- Home

- »

- Next Generation Technologies

- »

-

Embedded Lending Market Size & Share Report, 2026-2033GVR Report cover

![Embedded Lending Market (2026 - 2033)Report]()

Embedded Lending Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Platform, Services), By Deployment (Cloud-based, On-premise), By Enterprise, By Industry (Retail, Education, Real Estate), By Region, And Segment Forecasts

Market Size, 2025

$21.5BMarket Estimate, 2026

$28.4BMarket Forecast, 2033

$250.9BCAGR, 2026–2033

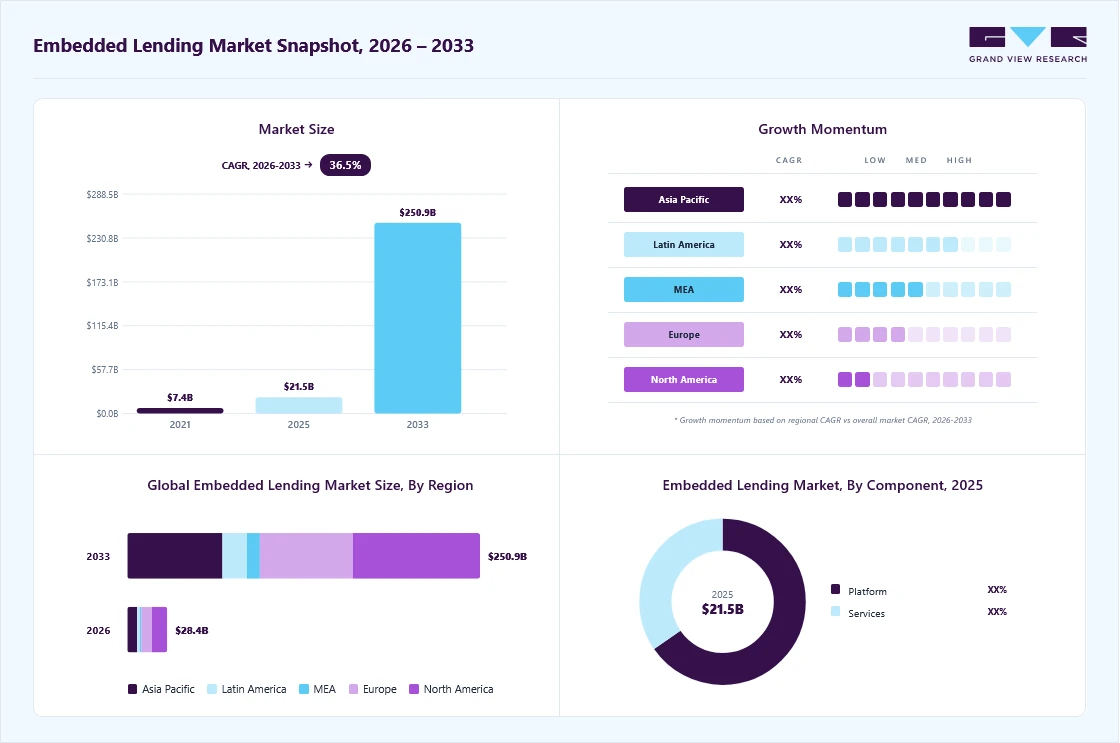

36.5%Embedded Lending Market Summary

The global embedded lending market size was valued at USD 21.5 billion in 2025 and is projected to grow from USD 28.4 billion in 2026 to USD 250.9 billion by 2033, at a CAGR of 36.5% from 2026 to 2033. The market in North America dominated with a revenue share of 38.6% in 2025. Rising demand for seamless access to credit at the point of need across digital platforms is driving the growth of the market.

Key Market Trends & Insights

- By component: Platform segment held the largest market share of 65.3% in 2025.

- By enterprise: Small and mid-sized enterprises (SMEs) segment held the largest market share in 2025.

- By deployment: Cloud-based segment held the largest market share in 2025.

- By industry: Retail segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (38.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 21.5 Billion

- Estimated market size in 2026: USD 28.4 Billion

- Projected market size by 2033: USD 250.9 Billion

- CAGR (2026-2033): 36.5%

Businesses are increasingly integrating lending solutions into e-commerce websites, B2B marketplaces, accounting software, and service platforms to improve customer conversion rates, increase transaction values, and strengthen user retention. Small and mid-sized enterprises (SMEs) are also adopting embedded credit products to address working capital gaps and cash flow requirements. In addition, the growing penetration of smartphones, the adoption of digital payments, and the expansion of online commerce are creating a favorable environment for embedded lending globally.")

