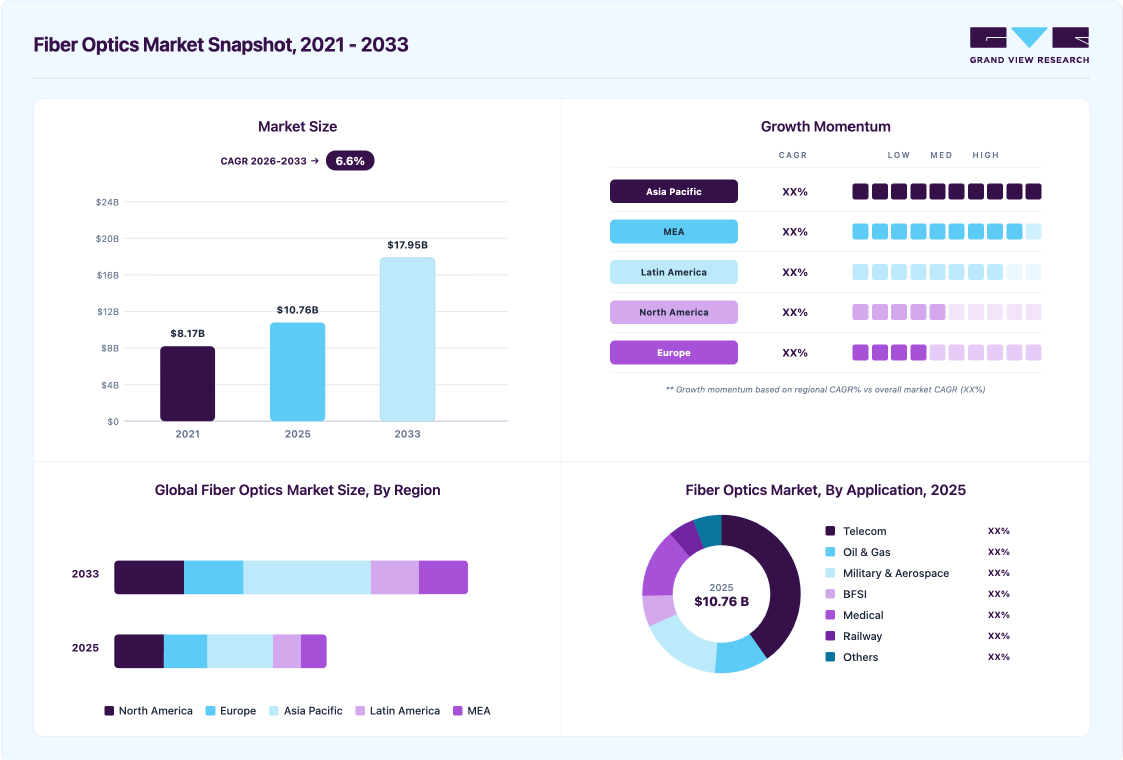

The global fiber optics market size was valued at USD 10.8 billion in 2025 and is projected to grow from USD 11.5 billion in 2026 to USD 18.0 billion by 2033, at a CAGR of 6.6% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 30.9% in 2025. The rapid advancement of high-speed communication networks is driving widespread fiber deployment, rising data traffic from cloud computing and video streaming is boosting demand for optical connectivity, growing adoption of fiber in smart city and IoT infrastructure is accelerating market expansion, and continuous innovations in fiber materials and transmission technologies are enhancing performance and supporting long-term market scalability.

Key Market Trends & Insights

- By type: Multi-mode segment held the largest market share of 53% in 2025.

