- Home

- »

- Next Generation Technologies

- »

-

Engineering Services Outsourcing Market Size Report, 2033GVR Report cover

![Engineering Services Outsourcing Market (2026 - 2033)Report]()

Engineering Services Outsourcing Market (2026 - 2033)

Size, Share & Trends Analysis Report By Services (Designing, Prototyping, System Integration, Testing), By Location (On-shore, Off-shore), By Application (Aerospace, Automotive), By Region, And Segment Forecasts

Market Size, 2025

$3.2BMarket Estimate, 2026

$4.1BMarket Forecast, 2033

$15.2BCAGR, 2026–2033

20.4%Engineering Services Outsourcing Market Summary

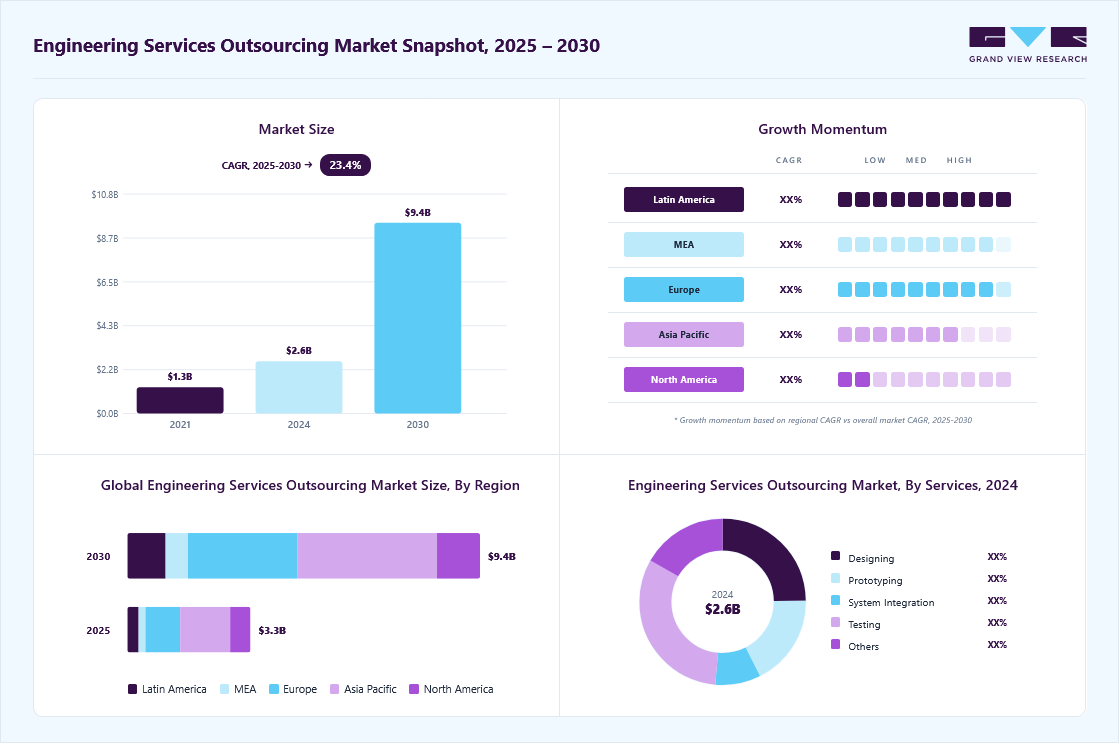

The global engineering services outsourcing market size was valued at USD 3.2 billion in 2025 and is projected to grow from USD 4.1 billion in 2026 to USD 15.2 billion by 2033, growing at a CAGR of 20.4% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 40.5% in 2025. The growth of the market can be attributed to several factors, including the increasing complexity of engineering projects that necessitate specialized expertise and advanced technological capabilities.

Key Market Trends & Insights

- By service: Testing segment accounted for the largest market share of over 32.2% in 2025.

- By location: On-shore segment accounted for the largest market share of 64.18% in 2025.