Technological innovation is reshaping the competitive landscape of the embedded lending industry. API-first architectures, cloud-native lending platforms, and Banking-as-a-Service (BaaS) models are enabling faster deployment and easier integration of credit products into non-financial platforms. Artificial intelligence and machine learning are increasingly being used for automated underwriting, fraud detection, credit scoring, and personalized loan offers based on real-time user behavior. Open banking frameworks and alternative data sources are also improving lending decisions by allowing providers to assess borrower eligibility more accurately and efficiently.

The rapid expansion of digital commerce and platform-based business models is supporting market growth. Online retailers, B2B marketplaces, software-as-a-service (SaaS) providers, and gig economy platforms are integrating lending products to improve conversion rates, increase basket sizes, and strengthen customer loyalty. For merchants and platform operators, embedded lending also creates new revenue streams through commissions, interest-sharing models, or financing fees, making it an attractive value-added service.

Growing financing needs among small and mid-sized enterprises (SMEs) are accelerating demand for embedded lending solutions. Many SMEs face challenges in accessing traditional bank credit due to lengthy approval processes, collateral requirements, or limited credit history. Embedded lending platforms use transaction data, payment flows, and operational metrics from digital ecosystems to assess risk more efficiently and offer faster access to working capital, invoice financing, and short-term business loans. This has made embedded lending particularly relevant for underserved business segments.

Despite strong growth prospects, the embedded lending industry faces several restraints. Credit risk and rising default rates remain key concerns, especially during periods of economic uncertainty or high interest rates. Many providers also face challenges related to fraud, customer acquisition costs, and the complexity of integrating lending solutions into legacy enterprise systems. Regulatory uncertainty across jurisdictions can delay expansion plans and increase compliance costs. In addition, consumer trust issues regarding data usage, hidden fees, and over-indebtedness may limit adoption in certain markets.

Component Insights

The platform segment accounted for the largest share of 65.3% in 2025. The increasing adoption of API-based lending infrastructure, cloud-native loan management systems, and white-label financing solutions by digital platforms and enterprises is driving the growth of the platform segment. Businesses across e-commerce, retail, SaaS, and B2B marketplaces are seeking scalable technology that enables them to integrate credit offerings directly into customer journeys without developing in-house lending capabilities. Platforms provide automated underwriting, loan origination, compliance workflows, repayment management, and analytics, enabling faster, more cost-efficient deployment. In addition, rising demand for seamless user experiences, real-time approvals, and personalized financing options is encouraging organizations to invest in embedded lending platforms that can support high transaction volumes and multi-market expansion.

The services segment is expected to grow at a significant CAGR during the forecast period. The services segment is growing steadily as enterprises require specialized support to implement, customize, and manage embedded lending solutions. Many organizations depend on consulting, system integration, onboarding, risk management, compliance advisory, and managed services to launch lending programs within existing digital ecosystems successfully. Due to the increasing complexity of regulatory requirements, businesses are relying more on service providers for KYC, AML, fraud prevention, and data security support. Furthermore, companies operating with legacy systems often need technical assistance to connect embedded lending platforms with ERP, CRM, payment gateways, and other enterprise software, which continues to drive demand for professional and managed services.

Deployment Insights

The cloud-based segment dominated the market in 2025. The increasing preference for scalable, flexible, and cost-efficient deployment models among fintech companies, lenders, and enterprises is fueling the growth of the segment. Cloud-based embedded lending platforms enable faster implementation, lower upfront infrastructure investment, and seamless integration with e-commerce platforms, payment gateways, ERP systems, and digital marketplaces through APIs. Businesses also benefit from automatic software updates, real-time analytics, remote accessibility, and the ability to scale operations based on transaction demand.

The on-premise segment is projected to grow at a significant CAGR of 33.4% over the forecast period. The on-premise segment continues to grow steadily as many traditional banks, financial institutions, and large enterprises prioritize greater control over data, infrastructure, and security environments. Organizations operating in highly regulated sectors often prefer on-premise deployment to meet internal governance requirements, data residency policies, and strict cybersecurity standards. On-premise systems also allow deeper customization and easier alignment with legacy IT architecture, making them suitable for institutions with complex operational workflows.