- By application: Telecom segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (30.9% revenue share, 2025)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 10.8 Billion

- Estimated market size in 2026: USD 11.5 Billion

- Projected market size by 2033: USD 18.0 Billion

- CAGR (2026-2033): 6.6%

The global push for high-speed connectivity is driving large-scale deployments of fiber networks across urban and rural regions. Governments and private operators are accelerating fiber-to-the-home (FTTH) rollouts to support next-generation digital services. Rising internet consumption, fueled by remote work and cloud adoption, is further boosting demand for high-capacity fiber infrastructure. Network operators are prioritizing fiber upgrades to replace aging copper systems and enhance service reliability. Overall, broadband modernization remains a core driver of fiber optics market expansion.Energy and utility operators are rapidly integrating fiber to strengthen real-time control and monitoring capabilities. Smart grid initiatives rely on high-speed fiber to coordinate distributed energy resources and precision demand management. Fiber connectivity is dramatically improving fault detection and enabling faster outage response across grid networks. Renewable energy facilities are also leveraging fiber links to support seamless communication between field assets and control centers. As digital substations evolve, fiber is becoming the preferred medium for secure and interference-free data flow. The modernization of the energy sector is positioning fiber as a critical driver of future grid resilience.")

Innovations in photonics are actively pushing fiber network efficiency to new performance thresholds. Companies are rolling out advanced WDM systems and high-speed transceivers to expand bandwidth capacity. Newer fiber types, including bend-insensitive and ultra-low-loss variants, are enabling more flexible deployment in dense environments. Enhanced optical amplifiers and connector technologies are improving long-distance signal strength and reducing transmission loss. Integrated photonics chips redefine optical processing speeds and creating new industry benchmarks. Collectively, these technological leaps are driving stronger adoption of next-generation fiber infrastructure.

Market Dynamics

The rapid expansion of cloud computing platforms and digital content ecosystems is significantly accelerating demand for advanced fiber optic infrastructure worldwide. Enterprises across industries are increasingly migrating workloads, applications, and storage environments to cloud-based architectures, creating substantial requirements for high-speed and low-latency optical communication networks. Simultaneously, the rising consumption of ultra-high-definition video streaming, online gaming, virtual collaboration platforms, and over-the-top (OTT) media services is intensifying global internet traffic volumes. Telecom operators and network providers are therefore investing aggressively in fiber optic backbone networks to support uninterrupted data transmission and enhanced network reliability. This growing dependence on data-intensive digital services continues to position fiber optics as a critical enabler of scalable and resilient connectivity infrastructure.

The increasing adoption of artificial intelligence applications, edge computing, and hyperscale data center operations is further strengthening the demand outlook for fiber optic technologies. Cloud service providers are expanding interconnectivity capabilities between data centers to manage rising data processing requirements and maintain operational efficiency across distributed computing environments. In parallel, streaming platforms are enhancing content quality through 4K, 8K, and immersive video experiences, which require significantly higher bandwidth capacities supported by fiber networks. Businesses are also prioritizing high-performance connectivity solutions to enable seamless digital operations, remote workforce collaboration, and real-time analytics capabilities. As a result, the sustained growth in cloud-driven workloads and digital media consumption is expected to remain a major long-term growth driver for the fiber optics market.

The increasing dependence on fiber optic infrastructure for critical communication networks has heightened concerns regarding physical cable damage and service disruptions. Fiber optic cables are highly vulnerable to accidental cuts caused by construction activities, road excavation projects, natural disasters, and infrastructure expansion works. Such incidents can lead to significant network downtime, interrupted data transmission, and operational losses for telecom operators, enterprises, and cloud service providers. In sectors requiring uninterrupted connectivity, including financial services, healthcare, transportation, and data centers, even short-term disruptions can negatively impact business continuity and customer experience. Consequently, the growing frequency of physical infrastructure damage remains a major restraint affecting the reliability and operational efficiency of fiber optic networks.

In addition, repairing damaged fiber optic infrastructure often requires specialized technical expertise, advanced testing equipment, and substantial maintenance expenditures, which increase operational complexity for network providers. Fiber restoration activities can also result in prolonged service outages, particularly in remote or densely populated urban regions where cable accessibility remains challenging. The rising deployment of undersea and long-haul fiber networks further intensifies these risks, as environmental conditions and accidental anchor or fishing activities can severely damage submarine cables. Moreover, businesses relying heavily on high-speed connectivity face increasing financial and reputational risks associated with recurring network interruptions and service instability. As a result, concerns related to infrastructure vulnerability and network resilience continue to restrain the large-scale expansion of fiber optic deployments across several regions.