- By Application: Healthcare segment is expected to register the fastest CAGR from 2025 to 2033.

Regional Highlights

- Largest regional market: Asia Pacific (40.5% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 3.2 Billion

- Estimated market size in 2026: USD 4.1 Billion

- Projected market size by 2033: USD 15.2 Billion

- CAGR (2026-2033): 20.4%

Additionally, the demand for cost reduction and operational efficiency drives businesses to seek external partners who can provide high-quality engineering services at competitive prices is driving the engineering services outsourcing industry growth. Cost reduction and efficiency gains are significant drivers fueling the growth of the Engineering Services Outsourcing (ESO) market. One of the primary reasons for this growth is the ability of ESO to reduce operational costs. By outsourcing engineering services, companies can leverage labor cost arbitrage, particularly by partnering with providers in regions such as India, the Philippines, or Eastern Europe, where engineering talent is available at lower costs. Additionally, ESO eliminates the need for companies to invest in costly infrastructure such as advanced software, tools, and research facilities. This reduction in overhead allows organizations to reallocate budgets to other strategic areas, thereby propelling engineering services outsourcing industry expansion.")

Additionally, the growing adoption of Artificial Intelligence (AI), the Internet of Things (IoT), and Digital Twins. These technologies have transformed traditional engineering processes, enabling more accurate simulations, predictive maintenance, and real-time monitoring. ESO providers are often at the forefront of these innovations, investing heavily in advanced software and tools. For instance, Digital Twin technology allows companies to create virtual replicas of physical systems, enabling them to optimize performance and identify potential issues before deployment. By outsourcing these capabilities, businesses gain access to state-of-the-art tools without incurring the high costs of in-house development.

The adoption of Industry 4.0 technologies is significantly driving the growth of the Engineering Services Outsourcing (ESO) market. Industry 4.0, often referred to as the Fourth Industrial Revolution, incorporates advanced technologies such as automation, artificial intelligence (AI), the Internet of Things (IoT), digital twins, and big data analytics into industrial processes. This shift is transforming the engineering landscape, creating a surge in demand for specialized expertise that ESO providers are uniquely positioned to deliver, thereby driving engineering services outsourcing industry growth.

Automation and robotics are central to Industry 4.0, enabling businesses to increase productivity and reduce costs. The design, development, and deployment of robotic systems require specialized engineering services, from mechanical design to software programming and integration. ESO providers have the necessary expertise to deliver end-to-end solutions for automation projects, allowing companies to implement robotic systems more quickly and efficiently. This growing demand for robotics-related engineering services is further fueling the expansion of the engineering services outsourcing industry.

Market Dynamics

Engineering services outsourcing is gaining significant traction as organizations seek specialized engineering expertise, cost optimization, and faster product development cycles in an increasingly competitive business environment. Engineering services outsourcing providers offer capabilities such as product design, mechanical engineering, electronics engineering, embedded software development, industrial automation, simulation & testing, digital engineering, and research & development support. These services enable enterprises across automotive, aerospace, industrial manufacturing, energy, healthcare, telecommunications, and construction sectors to accelerate innovation, improve operational efficiency, and reduce time-to-market while focusing on their core business activities.

The Engineering Services Outsourcing Market is experiencing substantial growth due to the increasing demand for cost-effective engineering solutions and access to highly skilled technical talent. Companies across industries are facing growing pressure to reduce operational expenses while accelerating product innovation and development timelines. Outsourcing engineering functions allows organizations to leverage global talent pools, optimize resource allocation, and gain access to specialized expertise in areas such as product design, software engineering, digital twins, simulation, artificial intelligence, and advanced manufacturing technologies.

In addition, the rising complexity of modern products and systems is driving organizations to collaborate with engineering service providers that possess domain-specific knowledge and advanced technological capabilities. The growing adoption of Industry 4.0, Internet of Things (IoT), cloud computing, automation, and connected technologies is further increasing demand for outsourced engineering services. As businesses continue to focus on digital transformation and innovation-led growth strategies, engineering services outsourcing is becoming a critical tool for improving competitiveness, accelerating product development, and enhancing operational efficiency.

