- Home

- »

- Next Generation Technologies

- »

-

E-learning Services Market Size & Share Report, 2026-2033GVR Report cover

![E-learning Services Market (2026 - 2033)Report]()

E-learning Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type, By Courses (Self-Paced Courses, Instructor-Led Virtual Courses), By Learning Method (Blended Learning, Mobile Learning, Simulation), By Technology, By End-Use, By Region, And Segment Forecasts

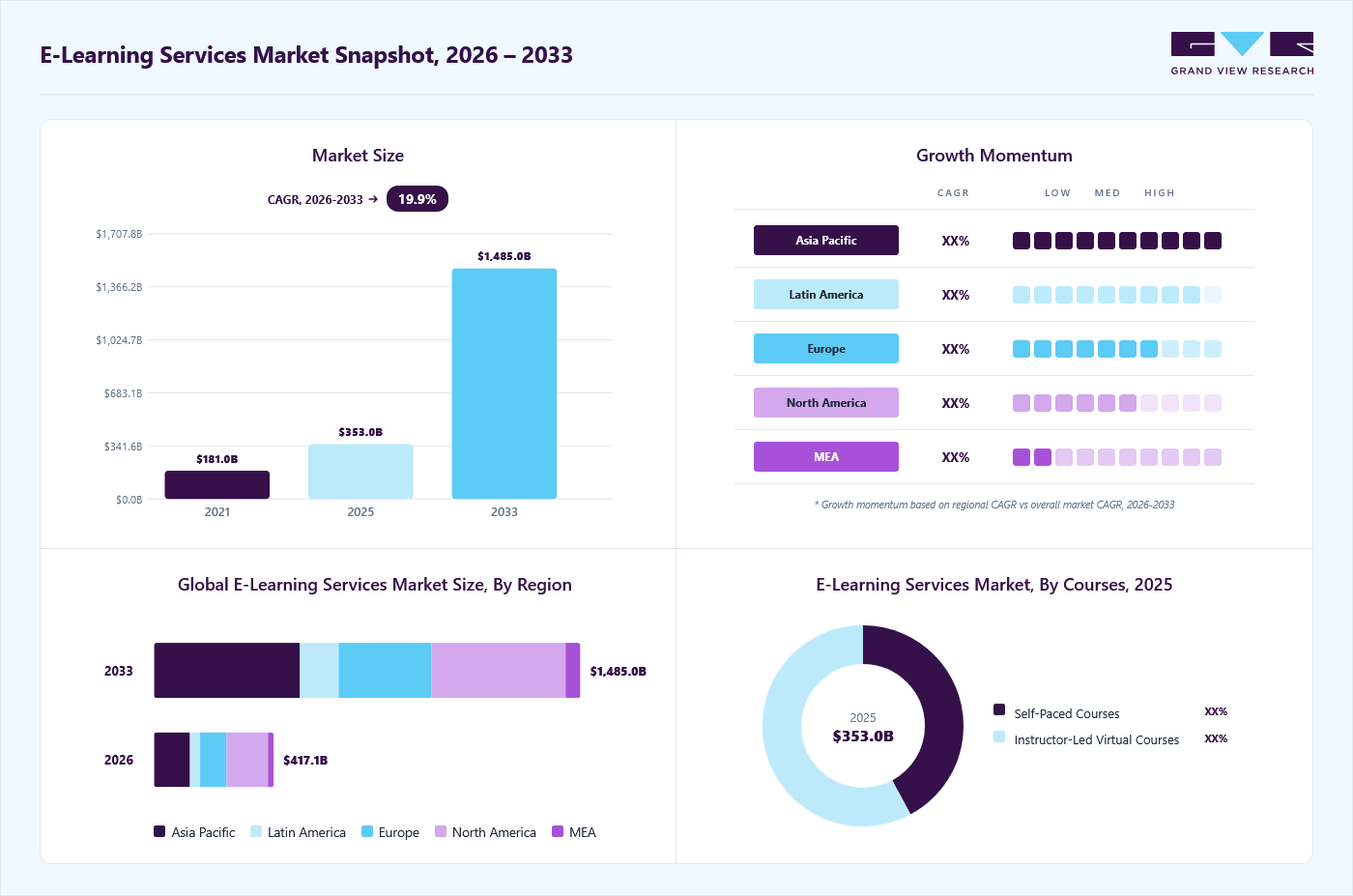

Market Size, 2025

$353.0BMarket Estimate, 2026

$417.1BMarket Forecast, 2033

$1,485.0BCAGR, 2026–2033

19.9%E-learning Services Market Summary

The global e-learning services market size was valued at USD 353.0 billion in 2025 and is projected to grow from USD 417.1 billion in 2026 to USD 1,485.0 billion by 2033, at a CAGR of 19.9% from 2026 to 2033. The market in North America dominated with a revenue share of 34.9% in 2025. This rapid growth is driven by increased adoption of digital learning platforms across educational institutions and corporate sectors, fueled by demand for remote learning and upskilling opportunities.