The rapid digital transformation across emerging economies is creating substantial growth opportunities for the fiber optics market. Governments and telecom operators in developing regions are increasingly investing in broadband expansion initiatives to improve internet accessibility, strengthen digital infrastructure, and accelerate economic development. Rising smartphone penetration, expanding digital payment ecosystems, and growing adoption of cloud-based services are significantly increasing the demand for high-speed and reliable connectivity solutions. In addition, the expansion of e-learning platforms, telemedicine services, e-commerce activities, and remote working models is further driving the need for advanced fiber optic communication networks. As a result, emerging economies are becoming key investment destinations for fiber optic manufacturers, network infrastructure providers, and telecom service operators.

The ongoing deployment of 5G infrastructure and smart city projects across Asia Pacific, Latin America, the Middle East, and Africa is further strengthening market opportunities for fiber optic technologies. Several governments are introducing favorable regulatory frameworks, public-private partnerships, and digital inclusion programs to accelerate nationwide fiber network deployment. Telecom companies are also expanding fiber-to-the-home (FTTH) and fiber-to-the-business (FTTB) connectivity to address the growing consumer and enterprise demand for high-bandwidth internet services. Furthermore, increasing foreign direct investments in data centers, industrial automation, and digital infrastructure projects are expected to enhance long-term market expansion prospects. Consequently, the rising need for scalable and high-capacity communication infrastructure in emerging economies is anticipated to create significant revenue generation opportunities for the global fiber optics market over the forecast period.

Market Concentration & Characteristics

The fiber optics market is moderately concentrated, with established cable manufacturers, telecom infrastructure providers, and optical technology companies competing across broadband, data center, industrial, and 5G network applications. Leading players strengthen their market positions through large-scale manufacturing capabilities, advanced optical fiber technologies, strong telecom partnerships, and global distribution networks. Emerging and regional companies are increasingly focusing on cost-effective fiber deployment solutions, localized broadband expansion projects, and customized connectivity offerings to address evolving customer requirements. The rapid growth of hyperscale data centers, 5G infrastructure, fiber-to-the-home (FTTH) deployments, and cloud computing services is intensifying market competition and accelerating technological innovation across the industry. Strategic collaborations, capacity expansion initiatives, investments in next-generation optical communication technologies, and acquisitions remain key competitive strategies as companies seek to enhance network performance, improve scalability, and strengthen their global market presence.

The fiber optics market faces competition from wireless communication technologies, satellite internet solutions, and legacy copper-based infrastructure that continue to serve specific connectivity requirements in certain regions and applications. Some enterprises and telecom operators may delay fiber deployment due to high infrastructure installation costs, complex network upgrades, and lengthy regulatory approval processes. In addition, advancements in fixed wireless access (FWA), low-earth orbit (LEO) satellite connectivity, and hybrid communication technologies are increasing competitive pressure within broadband and enterprise networking segments. Nevertheless, fiber optic solutions maintain a strong competitive advantage due to their superior bandwidth capacity, low latency, enhanced reliability, and long-distance data transmission capabilities. The increasing global demand for high-speed internet connectivity, AI-driven data center expansion, smart city infrastructure, and digital transformation initiatives continues to support long-term market growth and sustained investment in fiber optic network deployment.

Type Insights

The multi-mode segment led the market, accounting for over 53% of the global revenue in 2025, driven by its cost-efficient deployment and strong bandwidth performance for short-to-medium distance applications. Enterprises increasingly adopted multi-mode fiber to support high-density connectivity for cloud workloads and internal communication systems. Its lower transceiver costs and easy installation made it a preferred option for modernizing data centers and campus networks. The segment also gained momentum due to rising demand for scalable LAN infrastructure across commercial and institutional environments. Overall, multi-mode fiber maintained a dominant market position by offering a compelling balance of performance, scalability, and cost efficiency.