Despite strong growth prospects, the Engineering Services Outsourcing Market faces challenges related to data security, intellectual property (IP) protection, and project management complexities. Engineering projects often involve sensitive product designs, proprietary technologies, confidential technical specifications, and critical business information. Organizations may hesitate to outsource core engineering functions due to concerns regarding data breaches, unauthorized access, and potential loss of intellectual property.

Furthermore, managing geographically distributed engineering teams can create challenges related to communication, coordination, quality control, and compliance with industry standards and regulatory requirements. Differences in technical practices, project methodologies, and cultural or language barriers may impact project execution and delivery timelines. The shortage of highly specialized engineering professionals in certain domains, combined with increasing competition for talent, can also affect service quality and project scalability. These factors may limit outsourcing adoption among organizations operating in highly regulated or technology-intensive industries.

The rapid adoption of digital engineering technologies is creating significant growth opportunities for the engineering services outsourcing market. Enterprises are increasingly investing in digital product development, smart manufacturing, digital twins, model-based systems engineering, predictive maintenance, industrial automation, and connected product ecosystems. Engineering service providers are expanding their capabilities to support these advanced technologies, enabling organizations to accelerate innovation while reducing development costs and operational risks.

Furthermore, growing demand for electric vehicles, autonomous systems, renewable energy infrastructure, smart cities, medical devices, and advanced telecommunications networks is creating new outsourcing opportunities across multiple industry verticals. The integration of artificial intelligence, machine learning, cloud-based engineering platforms, and simulation-driven design processes is further enhancing the value proposition of outsourced engineering services. As organizations continue to embrace digital transformation and next-generation product innovation, engineering services outsourcing is expected to play a pivotal role in supporting technological advancement and business growth.

Market Concentration & Characteristics

The Engineering Services Outsourcing (ESO) Market is highly fragmented, characterized by the presence of numerous global engineering service providers, IT services companies, niche engineering specialists, design consultancies, and regional outsourcing firms competing across various industry verticals. The market includes large multinational players such as Accenture, Capgemini, Tata Consultancy Services, Infosys, HCLTech, Wipro, and LTTS, alongside hundreds of mid-sized and specialized engineering firms.

The high degree of fragmentation is driven by the broad scope of engineering services, diverse end-use industries, varying technical specializations, and the availability of engineering talent across multiple geographies. Companies compete based on domain expertise, digital engineering capabilities, Industry 4.0 solutions, pricing, global delivery models, and long-term client relationships.

Analyst Perspective

The engineering services outsourcing market sits at the intersection of accelerating digital transformation, increasing product complexity, and growing pressure on enterprises to optimize costs while accelerating innovation. Demand is being driven by the rapid adoption of Industry 4.0 technologies, connected products, electric vehicles, embedded software, artificial intelligence, cloud engineering, and smart manufacturing initiatives across industries. As organizations seek to shorten product development cycles and gain access to specialized engineering expertise, outsourcing engineering functions has evolved from a cost-saving strategy into a critical enabler of innovation and competitive differentiation.

Service Insights

The testing segment accounted for the largest market share of over 31% in 2024. This dominance is driven by the increasing complexity of automotive systems and components, particularly with the rise of electric vehicles (EVs) and autonomous driving technologies. As Original Equipment Manufacturers (OEMs) seek to ensure safety and compliance with stringent regulations, there is a growing demand for comprehensive testing services. This includes simulation, validation, and verification processes that can efficiently handle advanced technologies. The need for rapid prototyping and the ability to bring products to market faster also contribute to the segment's dominance, as companies look to outsource these specialized tasks to reduce costs and enhance operational efficiency.

