- Home

- »

- Next Generation Technologies

- »

-

Digital Twin Market Size And Share, Industry Report, 2033GVR Report cover

![Digital Twin Market Size, Share, & Trend Report]()

Digital Twin Market (2026 - 2033) Size, Share, & Trend Analysis Report By Solution (Component, Process, System), By Deployment, By Enterprise Size, By Application, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$35.8BMarket Estimate, 2026

$49.5BMarket Forecast, 2033

$328.5BCAGR, 2026–2033

31.1%Digital Twin Market Summary

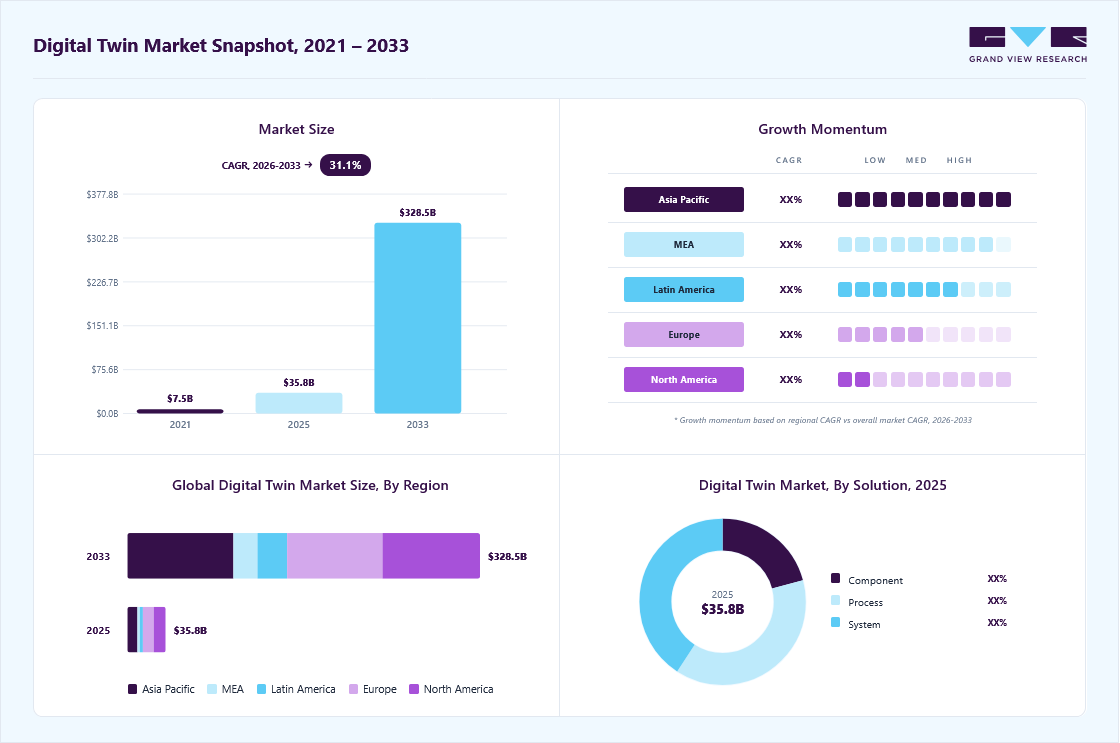

The global digital twin market size was valued at USD 35.8 billion in 2025 and is projected to grow from USD 49.5 billion in 2026 to USD 328.5 billion by 2033, at a CAGR of 31.1% from 2026 to 2033. The North America digital twin market held the largest share of 31.3% of the global market in 2025. Due to the rapid adoption of Industry 4.0 practices, rising demand for predictive maintenance across industries, and the growing need for real-time monitoring of assets to reduce operational costs and downtime. Expanding applications in sectors such as aerospace, automotive, energy, healthcare, and smart cities are fuelling adoption, supported by advancements in IoT, AI, cloud computing, and 5G connectivity that enable seamless data integration between physical and digital systems.

Key Market Trends & Insights

- By solution: System led the market and held the largest revenue share of 40.9% in 2025.

- By deployment: On-premise segment accounted for the largest revenue share in 2025.

- By end use: Telecommunication segment is expected to grow at the fastest CAGR from 2026 to 2033.

Regional Highlights

- Largest regional market: North America (31.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The digital twin industry in the U.S. is expected to grow significantly over the forecast period.