The plastic optical fiber segment is predicted to experience significant growth in the forecast period, owing to its low-cost installation, high flexibility, and suitability for short-distance communication applications. Its ease of handling and resistance to bending make it highly attractive for consumer electronics, automotive systems, and home networking solutions. The growing adoption of in-vehicle infotainment, advanced driver-assistance systems, and smart home devices is further accelerating demand for plastic optical fiber. Manufacturers are also leveraging its lightweight design to support compact, space-efficient system architectures. As a result, the segment is positioned to capture strong growth as industries increasingly prioritize affordable and adaptable optical connectivity solutions.

Application Insights

The telecom segment is expected to hold the highest market share of the global revenue in 2025, primarily driven by accelerating investments in fiber-based broadband expansion and large-scale 5G rollout initiatives. Operators are rapidly upgrading legacy copper networks to fiber to support higher bandwidth, lower latency, and improved service reliability. The surge in mobile data consumption, cloud adoption, and video streaming is further pushing telecom providers to strengthen their fiber backbone infrastructure. Additionally, rising deployment of fiber for small-cell densification and next-generation network architectures is reinforcing market leadership for the telecom sector.

The medical segment is projected to achieve substantial growth over the forecast period. Rising adoption of fiber optic technology in medical imaging, endoscopy, and minimally invasive procedures is driving strong demand. Healthcare providers are increasingly deploying fiber-based solutions to enhance imaging resolution, patient monitoring, and diagnostic accuracy. Continuous advancements in fiber optic sensors and wearable medical devices are further accelerating market penetration. As a result, the segment is well-positioned for sustained expansion, driven by the healthcare industry’s focus on precision, efficiency, and reliable data transmission.

Regional Insights

North America fiber optics market is expected to hold a significant share of over 23% in 2025. The region’s leadership is driven by robust investments in high-speed broadband infrastructure and large-scale 5G deployment. Strong adoption of cloud computing, data centers, and enterprise networking solutions continues to fuel demand for advanced fiber technologies. Government initiatives and private sector commitments to upgrade legacy networks further reinforce the market’s growth trajectory.

U.S. Fiber Optics Market Trends

The U.S. fiber optics market maintains a strong position owing to rapid network modernization and digital transformation initiatives. Telecom operators are investing heavily in fiber-to-the-home (FTTH) and fiber-to-the-premises (FTTP) projects to meet growing bandwidth needs. Increasing deployment of smart city projects and enterprise connectivity solutions further drives adoption. The market benefits from a well-established technology ecosystem, high-capacity infrastructure, and supportive regulatory frameworks.

Europe Fiber Optics Market Trends

Europe fiber optics market is expanding steadily, supported by extensive broadband rollout programs and 5G network expansion. Government-backed initiatives to enhance digital infrastructure across both urban and rural areas are key growth drivers. Demand is rising from data centers, industrial automation, and enterprise networks requiring high-capacity and reliable fiber solutions. The region’s focus on sustainable and energy-efficient network deployments further strengthens fiber adoption.

Asia Pacific Fiber Optics Market Trends

Asia Pacific is expected to record the fastest CAGR over the forecast period, driven by rapid urbanization, large-scale 5G deployment, and increasing demand for high-speed broadband connectivity. Telecom operators and government initiatives are accelerating fiber network expansion to support growing internet penetration and enterprise digitalization.

The surge in data center construction, cloud adoption, and smart city projects is further fueling fiber optics demand. Combined with supportive policies and industrial automation trends, these factors are positioning the region as the fastest-growing market for fiber solutions.

Key Fiber Optics Company Insights

Some key companies in the fiber optics industry are Corning Incorporated, Prysmian Group, Sterlite Technologies Limited, Yangtze Optical Fiber and Cable Joint Stock Limited Company (YOFC), AFL

-

Corning is a prominent player in optical fiber and cable solutions, specializing in high-performance fiber for telecommunications, data centers, and enterprise networks. The company develops and manufactures optical fiber, cable, and related connectivity solutions that support high-speed data transmission. Its innovations include bend-insensitive fiber and advanced glass technologies that enhance network reliability and performance. Corning serves a wide range of industries, including telecom, cloud services, and industrial automation, maintaining a strong presence in the fiber optics market.