The designing segment is expected to witness the fastest CAGR of over 22.6% from 2026 to 2033.. This rapid growth can be attributed to the rapid evolution of automotive technologies and consumer preferences. As automakers increasingly focus on innovation, they require advanced design capabilities that incorporate the latest trends in connectivity, sustainability, and user experience. The shift towards modular vehicle architectures and platform sharing allows for more flexible design processes, enabling quicker adaptations to market demands. Additionally, the integration of artificial intelligence (AI) and machine learning in design processes enhances creativity and efficiency, driving further growth in this segment.

Location Insights

Based on application, the Onshore segment led the market with the largest revenue share of 64.1% in 2025. The on-shore segment benefits from the increasing emphasis on quality control, intellectual property protection, and regulatory compliance. Companies are recognizing the advantages of keeping engineering services closer to their operational bases to facilitate better communication and collaboration among teams. This trend is particularly relevant in regions with high labor costs where businesses are willing to invest in local expertise to ensure high-quality outcomes. Additionally, the rising consumer demand for locally produced goods fosters a preference for on-shore outsourcing as companies seek to enhance their brand image and meet sustainability goals.

The off-shore segment is expected to witness the fastest CAGR from 2026 to 2033, as manufacturers continue to leverage cost advantages associated with outsourcing engineering services to countries with lower labor costs. This strategy allows OEMs to focus on core competencies while accessing specialized skills and technologies that may not be available domestically. The growing trend of digital transformation within the automotive industry also supports off-shoring efforts, as companies can utilize advanced digital tools and platforms for seamless collaboration across borders. Furthermore, the increasing complexity of automotive systems necessitates a diverse skill set that off-shore providers can offer at competitive prices.

Application Insights

Based on application, the Automotive segment led the market with the largest revenue share of 19.4% in 2025, driven by the ongoing push for efficiency and scalability in production processes. As automakers strive to reduce production costs while maintaining high-quality standards, there is a growing reliance on outsourced manufacturing services that can provide specialized expertise and advanced technologies. Additionally, the shift towards electrification and sustainable manufacturing practices is prompting manufacturers to seek partners who can support these initiatives through innovative solutions. The need for rapid adaptation to changing market conditions further fuels demand for flexible manufacturing options.

The healthcare segment is expected to register the fastest CAGR from 2026 to 2033, owing to the increasing integration of advanced technologies such as IoT, AI, and big data analytics in medical devices and healthcare systems. As healthcare providers look to enhance patient outcomes through personalized medicine and improved diagnostics, there is a rising demand for engineering services that can support the development of sophisticated medical devices. Additionally, regulatory pressures and the need for compliance with stringent safety standards drive healthcare organizations to outsource specialized engineering services that ensure quality and reliability in their products.

Regional Insights

Asia Pacific dominated the engineering services outsourcing market with the largest revenue share of 40.5% in 2025, fueled by its rapid economic growth, an abundance of highly skilled labor, and a favorable business environment for global companies. With lower labor costs and a growing pool of qualified engineers, countries such as India and China have become attractive destinations for outsourcing engineering tasks. Furthermore, the increasing demand for digital and technological innovation in industries such as manufacturing, automotive, and IT drives the need for more outsourced engineering expertise in this region.

China Engineering Services Outsourcing Market Trends

The engineering services outsourcing market in the China held the largest share in the Asia Pacific region in 2025. Engineering services outsourcing market in China is witnessing rapid growth driven by the country's massive investments in renewable energy infrastructure and technology. As one of the largest consumers of energy globally, China is focusing on optimizing its energy consumption through advanced engineering services. The government's initiatives to reduce reliance on coal and increase the share of renewables are creating significant opportunities for ESO providers. The market is anticipated to grow as China continues to implement smart grid technologies and enhance its overall energy efficiency.

Japan's engineering services outsourcing market is gaining traction owing to the increasing demand for high-quality engineering services, particularly in the automotive and healthcare sectors. Companies are increasingly outsourcing specialized engineering tasks to leverage global expertise while managing costs effectively.