Key Market Trends & Insights

- By learning method: Blended learning segment held the largest market share of 33.6% in 2025.

- By type: Custom e-learning segment held the largest market share of 29.5% in 2025.

- By courses: Instructor-led virtual courses segment held the largest market share in 2025.

- By technology: Cloud computing segment held the largest market share in 2025.

- By end use: Academic segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (34.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 353.0 Billion

- Estimated market size in 2026: USD 417.1 Billion

- Projected market size by 2033: USD 1,485.0 Billion

- CAGR (2026-2033): 19.9%

Organizations across industries are expanding the use of e-learning services to support employee training, technical skill enhancement, and compliance management, driven by the growing shift toward hybrid and remote work environments. Enterprises are integrating learning management systems, virtual training modules, and cloud-based learning platforms to improve workforce productivity, streamline content delivery, and reduce overall training costs across geographically distributed teams. Interactive learning content, real-time assessments, and digital certification programs are further improving employee participation, engagement, and knowledge retention within corporate training frameworks.")

In addition, companies are placing greater focus on continuous professional development to address rapidly changing technological advancements, operational requirements, and industry standards. The growing demand for flexible, scalable, and accessible training solutions is encouraging organizations to expand investments in digital education infrastructure and online learning ecosystems. Furthermore, the ability of e-learning platforms to deliver content updates more quickly, support performance tracking, and provide personalized training experiences is driving higher adoption across multiple industry verticals.

The increasing availability of high-speed internet services and affordable smart devices is improving access to digital education platforms across emerging economies. Students and working professionals are increasingly accessing online learning resources through smartphones, tablets, and low-cost laptops, supporting wider participation in virtual education programs. Governments and telecom providers are investing in digital infrastructure to improve educational access across urban and rural areas, further supporting market expansion.

Type Insights

The custom e-learning segment led the market with the largest revenue share of 29.5% in 2025, driven by increasing demand for organization-specific training programs across the corporate and academic sectors. Enterprises are focusing on digital learning modules aligned with operational workflows, compliance requirements, and employee skill development objectives. For instance, in March 2025, Upside Learning, part of Mitr Learning & Media, was included in the 2025 Training Industry Custom Content Development Watchlist. This recognition highlights their skill in creating digital learning solutions and custom training programs that support business goals.

The game-based learning segment is predicted to grow at the fastest CAGR during the forecast period. The growing preference for interactive and immersive education models is driving the adoption of game-based learning solutions across schools, universities, and corporate training environments. Educational institutions and enterprises are increasingly incorporating gamification techniques, simulations, and reward-based learning systems to improve learner engagement, participation, and knowledge retention. These platforms support practical skill development, problem-solving abilities, and collaborative learning through engaging digital experiences.

Courses Insights

The instructor-led virtual courses segment accounted for the largest market revenue share in 2025. The increasing adoption of remote and hybrid learning environments is supporting demand for instructor-led virtual courses across academic and corporate sectors. Educational institutions and enterprises are incorporating live online sessions to enable real-time interaction, collaborative learning, and immediate feedback between instructors and learners. These virtual training programs improve accessibility for geographically dispersed participants while reducing travel and infrastructure expenses.

The self-paced courses segment is predicted to grow at the fastest CAGR during the forecast period. Learners are increasingly opting for self-directed modules that allow them to complete courses at their own pace and within their own schedules, accommodating professional commitments. In response, educational institutions and enterprises are adopting self-paced digital content to improve accessibility, scalability, and cost efficiency in training delivery. The increasing availability of mobile-based learning applications and multilingual course content is further supporting the adoption of self-paced courses.

Learning Method Insights

The blended learning segment accounted for the largest market revenue share in 2025. Educational institutions and enterprises are increasingly adopting blended learning models that combine instructor-led training with digital learning platforms to enhance flexibility and learning outcomes. This approach enables learners to access educational content across multiple devices while supporting interactive, self-paced learning. For instance, in March 2026, Atal Innovation Mission (AIM), Learning Links Foundation, and Shell India launched the NXplorers Blended Learning Model to expand STEM innovation and structured problem-solving education across schools in India.