Market Size & Forecast

- Market size in 2025: USD 35.8 Billion

- Estimated market size in 2026: USD 49.5 Billion

- Projected market size by 2033: USD 328.5 Billion

- CAGR (2026-2033): 31.1%

Additionally, increasing investments in sustainability, regulatory compliance, and resource optimization are prompting enterprises and governments worldwide to adopt digital twins as a core tool for enhancing efficiency, driving innovation, and achieving competitive differentiation.The increasing adoption of digital twin technology to optimize operational efficiency, enable predictive maintenance, and enhance real-time decision-making is creating a positive outlook for the digital twin market. Organizations across various industries, including manufacturing, aerospace & defense, automotive, healthcare, energy & utilities, and construction, are leveraging digital twins to simulate, monitor, and analyze the performance of physical assets and processes. They are also partnering with technology providers to integrate IoT, artificial intelligence (AI), and advanced analytics capabilities into their digital twin ecosystems, thereby improving asset reliability, reducing downtime, and accelerating innovation.

")

For instance, in May 2025, Endava partnered with AlixPartners to deliver comprehensive, end-to-end, technology-driven solutions to clients worldwide. This collaboration brings together complementary capabilities, combining AlixPartners’ deep expertise in industry-focused operational consulting with Endava’s advanced technical strengths in areas such as AI, cloud adoption, and data analytics. By uniting these skill sets, the partnership is designed to accelerate digital transformation, foster innovation, and tackle complex business challenges. The joint approach enables organizations to move with greater speed, minimize risk, and resolve issues more effectively while maintaining focus on their broader strategic objectives.

Cloud computing and edge computing are transforming the digital twin market by making it easier to deploy scalable and cost-effective solutions. The cloud provides the infrastructure for storing and analyzing vast data sets, while edge computing ensures faster data processing closer to the source. Together, they enable seamless integration of digital twins across large enterprises, supporting remote monitoring and real-time collaboration. This trend is especially valuable in industrial settings, where immediate responses to machine conditions can prevent costly breakdowns and ensure safety compliance. Furthermore, the emergence of 5G technology is acting as a catalyst for digital twin adoption. With its high-speed, low-latency connectivity, 5G facilitates the smooth transmission of data from numerous IoT devices to digital twin platforms.

Market Dynamics

The Internet of Things (IoT) is transforming businesses globally. It also creates opportunities for the digital twin market to meet consumers’ evolving demands for innovative ways of delivering adjacent services to end users. Digital twin platform developers leverage IoT to improve operations, enhance system productivity, and augment sales. The proliferation of IoT devices opens new avenues for growth for digital twin platform developers. As such, the developers of the digital twin platform are developing IoT-enabled digital twin solutions to strengthen their market position. ABB, General Electric, Siemens AG, AVEVA Group plc, Dassault Systèmes, and Hexagon AB, among others, are among the players that have added IoT-enabled digital twin solutions to their digital twin portfolios. Implementing IoT in manufacturing enables electronic devices to communicate with each other without human intervention through existing internet infrastructure. It could have a profound impact on the digital twin industry. IoT allows connected devices to interact with each other and exchange critical notifications, such as defective or damaged ping. As such, an IoT-connected device notifies the user or another device upon detecting a failure, thereby improving the quality of the end product, reducing waste, and curtailing overall downtime and related costs.

The emergence of connected and cloud computing environments creates new threats to public safety, privacy, and economic stability, particularly in the wake of the growing instances of sophisticated cyber-attacks. Organizations find it particularly challenging to draft a cybersecurity strategy strong enough to safeguard confidential data due to a looming lack of skilled cybersecurity professionals. Organizations recognize the need for more skilled cybersecurity professionals across departments. A digital twin is a replica of physical assets. Key players collaborate with cloud service providers to provide cloud-based digital twin solutions. For instance, General Electric partnered with Microsoft Azure, and Siemens partnered with Amazon AWS to offer cloud-based digital twin solutions and make a foray into the IIoT market.