-

Prysmian Group is a manufacturer of optical fibers, cables, and systems for telecom, energy, and industrial applications. The company offers solutions for high-capacity long-distance networks, including submarine and terrestrial fiber optic infrastructure. Prysmian invests heavily in R&D to develop next-generation fiber technologies, such as ultra-low-loss and bend-insensitive fibers. Its global footprint and comprehensive product portfolio make it a key player in enabling digital transformation and network modernization worldwide.

Key Fiber Optics Companies:

The following are the leading companies in the fiber optics market. These companies collectively hold the largest Market share and dictate industry trends.

- AFL

- Birla Furukawa Fiber Optics Limited

- Corning Incorporated

- Finolex Cables Limited

- Molex, LLC

- OFS Fitel, LLC

- Optical Cable Corporation (OCC)

- Prysmian Group

- Sterlite Technologies Limited

- Yangtze Optical Fiber and Cable Joint Stock Limited Company (YOFC)

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Corning Incorporated; Prysmian Group; OFS Fitel, LLC

- Focus on expanding high-capacity fiber optic production and global broadband infrastructure partnerships to address rising telecom and data center demand.

- Invest heavily in next-generation optical fiber technologies, submarine cable systems, and hyperscale connectivity solutions.

- Strong global manufacturing capabilities, established telecom relationships, and diversified product portfolios strengthen market leadership.

- Advanced R&D expertise and large-scale deployment experience enable delivery of reliable and high-performance fiber optic solutions..

- High capital investment requirements and dependence on raw material supply chains can impact operational flexibility.

- Large organizational structures may slow responsiveness to rapidly evolving optical communication technologies and regional market shifts.

Emerging Players: Sterlite Technologies Limited; HFCL Limited; Optical Cable Corporation (OCC)

- Focus on cost-effective fiber deployment solutions and localized broadband expansion projects to capture emerging market opportunities.

- Prioritize flexible manufacturing, rapid network customization, and innovation in FTTH and 5G fiber infrastructure solutions.

- Strong agility and faster deployment capabilities support rapid response to changing telecom and enterprise connectivity requirements.

- Competitive pricing strategies and regional expansion initiatives help strengthen presence in high-growth developing markets.

- Limited global brand visibility and smaller financial scale may restrict expansion across large international infrastructure projects.

- Dependence on regional demand cycles and telecom spending can increase operational and revenue volatility.

Recent Developments

-

In November 2025, Crown Fiber Optics announced it had secured over USD 100 million in multi-year fiber infrastructure contracts. These agreements cover major broadband projects in New Mexico and the Seattle area, each contributing significant annual revenue. Additional rural broadband contracts in Oregon, including RUS-funded initiatives, further increased the company’s backlog. This achievement demonstrates strong demand for fiber-optic infrastructure and reinforces Crown Fiber’s commitment to providing high-quality broadband solutions in both urban and rural markets.

-

In October 2025, Fraunhofer IIS launched SpikeHERO, an initiative to develop an AI chip that combines optical and electrical spiking neural network processing for fiber-optic networks. The project seeks to improve signal quality and increase data transmission rates by integrating brain-inspired SNN technology into fiber infrastructure. SpikeHERO is expected to reduce latency, enhance energy efficiency, and support next-generation digital networks. This initiative demonstrates the increasing convergence of advanced AI hardware and fiber-optic communications to address the demand for high-speed, efficient data transmission.

-

In September 2025, Relativity Networks partnered with Network Planning Solutions (NPS) to accelerate the deployment of its hollow-core fiber (HCF) infrastructure. NPS, as the first “Trusted Installation Partner,” manages planning, pre-staging, installation, and ongoing support for HCF rollouts. This collaboration streamlines large-scale deployment, enabling faster and more efficient implementation of next-generation fiber networks. Clients in AI, cloud computing, and high-performance networking benefit from lower latency and higher data throughput compared to conventional fiber solutions.