The simulation segment is predicted to grow at the fastest CAGR during the forecast period. The growing focus on practical, experience-based learning is accelerating the adoption of simulation-based learning across healthcare, aviation, manufacturing, and corporate sectors. These learning solutions allow users to practice real-world scenarios within controlled digital environments, improving decision-making, technical skills, and risk management capabilities. Organizations are increasingly integrating virtual, augmented, and AI-enabled simulation platforms to enhance learner engagement and training effectiveness.

Technology Insights

The cloud computing segment accounted for the largest market revenue share in 2025. The increasing adoption of cloud-based learning management systems is contributing to the market growth by enabling scalable and centralized education delivery. Educational institutions and enterprises are increasingly transitioning to cloud infrastructure to enhance content accessibility, improve data storage efficiency, and support remote collaboration. Cloud computing facilitates real-time course updates, seamless integration of multimedia content, and flexible subscription-based learning models accessible across multiple devices.

The artificial intelligence segment is predicted to grow at the fastest CAGR during the forecast period. The integration of artificial intelligence in e-learning services is improving personalization, learner engagement, and assessment efficiency across digital education platforms. AI-powered recommendation engines and adaptive learning systems analyze user behavior to deliver customized course pathways and targeted educational content, creating more individualized learning experiences. Educational institutions and corporate training providers are increasingly adopting AI-based chatbots, automated grading systems, and virtual assistants to improve learner support and streamline administrative processes.

End Use Insights

The academic segment accounted for the largest market revenue share in 2025. The academic sector is experiencing strong adoption of e-learning services as schools, universities, and higher education institutions continue integrating digital education platforms into their learning environments. Educational organizations are increasing the use of virtual classrooms, online assessments, and cloud-based learning management systems to enhance accessibility, flexibility, and student engagement. The expanding adoption of remote and hybrid learning models is driving investments in scalable digital learning infrastructure and interactive educational content.

The corporate segment is projected to grow at the fastest CAGR over the forecast period. The corporate sector is increasingly adopting e-learning services to support workforce training, employee upskill, and compliance management across geographically distributed operations. Organizations are integrating digital learning platforms to deliver flexible, cost-efficient training programs that improve productivity and operational efficiency while addressing the rising need for continuous learning amid rapid technological advancements across industries.

Regional Insights

North America dominated the e-learning services market with the largest revenue share of 34.9% in 2025, supported by advanced digital infrastructure and the strong presence of established online education providers across the region. Educational institutions and enterprises are increasingly adopting immersive technologies, such as virtual simulations and interactive learning environments, to enhance learner engagement and training efficiency. The growing adoption of subscription-based and self-paced learning models is also contributing to the continued expansion of the North America market.

U.S. E-learning Services Market Trends

The e-learning services market in the U.S. accounted for the largest revenue share in North America in 2025, driven by the increasing integration of AI and data analytics into digital learning platforms across academic and corporate environments. Enterprises are expanding investments in digital leadership training, cybersecurity education, and technology-oriented workforce development programs to address industry-wide skill gaps. The strong presence of established educational technology providers and online certification platforms continues to support the expansion of advanced learning solutions across the country.

Europe E-learning Services Market Trends

The e-learning services market in Europe is experiencing steady growth due to the rising importance on multilingual digital education and cross-border academic collaboration among educational institutions. In parallel, regulatory initiatives focused on workforce reskilling and vocational education are encouraging enterprises to implement structured digital learning and professional certification programs. Organizations across the region are also integrating sustainability-focused and compliance-oriented training modules into corporate learning platforms to support evolving industry requirements.

Asia Pacific E-learning Services Market Trends

The e-learning services market in the Asia Pacific is anticipated to grow at the fastest CAGR during the forecast period,due to its large student population and the rising demand for affordable digital education solutions across developing economies. Governments across the region are implementing digital education initiatives to improve access to quality learning resources in rural and underserved areas. The growing popularity of competitive examination preparation platforms and skill development courses is further driving demand for online learning services.

Key E-learning Services Company Insights

Some key companies in the e-learning services industry are SAP SE, BYJU’S,edX LLC, McGraw Hill

-

BYJU’S operates as a digital education platform offering learning programs for school students, competitive examinations, and skill-based education across multiple academic categories. The company provides interactive video-based lessons, adaptive learning modules, live classes, and personalized study support designed to improve student engagement and conceptual understanding. Its platform integrates artificial intelligence-enabled learning analytics to track learner performance and deliver customized educational experiences. BYJU’S also offers programs focused on test preparation, early learning, and professional education through digital and hybrid learning formats.

