- Home

- »

- Next Generation Technologies

- »

-

Enterprise Software Market Size, Growth Report, 2026-2033GVR Report cover

![Enterprise Software Market (2026 - 2033)Report]()

Enterprise Software Market (2026 - 2033)

Size, Share & Trends Analysis Report By Software (Business Intelligence Software, Content Management Software), By Deployment (On-premise, Cloud), By Enterprise Size, By End-use, By Region, And Segment Forecasts

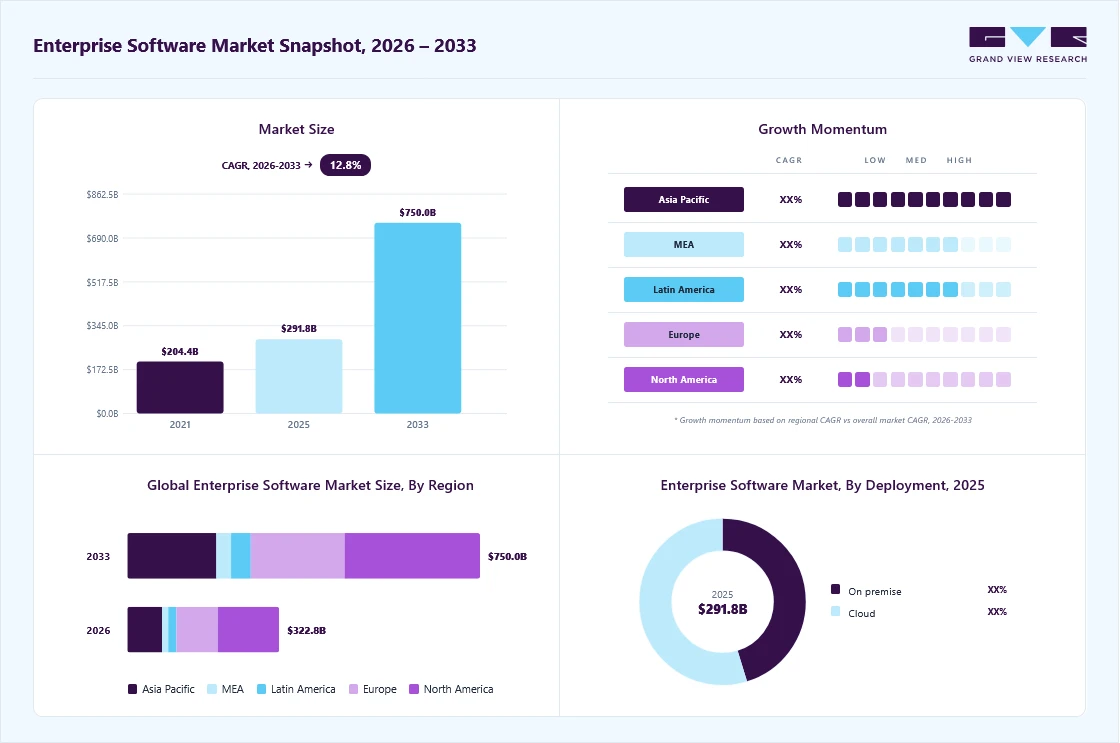

Market Size, 2025

$291.8BMarket Estimate, 2026

$322.8BMarket Forecast, 2033

$750.0BCAGR, 2026–2033

12.8%Enterprise Software Market Summary

The global enterprise software market size was valued at USD 291.8 billion in 2025 and is projected to grow from USD 322.8 billion in 2026 to USD 750.0 billion by 2033, at a CAGR of 12.8% from 2026 to 2033. North America dominated the global market, accounting for the largest revenue share of 40.7% in 2025. The application of enterprise software is rapidly growing among organizations owing to its advanced capabilities, including enterprise resource planning, human resource management, content management, document management, and business intelligence.

Key Market Trends & Insights

- By software: Enterprise resource planning (ERP) software segment held the largest revenue share of 23.2% in 2025.

- By deployment: Cloud segment held the largest revenue share in 2025.

- By enterprise size: SMEs segment is expected to grow at the fastest CAGR during the forecast period.

Regional Highlights

- Largest regional market: North America (40.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. enterprise software industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 291.8 Billion

- Estimated market size in 2026: USD 322.8 Billion

- Projected market size by 2033: USD 750.0 Billion

- CAGR (2026-2033): 12.8%

The software streamlines functions and tasks across an organization, enabling collaborative communication and data-driven decision-making. This shift aims to enhance overall operational efficiency across industries. In response, market players are recognizing the growing need for advanced enterprise resource planning (ERP), customer relationship management (CRM), and data analytics software, positioning themselves to meet this demand with innovative offerings. Enterprise software is widely utilized across various industries and sectors, including BFSI, healthcare, retail, manufacturing, government, and education. Organizations in these fields often manage vast databases containing critical information and face complex business processes, such as financial management, patient data updates, customer relationship management, official record documentation, and internal workflow management. As a result, businesses are increasingly demanding advanced software solutions.