AI and ML are gaining popularity across various industries, including automotive, healthcare, defense & aerospace, and manufacturing. To offer enhanced products to customers, incumbents of these industries are integrating AI and ML into their existing products. The growing implementation of AI in self-driving cars and Electric Vehicles (EVs) is highly evident in the automotive industry. The growing demand to prevent product recalls, and the need to reduce carbon emissions and enhance engine efficiency, have led to significant adoption of digital twin solutions in the automotive, defense & aerospace industries. AI and generative design, along with cloud-based computing, help digital twin developers generate numerous design options and improve the design process.

General Electric uses a digital twin framework called the Air Force Research Laboratory (AFRL) Digital Twin Spiral 1 IDIQ, an aircraft-tracking model. The company has developed the digital twin to track, monitor, and maintain an aircraft engine blade, realizing that aircraft blades can witness spallation, wherein materials in the blade begin to erode. Such erosion is particularly evident in Middle Eastern countries with sandy conditions. According to a General Electric aviation customer, digital twins in the aviation industry can enable early degradation prediction, thereby triggering maintenance before a problem occurs.

Market Concentration & Characteristics

The digital twin market is highly concentrated, with a mix of established enterprise technology providers, industrial software companies, and specialized simulation platform developers shaping the competitive landscape. Major players such as Microsoft, Siemens, IBM, and Dassault Systèmes hold significant market share due to their strong software ecosystems, advanced analytics capabilities, and long-standing client relationships across the industrial, manufacturing, healthcare, aerospace, and infrastructure sectors. In terms of market characteristics, the industry is highly technology-driven and innovation-intensive, with a strong emphasis on real-time data synchronization, predictive analytics, machine learning, edge computing, and interoperability across connected systems.

Additionally, the market is characterized by long implementation cycles, high initial investment requirements, and significant customization needs depending on industry-specific applications and operational complexity. From a competitive standpoint, the digital twin market demonstrates strong customer retention due to high integration dependency, long-term software contracts, and the strategic role these platforms play in core operational processes.

Solution Insights

The system segment dominated the market and accounted for the revenue share of 40.9% in 2025, driven by the rising enterprise demand for real-time process optimization, operational resilience, and system-wide visibility across manufacturing, logistics, and utility sectors. Digital twins at the process level are increasingly being adopted to simulate entire workflows, improve predictive planning, and support autonomous decision-making, especially in high-variability environments. The growing integration of AI and IoT into digital twin platforms enables the dynamic modeling of production lines, supply chains, and energy management systems, helping to reduce downtime, enhance throughput, and streamline compliance.

The process segment is anticipated to grow at the highest CAGR during the forecast period, driven by the increasing deployment of integrated digital twin environments that simulate the behavior and performance of complex systems across industries. System-level digital twins combine components and processes into unified, large-scale models that support cross-functional optimization, real-time monitoring, and improved decision-making across operations, infrastructure, and enterprise ecosystems.

Deployment Insights

The on-premise segment dominated the market and accounted for the largest revenue share in 2025 due to heightened data security and compliance requirements across industries such as manufacturing, energy, and healthcare. Organizations dealing with sensitive operational or proprietary data prefer on-premise solutions to maintain full control over their digital twin environments, ensuring minimal risk of data breaches and adherence to regulatory standards. Additionally, industries with legacy infrastructure or low-latency operational needs benefit from on-premise deployments, as they allow seamless integration with existing systems and real-time data processing without reliance on cloud connectivity.

The cloud segment is anticipated to grow at the highest CAGR during the forecast period due to its scalability, cost efficiency, and flexibility, enabling organizations to deploy, manage, and update digital twin models without incurring heavy upfront infrastructure investments. Cloud-based digital twins enable real-time collaboration across geographically dispersed teams, seamless integration with IoT and AI analytics, and rapid access to large-scale computational resources, which is particularly valuable for industries such as smart manufacturing, automotive, and energy.

Enterprise Size Insights

The large enterprise segment dominated the market, accounting for the largest revenue share in 2025, driven by the need for operational efficiency, predictive maintenance, and informed strategic decision-making across complex, asset-intensive operations. Large organizations, particularly in manufacturing, energy, automotive, and aerospace, are adopting digital twins to simulate processes, monitor assets in real time, and optimize supply chains, which helps reduce downtime and operational costs. Their substantial IT budgets and focus on digital transformation enable investments in advanced analytics, AI integration, and IoT-enabled digital twin solutions, further accelerating adoption.