-

edX operates as an online learning platform providing professional courses, certification programs, and degree-based education in collaboration with universities and industry organizations. The platform offers courses across multiple disciplines, including business management, computer science, artificial intelligence, healthcare, and data analytics. edX also supports career-focused learning through micro-credentials, executive education, and industry-recognized certification programs aligned with evolving workforce requirements. The platform integrates assessment tools, progress-tracking systems, and multilingual course accessibility to improve learner engagement and educational access.

Key E-learning Services Companies:

The following key companies have been profiled for this study on the E-learning services market.

- McGraw-Hill

- SAP SE

- IBM Corporation

- upGrad Education Private Limited

- NIIT (USA) Inc.

- Adobe

- LinkedIn Corporation

- Docebo

- Coursera Inc.

- BYJU’S

- edX LLC

- Udemy, Inc.

- Udacity, Inc.

Recent Developments

-

In April 2026, Docebo launched Docebo AgentHub, integrating skills intelligence, enterprise knowledge, and agentic AI into a unified learning platform. The platform enhancement supports enterprise learning workflows through AI-driven automation, knowledge access, and personalized learning experiences.

-

In April 2026, McGraw-Hill launched new AI features in the Connect digital course solution, a conversational AI tutor designed to provide real-time academic support. The platform also added AI-powered translation tools and AI literacy modules to help students understand course materials and apply generative AI responsibly.

-

In December 2025, Udemy introduced new instructor-focused innovations, including AI-powered micro-learning tools and instructor subscription features. These initiatives supported enhanced learner engagement and diversified content delivery formats across enterprise and individual learning segments.

-

In September 2025, Coursera announced the launch of Skills Tracks, a data-backed learning solution designed to support role-based skill development across functional teams. The platform integrates expert-led content, hands-on practice, and verified assessments to help organizations address workforce skill gaps through structured learning pathways.

E-learning Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 353.0 billion

Estimated market size in 2026

USD 417.1 billion

Projected market size by 2033

USD 1,485.0 billion

Growth rate

CAGR of 19.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, curses, learning method, technology, end use, regional.

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

McGraw Hill; SAP SE; IBM Corporation; upGrad Education Private Limited; NIIT (USA) Inc.; Adobe; LinkedIn Corporation; Docebo; Coursera Inc.; BYJU’S; edX LLC; Udemy, Inc.; Udacity, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global E-learning Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global e-learning services market report based on type, courses, learning method, technology, end-use, and region:

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Custom E-Learning

-

Responsive E-Learning

-

Micro E-Learning

-

Translation & Localization

-

Game-Based Learning

-

Rapid E-Learning

-

-

Courses Outlook (Revenue, USD Billion, 2021 - 2033)

-

Self-Paced Courses

-

Instructor-Led Virtual Courses

-

-

Learning Method Outlook (Revenue, USD Billion, 2021 - 2033)

-

Blended Learning

-

Mobile Learning

-

Virtual Classrooms

-

Simulation

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud Computing

-

Big Data

-

Augmented Reality and Virtual Reality

-

Artificial Intelligence

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Academic

-

Corporate

-

Government

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

Key factors driving market growth include the increasing adoption of digital learning platforms across educational institutions and the corporate sector, fueled by demand for remote learning and upskilling opportunities.

Asia Pacific is the fastest-growing region over the forecast period.

The custom e-learning segment led with a 29.5% revenue share in 2025, while game-based learning is the fastest-growing type.

Instructor-led virtual courses segment held the largest revenue share in 2025, while self-paced courses is the fastest-growing courses.

The blended learning segment led with a 33.6% revenue share in 2025, while simulation is the fastest-growing method.

Cloud computing segment held the largest share in 2025, while artificial intelligence is the fastest-growing technology.

Key players include McGraw Hill; SAP SE; IBM Corporation; upGrad Education Private Limited; NIIT (USA) Inc.; Adobe; LinkedIn Corporation; Docebo; Coursera Inc.; BYJU’S; edX LLC; Udemy, Inc.; Udacity, Inc.

The global e-learning services market size was valued at USD 353.0 billion in 2025 and is estimated at USD 417.1 billion for 2026.

The global e-learning services market is expected to grow at a CAGR of 19.9% from 2026 to 2033, reaching USD 1,485.0 billion by 2033.

North America dominated the e-learning services market with a 34.9% market share in 2025, supported by advanced digital infrastructure and the strong presence of established online education providers across the region.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.