North America Engineering Services Outsourcing Market Trends

North America engineering services outsourcing industry is expected to grow at the fastest CAGR of over 16% from 2025 to 2030, primarily driven by the need for cost reduction, access to specialized skills, and the pressure to innovate quickly. Companies in the region are increasingly outsourcing engineering functions to improve efficiency, reduce overhead costs, and focus on their core competencies. The availability of a skilled workforce in emerging economies and the rise of digital transformation are also significant factors contributing to this trend.

The U.S. engineering services outsourcing industry is expected to grow at a CAGR of over 15% from 2025 to 2030, driven by the early adoption of energy optimization services and a trend towards outsourcing non-core energy management operations. The market is projected to grow significantly, with investments in upgrading aging power infrastructure and advancements in smart grid technologies enhancing demand for energy optimization solutions.

Europe Engineering Services Outsourcing Market Trends

Europe engineering services outsourcing industry is expected to grow at a CAGR of over 25% from 2025 to 2030. In Europe, the market largely driven by the region’s need to maintain competitiveness in the global market. Outsourcing helps European firms access advanced technologies, lower labor costs, and tap into specialized expertise that may not be readily available in-house. Additionally, economic pressures and regulatory complexities in various European countries encourage businesses to seek external partners for engineering support to streamline operations and remain flexible.

The UK engineering services outsourcing market is expected to grow at a significant rate in the coming years. This expansion is characterized by a strong push towards sustainability and renewable energy integration. Government policies aimed at reducing carbon footprints and promoting green technologies are driving investments in energy optimization services. The increasing demand for digitization in energy management systems is also fostering growth in this sector.

The engineering services outsourcing market in Germany is characterized by its leadership in renewable energy adoption and stringent environmental regulations. The country has made significant investments in wind and solar power, which necessitate advanced energy management solutions to optimize performance and reliability. As a result, there is a growing demand for ESO services that can integrate these renewable sources into existing grids while ensuring efficiency and sustainability.

Key Engineering Services Outsourcing Company Insights

Some of the key players operating in the market are Tata Consultancy Services (TCS) and ALTEN Group.

-

ALTEN Group is a global technology consulting and engineering services company that specializes in providing innovative solutions across various industries, including aeronautics, automotive, telecommunications, and life sciences. The company focuses on delivering comprehensive services that encompass the entire product development cycle, from design and engineering to IT solutions. The company's commitment to innovation and sustainable practices makes it a trusted partner for organizations looking to enhance their operational efficiency and competitiveness in a rapidly evolving market.

-

Tata Consultancy Services (TCS) is a global IT services, consulting, and business solutions organization providing a comprehensive range of services, including application development, business process outsourcing, and digital transformation solutions. With a strong focus on innovation and sustainability, TCS leverages advanced technologies to help clients across various sectors enhance their operational efficiency and drive growth. The company operates in numerous countries worldwide, serving some of the largest enterprises and contributing significantly to the global IT landscape.

HCL Technologies Limited and Emerson Electric Co some of the emerging participants in the engineering services outsourcing market.

-

HCL Technologies Limited is a global IT services and consulting company that specializes in a wide range of services, including IT and business services, engineering and R&D services, and products and platforms, catering to diverse industries such as finance, healthcare, and telecommunications. The company has established a strong presence in over 60 countries, focusing on innovation and client-centric solutions to drive digital transformation and operational efficiency for its clients. The company is known for its commitment to research and development, evidenced by its extensive portfolio of patents and numerous innovation labs worldwide.

-

Emerson Electric Co. is a global technology and engineering company that was established as a manufacturer of electric motors and fans. The company delivers automation solutions, providing innovative products and services across various sectors, including industrial, commercial, and residential markets. The company specializes in measurement and analytical instrumentation, process control systems, and fluid control technologies, among others.

Key Engineering Services Outsourcing Companies

The following key companies have been profiled for this study on the engineering services outsourcing market.