")

Key industry trends such as Industry 4.0, digitization, modern manufacturing, robotics, and the rise of connected devices are driving the demand for advanced technology solutions across sectors like BFSI, manufacturing, healthcare, and government. Additionally, the growing shift toward hybrid work models has significantly boosted the adoption of enterprise software in industries such as healthcare, education, and retail. For example, in the healthcare sector, enterprise software solutions support critical functions such as hospital management, patient care, and electronic health record management. This expanding use of enterprise software across industries underscores its critical role in optimizing operations and enhancing efficiency in the evolving digital landscape.

Data safety and privacy are critical drivers in the enterprise software market, as organizations increasingly prioritize the protection of sensitive information and compliance with stringent regulations. With rising concerns over data breaches and cyberattacks, businesses across various sectors are turning to enterprise software solutions that offer robust security features, including encryption, multi-factor authentication, and advanced monitoring tools.

Regulatory frameworks such as GDPR, HIPAA, and other data protection laws have heightened the need for compliance-focused software, driving demand for solutions that ensure secure handling and storage of personal and financial data. This focus on data privacy has opened new opportunities for vendors offering specialized software that integrates strong security protocols while maintaining operational efficiency. The growing trend toward hybrid work environments has further underscored the importance of secure remote access, making data protection an essential factor in the continued growth of the enterprise software market.

Software Insights

The enterprise resource planning (ERP) software segment accounted for the largest market share of 23.2% in 2025, driven by the increasing need for integrated business management solutions across finance, supply chain, human resources, and operations. Organizations are rapidly adopting ERP systems to streamline workflows, improve real-time data visibility, and enhance decision-making capabilities. Key drivers include the growing shift toward cloud-based ERP solutions, rising demand for automation and AI-enabled analytics, and the need for regulatory compliance and operational efficiency across industries. In addition, the expansion of digital transformation initiatives and the integration of advanced technologies such as machine learning and IoT are further accelerating ERP adoption.

The customer relationship management (CRM) software segment is expected to grow at the fastest CAGR during the forecast period. The enterprise software market growth is driven by the increasing focus on customer-centric strategies and personalized engagement across industries. Organizations are rapidly adopting CRM platforms to enhance sales automation, improve customer insights through data analytics, and streamline marketing and service operations. The integration of artificial intelligence, cloud deployment models, and omnichannel communication capabilities is further accelerating adoption, enabling businesses to deliver real-time, customized experiences.

Deployment Insights

The cloud segment accounted for the largest market share in 2025. The growth is driven by the increasing shift toward scalable, flexible, and cost-efficient IT infrastructure. Organizations are rapidly adopting cloud-based deployment models to enable remote access, support real-time collaboration, and reduce upfront capital expenditures associated with on-premises systems. Key drivers include the growing demand for SaaS-based enterprise applications, rising adoption of AI and data analytics in cloud environments, and the need for seamless integration across business functions. Additionally, enhanced security, automatic updates, and faster deployment cycles are further accelerating cloud adoption.

The on-premise segment is expected to grow at a significant CAGR during the forecast period. The enterprise software market growth is driven by the increasing demand for enhanced data security, regulatory compliance, and greater control over IT infrastructure. Large enterprises and organizations operating in highly regulated industries such as banking, government, and healthcare continue to prefer on-premise deployment to safeguard sensitive data and ensure compliance with strict data protection laws. Additionally, the need for customization, legacy system integration, and low-latency performance is supporting adoption.

Enterprise Size Insights

The large enterprise segment accounted for the largest market share in 2025. Substantial IT budgets, complex operational requirements, and early adoption of advanced technologies such as cloud computing, artificial intelligence, and data analytics drive the market growth. These organizations require scalable and integrated enterprise software solutions to manage large volumes of data, streamline cross-functional operations, and enhance decision-making capabilities. In addition, the increasing focus on digital transformation, cybersecurity, and global business expansion further supports adoption. For instance, large enterprises widely deploy solutions like SAP S/4HANA by SAP SE to integrate business processes, improve operational efficiency, and enable real-time insights across global operations.