Enterprise Insights

The small and mid-sized enterprises (SMEs) segment dominated the market in 2025. The increasing demand for quick, accessible financing solutions to manage working capital, inventory purchases, payroll, and day-to-day cash flow needs is driving the adoption of embedded lending among SMEs. Many SMEs face challenges obtaining traditional bank loans due to lengthy approval timelines, collateral requirements, or limited credit histories. Embedded lending platforms address these gaps by leveraging transaction data, sales history, and platform activity to provide faster credit decisions and simplified digital loan applications. In addition, the rising adoption of e-commerce marketplaces, accounting software, and SME-focused SaaS platforms is creating new channels through which financing can be offered to small businesses seamlessly.

The large enterprise segment is expected to grow at a significant CAGR over the forecast period. The large enterprise segment is growing steadily as major corporations increasingly integrate embedded lending solutions into their customer ecosystems, supplier networks, and digital platforms. Large retailers, marketplaces, healthcare providers, real estate platforms, and enterprise software companies use embedded lending to enhance customer retention, increase transaction volumes, and create additional revenue streams through financing offerings. These organizations also possess stronger IT budgets, advanced analytics capabilities, and established compliance frameworks, enabling faster deployment of sophisticated lending solutions.

Industry Insights

The retail segment dominated the market in 2025. The rising demand for flexible payment options at checkout, including installment financing and Buy Now Pay Later (BNPL) solutions, is driving the adoption of embedded financing among retailers. Retailers are increasingly integrating lending products into e-commerce platforms, mobile apps, and in-store digital channels to improve conversion rates, increase average order vlues, and reduce cart abandonment. Embedded lending also helps merchants attract price-sensitive consumers by making higher-ticket purchases more affordable through manageable repayment plans.

The medical and healthcare segment is projected to grow at the fastest CAGR over the forecast period. The medical and healthcare industry is witnessing growing adoption of embedded lending as patients seek affordable ways to manage rising treatment and healthcare costs. Hospitals, clinics, dental centers, vision providers, and wellness platforms are integrating financing options directly into payment workflows to support elective procedures, diagnostics, surgeries, and recurring care expenses. Embedded lending improves patient access to treatment by reducing upfront payment burdens and enabling installment-based repayment plans.

Regional Insights

The North America embedded lending industry held a significant share in 2025. It represents one of the most mature markets for embedded lending, supported by advanced digital payment infrastructure, strong fintech penetration, and widespread adoption of alternative credit solutions. Businesses across e-commerce, retail, SaaS, and B2B marketplaces are increasingly integrating lending products to improve customer acquisition and transaction volumes.

U.S. Embedded Lending Market Trends

The U.S. embedded lending industry held a dominant position in 2025. The growth in the country is driven by a highly developed fintech ecosystem and strong demand for point-of-sale financing, SME credit, and Buy Now Pay Later solutions. Leading payment companies, lenders, and software platforms are actively embedding lending capabilities into commerce and enterprise ecosystems.

Europe Embedded Lending Industry Trends

The Europe embedded lending industry was identified as a lucrative region in 2025. The growth in the region is supported by open banking regulations, digital banking adoption, and increasing collaboration between fintech firms and traditional financial institutions. Businesses across retail, travel, healthcare, and B2B commerce are leveraging embedded credit to improve customer experience and generate ancillary revenue streams.

The UK embedded lending industry is expected to grow rapidly in the coming years. The growth in the country is attributed to its advanced fintech sector, favorable regulatory environment, and strong consumer adoption of digital finance solutions. E-commerce platforms, challenger banks, and payment providers are increasingly offering embedded credit products to consumers and SMEs.

Asia Pacific Embedded Lending Industry Trends

The Asia Pacific embedded lending industry is expected to grow at the fastest CAGR of 38.4% over the forecast period. The growth in the region is due to rapid digitalization, expanding e-commerce activity, and large underserved consumer and SME populations. Super apps, digital wallets, and marketplace platforms play a critical role in integrating lending services into everyday transactions.

The Japan embedded lending industry is expected to grow rapidly in the coming years. The growth in the region is supported by the country’s strong digital commerce sector, advanced financial infrastructure, and increasing interest in cashless payments. Businesses are integrating financing options into online retail, consumer electronics, and service platforms to enhance purchasing flexibility.

China embedded lending industry is a major market within Asia Pacific, driven by its extensive e-commerce ecosystem, mobile payment leadership, and widespread use of platform-based financial services. Large digital platforms have successfully integrated consumer and merchant credit products into shopping, logistics, and business operations. The country’s robust data ecosystem enables rapid credit assessment and personalized lending on a scale.