-

AKKA Technologies (Akkodis)

-

Alten Group

-

Capgemini Engineering

-

Entelect

-

HCL Technologies Limited

-

Emerson Electric Co

-

Infosys Limited

-

Tata Elxsi

-

Tata Consultancy Services Limited

-

Tech Mahindra Limited

-

Wipro Limited

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (AKKA Technologies (Akkodis), Alten Group, Capgemini Engineering, HCL Technologies Limited, Infosys Limited, Tata Consultancy Services Limited, Tech Mahindra Limited, Wipro Limited)

- Expand engineering service portfolios through acquisitions, strategic partnerships, and global delivery centers.

- Strengthen long-term engagements with automotive, aerospace, industrial manufacturing, healthcare, telecommunications, and energy companies while expanding offshore and nearshore engineering capabilities.

- Strong global delivery networks, extensive engineering talent pools, diversified industry expertise, established client relationships, and significant investments in digital engineering and R&D.

- Ability to provide end-to-end product lifecycle services, scale large projects, and support multinational customers across multiple geographies.

- High dependency on skilled engineering talent, rising wage inflation, and intense competition from regional and niche engineering service providers.

- Challenges related to talent retention and maintaining service quality while scaling operations globally.

Emerging Players (Tata Elxsi Limited, Entelect (Pty) Ltd., Emerson Electric Co.)

- Focus on specialized engineering domains such as embedded systems, automotive software, digital product engineering, industrial automation, IoT solutions, and industry-specific design services.

- Invest in emerging technologies including AI, digital twins, EV engineering, and smart manufacturing solutions to differentiate service offerings.

- Strong niche expertise, greater operational flexibility, and faster decision-making compared to large multinational competitors.

- Ability to deliver highly customized engineering solutions, respond quickly to evolving customer requirements, and capitalize on emerging technology trends in specific industry verticals.

- Challenges in expanding international customer bases, competing for large multi-year contracts, attracting specialized engineering talent, and sustaining investments in advanced digital engineering capabilities and global delivery infrastructure.

Recent Developments

-

In December 2024, ALTEN Group announced the completion of its acquisition of the Worldgrid business unit from Atos SE. Worldgrid specializes in providing consulting and engineering services to energy and utility companies, primarily operating in France, Germany, and Spain.

-

In December 2024, HCLTechnologies announced the acquisition of assets from HPE's Communications Technology Group. This acquisition will expand HCL's portfolio of service offerings, including Business Support Systems (BSS) and network applications while integrating advanced technologies like AI and IoT into its services.

-

In March 2024, Tata Consultancy Services (TCS) announced a multimillion-dollar strategic partnership with Ramboll, a global architecture and engineering consultancy based in Denmark, to transform its IT infrastructure over the next seven years. This collaboration aims to modernize Ramboll's IT operating model, enhancing business growth while optimizing costs and reducing its carbon footprint.

Engineering Services Outsourcing Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 3.2 billion

Estimated market size in 2026

USD 4.1 billion

Projected market size by 2033

USD 15.2 billion

Growth rate

CAGR of 20.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Application, service, location, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; U.K; France; China; Japan; India; South Korea; Australia; Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

AKKA Technologies (Akkodis); Alten Group; Capgemini Engineering; Entelect (Pty) Ltd.; HCL Technologies Limited; Emerson Electric Co.; Infosys Limited; Tata Elxsi Limited; Tata Consultancy Services Limited; Tech Mahindra Limited; Wipro Limited.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Engineering Services Outsourcing Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest technology trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the engineering services outsourcing market report based on service, location, application, and region:

-

Services Outlook (Revenue, USD Million, 2021 - 2033)

-

Designing

-

Prototyping

-

System Integration

-

Testing

-

Others

-

-

Location Outlook (Revenue, USD Million, 2021 - 2033)

-

On-shore

-

Off-shore

-

Near-shore

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Aerospace

-

Automotive

-

Industrial

-

Consumer Electronics

-

Semiconductors

-

Healthcare

-

Telecom

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Mexico

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

Research Methodology

Segment Definition

Segment - Application

Revenue capture definition

Aerospace

Revenue is generated through the provision of outsourced engineering services across aircraft design, structural engineering, avionics development, propulsion systems, simulation & testing, maintenance engineering, digital engineering, and product lifecycle management.