-

In September 2025, VCTI launched VCTI‑RoBERTa‑Fiber, an open-source AI encoder model tailored for the optical communications and photonics industry. Trained on fiber-optic datasets, the model understands technical language and industry requirements. It supports semantic search, intelligent chatbots, predictive maintenance, and automated network fault detection. By releasing the model openly, VCTI seeks to accelerate innovation, shorten product development cycles, and promote collaboration within the optical communications ecosystem.

Fiber Optics Market Report Scope

Report Attribute

Details

Market size in 2025

USD 10.8 billion

Estimated market size in 2026

USD 11.5 billion

Projected market size by 2033

USD 18.0 billion

Growth rate

CAGR of 6.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

AFL; Birla Furukawa Fiber Optics Limited; Corning Incorporated; Finolex Cables Limited; OFS Fitel, LLC; Optical Cable Corporation (OCC); Prysmian Group; Sterlite Technologies Limited; Yangtze Optical Fiber; Cable Joint Stock Limited Company(YOFC)

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Fiber Optics Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global fiber optics market report based on type, application, and region.

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Single-Mode

-

Multi-Mode

-

Plastic Optical Fiber

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Telecom

-

Oil & Gas

-

Military & Aerospace

-

BFSI

-

Medical

-

Railway

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Objective

Custom Research Modules Delivered

Strategic Value / Business Impact

Market Entry & Expansion Assessment

- Regional fiber optic demand sizing and traffic forecasting

- Telecom operator and enterprise connectivity adoption analysis

- Competitive benchmarking of fiber network providers and OEMs

- Regulatory, infrastructure, and broadband deployment assessment

- Identified high-growth regional deployment opportunities

- Supported market entry and network expansion strategies

- Highlighted investment risks and infrastructure gaps

- Enabled data-driven fiber expansion planning

Product Positioning & Competitive Intelligence

- Fiber cable and optical component benchmarking

- Pricing, bandwidth, and performance comparison analysis

- Customer preference and network reliability assessment

- Competitor technology and deployment strategy evaluation

- Improved product differentiation and positioning strategy

- Supported pricing and solution optimization initiatives

- Identified unmet connectivity and performance requirements

- Enhanced competitive advantage in telecom and data center markets

Technology & Innovation Assessment

- Next-generation optical fiber technology analysis

- Photonics innovation and patent review

- Fiber modernization readiness assessment

- Identified future technology growth areas

- Supported innovation roadmap planning

- Evaluated commercialization potential

Frequently Asked Questions About This Report

The global fiber optics market size was valued at USD 10.8 billion in 2025 and is estimated at USD 11.5 billion for 2026.

The multi-mode segment led with a 53% revenue share in 2025, while the plastic optical fiber segment is the fastest-growing.

The telecom segment held the largest revenue share in 2025, while the medical segment is the fastest-growing.

The global fiber optics market is expected to grow at a CAGR of 6.6% from 2026 to 2033, reaching USD 18.0 billion by 2033.

Asia Pacific dominated with a 30.9% revenue share in 2025.

Key players include AFL; Birla Furukawa Fiber Optics Limited; Corning Incorporated; Finolex Cables Limited; OFS Fitel, LLC; Optical Cable Corporation (OCC); Prysmian Group; Sterlite Technologies Limited; Yangtze Optical Fiber; Cable Joint Stock Limited Company(YOFC)

Key factors driving the growth of the fiber optics market include the rising demand for high-speed broadband and 5G network deployment, increasing data center expansion and cloud computing adoption, growing investments in smart cities and digital infrastructure, and the strong uptake of fiber-to-the-home solutions across residential and enterprise networks.

About the Author(s)

Communications Infrastructure Research Team

Technology · Communications InfrastructureThis report was authored by the communications infrastructure research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the communications infrastructure segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.