Key Embedded Lending Company Insights

Some of the key companies in the embedded lending industry include Stripe, LLC, Plaid Inc., Unit Finance Inc., Adyen, Klarna, and others. Organizations are focusing on increasing the customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Stripe, Inc. is a financial infrastructure and payments technology company. The company provides software tools and APIs that enable businesses to accept payments, manage revenue operations, automate billing, issue cards, prevent fraud, and facilitate cross-border commerce. Stripe serves startups, small and medium-sized enterprises, and large multinational corporations across e-commerce, SaaS, marketplaces, and enterprise sectors. Its broader product ecosystem includes payment processing, subscription billing, embedded finance capabilities, treasury solutions, lending enablement, and business incorporation tools.

-

Plaid Inc. is a financial technology company. The company specializes in data connectivity infrastructure that enables consumers and businesses to securely connect bank accounts with digital applications and financial services platforms. Plaid’s API-driven platform supports account authentication, balance checks, transaction data access, identity verification, income validation, and fraud prevention solutions. Its technology is widely used by fintech firms, digital lenders, neobanks, payment providers, wealth management platforms, and embedded finance companies to streamline onboarding and improve financial decision-making.

Key Embedded Lending Companies:

The following key companies have been profiled for this study on the embedded lending market.

- Stripe, LLC

- Plaid Inc.

- Unit Finance Inc.

- Adyen

- Klarna

- PayPal

- Lendflow

- Pismo

- YouLend Limited

- Liberis

Recent Developments

-

In February 2026, Pulse, an embedded credit and SaaS platform, partnered with Binq, an AI-powered UK SME business marketplace, and Nucleus Commercial Finance to deliver seamless embedded lending directly through Binq's app. Pulse supplies the API-first technology for real-time credit decisioning, data orchestration, and frictionless loan journeys using open banking data. At the same time, Nucleus provides the funding capital, enabling SMEs to get instant eligibility checks, minute-long applications, and diverse options such as cashflow bridging or growth investments without manual processes.

-

In February 2026, Deem Finance, a subsidiary of the UAE's Gargash Group, partnered with AI-powered lending platform Biz2X to deliver data-driven embedded Finance for SMEs, integrating POS-based credit into Binq's business marketplace. Merchants access loans via real-time sales/transaction data rather than traditional balance sheets, with fully digital onboarding, 48-hour approvals, and repayments tied to cash flow, addressing UAE SME funding gaps that conventional models overlook by focusing on static balance sheets.

Embedded Lending Market Report Scope

Report Attribute

Details

Market size in 2025

USD 21.5 billion

Estimated market size in 2026

USD 28.4 billion

Projected market size by 2033

USD 250.9 billion

Growth rate

CAGR of 36.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, deployment, enterprise, industry, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Stripe, LLC; Plaid Inc.; Unit Finance Inc.; Adyen; Klarna; PayPal; Lendflow; Pismo; YouLend Limited; Liberis

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Embedded Lending Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global embedded lending market report based on component, deployment, enterprise, end use, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Platform

-

Services

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud-based

-

On-premise

-

-

Enterprise Outlook (Revenue, USD Billion, 2021 - 2033)

-

Small and Mid-sized Enterprises (SMEs)

-

Large Enterprises

-

-

Industry Outlook (Revenue, USD Billion, 2021 - 2033)

-

Retail

-

Education

-

Medical and Healthcare

-

IT / IT Services

-

Real Estate

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global embedded lending market size was valued at USD 21.5 billion in 2025 and is estimated at USD 28.4 billion for 2026.

The global embedded lending market is expected to grow at a CAGR of 36.5% from 2026 to 2033, reaching USD 250.9 billion by 2033.

The platform segment accounted for the largest share of 65.3% in 2025. The increasing adoption of API-based lending infrastructure, cloud-native loan management systems, and white-label financing solutions by digital platforms and enterprises is driving the growth of the platform segment.

Rising demand for seamless access to credit at the point of need across digital platforms is driving the growth of the embedded lending market.

North America dominated with a 38.6% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The cloud-based segment held the largest revenue share in 2025.

The small and mid-sized enterprises (SMEs) segment held the largest revenue share in 2025.

Retail segment held the largest share in 2025, while medical and healthcare is the fastest-growing industry.

Key players include Stripe, LLC; Plaid Inc.; Unit Finance Inc.; Adyen; Klarna; PayPal; Lendflow; Pismo; YouLend Limited; Liberis.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.