Automotive

Revenue is generated through the provision of outsourced engineering services across vehicle design and development, powertrain engineering, embedded software, electrical and electronic systems, autonomous driving technologies, connected vehicle solutions, and vehicle testing & validation.

Industrial

Revenue is primarily generated through engineering design, product development, industrial automation, plant engineering, manufacturing process optimization, and digital transformation services provided to industrial enterprises.

Consumer Electronics

Revenue is derived from outsourced engineering services supporting the design, development, testing, and optimization of consumer electronic products. Additional revenue is generated through embedded software development, hardware engineering, product prototyping, connectivity solutions, user interface design, and other connected consumer technologies.

Semiconductors

Revenue is generated through outsourced engineering services related to semiconductor design, chip development, verification and validation, ASIC/SoC engineering, physical design, embedded software development, and testing services.

Healthcare

Revenue is generated through outsourced engineering services supporting the design, development, testing, and optimization of medical devices, diagnostic equipment, digital health platforms, and healthcare technologies. Additional revenue streams include software and embedded systems engineering, regulatory compliance and certification support.

Telecom

Revenue is generated through outsourced engineering services for telecommunications network design, development, deployment, and optimization. Additional revenue comes from 5G engineering, network testing, OSS/BSS integration, embedded software development, and technology support services for telecom operators and network equipment providers.

Others

Revenue is generated through outsourced engineering services across sectors such as energy & utilities, construction, logistics, agriculture, and smart infrastructure. Additional revenue comes from product design, automation, digital engineering, testing, and specialized R&D support tailored to industry-specific requirements.

Segment - Service

Revenue capture definition

Designing

Engineering design services generate revenue through the development of product concepts, detailed engineering designs, CAD modeling, simulation, prototyping, and design optimization solutions delivered to clients across various industries. Additional revenue opportunities arise from design validation, product customization, digital engineering services, product lifecycle management support, and long-term design and development contracts aimed at accelerating innovation and reducing time-to-market.

Prototyping

Prototyping services generate revenue through the development of physical and digital prototypes used for product validation, performance testing, and design refinement. Additional revenue opportunities arise from rapid prototyping, 3D printing, proof-of-concept development, testing and validation services, and iterative engineering support that helps clients accelerate product development and reduce commercialization risks.

System Integration

System integration services generate revenue through the integration of hardware, software, communication networks, and engineering systems to ensure seamless functionality and interoperability. Additional revenue opportunities arise from implementation, customization, testing, deployment, maintenance, and technical support services that help organizations optimize operational performance and accelerate digital transformation initiatives.

Testing

Testing services generate revenue through the validation, verification, and performance assessment of products, systems, and engineering solutions to ensure quality, reliability, and regulatory compliance. Additional revenue opportunities arise from functional testing, simulation, certification support, quality assurance, and ongoing testing services throughout the product development lifecycle.

Others

Other engineering services generate revenue through specialized consulting, maintenance engineering, technical documentation, product lifecycle management, regulatory compliance support, and engineering project management activities

Segment - Location

Revenue capture definition

Onshore

Onshore engineering services generate revenue through the delivery of engineering, design, development, and consulting services within the client’s domestic market. Additional revenue opportunities arise from close collaboration, regulatory compliance support, project management, and specialized technical services that require proximity to client operations and faster project execution.

Offshore

Offshore engineering services generate revenue through the delivery of engineering, design, development, testing, and technical support services from lower-cost international locations. Additional revenue opportunities arise from dedicated engineering teams, long-term outsourcing contracts, digital engineering projects, and cost-optimization initiatives that enable clients to access specialized talent and scalable resources.

Estimation Model

Engineering Demand Layer

Outsourcing Readiness Layer

Adoption Layer

Monetization Layer

Who needs engineering services?

Who can outsource engineering functions?

Who actively uses outsourced engineering services?