The small and medium enterprises (SMEs) segment is expected to grow at a significant CAGR during the forecast period due to the increasing availability of affordable, cloud-based, and scalable digital twin solutions that lower the barrier to entry for smaller organizations. SMEs are adopting digital twins to optimize production processes, reduce operational costs, and enhance product design and quality without the need for extensive IT infrastructure.

Application Insights

The product design & development segment dominated the market, accounting for the largest revenue share in 2025, as organizations increasingly leverage digital twins to accelerate innovation, reduce time-to-market, and enhance product quality. By creating virtual replicas of products, companies can simulate performance, test design variations, and identify potential flaws before physical production, thereby minimizing the cost of prototypes and rework. Industries such as automotive, aerospace, and consumer electronics are driving adoption due to the need for complex, high-precision products and the integration of IoT and AI for predictive insights.

The business optimization segment is expected to grow at a significant CAGR during the forecast period as organizations increasingly rely on digital twins to enhance operational efficiency, reduce costs, and improve decision-making across complex processes. By providing a virtual representation of entire business operations, digital twins enable real-time monitoring, scenario simulation, and predictive analytics, helping companies identify bottlenecks, optimize resource allocation, and streamline workflows.

End Use Insights

The automotive & transport segment dominated the market, accounting for the largest revenue share in 2025, driven by the industry’s focus on enhancing vehicle design, safety, performance, and operational efficiency. Automotive manufacturers and transportation operators are leveraging digital twins to simulate vehicle dynamics, test new technologies, and optimize production lines, reducing development time and costs. The rise of electric vehicles (EVs), autonomous driving technologies, and connected mobility solutions further fuels adoption, as digital twins enable real-time monitoring, predictive maintenance, and data-driven decision-making.

The telecommunication segment is expected to grow at a significant CAGR over the forecast period as telecom operators adopt digital twins to optimize network planning, deployment, and maintenance while enhancing service quality. By creating virtual models of network infrastructure, including towers, fiber optics, and 5G equipment, companies can simulate network performance, predict outages, and efficiently manage capacity and traffic loads. The rapid expansion of 5G networks, IoT connectivity, and increasing demand for low-latency, high-bandwidth services are key drivers, enabling operators to reduce downtime, improve customer experience, and lower operational costs.

Regional Insights

North America dominated the global market with the largest revenue share of 31.3% in 2025, driven by extensive adoption of Industry 4.0 technologies across manufacturing, aerospace, and automotive sectors. Strong R&D investments, the presence of leading technology providers, and government initiatives promoting smart manufacturing and digital infrastructure are accelerating the deployment of digital twin solutions for predictive maintenance, operational efficiency, and innovation.

U.S. Digital Twin Market Trends

The digital twin market in the U.S. is expected to grow significantly at a CAGR of 27.5% from 2026 to 2033, due to rapid integration of IoT, AI, and cloud computing into industrial processes is a key growth driver. Enterprises are leveraging digital twins to optimize complex supply chains, enhance product lifecycle management, and enable real-time data analytics, supported by a mature IT ecosystem and high technology adoption rates.

Europe Digital Twin Market Trends

The digital twin market in Europe is expected to experience considerable growth from 2026 to 2033, driven by regulatory frameworks that emphasize sustainability and energy efficiency, particularly in the manufacturing and energy sectors. Companies are deploying digital twins to monitor emissions, optimize energy usage, and ensure compliance with EU environmental standards, driving demand for simulation and predictive tools.

The UK digital twin market is expected to grow rapidly in the coming years, owing to smart infrastructure initiatives and the push toward digital cities. Public and private sectors are utilizing digital twins for urban planning, transportation optimization, and infrastructure management, enabling improved decision-making and cost saving.

The Germany digital twin market held a substantial market share in 2025 due to the strong automotive and industrial manufacturing base. Digital twins are being implemented for precision engineering, advanced factory automation, and predictive maintenance, helping German companies maintain global competitiveness and operational excellence.

Asia Pacific Digital Twin Market Trends

Asia Pacific digital twin held a significant share in the global market in 2025, due to rapid industrialization, increasing urbanization, and the adoption of smart manufacturing technologies in countries like South Korea, Singapore, and India. The focus on cost optimization, productivity enhancement, and modernization of legacy industrial processes is boosting demand.