The SMEs segment is expected to grow at the fastest CAGR over the forecast period. Small and medium-sized enterprises are rapidly embracing digital tools to enhance operational efficiency, improve customer engagement, and remain competitive in a dynamic business environment. Key drivers include the availability of subscription-based SaaS models, reduced upfront infrastructure costs, and growing awareness of data-driven decision-making. Besides, government initiatives supporting digitalization and the rise of remote work are further accelerating adoption among SMEs.

End Use Insights

The IT & Telecom segment accounted for the largest revenue market share in 2025. The market growth is driven by the sector’s high reliance on advanced digital infrastructure, data management, and continuous innovation. Companies in this segment extensively adopt enterprise software solutions to manage complex networks, optimize operations, and enhance customer service delivery. Key drivers include the rapid deployment of 5G networks, increasing demand for cloud computing, and the need for real-time data analytics and cybersecurity solutions. In addition, the growing adoption of AI-driven automation and network management tools is further supporting market growth.

The healthcare segment is expected to grow rapidly during the forecast period. The increasing adoption of digital health solutions, electronic health records (EHRs), and data-driven patient care systems drives the market growth. Healthcare organizations are rapidly implementing enterprise software to improve operational efficiency, enhance patient outcomes, and ensure regulatory compliance. Key drivers include the rising demand for telemedicine, the growing volume of healthcare data, and the need for secure and interoperable systems. In addition, the integration of AI and analytics for diagnostics, patient management, and predictive care is further accelerating adoption.

Regional Insights

The enterprise software industry in North America held the largest market share of 40.7% in 2025. The promising pace of technological advancements in the region, coupled with the heightened adoption of cloud-based enterprise solutions among organizations, is expected to drive the demand for enterprise software. Organizations in the region are compelled to adopt enterprise software to enhance their operational capabilities, improve decision-making, and optimize efficiency. This scenario is expected to drive the growth of the North America market.

U.S. Enterprise Software Market Trends

The enterprise software industry in theU.S. is growing at a considerable CAGR from 2026 to 2033. The fast-paced innovations introduced by key players in the market are expected to strengthen the growth. Besides, the rising applications of enterprise software in industries such as healthcare and the BFSI sector in the U.S. are also expected to support market growth.

Asia Pacific Enterprise Software Market Trends

The enterprise software industry in the Asia Pacific is growing at a significant CAGR from 2026 to 2033. The growth can be attributed to the implementation of advanced technologies such as AI, ML, IoT, and robotics in business processes across industries such as manufacturing, retail, BFSI, and healthcare. Enterprise software, including enterprise resource planning, human resource management, customer relationship management, and business intelligence, empowers small and medium business enterprises to become self-reliant, make data-driven decisions, optimize resources, and reduce operational costs. Furthermore, the fierce competition between companies and organizations in the region is expected to bode well for market growth as it is likely to result in more software providers offering innovative solutions at competitive prices.

The China enterprise software industry is growing owing to the digitization and availability of large manufacturing businesses, which are driving the growth of the regional market. The government's support initiatives to improve the digital ecosystem also attract key players to the market.

Europe Enterprise Software Market Trends

The enterprise software industry in Europe is growing at a significant CAGR of 11.7% from 2026 to 2033. In Europe, organizations are adopting enterprise software to make the transaction process seamless and automated. Technological advancements and innovations enable European businesses to make data-driven decisions by integrating insights from various business processes, including sales, marketing, finance, human resource, and customer support teams.

The UK enterprise software industry is expected to grow considerably over the forecast period, owing to the growing emphasis on adopting advanced software solutions, helping organizations become more agile, customer-centric, and efficient. Furthermore, the UK market has seen significant technological advancements in recent years, driven by the increasing demand for more effective and efficient enterprise software such as ERP, HCM, and CRM, among others.

Key Enterprise Software Company Insights

Some of the key players operating in the market include Accenture, Broadcom Inc., Cisco Systems Inc., Deltek, Inc., Epicor Software Corporation, Hewlett Packard Enterprise, IBM Corporation, and Infor, among others.

-

Accenture plc provides technology solutions and professional services in areas such as network management and consulting. It operates through five business lines, namely Accenture Technology, Accenture Operations, Accenture Digital, Accenture Strategy, and Accenture Consulting. The company offers business process, infrastructure, security, and cloud services under the Accenture Operations business. It manages 51 subsidiaries and affiliates across the globe. Moreover, it serves industries and sectors such as automotive, banking, chemicals, communication & technology, energy, healthcare, consumer goods, life sciences, insurance, retail, travel, and natural resources.

-

Cisco Systems, Inc. specializes in networking hardware, software, and services. The company has seven business segments, namely Networking, Internet of Things (IoT), Mobility & Wireless, Security, Collaboration, Datacenters, and Cloud. It serves industries and sectors such as energy, finance, government, healthcare, manufacturing, retail, sports & entertainment, and transportation.