How much revenue is generated?

Identify industries with high engineering intensity such as automotive, aerospace, industrial manufacturing, semiconductors, healthcare, telecommunications, and consumer electronics to define the potential engineering services demand base.

Apply outsourcing penetration rates across engineering activities including product design, embedded software, prototyping, testing, system integration, and product lifecycle management to determine the addressable outsourcing market.

Apply enterprise outsourcing adoption rates, digital transformation initiatives, and engineering resource gaps to estimate the number of organizations actively engaging third-party engineering service providers across industries.

Multiply active outsourcing engagements by average engineering project values, service contract spending, engineering headcount utilization, and onsite/offshore delivery mix to estimate total Engineering Services Outsourcing market revenue.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Engineering Outsourcing Landscape & Competitive Benchmarking

Conducted a comprehensive analysis of global engineering service providers, outsourcing models, service portfolios, delivery capabilities, and competitive positioning across automotive, aerospace, industrial, healthcare, telecom, semiconductor, and consumer electronics industries.

Helps stakeholders identify leading service providers, evaluate competitive differentiation, and assess partnership, acquisition, and market expansion opportunities within the ESO ecosystem.

Enterprise Adoption & Industry Demand Analysis

Evaluated outsourcing adoption trends across key industries, including product design, embedded software development, prototyping, testing, system integration, and digital engineering services. Assessed engineering spending patterns, outsourcing intensity, and technology-driven demand drivers.

Provides insights into high-growth end-use industries, engineering demand trends, and outsourcing opportunities to support strategic planning, client acquisition, and business expansion initiatives.

Digital Engineering & Growth Opportunity Assessment

Assessed the impact of Industry 4.0, digital twins, artificial intelligence, IoT, cloud engineering, EV development, and smart manufacturing initiatives on engineering outsourcing demand.

Supports investment and growth strategies by identifying emerging technology opportunities, evaluating market attractiveness, and understanding the key factors influencing long-term development of the Engineering Services Outsourcing market.

Frequently Asked Questions About This Report

The global engineering services outsourcing market size was valued at USD 3.2 billion in 2025 and is expected to reach USD 4.1 billion by 2026.

Key factors that are the rising demand for incorporating the most delinquent technologies in the product offerings, and the increasing need to trim the product lifecycles and trim costs are also anticipated to contribute to the ESO market's growth. The growing alliance among Engineering Service Providers (ESP) and Original Equipment Manufacturers (OEM) is predicted to appear to be one of the direct factors propelled by the increase in the acceptance of engineering services outsourcing (ESO).

Some key players operating in the engineering services outsourcing market include Tata Consultancy Services Limited, Tata Elxsi, ALTEN Group, AKKA and Capgemini Engineering.

The global engineering services outsourcing market is expected to grow at a compound annual growth rate of 20.4% from 2026 to 2033 to reach USD 15.2 billion by 2033

The testing segment dominated the market in 2025 of over 32.2%, driven by the increasing complexity of automotive systems and components, particularly with the rise of electric vehicles (EVs) and autonomous driving technologies.

Latin America is projected to be the fastest-growing region in the Engineering Services Outsourcing Market, registering a CAGR of 24.3% during the forecast period. This growth is driven by increasing investments in digital transformation, expanding manufacturing and automotive sectors, rising adoption of Industry 4.0 technologies, and growing demand for cost-effective engineering expertise.

Automotive led the Engineering Services Outsourcing Market with a 19.4% market share in 2025, driven by increasing investments in electric vehicles (EVs), autonomous driving technologies, connected vehicle platforms, and software-defined vehicles.

Designing led the service segment with a 25.1% market share in 2025, driven by increasing demand for outsourced product design, CAD modeling, engineering simulation, and digital design services across automotive, aerospace, industrial, semiconductor, and healthcare industries.

Onshore services led the location segment with a 64.1% market share in 2025, driven by the need for close client collaboration, regulatory compliance, faster project execution, and access to domain-specific engineering expertise across various region.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.