The Japan digital twin market is expected to grow rapidly in the coming years, driven by a focus on robotics, automation, and high-tech manufacturing. Digital twins are extensively used for quality improvement, process optimization, and reducing production downtime, aligning with Japan’s emphasis on precision, efficiency, and advanced engineering solutions.

The China digital twin market held a substantial market share in 2025, due to large-scale investments in smart factories, industrial IoT, and national initiatives for digital transformation such as Made in China 2025. The market benefits from rapid adoption of AI-driven predictive analytics, real-time monitoring, and automation in manufacturing, energy, and transportation sectors.

Key Digital Twin Company Insights

Key players operating in the digital twin industry are ABB, ANSYS, Inc., AVEVA Group Limited, Bentley Systems, Incorporated, Siemens, IBM Corporation, Microsoft, and Rockwell Automation. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In November 2025, Rockwell Automation and Eplan, an India-based software and service solutions provider, launched a digital twin-driven integration that links Eplan’s schematic design tools with Rockwell’s Emulate3D software. This allows engineers to virtually model, test, and optimize systems like industrial robots, control panels, and automated conveyors before hardware construction, streamlining workflows, reducing engineering time, and improving simulation accuracy.

-

In October 2025, ABB introduced its next-generation excitation system, UNITROL 8000, designed to enhance power generation reliability amid rising energy demand and increased renewable integration. The system combines real-time excitation control, embedded digital twin capabilities, built-in data analytics, and cybersecurity by design. With support for both legacy and modern communication protocols, UNITROL 8000 ensures seamless integration with existing control systems, while its modular design allows customization to site-specific conditions and future upgrades without operational disruption.

-

In June 2025, Siemens and Arm launched the PAVE360 digital twin, giving developers cloud access to virtual models of Arm automotive IP, including the new Zena CSS, ahead of silicon availability. It enables testing of AI-driven, complex vehicle workloads and helps identify system integration issues before hardware and software deployment.

Key Digital Twin Companies:

The following are the leading companies in the digital twin market. These companies collectively hold the largest market share and dictate industry trends.

- ABB

- Amazon Web Services, Inc.

- ANSYS, Inc.

- Autodesk Inc.

- AVEVA Group Limited

- Bentley Systems, Incorporated

- Dassault Systèmes

- General Electric Company

- Hexagon AB

- IBM Corporation

- Microsoft

- PTC

- Robert Bosch GmbH

- Rockwell Automation

- SAP

- Siemens

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: General Electric Company; Dassault Systèmes; Siemens; IBM Corporation; Microsoft

- Mature players focus on integrated digital twin platforms combining design, simulation, IoT, analytics, and lifecycle management.

- They invest in R&D, cloud integration, and industry partnerships to expand adoption across manufacturing, energy, automotive, and smart infrastructure.

- Mature players gain advantage through well-established digital engineering platforms, large installed industrial bases, and strong global ecosystems.

- Their solutions combine design tools, IoT platforms, and analytics engines to model products, production systems, and operational assets simultaneously.

- Challenges related to complex implementation processes and high deployment costs.

- Large platforms may require extensive system integration, specialized expertise, and significant infrastructure investment, which can limit adoption among small and mid-sized enterprises.

Emerging Players: Twinsity; Geminum; ProtoTwin; Thingspine; Twyn; Urbim; AIOTEL; Hopara; Treedis; ViManPro

- Emerging players focus on industry-specific digital twin solutions tailored to sectors such as infrastructure, energy, utilities, and industrial manufacturing.

- Strategies emphasize integrating operational data from sensors, control systems, and enterprise platforms to create digital replicas.

- Emerging players gain an advantage by delivering specialized digital twin capabilities for targeted industries.

- For example, some focus on infrastructure and smart city modeling, while others emphasize industrial automation, energy management, or enterprise data integration.

- Limitations related to smaller global ecosystems and lower brand visibility compared to established providers.

- Scaling deployments across multiple industries or global markets can be challenging without extensive partner networks and enterprise integration capabilities.