Key Enterprise Software Companies:

The following key companies have been profiled for this study on the enterprise software market

- Accenture

- Broadcom Inc. (CA Technologies, Inc.)

- Cisco Systems Inc.

- Deltek, Inc.

- Epicor Software Corporation

- Hewlett Packard Enterprise

- IBM Corporation

- Infor

- Microsoft Corporation

- Oracle Corporation

- Salesforce.com, Inc.

- SAP SE

- SYSPRO

- TIBCO Software Inc.

- VMware, Inc.

Recent Developments

-

In February 2026, Accenture acquired advanced AI technology from Avanseus to enhance its AI and machine learning capabilities for telecom clients. This development is closely linked to the enterprise software market as it strengthens Accenture’s portfolio of AI-driven enterprise solutions, enabling organizations to adopt autonomous network operations, improve predictive analytics, and optimize large-scale business processes.

-

In October 2025, IBM Corporation announced the acquisition of Cognitus, a leading SAP S/4HANA services provider, to strengthen its AI-driven enterprise application and consulting capabilities. The acquisition enhances IBM’s ability to deliver large-scale SAP transformations by integrating Cognitus’ industry-specific, AI-powered software assets and deep domain expertise. This development is significant for the enterprise software industry as it accelerates cloud ERP adoption, improves data migration and automation capabilities, and supports enterprises in achieving greater operational efficiency and digital transformation across complex and regulated industries.

-

In May 2025, IBM Corporation and Oracle Corporation expanded their strategic partnership to integrate IBM’s watsonx AI portfolio with Oracle Cloud Infrastructure, enabling enterprises to deploy agentic AI and hybrid cloud solutions to enhance productivity and streamline multi-system business processes.

Enterprise Software Market Report Scope

Report Attribute

Details

Market size in 2025

USD 291.8 billion

Estimated Market size in 2026

USD 322.8 billion

Projected Market size by 2033

USD 750.0 billion

Growth rate

CAGR of 12.8% from 2026 to 2033

Base year

2025

Historic data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share, competitive landscape, growth factors, and trends

Segments covered

Software, deployment, enterprise size, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; South Korea; Australia; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Accenture; Broadcom Inc. (CA Technologies, Inc.); Cisco Systems Inc.; Deltek, Inc.; Epicor Software Corporation; Hewlett Packard Enterprise; IBM Corporation; Infor; Microsoft Corporation; Oracle Corporation; Salesforce.com, Inc.; SAP SE; SYSPRO; TIBCO Software Inc.; VMware, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Enterprise Software Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends from 2021 to 2033 in each of the sub-segments. For this study, Grand View Research has segmented the global enterprise software market report based on software, deployment, enterprise size, end use, and region:

-

Software Outlook (Revenue, USD Billion, 2021 - 2033)

-

Enterprise Resource Planning (ERP) Software

-

Business Intelligence Software

-

Content Management Software

-

Supply Chain Management Software

-

Customer Relationship Management Software

-

Cybersecurity Software

-

Others

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-premise

-

Cloud

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

SMEs

-

Large Enterprises

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Retail

-

Healthcare

-

IT & Telecom

-

Government & Education

-

Manufacturing

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The increasing preference for automated and integrated solutions is driving the growth of the enterprise software market. As more organizations seek streamlined, reliable software to reduce reliance on human resources, automate routine tasks, and minimize manual errors, the demand for enterprise software solutions continues to rise. This shift is aimed at enhancing overall operational efficiency across industries.

The global enterprise software market size was valued at USD 291.8 billion in 2025 and is estimated at USD 322.8 billion for 2026.

The global enterprise software market is expected to grow at a CAGR of 12.8% from 2026 to 2033, reaching USD 750.0 billion by 2033.

The enterprise resource planning (ERP) software segment accounted for the largest market share of over 23.2% in 2025. Enterprise Resource Planning (ERP) software is an integrated and comprehensive suite of applications that streamline and optimize critical business processes within organizations.

North America dominated with a 40.7% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The cloud segment held the largest revenue share in 2025.

The large enterprise segment held the largest revenue share in 2025, while SMEs is the fastest-growing segment.

IT & telecom segment dominated the market and accounted for the largest share in 2025.

Key players include Accenture; Broadcom Inc. (CA Technologies, Inc.); Cisco Systems Inc.; Deltek, Inc.; Epicor Software Corporation; Hewlett Packard Enterprise; IBM Corporation; Infor; Microsoft Corporation; Oracle Corporation; Salesforce.com, Inc.; SAP SE; SYSPRO; TIBCO Software Inc.; VMware, Inc.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.