Digital Twin Market Report Scope

Report Attribute

Details

Market size in 2025

USD 35.8 billion

Estimated market size in 2026

USD 49.47 billion

Projected market size by 2033

USD 328.51 billion

Growth rate

CAGR of 31.1% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report enterprise size

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Solution, Deployment, Enterprise Size, Application, End Use, and Region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

ABB; Amazon Web Services, Inc.; ANSYS, Inc.; Autodesk Inc.; AVEVA Group Limited; Bentley Systems, Incorporated; Dassault Systèmes; General Electric Company; Hexagon AB; IBM Corporation; Microsoft; PTC; Robert Bosch GmbH; Rockwell Automation; SAP; Siemens

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Digital Twin Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the digital twin market report based on solution, deployment, enterprise size, application, end use, and region.

-

Solution Outlook (Revenue, USD Billion, 2021 - 2033)

-

Component

-

Process

-

System

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud

-

On-premise

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

Small and Medium Enterprises (SMEs)

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Product Design & Development

-

Predictive Maintenance

-

Business Optimization

-

Others

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Manufacturing

-

Agriculture

-

Automotive & Transport

-

Energy & Utilities

-

Healthcare & Life Sciences

-

Residential & Commercial

-

Retail & Consumer Goods

-

Aerospace

-

Telecommunication

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Global Digital Twin Market Opportunity Assessment for an Industrial Automation Technology Provider

Assessment of enterprise demand for digital twin solutions across manufacturing, energy, automotive, and industrial operations

Identification of operational challenges, including unplanned downtime, process inefficiencies, and limited real-time asset visibility

Analysis of digital transformation readiness, data infrastructure maturity, and simulation adoption across target customer groups

Identified high-potential application areas for digital twin deployment across asset-intensive industries

Supported development of industry-specific solution positioning based on operational pain points

Enabled prioritization of customer segments with strong digital adoption potential

Smart Infrastructure & Asset Performance Digital Twin Strategy for an Engineering Solutions Company

Analysis of infrastructure management challenges related to asset monitoring, maintenance planning, energy optimization, and lifecycle visibility

Assessment of digital twin use cases in smart buildings, transportation networks, utilities, and urban infrastructure projects

Evaluation of integration requirements between IoT sensors, operational systems, and visualization platforms

Identified long-term infrastructure modernization opportunities through predictive monitoring solutions

Supported expansion into sustainability-driven asset management applications

Enabled creation of customized solutions for infrastructure owners and facility operators

Digital Twin Platform Commercialization & Product Feasibility Assessment for a Software Developer

Evaluation of enterprise demand for virtual simulation, remote monitoring, and predictive analytics capabilities

Analysis of customer expectations around real-time decision support, operational transparency, and process optimization

Identification of adoption barriers, including integration complexity, data interoperability, and implementation costs

Supported product roadmap development aligned with enterprise operational priorities

Identified recurring revenue opportunities through software subscription and managed service models

Enabled go-to-market strategy focused on solving real-world operational and maintenance challenges

Frequently Asked Questions About This Report

North America dominated the global market with the largest revenue share of 31.3% in 2025, driven by extensive adoption of Industry 4.0 technologies across manufacturing, aerospace, and automotive sectors.

The automotive and transport segment held the largest revenue share in 2025. The high market share is driven by by the industry’s focus on enhancing vehicle design, safety, performance, and operational efficiency. Automotive manufacturers and transportation operators are leveraging digital twins to simulate vehicle dynamics, test new technologies, and optimize production lines, reducing development time and costs.

Key players include ABB; Amazon Web Enterprise size, Inc.; ANSYS, Inc.; Autodesk Inc.; AVEVA Group Limited; Bentley Systems, Incorporated; Dassault Systèmes; General Electric Company; Hexagon AB; IBM Corporation; Microsoft; PTC; Robert Bosch GmbH; Rockwell Automation; SAP; Siemens.

Asia Pacific is the fastest-growing region over the forecast period.

Key factors include rapid adoption of Industry 4.0 practices, rising demand for predictive maintenance across industries, and the growing need for real-time monitoring of assets to reduce operational costs and downtime.

The system segment led with a 40.9% revenue share in 2025, while process is the fastest-growing solution.

The on-premise segment held the largest revenue share in 2025, while cloud is the fastest-growing deployment.

Large enterprise segment dominated the market and accounted for a highest revenue share in 2025.

The global digital twin market size was valued at USD 35.8 billion in 2025 and is estimated at USD 49.5 billion for 2026.

The global digital twin market is expected to grow at a CAGR of 31.1% from 2026 to 2033, reaching USD 328.5 billion by 2033.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.